Bank of England

View:

June 30, 2026

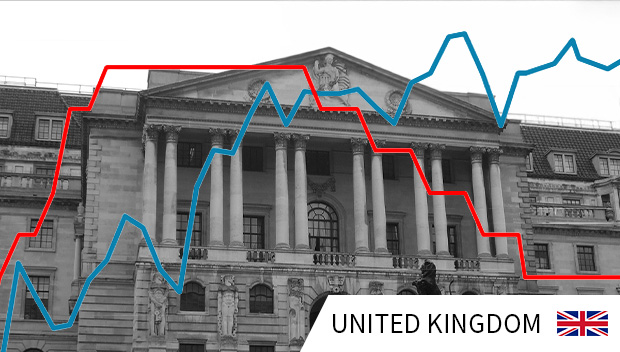

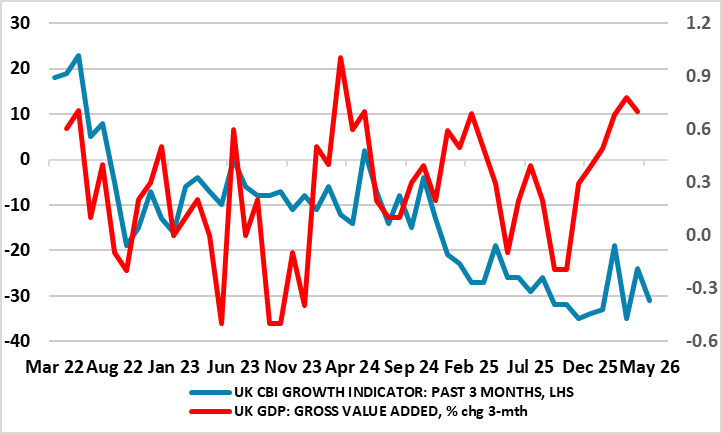

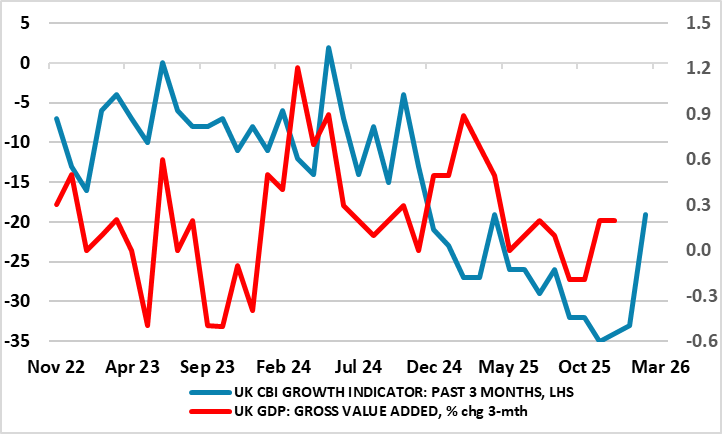

UK GDP Outlook Update – Still Fragile With Surveys Negative

June 30, 2026 4:13 PM UTC

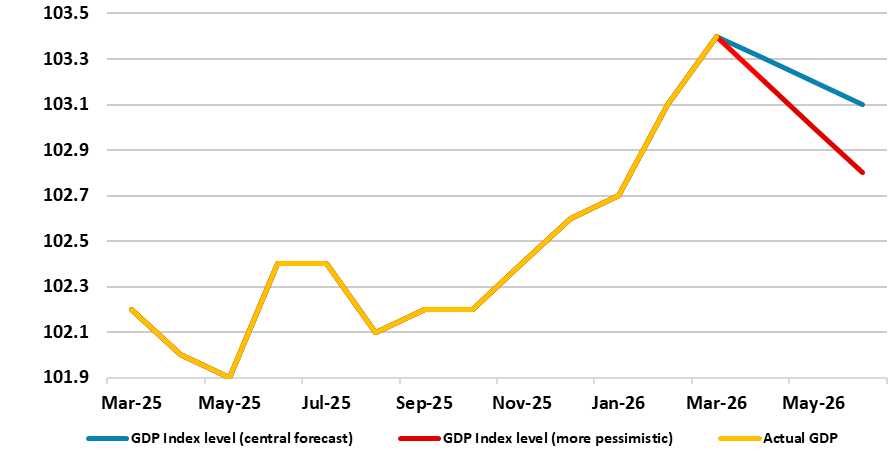

It is the relative norm for an economy to be offering disparate signals at any one juncture, if not actual conflicting ones. This is certainly the case in the UK currently, where upbeat Q1 GDP data of 0.6% q/q have been, confirmed and notably by a perkier consumer. Such shots of real growth ar

June 23, 2026

DM Rates Outlook: Tightening or Easing?

June 23, 2026 8:15 AM UTC

· With the U.S./Iran interim agreement likely to hold and energy prices softening, our projected consumer slowdown will likely tilt the Fed not to hike in H2 2026 and to actually ease by 50bps in 2027, with 25bps moves in both Q2 and Q3. With 2yr yields consistent with a hike, the tra

DM ex U.S. EZ Outlook (Japan and Western Europe): Navigating the Post Iran War Period?

June 23, 2026 7:43 AM UTC

· We have revised 2026 Japan GDP only slightly lower to 0.8% as wage growth is solidly above 3%, which will support consumption for the rest of 2026/27. The extension of energy stimulus will cap headline inflation for Q2/Q3 2026. For the BOJ, despite hawkish forward guidance, the 1% r

June 18, 2026

BOE: Gang of 6 and Steady 2026 Rates

June 18, 2026 11:27 AM UTC

Though Megan Greene joined Huw Pill in calling for a one off 25bps risk management hike, 6 MPC members feel that disinflation is showing through and a soft economy and labor market warrants waiting to see energy prices and potential 2nd round effects. This gang of 6 also feels that markets have ti

June 17, 2026

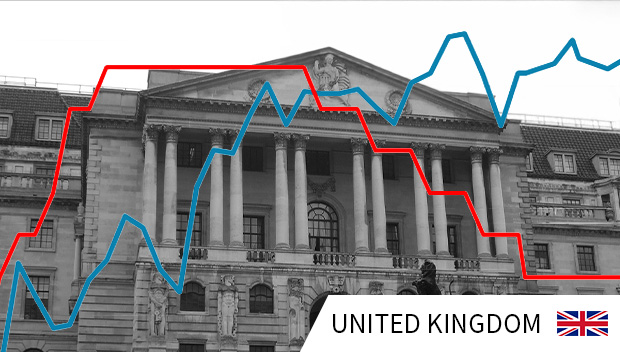

UK CPI Review: Inflation Peaking?

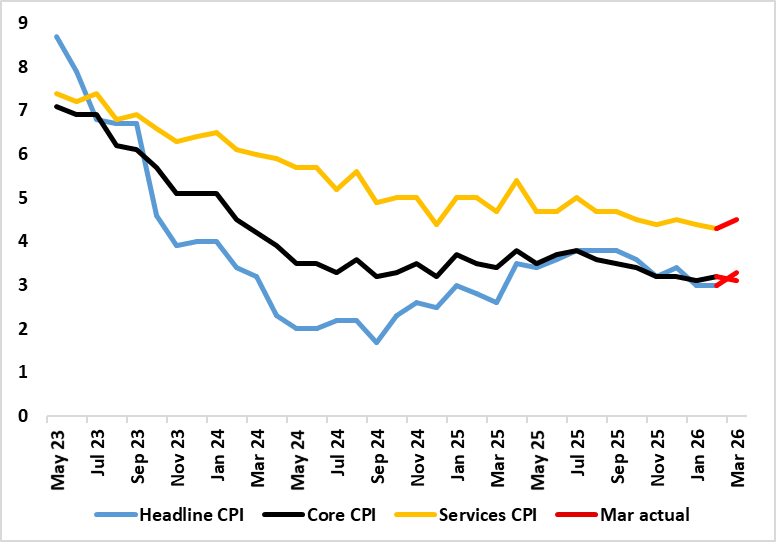

June 17, 2026 7:40 AM UTC

What have been energy induced price rises are starting to ease and may do so further In June before the OFGEM induced price rise hits July numbers. But a less worrying picture emerges in the latest (ie May) CPI and even PPI data. Indeed, once again, actual CPI have offered a more benign picture

June 12, 2026

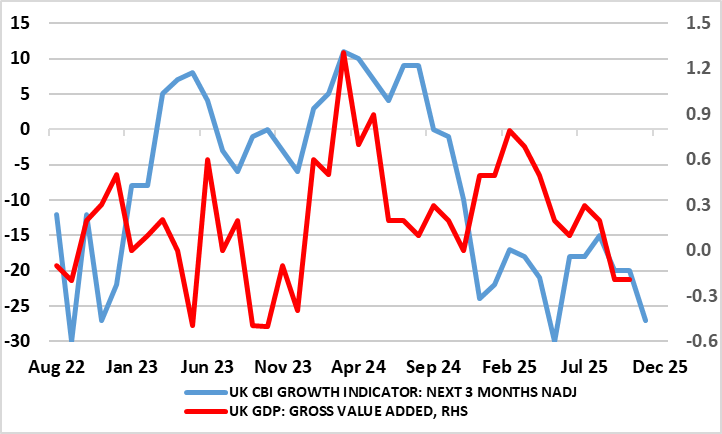

UK GDP Review: GDP Upside Surprises Persist?

June 12, 2026 6:56 AM UTC

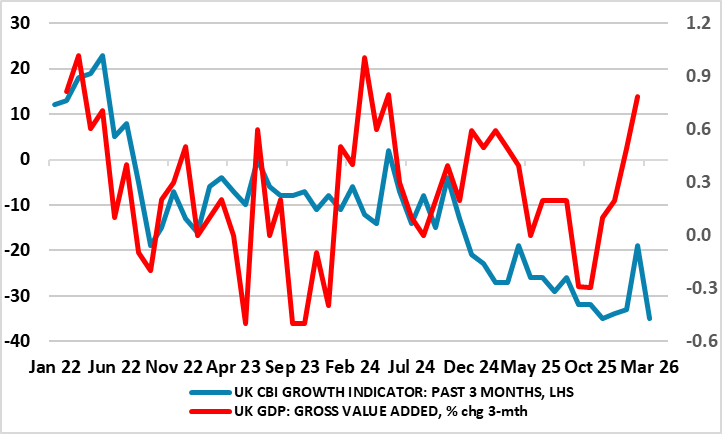

Perhaps it is a supreme irony that just as business surveys suggest clear weakness, if not fresh contraction, the actual real economy has surprised on the upside, even now into the second month after the Middle East conflict started. Indeed, and in perspective, official GDP data suggest that since

June 11, 2026

BoE Preview (Jun 18): Splits to Widen, But Stable Policy Outlook Intact

June 11, 2026 10:26 AM UTC

Not only this month, but we see the BoE being on hold for the rest of the year with rate cuts then resuming through 2027. Although markets are pricing just over two hikes from the current 3.75% with a 50%-plus probability of the first being delivered at the July 30 MPC meeting, our view is hardly

June 09, 2026

UK CPI Preview (Jun 17): Inflation Peaking?

June 9, 2026 9:37 AM UTC

What have been energy induced price rises are now very evident, even more so in some aspects of the latest PPI data. Regardless, actual CPI have offered a more benign picture both in terms fo headline and underlying trends. Indeed, having seen headline CPI jump to 3.3% in March and where service

June 04, 2026

UK GDP Preview (Jun 12): GDP Upside Surprises To Reverse?

June 4, 2026 9:49 AM UTC

Perhaps it is a supreme irony that just as business surveys suggest clear weakness, if not fresh contraction, the actual real economy has surprised on the upside, even in the first month after the Middle East conflict. Indeed, and in perspective, official GDP data suggest that since Labour took of

May 20, 2026

UK CPI Review: Inflation Falls Broadly But A Calm Before the Storm?

May 20, 2026 6:42 AM UTC

What are energy induced price rises are now very evident, even more so in the latest PPI data very much contrasting with the more benign picture in April’s more closely watched CPI figures. Thus, having seen headline CPI jump to 3.3% in March and where services rose to 4.5% on the back if what may

May 19, 2026

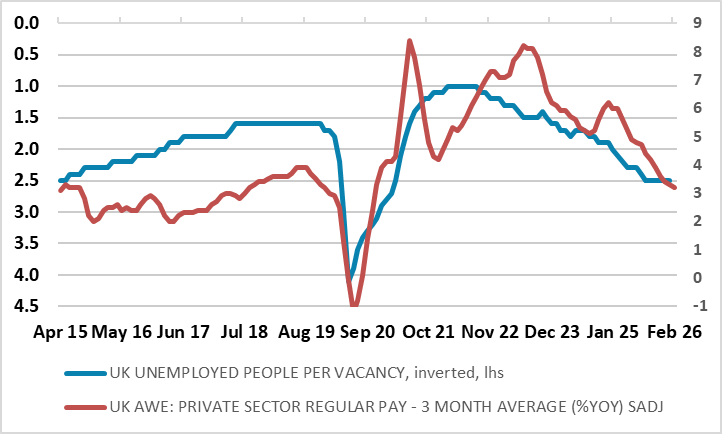

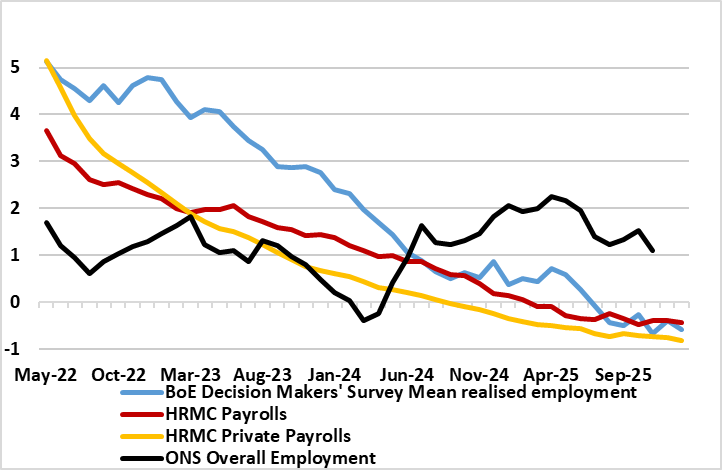

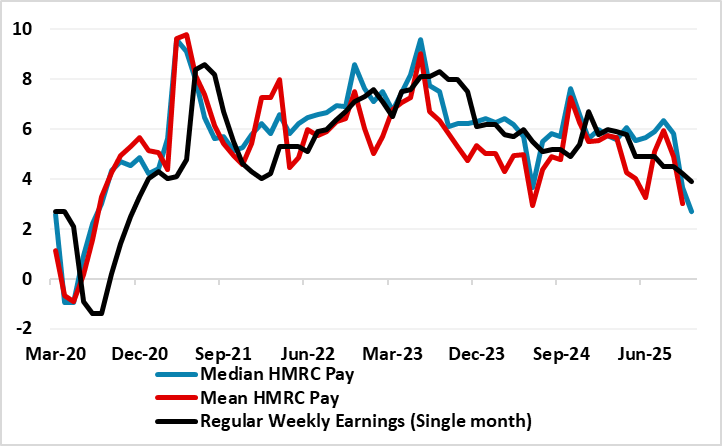

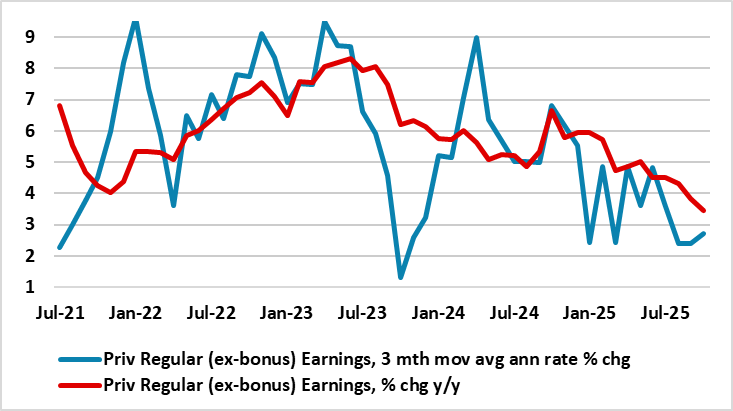

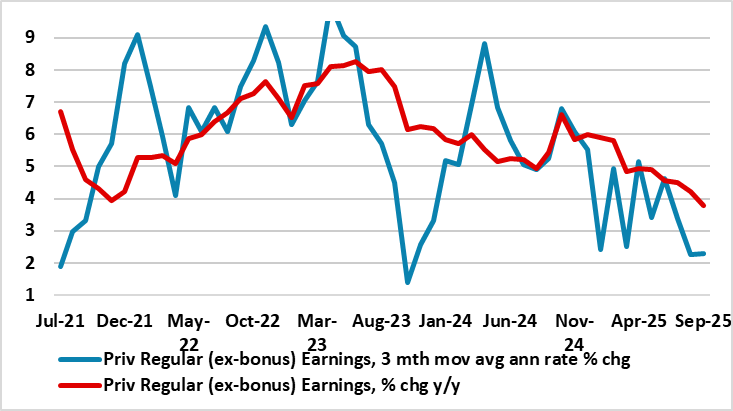

UK Labor Market: Core Wage Pressures hit New Cycle -Low as Jobs Growth into Sharp Reverse

May 19, 2026 6:56 AM UTC

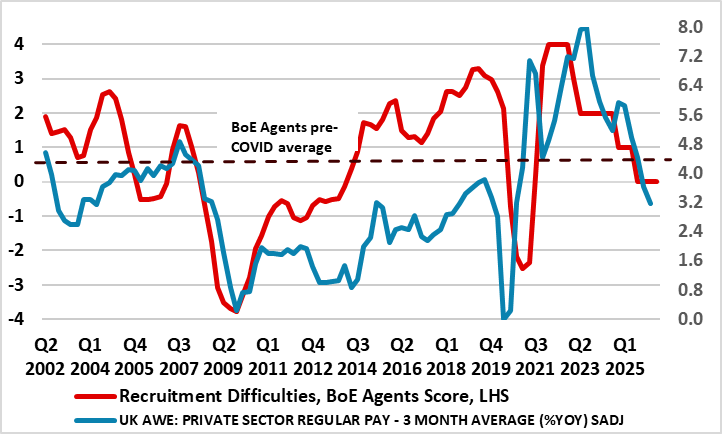

Even more clearly, there are further signs that the labor market is haemorrhaging jobs both clearly and broadly with fresh falls in the more authoritative measure of jobs covering payrolls. Indeed, private sector payrolls are still falling, down over 0.8 ppt in y/y terms with the m/m drop the larg

May 14, 2026

UK Politics – A Laboured Labour Election Ahead?

May 14, 2026 12:55 PM UTC

It is somewhat ironic that as markets (particularly gilts) fret over a shift to the left causing less fiscal prudency, it is actually the centre of the Labour party that is fermenting the most uncertainty. (Now Ex) Secretary Streeting has yet to make a formal bid to challenge PM Starmer for the le

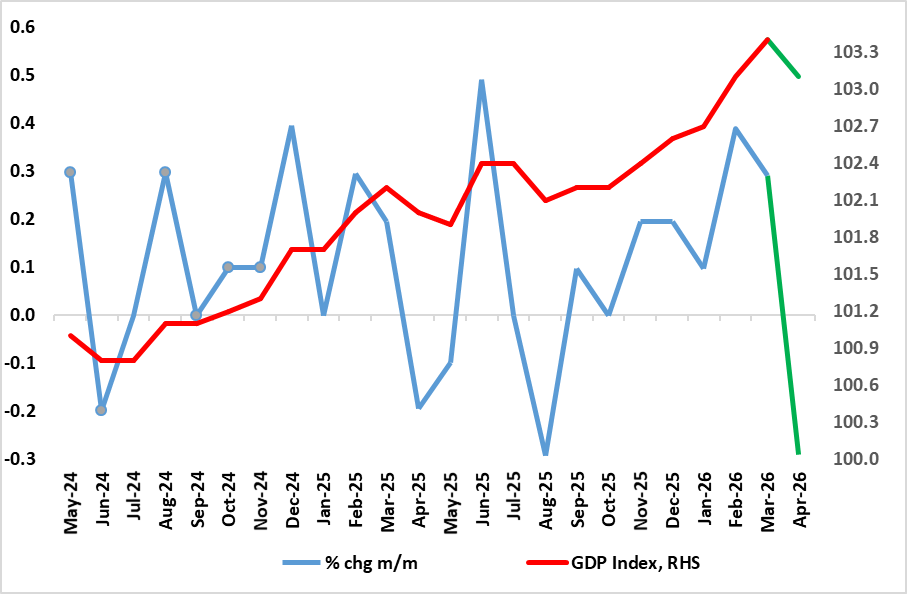

UK GDP Review: GDP Upside Surprises Continue, Correction Due or Fresh Trend?

May 14, 2026 6:59 AM UTC

Perhaps it is a supreme irony that just as the Labour government tears itself apart after disastrous election results last week, the actual real economy continues to surprise on the upside. Notably, since taking office in July 2024, the economy has grown a cumulative 2%-plus, ie over 1% per year.?

May 12, 2026

UK CPI Preview (May 20): Inflation Sedate For Now But Wages Still on the Wane?

May 12, 2026 12:05 PM UTC

What are energy induced price rises are now very evident, most notably in PPI data as well as the more closely watched CPI figures. Thus after a stable 3.0% (a 10-mth low) February’s headline – matching the consensus, headline CPI jumped to 3.3% in March. Services, however, rose from 4.3% a fo

May 05, 2026

UK GDP Preview (May 14): March GDP Drop Expected, Correction or Fresh Trend?

May 5, 2026 10:16 AM UTC

Before the outbreak of the Iran War there was already a split within the MPC about the policy outlook and that such divisions may have been accentuated by the much stronger than expected February GDP update which showed a m/m rise of 0.5%, the strongest in 14 months. This is likely to have been ab

April 30, 2026

BoE Review: MPC Playing Its Cards Safely (For Now)?

April 30, 2026 12:29 PM UTC

Very clearly, the BoE kept rates on hold with the MPC last month and the same decision was both expected and delivered this time around but with only token fresh dissent, with Chief Economist Pill wanting an immediate hike from the current 3.75%. But splits were more evident in the individual MPC

April 29, 2026

UK Political Risk – Bad Things Come in Threes?

April 29, 2026 12:12 PM UTC

The biggest set of elections since the 2024 general election takes place on 7 May in the UK. Already, UK markets are fretting about the possible outcome, in particular that serious electoral damage to the Labour Party currently running the government could make it swing more to left and dilute fis

April 24, 2026

BoE Preview (Apr 30) Divided Again But Unmoved (For Now)?

April 24, 2026 9:34 AM UTC

Very clearly, the BoE kept rates on hold with the MPC unanimous last month and the same decision is expected this time around but with probable fresh dissent, with up to 2-3 members opting for an immediate hike. These splits will be even more evident in the individual MPC member statements (as exp

April 22, 2026

UK CPI Review: Inflation Being Fuelled But Wages Still on the Wane?

April 22, 2026 6:35 AM UTC

What are energy induced price rises are now very evident, most notably in PPI data as well as the more closely watched CPI figures. Thus after a stable 3.0% (a 10-mth low) February’s headline – matching the consensus, headline CPI jumped to 3.3% in March. Services, however, rose from 4.3% a fo

April 21, 2026

UK Labor Market: Lower Jobless Rates Misleading, as Wage Pressures hit New Cycle -Low

April 21, 2026 6:54 AM UTC

There are further signs that the labor market is haemorrhaging jobs both clearly and broadly with fresh falls in the more authoritative measure of jobs covering payrolls. Indeed, private sector payrolls are still falling, down over 0.5 ppt in y/y terms. Admittedly, headlines may be formed around

April 16, 2026

UK GDP Review (Apr 16): Fresh But Fleeting Momentum Before the War

April 16, 2026 7:10 AM UTC

Without the outbreak of the Iran War there was already a split within the MPC about the policy outlook and that such divisions may have been accentuated by this latest GDP update which showed a very much above consensus m/m rise of 0.5%, the strongest in 14 months. But of course, the conflict has ch

April 13, 2026

UK CPI Preview (Apr 22): Inflation Being Fuelled But Watch Financial Conditions?

April 13, 2026 2:39 PM UTC

The stormy weather inflation wise is now very evident, most notably in UK fuel prices surging. Thus after a stable 3.0% (a 10-mth low) February’s headline – matching both consensus and BoE projections we see it jumping to 3.5% in March. Services, however, may stay at 4.3% which was a four-year

April 09, 2026

UK GDP Preview (Apr 16): Moving Sideways Even Before Conflict?

April 9, 2026 8:01 AM UTC

Fresh downside surprises were the story from the January GDP numbers and we expect a similarly muted outcome for the looming February numbers. There were expectations that the economy would enjoy a further successive rise in January, thereby providing the best three-month showing in two years were

March 25, 2026

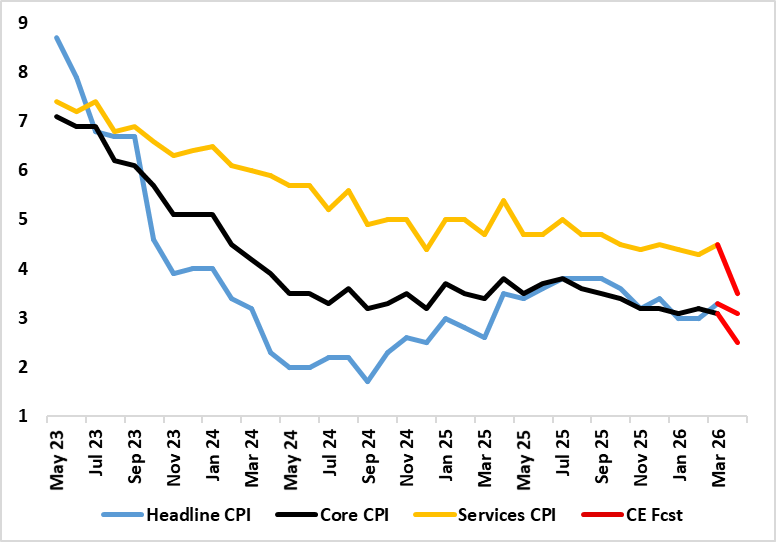

UK CPI Review: Goodbye to the Good Old Days?

March 25, 2026 7:33 AM UTC

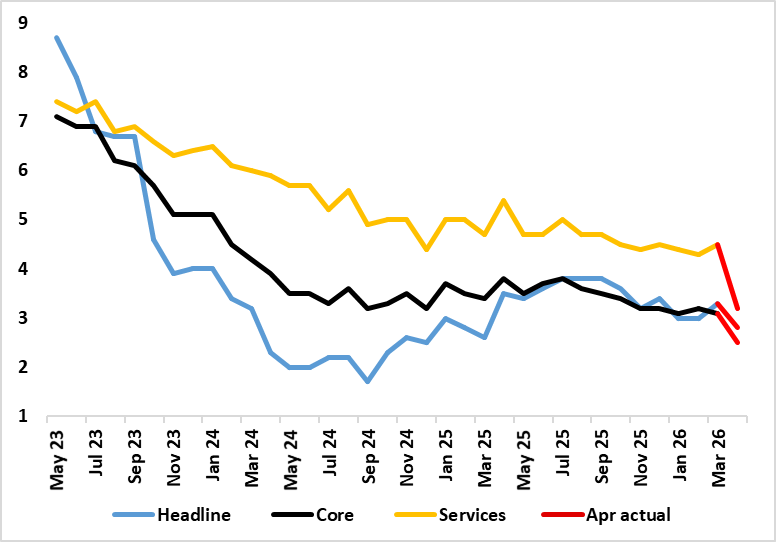

After January’s clear fall, even in the core rate, where the headline CPI rate fell from December’s 3.4% to 3.0% (a 10-mth low) it stayed there in February’s numbers – matching both consensus and BoE projections. Services fell 0.1 ppt to 4.3% which was a four-year low (Figure 1) but the co

March 24, 2026

DM Rates Outlook: Mixed Policy Rate and Yield Paths

March 24, 2026 8:46 AM UTC

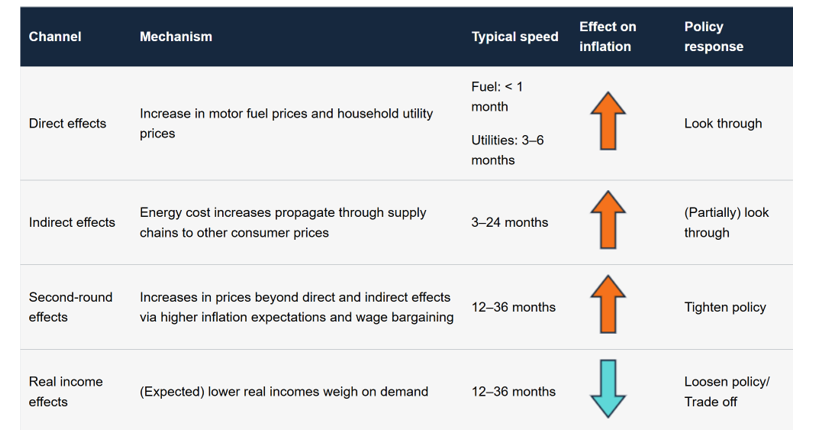

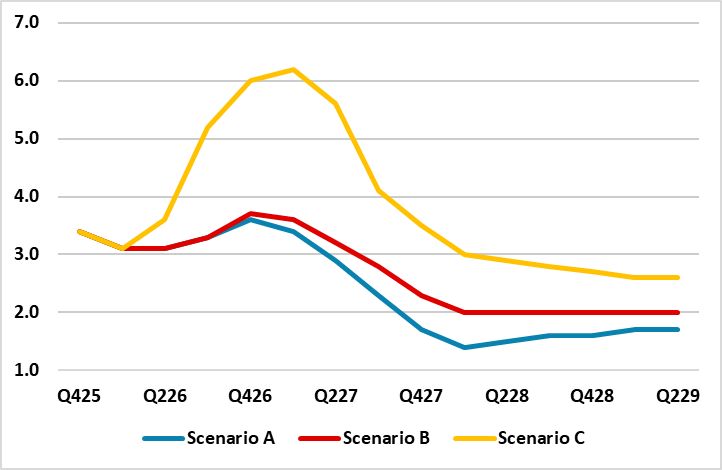

· The multi quarter outlook for DM rates depends on the length of the Iran war Our baseline is that it will be a 4-8 week war (here) and a 3-4 quarter retracement of oil prices back to pre-war levels – longer from Europe and Asian gas prices. We forecast WTI down to USD80-85 by June

Western Europe Outlook: Economies Slip on Oil

March 24, 2026 8:00 AM UTC

· In the UK, even without the Middle East impact we were suggesting a sub-consensus 2026 GDP picture which now has even greater downside risks attached. Our baseline is for 4-8 week war and a reversal of oil prices over 3 quarters. The BoE has a symmetric stance between 2nd round effe

March 19, 2026

BoE Review: A Fragile MPC Truce?

March 19, 2026 12:59 PM UTC

Very clearly, the BoE kept rates on hold with no dissents as it understandably waits for more information about the length, breadth and repercussions of the Iran war. The individual MPC member statements (as expected) showed diverging views as to the extent and reaction of what are now unfolding r

March 17, 2026

UK CPI Preview (Mar 25): The Calm Before the Storm?

March 17, 2026 8:53 AM UTC

Although most aspects of the January CPI came in a notch above BoE thinking, there was still a clear fall even in the core rate. Indeed, the headline CPI rate fell from December’s 3.4% to 3.0% (a 10-mth low) and we see it staying there is February’s numbers - as do BoE projections. Services

March 13, 2026

UK GDP Review: More Gloom?

March 13, 2026 7:41 AM UTC

Fresh downside surprises were the story from the January GDP numbers. Expectations that the economy would enjoy a further successive rise, thereby providing the best three-month showing in two years were dashed as GDP instead stagnated. Weakness was broad-based but most evident in private servic

March 12, 2026

BoE Preview (Mar 19): MPC Agree to Disagree?

March 12, 2026 2:35 PM UTC

The rate cut that seemed partly flagged by the narrow vote against easing in early February now looks highly unlikely this month. Indeed, it is also likely that the four who dissented in favor of cutting last time around will vote with the majority in favour of no change. But while the MPC as a wh

March 04, 2026

UK GDP Preview (Mar 13): Were Things Getting Better?

March 4, 2026 11:11 AM UTC

Belatedly, some good news; the UK economy grew for a second successive month in December, something not seen for almost a year. Even more encouragingly, it may very well enjoy a further rise in the looming January data, thereby providing the best three-month showing in two years. But as is famil

February 23, 2026

GBP: Foreign Investor Flows

February 23, 2026 11:05 AM UTC

· Inbound inflows into the UK have been solid in the last few years attracted by yield pick-up and fiscal consolidation for gilts and cheap comparable valuations in UK equities. UK BOP data suggests something would have to go really wrong to stop inbound portfolio flows e.g. UK recessio

February 18, 2026

UK CPI Review: Fresh and Marked Fall Resumes as Core Slips to Cycle-Low?

February 18, 2026 10:03 AM UTC

Although most aspects of the January CPI came in a notch above BoE thinking, the clear fall in the headline rate and further looser labor market messages still point to a BoE rate cut next month, not least given the likely return to the 2% target by April. These projected falls started with these Ja

February 17, 2026

UK Labor Market: Job Losses Weighing on Wages

February 17, 2026 7:52 AM UTC

There are further signs that the labor market is haemorrhaging jobs both clearly and broadly with fresh and deep falls in the more authoritative measure of jobs covering payrolls. Indeed, private sector payrolls are still falling, down almost a full ppt in y/y terms and more steeply so (Figure 1).

February 12, 2026

UK GDP Review: Underlying Economy Fragility Does Continue

February 12, 2026 7:52 AM UTC

First the good news; the UK economy grew for a second successive month in December, something not seen for almost a year. But as is familiar with recent UK real economy data, there is a negative flip side with the 0.1 m/m December advance negated by downward revisions to previous figures (November

February 11, 2026

UK Gilt Vigilantes and Politics

February 11, 2026 9:05 AM UTC

• The Gilt market is sensitive to the prospect that Starmer/Reeves could be replaced, resulting in some changes to the fiscal rules in the scanario of a new PM/Chancellor. Further fiscal rule refinement could be possible, but a new PM would want a political reset and this would likely pre

February 10, 2026

UK CPI Preview (Feb18): Fresh and Marked Fall to Resume as Core to Hit New Cycle-Low?

February 10, 2026 11:35 AM UTC

UK policy makers may not be able to say they have won the war against inflation, but a clear victory may be seen in the batter likely in the next few months with a likely return to the 2% target by April These projected falls are likely to commence with the looming January numbers (Figure 1) where a

February 05, 2026

BOE March Cut and Then More

February 5, 2026 1:25 PM UTC

· Six members of the MPC appear worried about the disinflationary impact from a weak economy and four of whom actually voted for a 25bps cut at the February meeting. BOE Bailey and Mann, looking at the MPC minutes, are very close to voting for a rate cut, which suggests high confidenc

UK GDP Preview (Feb 12): Underlying Economy Fragility Continues?

February 5, 2026 11:21 AM UTC

Even given the surprisingly solid November GDP release, this merely returns the level of GDP to where it was in June, albeit briefly as for the latter. Partly undermined by wet and warm weather through the month, we see no change on the December figure, in m/m terms (Figure 1), thus no reversal of

January 30, 2026

BOE Preview: Clues From February 5

January 30, 2026 8:05 AM UTC

· No change is expected at the Feb 5 BOE meeting, with communications leaving the door open to further interest rate cuts at a slower pace than 2025. However, we still forecast three 25bps cuts in 2026 to 3.00%, with the first likely arriving at the key April 30 meeting. The UK labor ma

January 16, 2026

UK: More BOE Easing and Politics/Fiscal Policy

January 16, 2026 11:55 AM UTC

• The BOE will likely deliver more rate cuts than discounted by money markets and we forecast three 25bps cuts in 2026 to 3.00%. The UK labor market is weak enough to prompt further wage inflation and underlying inflation slowdown, while fiscal policy is tightening multi-year.

•

January 14, 2026

DM Government Debt: 2026 Supply & Voters’ Resistance To Fiscal Consolidation

January 14, 2026 11:55 AM UTC

· We see the most persistent issue being supply (budget deficit + QT) in 2026, which should lessen into 2027 with a slowdown in ECB/BOE QT and a partial U turn by the BOJ. However, governments are also struggling with electorates that are resistant to higher taxes or lower governmen

January 08, 2026

UK GDP Preview (Jan 15): Underlying and Headline Economy Fragility Continues?

January 8, 2026 11:13 AM UTC

As we have underlined, UK GDP has hardly moved since March and this became even clearer with the last (October) GDP release, the question being whether weakness is getting more discernible and significant. Indeed, it has fallen in three of the last four months of data (Figure 1) and where we see n

December 19, 2025

Western Europe Outlook: Underlying Price Pressures Ebbing

December 19, 2025 9:34 AM UTC

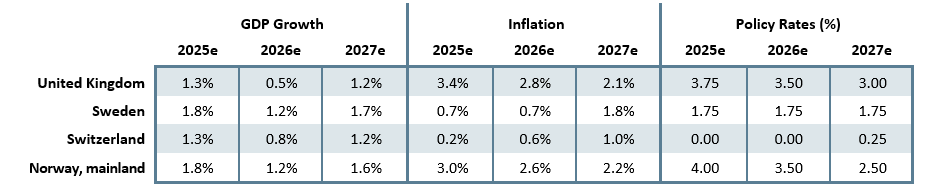

· In the UK, we have upgraded 2025 GDP growth by 0.1 ppt to 1.3%, but pared back that for next year by a two notches to a very sub-par 0.6%. We think the weak(er) labor market will accentuate somewhat refreshed disinflation allowing the BoE to ease further in 2026 by around 75 bp to 3.0

December 18, 2025

BoE Review (Dec 18): Splits More Entrenched?

December 18, 2025 12:41 PM UTC

That the BoE delivered a sixth 25 bp rate cut (to an almost three-year low of 3.75%) was hardly in doubt. But we were surprised that amid the recent run of weak data, that there were (again) four dissents with Governor Bailey switching sides. Notably, in a clear combative overtone, at least some

December 17, 2025

DM Rates Outlook: 2026 Yield Curve Steepening Before 2027 Flattening

December 17, 2025 9:21 AM UTC

· Multi quarter, we still look for 50bps of further Fed easing by end 2026, which will likely initially bring 2yr yields down to 3.35%. However, once the Fed Funds rate get closer to 3.0-3.25% and the assumed slowdown turns into a soft landing, the 2yr will likely move to a premium ve

UK CPI Review: Down More Than Expected from Likely Peak?

December 17, 2025 7:38 AM UTC

A clear downside surprise adds to the wealth of data suggesting a reining of price and cost pressures. This November result makes it more likely that the September CPI outcome will prove to be the CPI inflation peak. Indeed, although October figure fell a little less than the consensus by 0.2 pp

December 16, 2025

UK Labor Market: Job Losses Weighing Even More Clearly on Wages

December 16, 2025 8:06 AM UTC

Adding to the array if weak activity updates of late, there are increasing signs that the labor market is haemorrhaging jobs more clearly and broadly with fresh and deeper falls in the more authoritative measure of jobs covering payrolls. Indeed, private sector payrolls are still falling, down alm

December 12, 2025

UK GDP Review: Underlying and Headline Economy Negative, Fragile and Listless

December 12, 2025 7:47 AM UTC

As we have underlined, GDP has hardly moved since March and this became even clearer with the October GDP release, the question being whether weakness is getting more discernible and significant. Indeed, it has fallen in three of the last four months (Figure 1), and where the unexpected further 0.

December 09, 2025

BoE Preview (Dec 18): How Big a Split?

December 9, 2025 11:29 AM UTC

That the BoE will deliver a fifth 25 bp rate cut (to 3.75%) on Dec 18 is almost certain, even after a Budget that did not accentuate current emerging demand weakness. The question is whether the MPC vote will be as close as the 5:4 split seen last month but with Governor Bailey switching sides.