View:

August 11, 2026

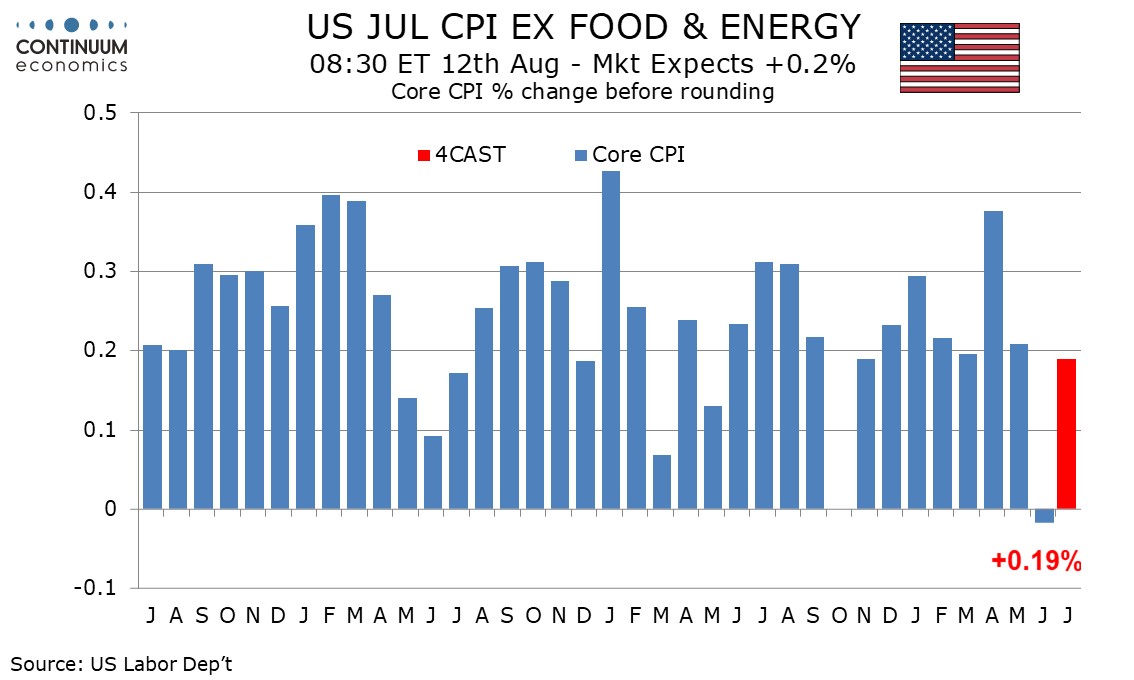

Preview: Due August 12 - U.S. July CPI - Another subdued month, if less so than June

August 11, 2026 12:50 PM UTC

We expect a subdued July CPI, up by 0.1% overall and 0.2% ex food and energy, with the respective gains before rounding being only 0.06% and 0.19%. This will however be less weak than June’s 0.4% decline overall, with the June core rate ex food and energy having been unchanged.

August 10, 2026

Taiwan: China Coastguard Quarantine Risks Grow

August 10, 2026 7:55 AM UTC

· Given China’s coastguard recent actions, we now raise the probability of a full quarantine of Taiwan shipping to 20% versus 10-15% in 2027/28 (Figure 2), with the probability of some further measures beyond radio requests now above 50% in 2027/28 and in our baseline. Quarantine meas

August 07, 2026

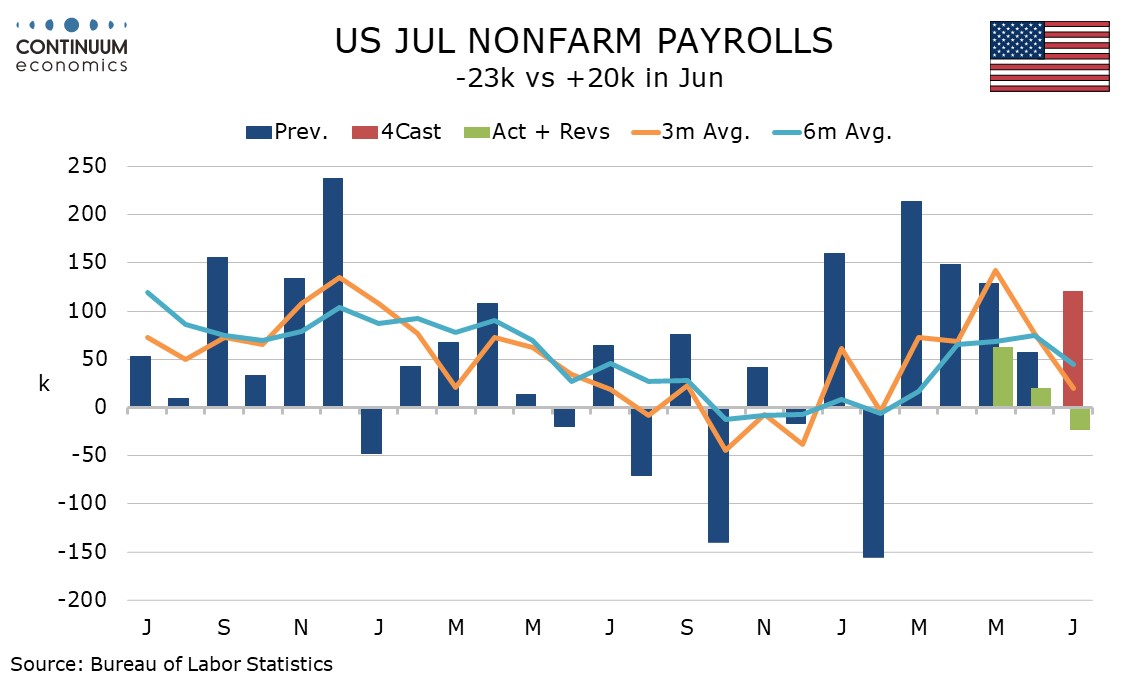

U.S. July Employment - Softer payroll and falling unemployment hint at labor shortages, but no lift to earnings

August 7, 2026 1:20 PM UTC

July’s non-farm payroll at -23k with negative back month revisions is weaker than expected but largely because of negatives in government led by local government education and leisure and hospitality, which may reflect labor shortages. A declining labor force saw the unemployment rate fall, to 4.1

August 06, 2026

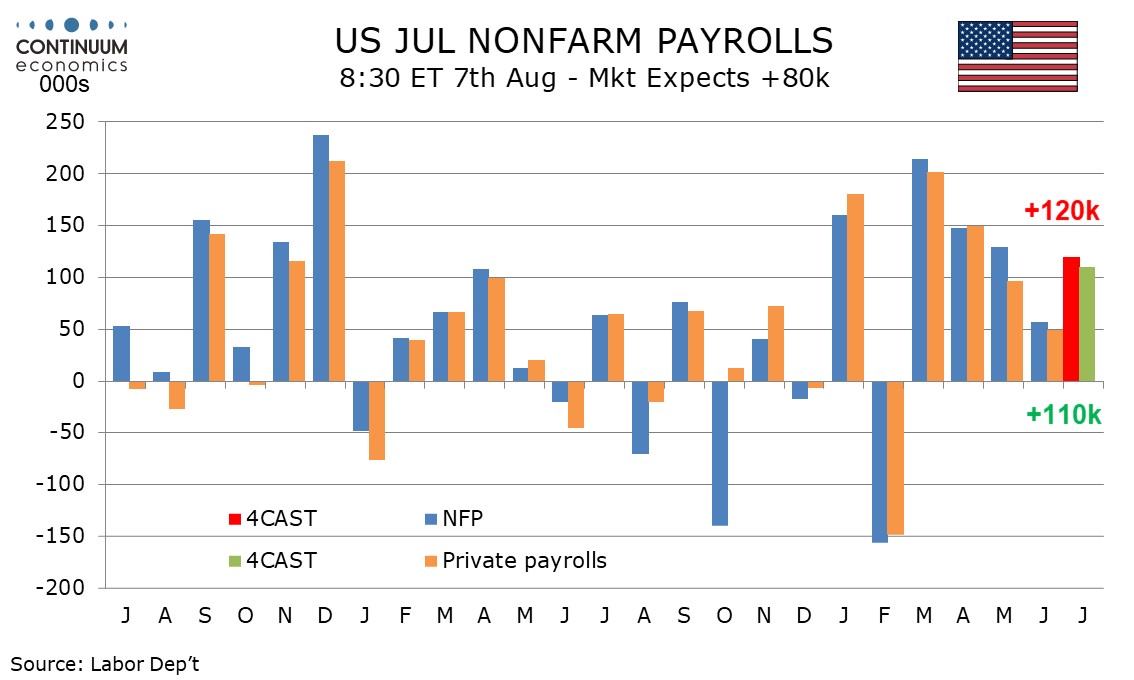

Preview: Due August 7 - U.S. July Employment (Non-Farm Payrolls) - Stronger than June, but with a rise in unemployment

August 6, 2026 1:27 PM UTC

We expect July’s non-farm payroll to rise by 120k overall and by 110k in the private sector, a significant improvement from June’s respective gains of 57k and 49k but largely explained by a recovery in leisure and hospitality. We expect unemployment to rise to 4.3% from 4.2%, reversing a June de