View:

July 28, 2026

July 27, 2026

Preview: Due August 7 - Canada August Employment - Another positive month, but tariffs a risk going forward

July 27, 2026 3:32 PM UTC

We expect Canadian employment to increase by 20k in July, a third straight gain, similar to June’s 18.2k though well below May’s 87.8k which was correcting preceding weakness. We expect unemployment to match June’s 6.5% but before rounding to fall to 6.451% from 6.498%.

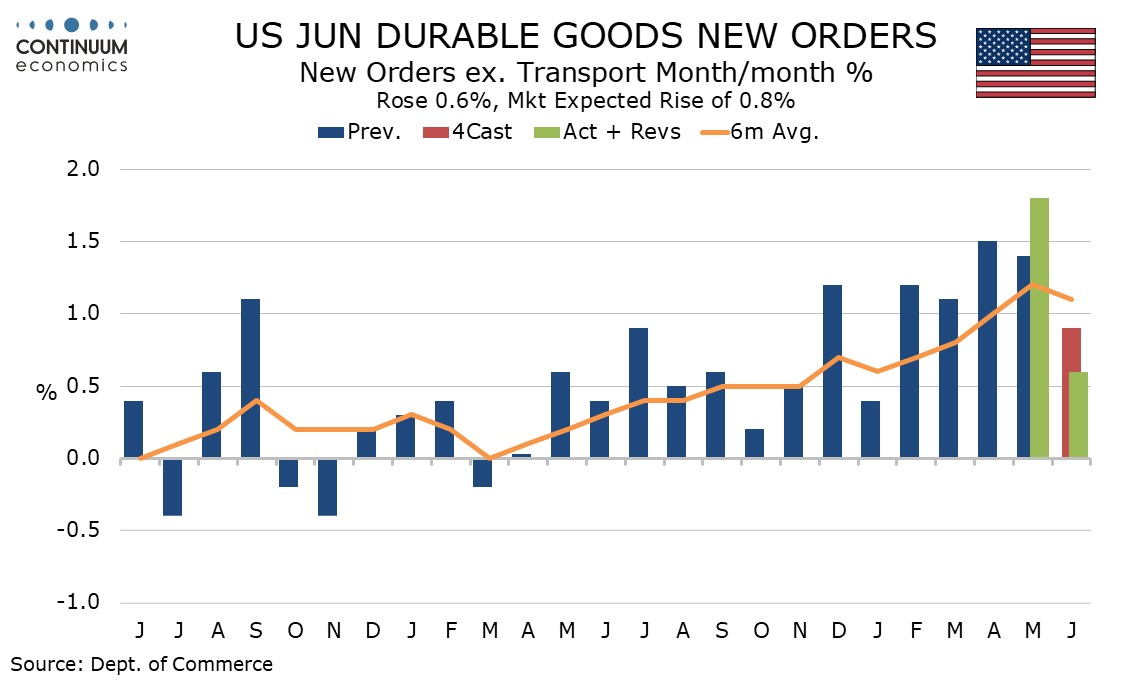

U.S. June Durable Goods Orders - Restrained by seasonal adjustments and possibly prices

July 27, 2026 12:49 PM UTC

June durable goods orders with a 0.3% rise were well below expectations with a bounce in aircraft orders implied by Boeing data failing to show up in seasonally adjusted data while the ex transport gain of 0.6% was the slowest since January, though this may in part reflect easing price pressures.

U.S. June Durable Goods Orders - Restrained by seasonal adjustments and possibly prices

July 27, 2026 12:49 PM UTC

June durable goods orders with a 0.3% rise were well below expectations with a bounce in aircraft orders implied by Boeing data failing to show up in seasonally adjusted data while the ex transport gain of 0.6% was the slowest since January, though this may in part reflect easing price pressures.

Preview: Due July 28 - U.S. June Advance Goods Trade Balance - Deficit to correct lower, but remain large

July 27, 2026 12:08 PM UTC

We expect an advance June trade deficit of $100.8bn, down from $105.9bn in May which was the widest since a record pre-tariff deficit in March 2025, but still significantly above the deficits seen in the first four months of 2026.

Margin Call - Does Margin Debt Really Predict Market Crashes?

July 27, 2026 11:31 AM UTC

· US margin debt has reached USD1.5tn, the kind of huge round figure milestone that is always going to get a fair amount of attention, especially with the market focused on risk and valuations. Should this number be sounding the alarm? The balanced answer is probably partially, though i