View:

August 10, 2026

Preview: Due August 11 - U.S. July Existing Home Sales - Surveys suggest slippage

August 10, 2026 1:20 PM UTC

We expect July existing home sales to see a second straight monthly fall, by 1.5% to 4.03m, as fears that the next Fed move is likely to be a hike pick up, while remaining in the year to date range.

August 07, 2026

Preview: Due August 18 - U.S. July Housing Starts and Permits - Modest declines, consistent with trend

August 7, 2026 3:07 PM UTC

We expect July housing starts to fall by 4.7% to 1360k while permits fall by 0.3% to 1370k. Trends in the housing sector appear to be showing a modest loss of momentum entering Q3.

August 06, 2026

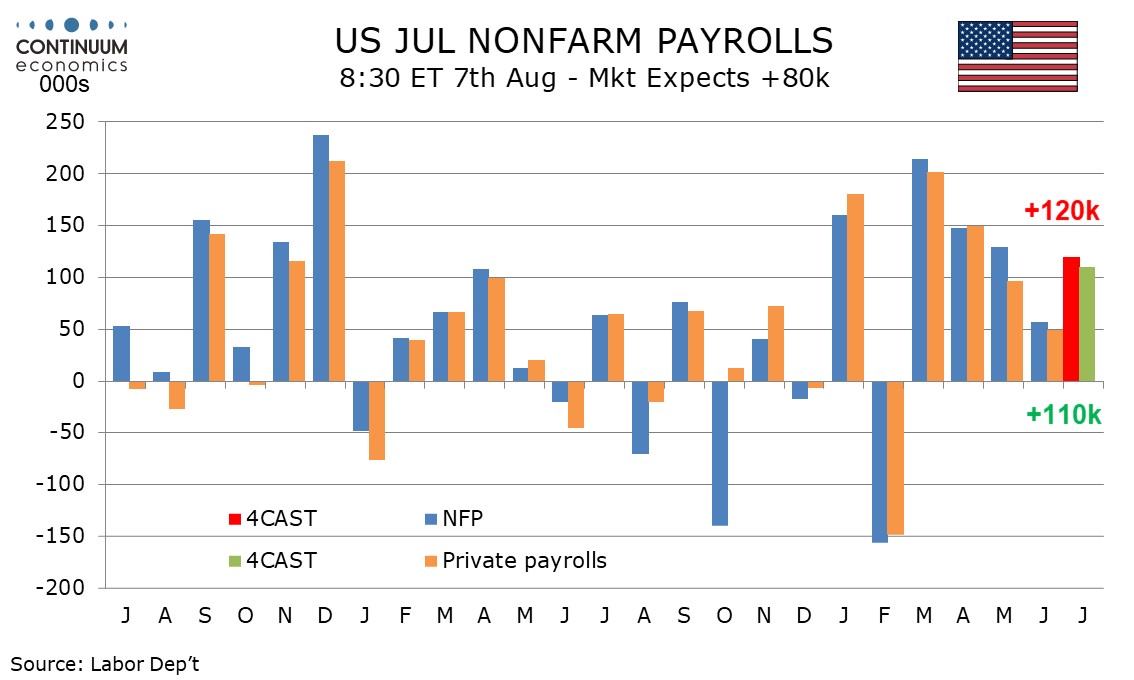

Preview: Due August 7 - U.S. July Employment (Non-Farm Payrolls) - Stronger than June, but with a rise in unemployment

August 6, 2026 1:27 PM UTC

We expect July’s non-farm payroll to rise by 120k overall and by 110k in the private sector, a significant improvement from June’s respective gains of 57k and 49k but largely explained by a recovery in leisure and hospitality. We expect unemployment to rise to 4.3% from 4.2%, reversing a June de

Preview: Due August 7 - U.S. July Employment (Non-Farm Payrolls) - Stronger than June, but with a rise in unemployment

August 6, 2026 1:27 PM UTC

We expect July’s non-farm payroll to rise by 120k overall and by 110k in the private sector, a significant improvement from June’s respective gains of 57k and 49k but largely explained by a recovery in leisure and hospitality. We expect unemployment to rise to 4.3% from 4.2%, reversing a June de

Preview: Due August 7 - Canada July Employment - Another positive month, but tariffs a risk going forward

August 6, 2026 11:53 AM UTC

We expect Canadian employment to increase by 20k in July, a third straight gain, similar to June’s 18.2k though well below May’s 87.8k which was correcting preceding weakness. We expect unemployment to match June’s 6.5% but before rounding to fall to 6.451% from 6.498%.

August 05, 2026

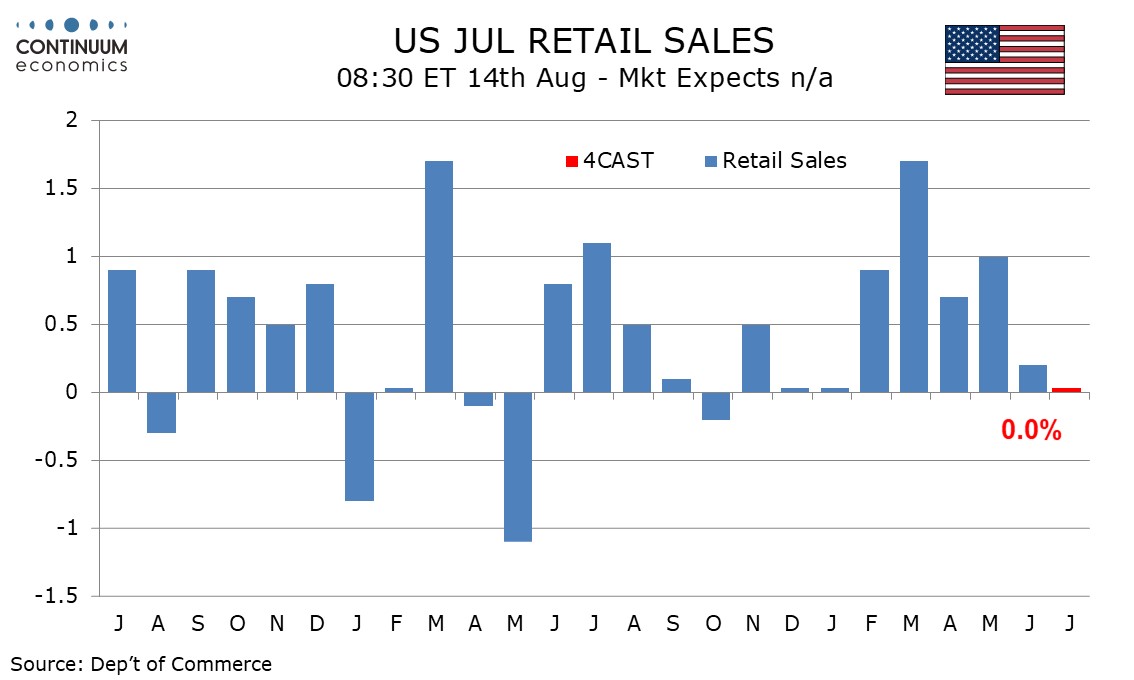

Preview: Due August 14 - U.S. July Retail Sales - Some loss of momentum, but still resilient

August 5, 2026 3:46 PM UTC

We expect June retail sales to unchanged overall, the weakest since a matching January, with a 0.2% increase ex autos, which would reverse a 0.2% June decline. Ex auto and gasoline we expect a second straight 0.4% increase.

Preview: Due August 14 - U.S. July Retail Sales - Some loss of momentum, but still resilient

August 5, 2026 3:46 PM UTC

We expect June retail sales to unchanged overall, the weakest since a matching January, with a 0.2% increase ex autos, which would reverse a 0.2% June decline. Ex auto and gasoline we expect a second straight 0.4% increase.

August 04, 2026

Preview: Due August 28 - Canada Q2/June GDP - Quarterly rebound seen largely on net exports

August 4, 2026 4:13 PM UTC

We expect Q3 Canadian GDP to increase by 3.3% annualized, in line with what monthly data is implying, assuming the preliminary estimate for a 0.2% increase in June is accurate and gains of 0.3% in May and 0.6% in April are unrevised. This will mark a return to growth after two straight negative quar

Preview: Due August 5 - U.S. July ADP Employment - Weekly ADP data suggests some slowing

August 4, 2026 11:05 AM UTC

We expect a 65k increase in July’s ADP estimate for private sector employment, which is well below our forecast for July’s private sector non-farm payroll of 110k (we expect overall payrolls to rise by 120k). It is however similar to June’s non-farm payroll, which rose by 57k and 49k in the pr

August 03, 2026

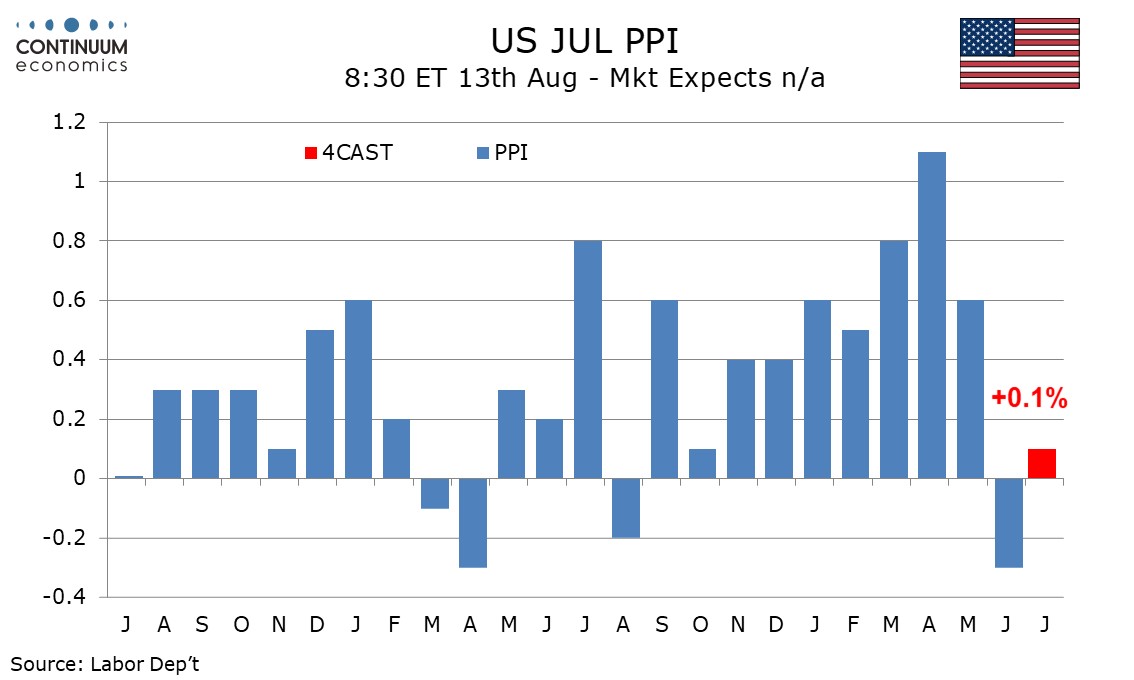

Preview: Due August 13 - U.S. July PPI - Prices seen subdued when data was surveyed

August 3, 2026 1:12 PM UTC

We expect July’s PPI to reflect more the more optimistic view of the Middle East seen at the start of the month than the riskier one later in the month. We expect gains of 0.1% overall, 0.3% ex food and energy and 0.2% ex food and trade, mostly subdued, if stronger than respective June outcomes of

Preview: Due August 13 - U.S. July PPI - Prices seen subdued when data was surveyed

August 3, 2026 1:12 PM UTC

We expect July’s PPI to reflect more the more optimistic view of the Middle East seen at the start of the month than the riskier one later in the month. We expect gains of 0.1% overall, 0.3% ex food and energy and 0.2% ex food and trade, mostly subdued, if stronger than respective June outcomes of

Preview: Due August 4 - U.S. June Trade Balance - Deficit to correct lower, but remain large

August 3, 2026 12:40 PM UTC

We expect a June trade deficit of $73.5bn, down from $77.6bn in May which was the widest since a record pre-tariff deficit in March 2025, but still significantly above the deficits seen in the first four months of 2026, each of which was close to $55bn.

July 31, 2026

Preview: Due August 17 - Canada July CPI - Slightly firmer on energy but with stable core rates

July 31, 2026 7:03 PM UTC

We expect July Canadian CPI to correct higher to 2.9% yr/yr from June’s 2.8% which slipped significantly from May’s 3.2%, on a modest increase in gasoline prices after a sharp fall in June. However, we expect the Bank of Canada’s core rates to be unchanged from June, with CPI-Median at 1.9%, C

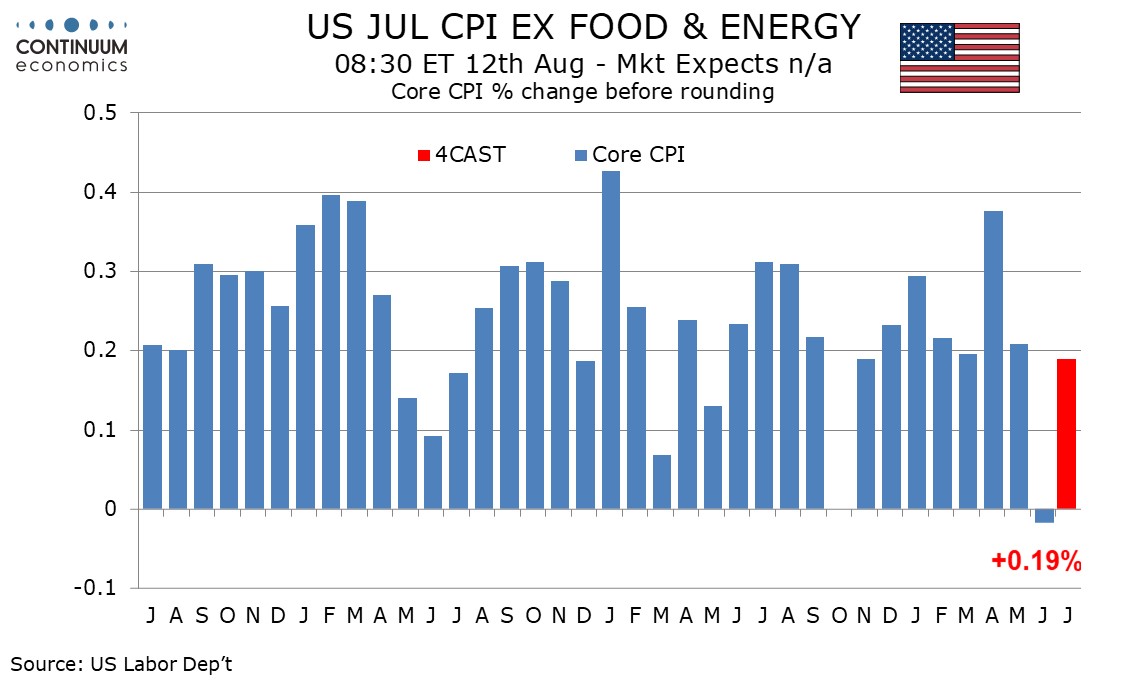

Preview: Due August 12 - U.S. July CPI - Another subdued month, if less so than June

July 31, 2026 3:52 PM UTC

We expect a subdued July CPI, up by 0.1% overall and 0.2% ex food and energy, with the respective gains before rounding being only 0.06% and 0.19%. This will however be less weak than June’s 0.4% decline overall, with the June core rate ex food and energy having been unchanged.

Preview: Due August 12 - U.S. July CPI - Another subdued month, if less so than June

July 31, 2026 3:51 PM UTC

We expect a subdued July CPI, up by 0.1% overall and 0.2% ex food and energy, with the respective gains before rounding being only 0.06% and 0.19%. This will however be less weak than June’s 0.4% decline overall, with the June core rate ex food and energy having been unchanged.

July 30, 2026

Preview: Due August 11 - U.S. July Existing Home Sales - Surveys suggest slippage

July 30, 2026 7:43 PM UTC

We expect July existing home sales to see a second straight monthly fall, by 1.5% to 4.03m, as fears that the next Fed move is likely to be a hike pick up, while remaining in the year to date range.

Preview: Due August 4 - U.S. June Trade Balance - Deficit to correct lower, but remain large

July 30, 2026 2:38 PM UTC

We expect a June trade deficit of $73.5bn, down from $77.6bn in May which was the widest since a record pre-tariff deficit in March 2025, but still significantly above the deficits seen in the first four months of 2026, each of which was close to $55bn.

Preview: Due July 31 - U.S. Q2 Employment Cost Index - Losing momentum

July 30, 2026 1:57 PM UTC

We look for the Q2 employment cost index (ECI) to increase by 0.7%, slower than Q1’s 0.9% but matching the Q4 outcome. This would see the yr/yr pace slow to 3.2% from 3.4%, reaching its slowest since Q2 2021.

July 29, 2026

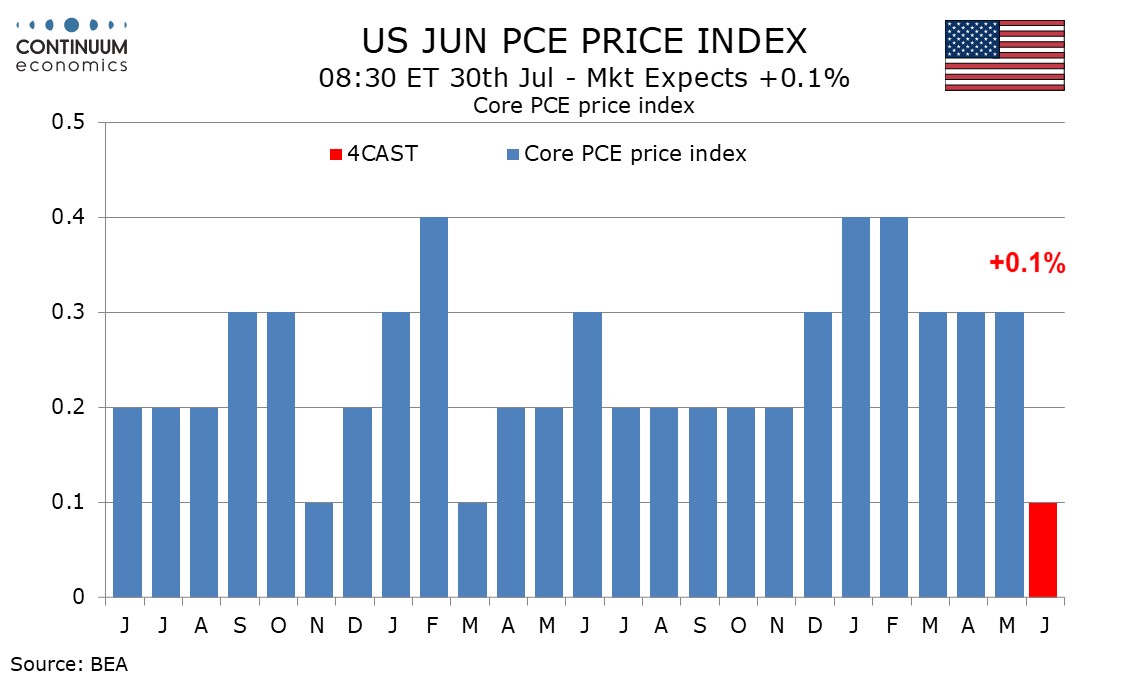

Preview: Due July 30 - U.S. June Personal Income and Spending - PCE Prices not quite as soft as CPI

July 29, 2026 12:47 PM UTC

June’s personal income and spending report may be overshadowed by the Q2 GDP report released at the same time. We expect a subdued 0.1% increase in core PCE prices, with overall PCE prices down by 0.1%, leaving gains of 0.3% in both personal income and personal spending looking respectable in real

Preview: Due July 30 - U.S. June Personal Income and Spending - PCE Prices not quite as soft as CPI

July 29, 2026 12:46 PM UTC

June’s personal income and spending report may be overshadowed by the Q2 GDP report released at the same time. We expect a subdued 0.1% increase in core PCE prices, with overall PCE prices down by 0.1%, leaving gains of 0.3% in both personal income and personal spending looking respectable in real