UK CPI Preview (Jul 16): Services Inflation to Fall Further?

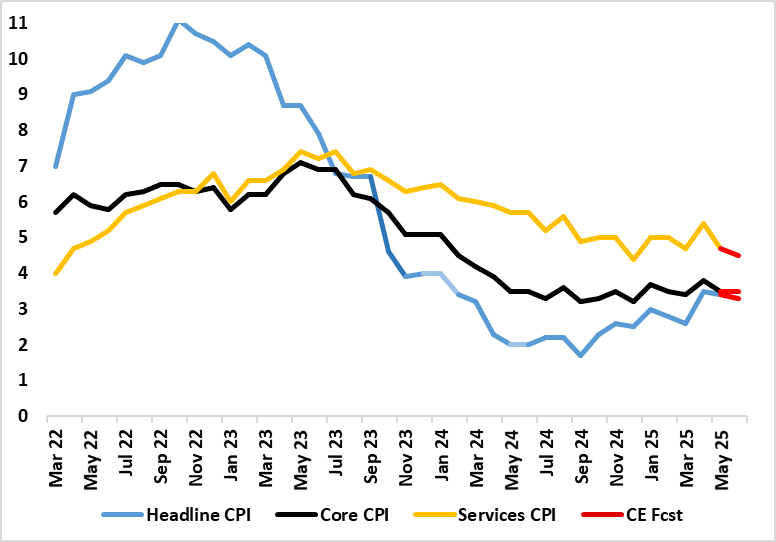

Calendar effects have been accentuating swings in UK CPI data of late. Indeed, the timing of Easter may have been a partial factor in the May CPI, where a distinct drop back in services and core rates failed to make the headline drop, which instead stayed at 3.4% in line with BoE thinking due to higher food and household goods prices. Food prices, amid what may be a poor UK harvest, may be a growing concern for the BoE both for its impact of spending power and on inflation. But real economy and labor market weakness, allied to fiscal concerns may be even bigger worries. This despite what may be only a small 0.1 ppt drop in the June headline CPI and where a slightly larger fall in services may be offset by still elevated food inflation at over 4.5%, adverse energy base effects and a stable core reading stuck at 3.5%.

Figure 1: June Inflation to Slip Only Slightly

Source: ONS, Continuum Economics, % chg y/y

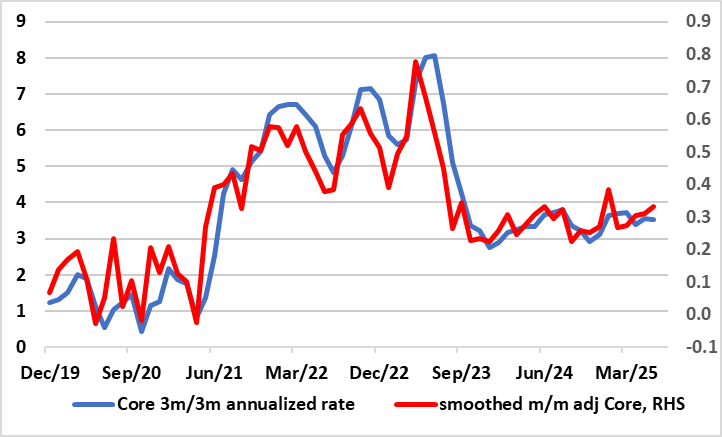

The April data may have persuaded some of the MPC not to cut last month had they been aware of the full data. But at the same time there was no clear fresh inflation spiral with six of the 12 CPI components seeing softer pressures and where consumer sensitive clothing and household equipment actually turned negative, possible a sign of reined in pricing power. This largely continued into May but with the reassuring development of a belated slowing in rent inflation. Admittedly, adjusted m/m data suggest disinflation may have stalled but this may be more a result of the calendar effects dominating this more short-term measure of price swings (Figure 2)

Figure 2: Clear Adjusted Core Inflation Drop Continues?

Source: ONS, Continuum Economics, % chg m/m

Albeit with some added upside risk from a likely rise back in fuel costs in June, we see inflation having peaking at this April/May level albeit with the rate returns (briefly) to (around) 3.5% in September, this latter outcome some 0.2 ppt below BoE thinking. As for BoE rate cutting, we still think upside surprises would have to dislodge the MPC from cutting at least twice more this year albeit it clear that the MPC will remain divided, if not more so, even against a backdrop where there is a general view that policy restriction needs to reduced, the difference being over how fast given worries about price persistence, and where looser labor market numbers and fiscal considerations may be more important in (re-)shaping policy thinking.