View:

July 27, 2026

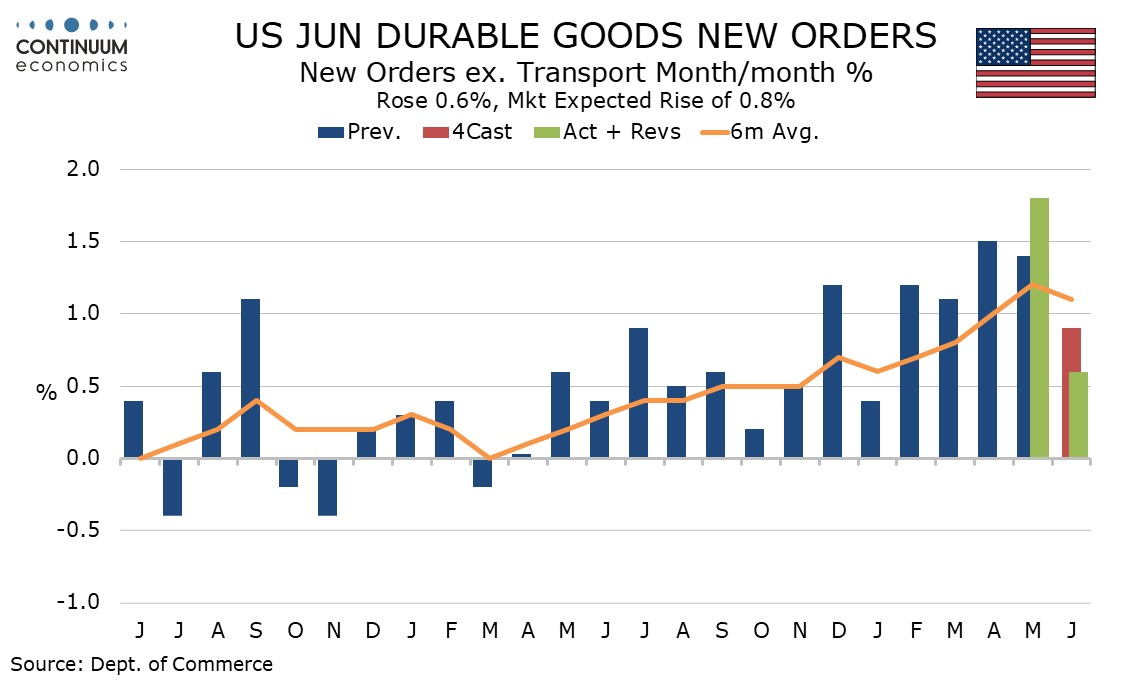

U.S. June Durable Goods Orders - Restrained by seasonal adjustments and possibly prices

July 27, 2026 12:49 PM UTC

June durable goods orders with a 0.3% rise were well below expectations with a bounce in aircraft orders implied by Boeing data failing to show up in seasonally adjusted data while the ex transport gain of 0.6% was the slowest since January, though this may in part reflect easing price pressures.

Margin Call - Does Margin Debt Really Predict Market Crashes?

July 27, 2026 11:31 AM UTC

· US margin debt has reached USD1.5tn, the kind of huge round figure milestone that is always going to get a fair amount of attention, especially with the market focused on risk and valuations. Should this number be sounding the alarm? The balanced answer is probably partially, though i

July 24, 2026

Trump: Tariffs 2.0

July 24, 2026 7:16 AM UTC

• Replacing section 122 at 10% with section 301 at 10-12.5% is unlikely to have much lasting economic impact in itself. However, the Trump administration are also undertaking section 301 investigation against 16 countries on excess production, with the report and new tariffs expected in A

July 23, 2026

ECB: September Hike 50% Probability?

July 23, 2026 1:41 PM UTC

· Lagarde disclosed that some ECB board members considered a hike at today’s meeting and she noted that the consensus was to wait for incoming data before the September 10 meeting and then reassess. This clearly signals that the September meeting will seriously consider a 25bps hike,

July 22, 2026

BOE Preview After CPI: Hawkish Noises

July 22, 2026 6:11 AM UTC

• The BOE will likely maintain a hawkish bias on July 30, but are unlikely to signal a September hike. The June CPI did not really change this picture, with the core unchanged at 2.6%. Though BOE Bailey recently noted the unstable process (in the Straits of Hormuz and for energy prices), he

July 21, 2026

UK Fiscal Policy and the New Chancellor

July 21, 2026 6:18 AM UTC

· Apprehension will exist until the Autumn budget, despite a repeated commitment by PM Burnham to stick to the fiscal rules. Spending commitments are clearer than tax raises measures, while new Chancellor Healey may not be strong enough to curtail spending pressures. This could mean

July 20, 2026

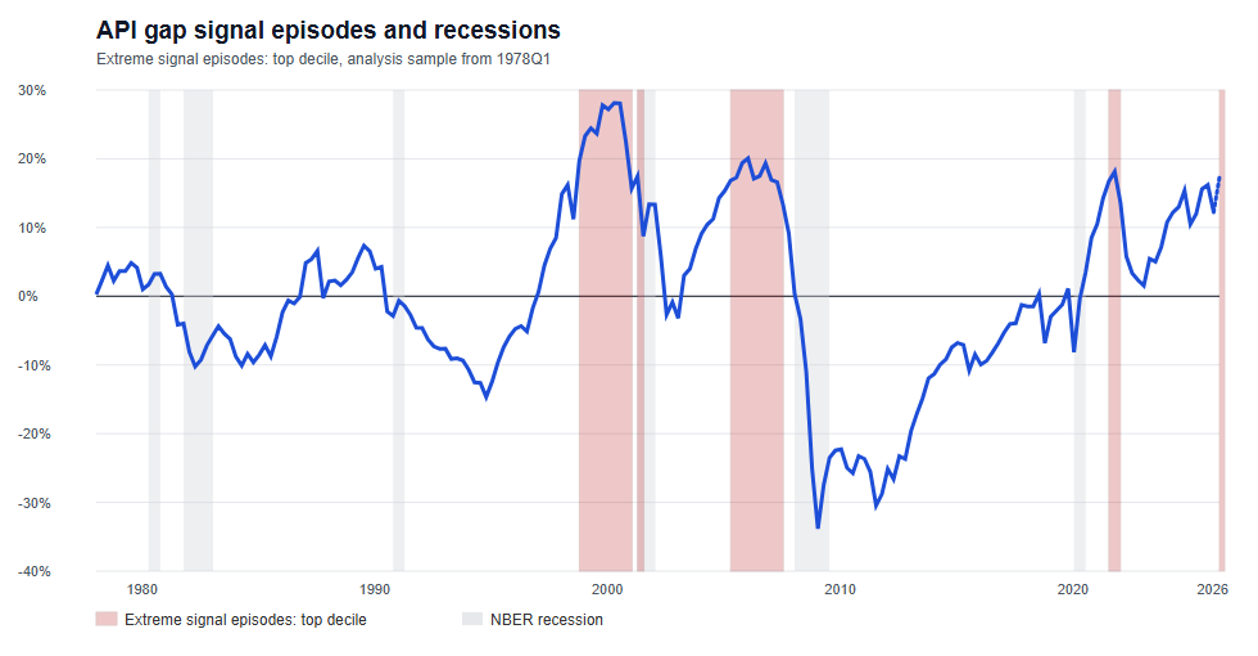

The Endpoint Problem: US Asset Prices, Investment and the Current Cycle

July 20, 2026 8:00 AM UTC

· Asset Price Index (API) framework suggests the US gap is elevated and, on some constructs, has moved into top-decile territory.

· The question is whether prices, capex and financing conditions are beginning to reinforce the same cyclical risk-accumulation dynamics.

·

July 17, 2026

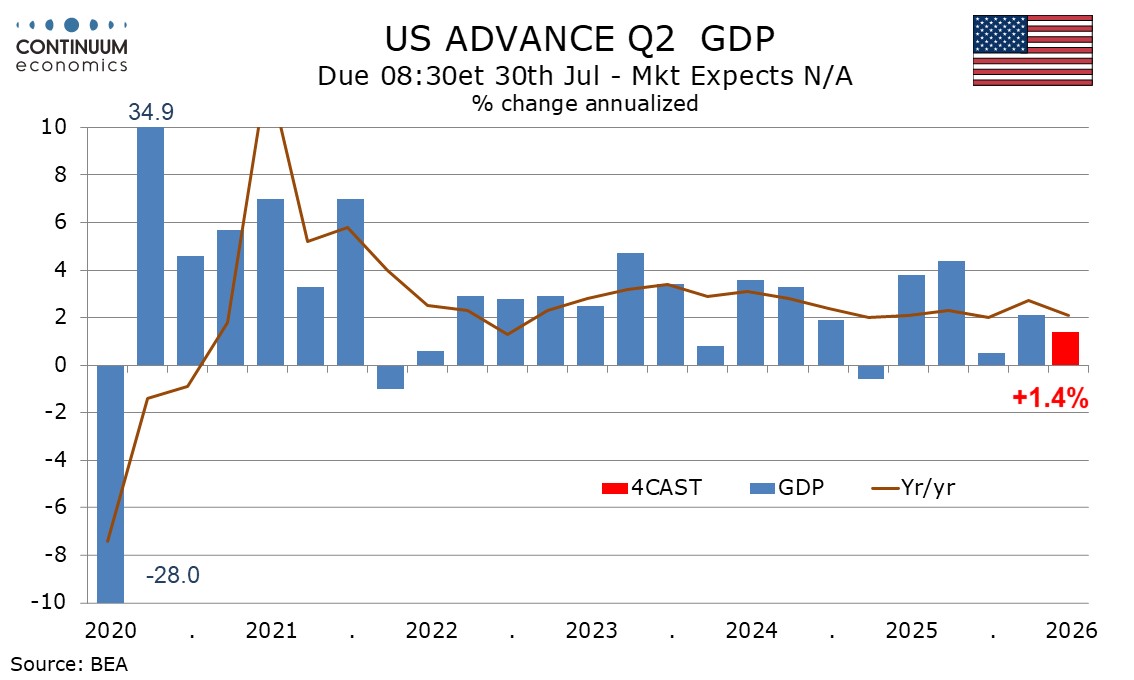

Preview: Due July 30 - U.S. Q2 GDP - Strong domestic demand but weakness in net exports and inventories

July 17, 2026 5:12 PM UTC

We expect a modest Q2 GDP increase of 1.4% annualized, though there is still uncertainty over June data for trade and inventories, which we expect to act as negatives in the quarter as a whole, while assuming some improvement in their June data.

Economic Data and Events Week Ahead July 20-24

July 17, 2026 3:00 PM UTC

The highlight of the week comes from the ECB meeting and press conference, although we do not expect it to provide much guidance regarding September, sticking to the non-pre-commit language, to keep options open depending on data and geopolitical developments.

The UK has its busy week, but data is

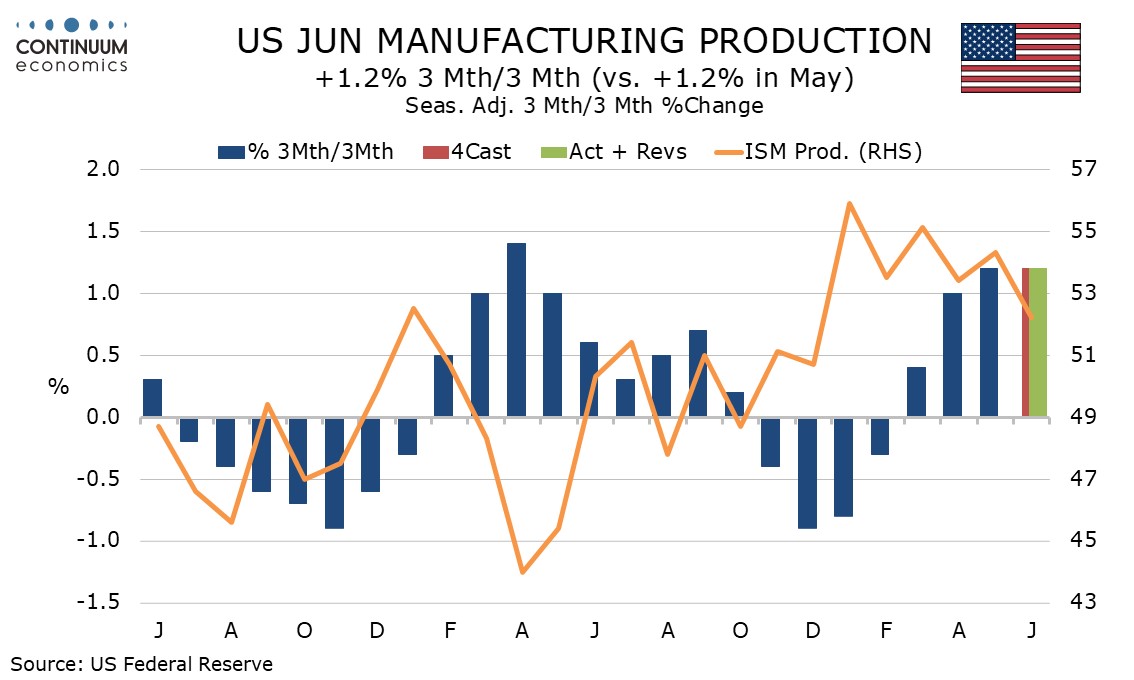

U.S. June Industrial Production - Subdued month, strong quarter

July 17, 2026 1:31 PM UTC

June industrial production has seen a second straight subdued month to follow a strong April, still leaving a healthy underlying picture but may temper some excessive optimism over the impact of rising AI-led investment.

ECB: Bark No Bite

July 17, 2026 7:05 AM UTC

· The vigilance mantra means that the ECB will still have a broad caution against 2nd round effects and the risks that energy prices could push higher. We feel that the June inflation data, plus the prospect that Iran/U.S. could call a new truce (here) will be enough to make most on t

July 16, 2026

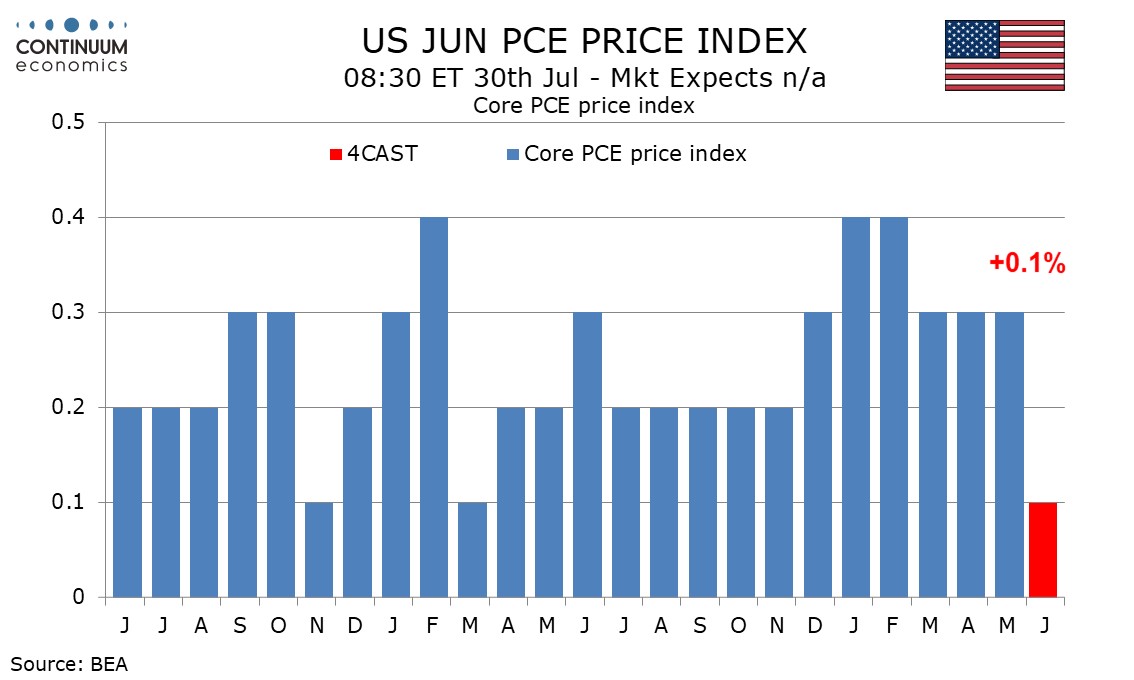

Preview: Due July 30 - U.S. June Personal Income and Spending - PCE Prices not quite as soft as CPI

July 16, 2026 4:22 PM UTC

June’s personal income and spending report may be overshadowed by the Q2 GDP report released at the same time. We expect a subdued 0.1% increase in core PCE prices, with overall PCE prices down by 0.1%, leaving gains of 0.3% in both personal income and personal spending looking respectable in real

U.S. June Retail Sales - Underlying resilience persists, Initial Claims fall and Philly Fed surges

July 16, 2026 1:09 PM UTC

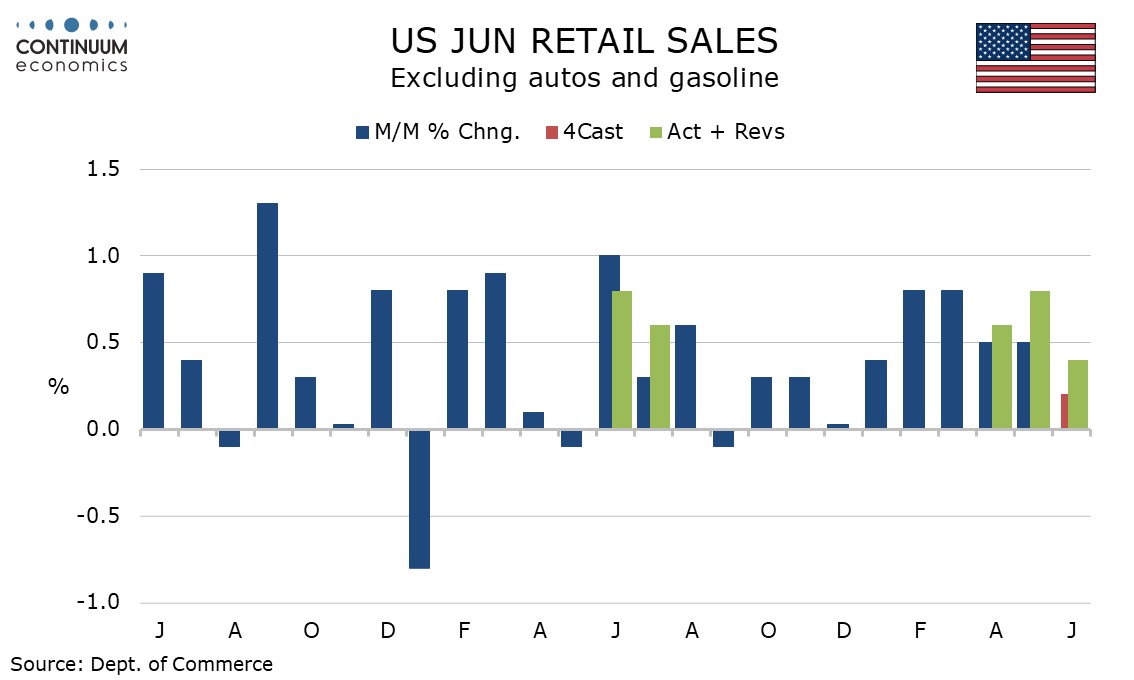

The latest US data is on the firm side of expectations. June retail sales are in line with expectations with a 0.2% increase and a gasoline-led 0.2% decline ex autos., but the control group that contributes to GDP maintains underlying strength with a rise of 0.5%. Weekly initial claims at 208k from

China Jun Activity Data Review: A Diverged Economy

July 16, 2026 6:32 AM UTC

China’s June activity data displayed divergence of statistics, as AI and related infrastructure boost industrial production. Urban Fixed Asset Investment was still depressed, due to on-going failure of mainland developers, retail sales still remained modest , weighed down by the wealth effect from

UK GDP and BOE Question

July 16, 2026 6:23 AM UTC

· UK GDP rose 0.1% in May as expected, helped by services but with softness remaining in other areas. H2 will depend on businesses and consumers, where a BOE rate hike would dent sentiment and spending – we look for no change in policy rates in 2026 however, followed by 2027 cuts. A

July 15, 2026

FOMC Preview for July 29: Unchanged policy with an unspoken tightening bias

July 15, 2026 3:52 PM UTC

The FOMC meets on July 29 in a meeting that will see no update to the dots or economic forecasts. With forward guidance now becoming limited all meetings should be seen as live, but after softer than expected June non-farm payroll and more importantly CPI data, a change in policy looks unlikely at t