View:

Margin Call - Does Margin Debt Really Predict Market Crashes?

July 27, 2026 11:31 AM UTC

· US margin debt has reached USD1.5tn, the kind of huge round figure milestone that is always going to get a fair amount of attention, especially with the market focused on risk and valuations. Should this number be sounding the alarm? The balanced answer is probably partially, though i

UK Fiscal Policy and the New Chancellor

July 21, 2026 6:18 AM UTC

· Apprehension will exist until the Autumn budget, despite a repeated commitment by PM Burnham to stick to the fiscal rules. Spending commitments are clearer than tax raises measures, while new Chancellor Healey may not be strong enough to curtail spending pressures. This could mean

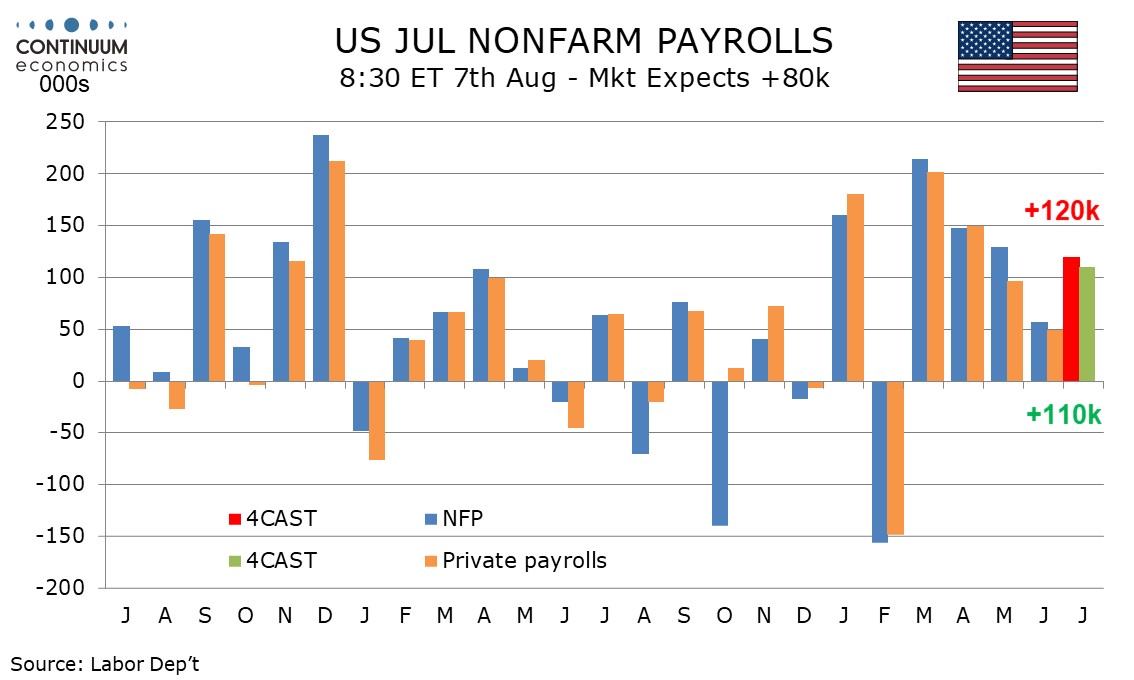

Preview: Due August 7 - U.S. July Employment (Non-Farm Payrolls) - Stronger than June, but with a rise in unemployment

July 28, 2026 3:49 PM UTC

We expect July’s non-farm payroll to rise by 120k overall and by 110k in the private sector, a significant improvement from June’s respective gains of 57k and 49k but largely explained by a recovery in leisure and hospitality. We expect unemployment to rise to 4.3% from 4.2%, reversing a June de

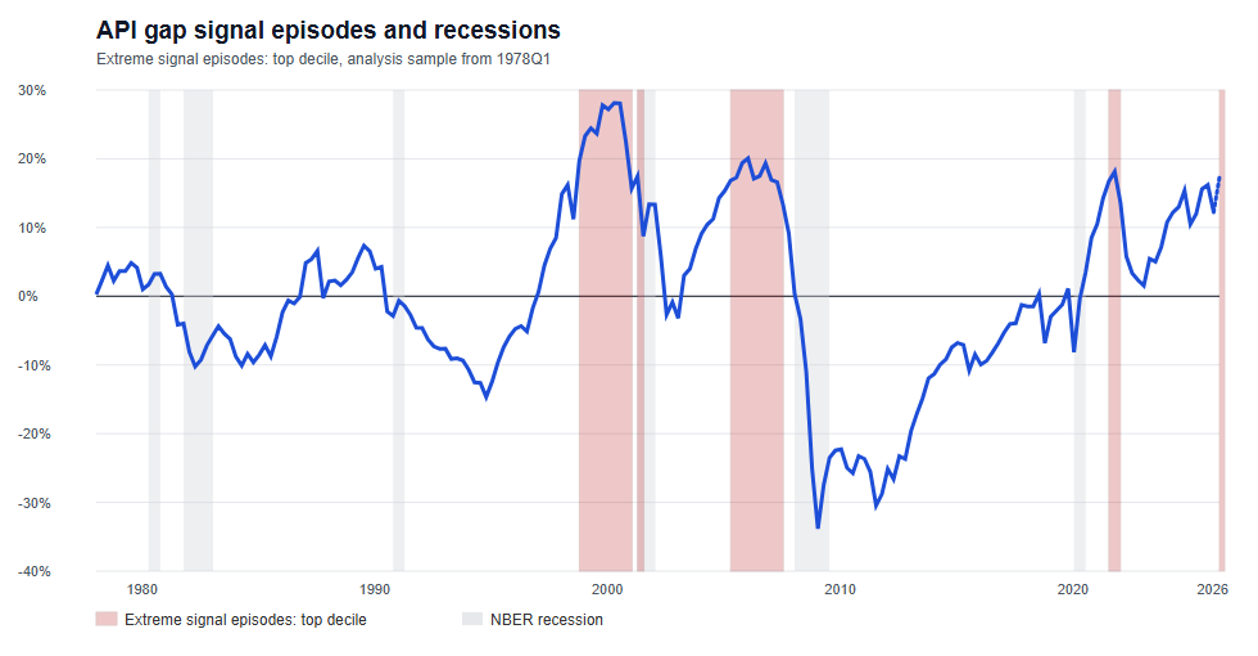

The Endpoint Problem: US Asset Prices, Investment and the Current Cycle

July 20, 2026 8:00 AM UTC

· Asset Price Index (API) framework suggests the US gap is elevated and, on some constructs, has moved into top-decile territory.

· The question is whether prices, capex and financing conditions are beginning to reinforce the same cyclical risk-accumulation dynamics.

·

The Fed's Balance Sheet: Revolution or Recalibration

August 3, 2026 9:18 AM UTC

· Fed chair Warsh has reopened the question of how the Federal Reserve implements monetary policy, not just the size of the balance sheet. The two go hand in hand.

· The realistic choice is not between today's balance sheet and a return to 2006, but among several ways of o

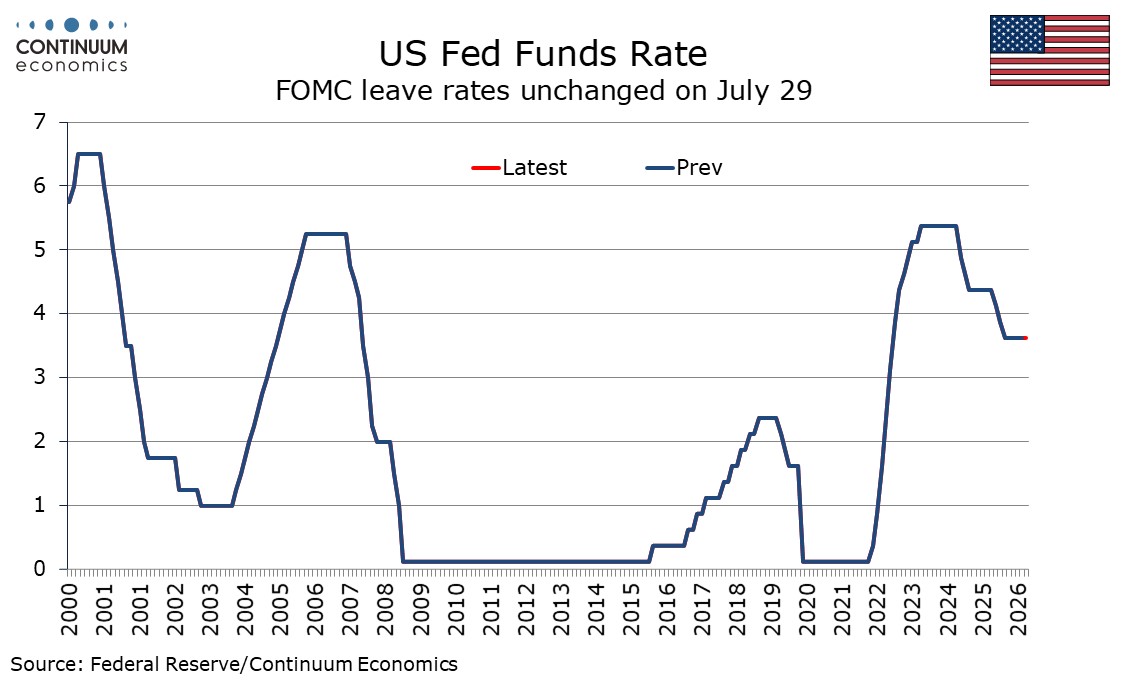

FOMC - Warsh leaves markets confused

July 29, 2026 7:30 PM UTC

That this FOMC meeting showed a 9-3 vote for unchanged policy, with the dissents being for tightening, shows there was a case for tightening and a case for steady policy. However, the press conference from Chairman Warsh gave little insight on the nature of the debate, talking a lot about how the Fe

Iran/U.S.: A New War or Escalating to Deescalate?

July 14, 2026 10:40 AM UTC

· Our baseline remains that the MOU will hold and that the Strait of Hormuz will reopen. Iran can be pressured economically by the U.S. naval blockade being re-established. Additionally, President Trump loves to escalate to de-escalate to get a deal. This is a 60% probability scenar

AI Equities: Correction/Consolidation?

August 5, 2026 7:40 AM UTC

• Overall, we feel that recent movements have been a correction/consolidation in the AI equity story. AI specific revenue growth still remains healthy and will support multi-year plans over cloud computing growth and in turn semiconductor demand. Even so, slowing free cash flows and ove

Preview: Due August 7 - U.S. July Employment (Non-Farm Payrolls) - Stronger than June, but with a rise in unemployment

August 6, 2026 1:27 PM UTC

We expect July’s non-farm payroll to rise by 120k overall and by 110k in the private sector, a significant improvement from June’s respective gains of 57k and 49k but largely explained by a recovery in leisure and hospitality. We expect unemployment to rise to 4.3% from 4.2%, reversing a June de

Trump: Tariffs 2.0

July 24, 2026 7:16 AM UTC

• Replacing section 122 at 10% with section 301 at 10-12.5% is unlikely to have much lasting economic impact in itself. However, the Trump administration are also undertaking section 301 investigation against 16 countries on excess production, with the report and new tariffs expected in A

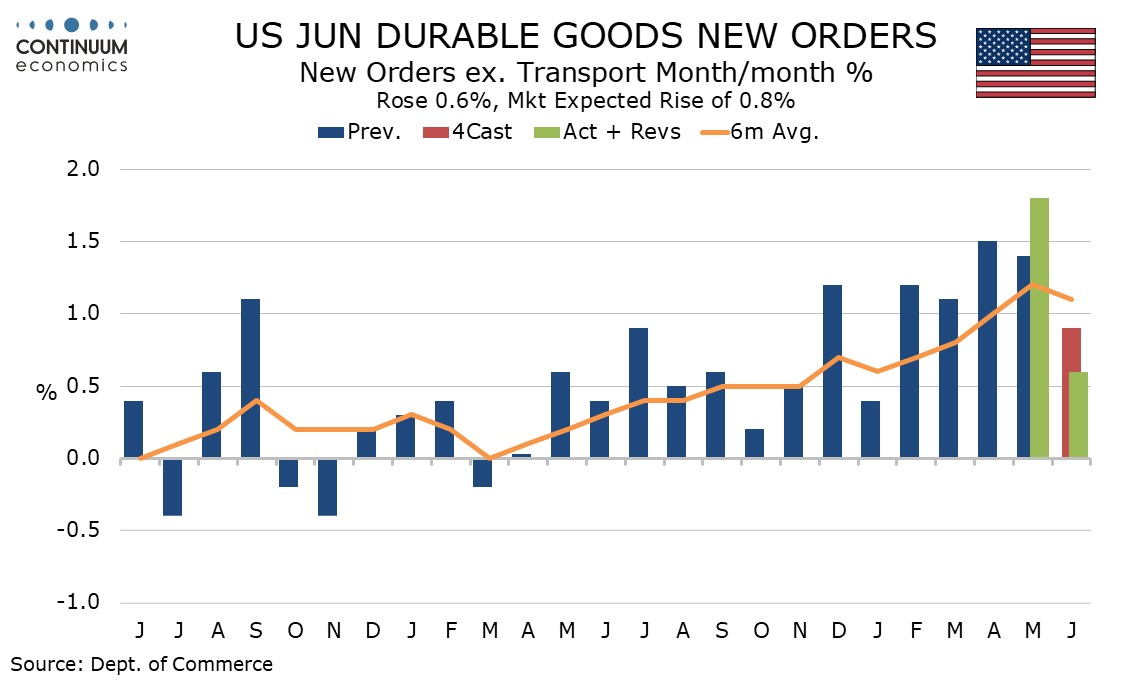

U.S. June Durable Goods Orders - Restrained by seasonal adjustments and possibly prices

July 27, 2026 12:49 PM UTC

June durable goods orders with a 0.3% rise were well below expectations with a bounce in aircraft orders implied by Boeing data failing to show up in seasonally adjusted data while the ex transport gain of 0.6% was the slowest since January, though this may in part reflect easing price pressures.

CHF/JPY and the carry question

July 30, 2026 1:39 PM UTC

· CHF/JPY has become interesting from several directions: extreme relative valuation, changing carry rankings, opposing official preferences over currency direction, and the beginnings of a possible technical rollover. When things align, they can encourage some migration in positioning

BOE: Split Does Not Mean September Hike

July 30, 2026 12:45 PM UTC

. · Overall, the July MPC minutes and monetary policy report/press conference suggest that the MPC is not convinced of a September hike and a worsening of energy price rises and/or 2nd round effects would be required to shift the voting to a 25bps hike. While the MPC has a hawkish

China: Debt Surge Problems

July 28, 2026 10:55 AM UTC

· China general government debt/GDP is on an unstable upward trend. China authorities are reluctant to ease underlying fiscal policy more than the already large primary budget deficit, but are also reluctant to consider broadening of income tax or property taxes that would help fiscal

Preview: Due July 20 - Canada June CPI - Energy to correct lower but BoC core rates seen mostly stable

July 17, 2026 5:39 PM UTC

We expect June Canadian CPI to correct lower to 3.0% yr/yr from May’s 3.2% which was the highest since December 2023, with a slowing to 2.98% from 3.23% before rounding. The Bank of Canada’s core rates however are likely to remain mostly stable with CPI-Median at 2.1% and CPI-Trim at 2.0%, both

Japan’s GPIF: Can it turn back the clock on the yen?

July 13, 2026 11:45 AM UTC

· The GPIF story is not that one public fund can singlehandedly ‘rescue the yen’. The question is more whether Japan can use one of the central institutions that helped drive the Abenomics flow-of-funds regime revolution to change the narrative, re-influence domestic allocation and

ECB: September Hike 50% Probability?

July 23, 2026 1:41 PM UTC

· Lagarde disclosed that some ECB board members considered a hike at today’s meeting and she noted that the consensus was to wait for incoming data before the September 10 meeting and then reassess. This clearly signals that the September meeting will seriously consider a 25bps hike,

FOMC Preview for July 29: Unchanged policy with an unspoken tightening bias

July 15, 2026 3:52 PM UTC

The FOMC meets on July 29 in a meeting that will see no update to the dots or economic forecasts. With forward guidance now becoming limited all meetings should be seen as live, but after softer than expected June non-farm payroll and more importantly CPI data, a change in policy looks unlikely at t

Slicing and dicing US inflation – why different measures are at the centre of Fed debate

August 10, 2026 1:01 PM UTC

* Wide divergence of US inflation measures becoming increasingly material to policy debate and sets the unusual statistical backdrop to the next CPI release

* Reflects many of the divergent opinions over AI, ‘relative price adjustment’ vs generalised inflation, temporary vs persistent overshoot.

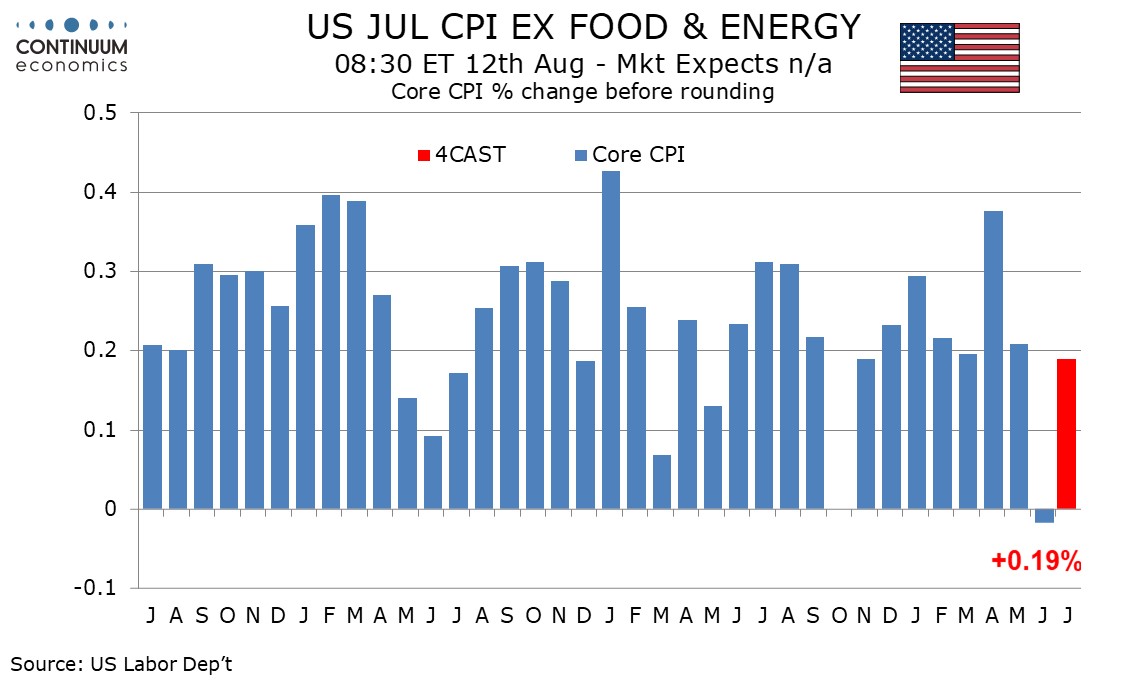

Preview: Due August 12 - U.S. July CPI - Another subdued month, if less so than June

July 31, 2026 3:52 PM UTC

We expect a subdued July CPI, up by 0.1% overall and 0.2% ex food and energy, with the respective gains before rounding being only 0.06% and 0.19%. This will however be less weak than June’s 0.4% decline overall, with the June core rate ex food and energy having been unchanged.

U.S. Q2 GDP strong outside net exports, inventories and government

July 30, 2026 1:28 PM UTC

The advance estimate of Q2 GDP at 1.5% annualized is weaker than the market expected but in line with our 1.4% call. The detail is also broadly in line with our expectations, healthy excluding negatives from inventories and net exports, with final sales to domestic buyers (GDP ex inventories and net