BoE Preview (Aug 7): Labour Market Softness to Trigger Further Cut, But Fiscal Risks Loom

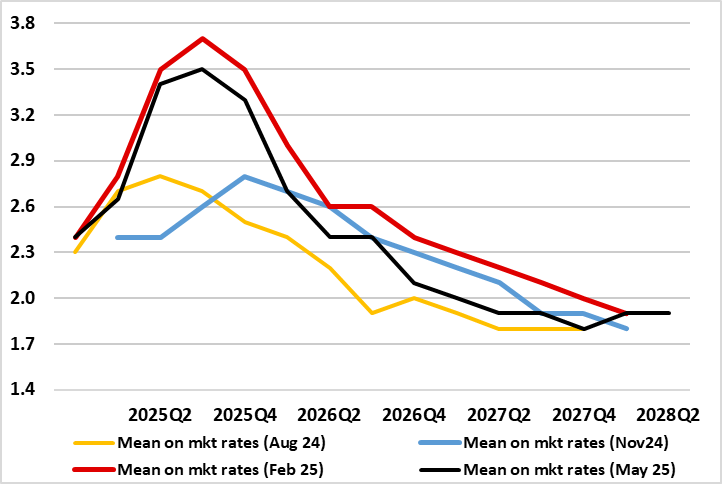

After what was widely considered to be a dovish hold at the last (June) MPC meeting (Bank Rate staying at 4.25%) which saw three dissents in favor of easing at that juncture, a 25 bp reduction is very much on the cards for the August decision. Likely to discuss its two alternative scenarios still, it is clear that previous MPC concerns about a ‘tight’ labor market have been diluted. But the hawks may stress a possibly slightly less unfavourable trade outlook given the ‘deal’ with the U.S. as well as higher CPI inflation numbers. Even so, beyond even softer labor market numbers (Figure 2), there are other concerns that the BoE will have to consider, not least signs of consumer dissaving (Figure 3) and a likely further and possibly marked fiscal tightening. The problem is that neither, because of a lack of detail, can be incorporated into the updated BoE projections. Thus, the message from those projections, likely still to show inflation below target perhaps only from 2027 (Figure 1) may be misleading although likely to mean that ostensibly the Monetary Policy Statement will still repeat the need for policy to be framed carefully as well as gradually.

Figure 1: BoE Projections to Suggest Still-Deferred Inflation Back Below Target

Source: BoE, CE, last four Monetary Policy Report vintages

Gauging Restriction

It is also likely to see the MPC repeating that monetary policy will need to continue to remain restrictive for sufficiently long – the question being whether those recent dissenters reject this line of thinking – and there may be a three-way split this time around. Back in June, partly based on what was seen as a ‘material further loosening in labour market conditions’, Dep Governor Ramsden (as he did twice in 2024) dissented in favor of a 25 bp rate cut, thereby adding to the more longstanding such demands from his colleagues Taylor and Dhingra. But the issue of what constitutes restriction is also important (recently, the lower BoE policy rate has not stopped there being tighter financial conditions) as it should help determine how much further and when the BoE eases.

We think that with the BoE regarding neutral policy rate as being well above 3%, two further 25 bp moves this year will be followed by another 50 bp in H1 2026. But we consider the risks are for deeper and possibly faster cuts as we think the BoE is both over optimistic about growth prospects and over-estimating policy neutrality – NB a recent IMF insight pointed to Bank Rate bottoming at 3% and averaging just 3.2% next year, ie well below market thinking. One question here is if the BoE slows its QT program, as we assume, will this have any overt bearing on conventional policy – we think that the MPC in September will likely accept that to avoid impacting the monetary transmission mechanism that annual rundown of gilts needs to be slowed from GBP 100bln pa to GBP 75bln, the question being whether the August minutes reveal any early discussion on the subject.

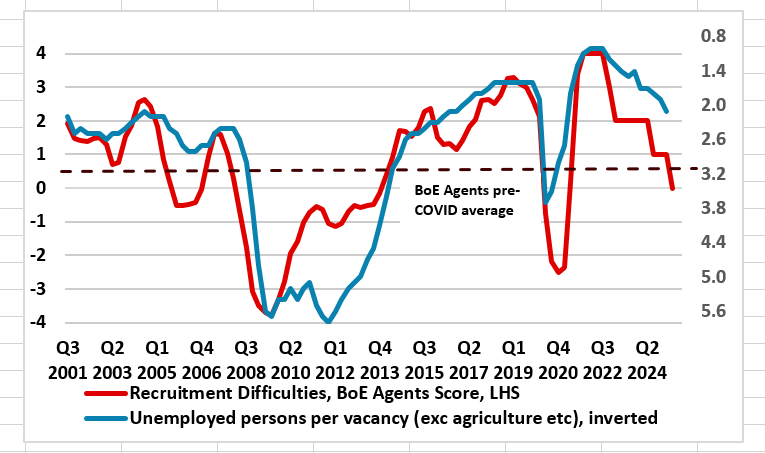

While BoE research seems to have reduced the tariff risk at least to the UK, it is clear that other global and domestic considerations have come to the fore instead. Indeed, the BoE still seems clear that global uncertainty remains elevated, and that energy prices have risen owing to an escalation of the conflict in the Middle East, but some on the MPC may regard higher oil (and now also food) prices ultimately to be disinflationary given the damage they would wreak to spending power. The latter issue is an increasingly complicated one as we think recent data very much suggests that the UK labor market that is now not so much less tight but decidedly loose. Indeed, we would assert that the official data is still underplaying the extent of emerging labor market slack in contrast to the BoE’s own survey data which is consistent with increasing spare capacity, now well above pre-COVID levels (Figure 2) – an update will be available to the MPC from its fresh Decision Makers Survey.

Figure 2: BoE Numbers Suggest Increasing and Above Average Labor Market Slack

Source; ONS, BoE, CE

Consumers Dissaving!

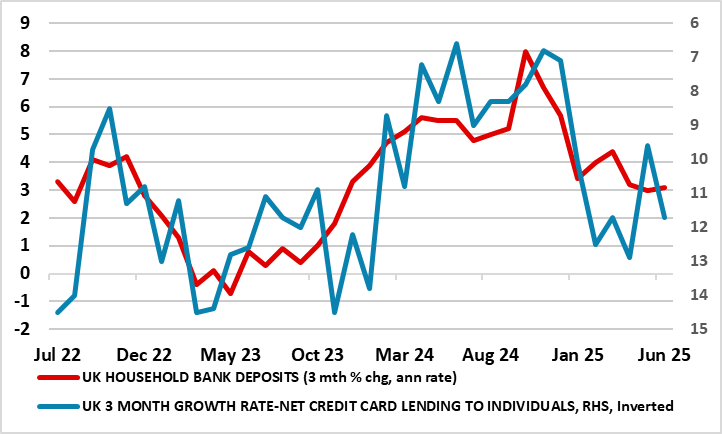

But there are also signs of consumer fragility. Indeed, it seems that households have been dissaving of late, both by accumulating fewer actual savings in their bank accounts but also by resorting to what may be an enforced surge in credit card usage (Figure 3). This is all the more important as it looks as if fiscal policy will be tightened in the autumn Budget; while there may be little direct tax rise for consumers, the overall package is likely to be broadly negative both on income and confidence effects. The problem here is that neither of these two issues can be formally incorporated it to the BoE’s updated projections, the former being too undefined while the BoE can only use existing government fiscal projections, not try and anticipate significant changes. All of which will makes the updated projection less relevant.

Figure 3: Households Saving Less and Borrowing More

Source; ONS, BoE, CE

Regardless, the MPC also noted its sensitivity to heightened unpredictability in the economic and geopolitical environment, and will continue to update its assessment of risks to the economy, the question here being what does sensitivity actually imply. This is even more so given that the MPC regards the steer from surveys over recent months to have remained consistent with a zero to slightly positive pace of underlying growth currently, which may still be somewhat optimistic. Moreover, such surveys needed to be considered in the wider context of the supply side of the economy, and the opening up of slack in the labour market and within companies.

Scenario Building in Context?

It is clear that elevated uncertainty underscores the BoE thinking and projections but this does not explain recent MPC divisions that led to the three-way vote in May and the three dissents last time around. Instead, they merely reflect the impact that scenario building is having with it seemingly the case that policy hawks’ thinking chimes with the inflation persistence alternative while the dissenters put more emphasis on the downside risk. The question then is the new policy framework in the aftermath of the Bernanke Review actually backfiring as the scenario building it is based around is seemingly exacerbating divisions among policy-makers. Perhaps the very opposite is the case as the Review was partly designed to deter the kind of group-think that is far less prevalent presently! If so, it may make consistent and swift policy decision all the harder to come by – this adding to the case that making policy verdict outside of the four per year MPC meetings with updated forecasts less likely.