UK GDP Review: Conflicting Signs

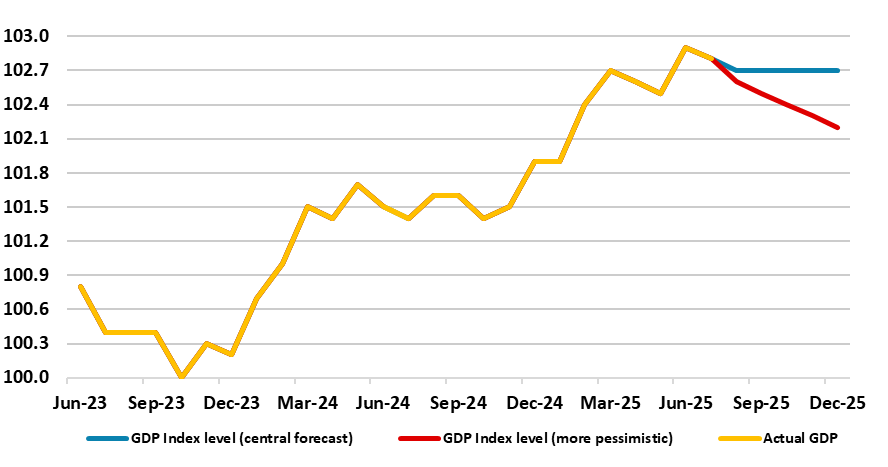

Although we are pointed to a flat m/m GDP outcome for the July data, thereby matching the official outcome, the actual outcome was a small m/m fall (before rounding). The three-month rate slowed a notch to 0.2% but we think this overstates what is very feeble momentum, which may actually be nearer zero. Even so, at this juncture, the strong June outcome of 0.4% has created a solid backdrop for the current quarter GDP to support the BoE’s 0.3% Q3 forecast – even successive 0.1% m/m declines would still leave the quarter up 0.1% in q/q terms, that is without what may still be likely revisions but his remains our projection.

Figure 1: GDP Growing Solidly – Alternative Scenarios?

Source: ONS, CE

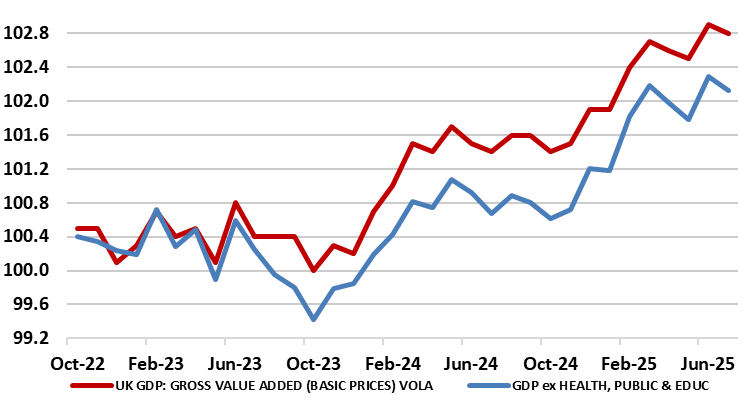

To what extent better weather in July GDP. The result was that the economy grew by 0.4% q/q in Q2 also higher than expected. But gauging the economy is all the more difficult given both conflicting signal and the extent to which the public sector has supported growth of late (Figure 2). The question is whether this latter factor will go in to reverse. As for conflicting signal this is best highlighted by recent headline regarding service sector surveys. Indeed, according to the CBO, activity across the services sector continues to weaken while August's PMI sees 'Steepest upturn in service sector output since April 2024'.

Figure 2: GDP Supported by Public Sector – But Can That Last?

Source: ONS, CE

I,Andrew Wroblewski, the Senior Economist Western Europe declare that the views expressed herein are mine and are clear, fair and not misleading at the time of publication. They have not been influenced by any relationship, either a personal relationship of mine or a relationship of the firm, to any entity described or referred to herein nor to any client of Continuum Economics nor has any inducement been received in relation to those views. I further declare that in the preparation and publication of this report I have at all times followed all relevant Continuum Economics compliance protocols including those reasonably seeking to prevent the receipt or misuse of material non-public information.