UK GDP Preview (Dec 12): Underlying Economy Fragile and Listless

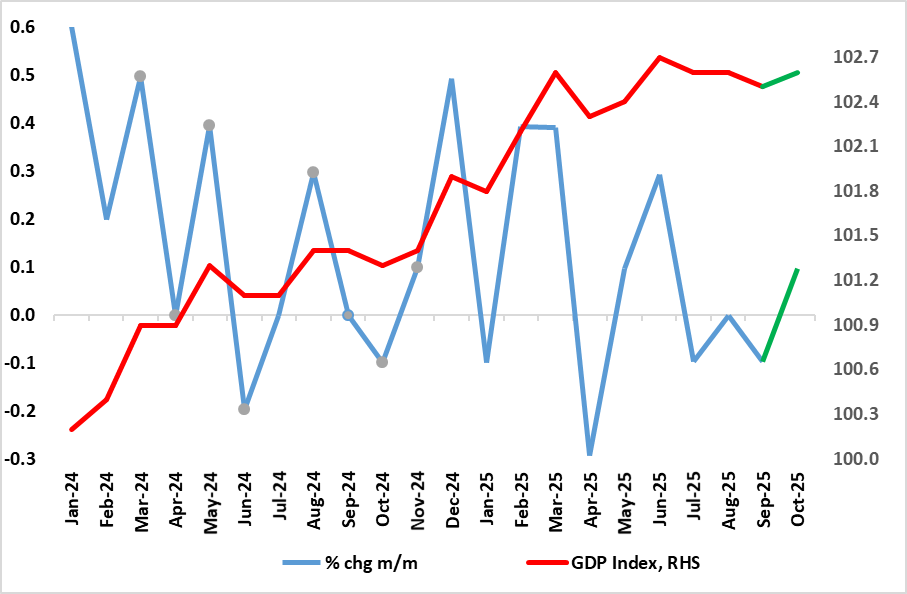

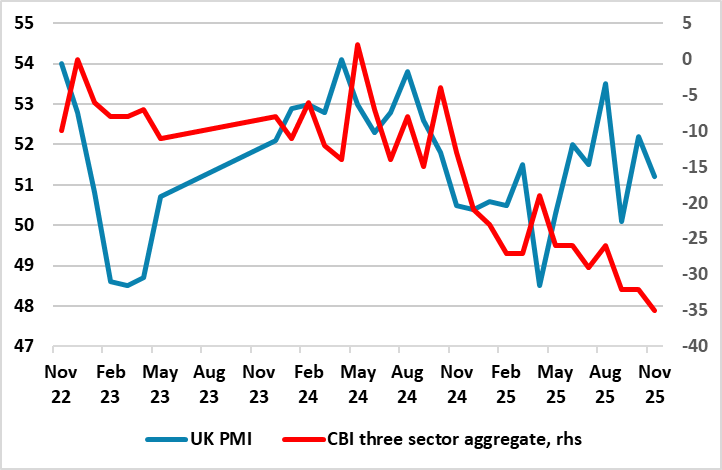

As we have underlined, GDP has hardly moved since March and this is un likely to change with the October GDP release. Indeed, it has fallen in two of the last three months (Figure 1), albeit where some recovery should be in store for the current quarter as the September numbers were hit (temporarily) by the cyber-attack at JLR vehicle manufacturing and by weather swings. But amid less friendly weather patterns and what have already been weak retail sales numbers as well as only a slow recovery on the vehicle side we see only a 0.1% m/m rise for October. Even with similar outcomes for the rest of the quarter, this points to Q4 GDP growth matching that of the previous quarter (ie 0.1% q/q), a projection well below the 0.3% projection of the BoE. This weakness chimes with what surveys still suggest (especially construction), namely the economy is at best moving sideways, and maybe contracting (Figure 2).

Figure 1: Solid GDP Growth Ebbing?

Source: ONS, CE

Revisions up to September GDP data now confirm small m/m falls in two of the last three months of data. This put the less volatile three-month rate at a 10-mth low of 0.1% (ie also equivalent to the Q3 result) which we think this reflects very feeble momentum, which may actually be nearer zero if not weaker at least according to some business survey data, especially once ever-clearer construction weakness is incorporated. Indeed, GDP has hardly moved since March. Admittedly, solid GDP outcomes early in the year suggest that UK GDP growth in 2025 will be around 1.4% - the highest in the G7 according to the IMF but this masks what is very much a weak(er) picture in per capita terms, this being a politically important issue amid current immigration issues. Indeed, the IMF see a cumulative per capita growth of 0.9% for 2025 and 2026, the weakest in the DM world save for a similar soggy outlook for Germany. Regardless, the 0.8% GDP projection we have penciled in for next year actually constitutes some modest pick-up in activity momentum.

Figure 2: Surveys More Negative?

Source: ONS, CE, CBI, Markit

To what extent better weather has helped prevent a more discernible weakening of late GDP is unclear. But gauging the economy is all the more difficult given both conflicting signals and the extent to which the public sector has supported growth and employment of late. The question is whether this latter factor will go in to reverse, sooner but probably later – health sector jobs already seem to be being shed.

I,Andrew Wroblewski, the Senior Economist Western Europe declare that the views expressed herein are mine and are clear, fair and not misleading at the time of publication. They have not been influenced by any relationship, either a personal relationship of mine or a relationship of the firm, to any entity described or referred to herein nor to any client of Continuum Economics nor has any inducement been received in relation to those views. I further declare that in the preparation and publication of this report I have at all times followed all relevant Continuum Economics compliance protocols including those reasonably seeking to prevent the receipt or misuse of material non-public information.