UK CPI Review: A Pause Before a Peak?

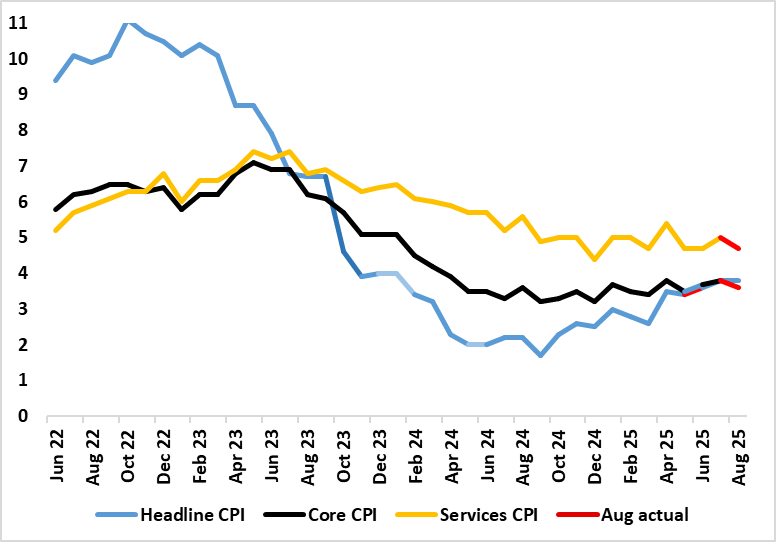

After the upside (and broad) June CPI surprise, CPI inflation rose further, up another 0.2 ppt to 3.8% in July, higher than the consensus but matching BoE thinking. Despite adverse rounding and fuel (and food) costs, the headline stayed there in the August figure, this foreshadowing a likely rise this month to what we (and the BoE think) will be the inflation peak in September of 4.0%. The August data was as expected as was the core rate, down 0.2 ppt to three-month low of 3.6% (Figure 2). After some further aberrant factors, the rate in August saw services inflation reverse the rise to 5.0% in July, back down to 4.7%. Notably, in adjusted terms of late (Figure 2), with the recent rise in headline inflation driven more by goods.

Figure 1: Headline to Nudge Higher Still, Core Stable?

Source: ONS, Continuum Economics

The July and now August CPI headline are the highest since January last year. The notable further 0.3 ppt rise in services inflation to 5.0% was also largely in line with BoE thinking, but reflected several special factors (airfares) as does the fall back this time around, albeit where the further rise in restaurants inflation possibly a result of tax-induced labor costs feeding through. Even so, the inflation rise in the last 2-3 months is far from broad as it reflected upward contributions from six (of 12) divisions, partially offset by downward contributions from six divisions, but where some BoE hawks will deduce signs of inflation persistence.

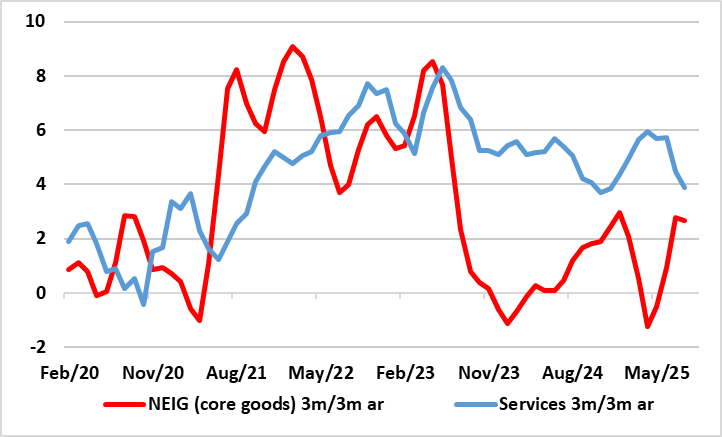

Figure 2: Inflation Boosted by Goods, Not Services?

Source: ONS, Continuum Economics

In fact, while all the media and policy attention has been apparently stubborn services inflation, the latter has been easing, this more discernible in m/m adjusted terms, with the recent rise in headline inflation driven more by goods. Notably, while relatively broad, goods inflation has been pushed higher largely by food and energy, neither of which seem to be demand driven. Clearly, higher food inflation is a worry to the BoE as will the energy rise, the latter partly driven by the UK’s peculiar method of estimation. But it can be argued that both food and energy being both non-discretionary are adding to already strained consumer finances which we feel will continue to weigh on the real economy picture into 2026. But the main downside factor for the economy is the ailing labor market, data for which appeared yesterday; they showed still high wage numbers but with the (now officially accredited) HMRC showing continued job losses!

As for further BoE easing, it will be interesting how the MPC present the likely reduction in the QT program it may present tomorrow and the extent to which it underscores that the policy outlook will be driven (at least partly) by likely fiscal tightening made all the more likely by far from unexpected news regarding the economy. It seems that Chancellor Reeves has been warned by the OBR that its estimates for productivity are likely to be downgraded to a degree that could create/accentuate a total fiscal hole of perhaps over £30bn, which would thereby need budget cuts in order to meet spending induced fiscal rules. The question is whether an externally-decided decision on potential growth could make the Chancellor change her mind regarding the fiscal rules.

I,Andrew Wroblewski, the Senior Economist Western Europe declare that the views expressed herein are mine and are clear, fair and not misleading at the time of publication. They have not been influenced by any relationship, either a personal relationship of mine or a relationship of the firm, to any entity described or referred to herein nor to any client of Continuum Economics nor has any inducement been received in relation to those views. I further declare that in the preparation and publication of this report I have at all times followed all relevant Continuum Economics compliance protocols including those reasonably seeking to prevent the receipt or misuse of material non-public information.