View:

July 24, 2026

Trump: Tariffs 2.0

July 24, 2026 7:16 AM UTC

• Replacing section 122 at 10% with section 301 at 10-12.5% is unlikely to have much lasting economic impact in itself. However, the Trump administration are also undertaking section 301 investigation against 16 countries on excess production, with the report and new tariffs expected in A

July 23, 2026

ECB: September Hike 50% Probability?

July 23, 2026 1:41 PM UTC

· Lagarde disclosed that some ECB board members considered a hike at today’s meeting and she noted that the consensus was to wait for incoming data before the September 10 meeting and then reassess. This clearly signals that the September meeting will seriously consider a 25bps hike,

July 22, 2026

BOE Preview: Hawkish Noises

July 22, 2026 6:12 AM UTC

• The BOE will likely maintain a hawkish bias on July 30, but are unlikely to signal a September hike. The June CPI did not really change this picture, with the core unchanged at 2.6%. Though BOE Bailey recently noted the unstable process (in the Straits of Hormuz and for energy prices), he

BOE Preview After CPI: Hawkish Noises

July 22, 2026 6:11 AM UTC

• The BOE will likely maintain a hawkish bias on July 30, but are unlikely to signal a September hike. The June CPI did not really change this picture, with the core unchanged at 2.6%. Though BOE Bailey recently noted the unstable process (in the Straits of Hormuz and for energy prices), he

July 21, 2026

UK Fiscal Policy and the New Chancellor

July 21, 2026 6:18 AM UTC

· Apprehension will exist until the Autumn budget, despite a repeated commitment by PM Burnham to stick to the fiscal rules. Spending commitments are clearer than tax raises measures, while new Chancellor Healey may not be strong enough to curtail spending pressures. This could mean

July 20, 2026

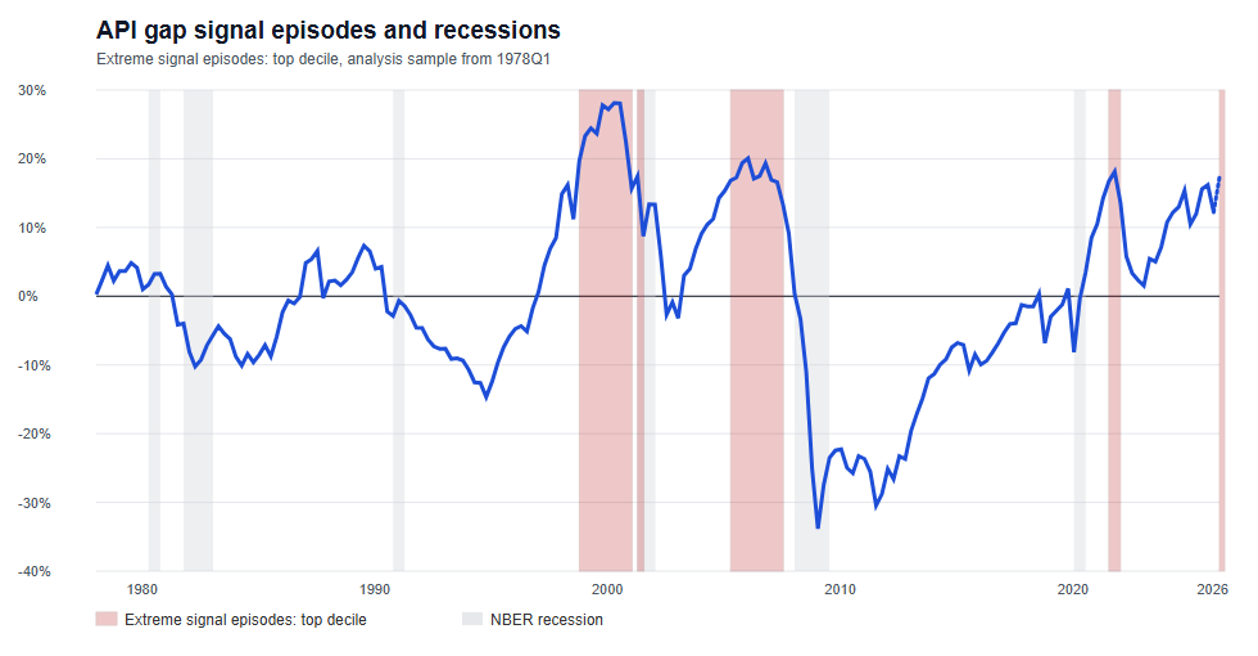

The Endpoint Problem: US Asset Prices, Investment and the Current Cycle

July 20, 2026 8:00 AM UTC

· Asset Price Index (API) framework suggests the US gap is elevated and, on some constructs, has moved into top-decile territory.

· The question is whether prices, capex and financing conditions are beginning to reinforce the same cyclical risk-accumulation dynamics.

·

July 17, 2026

ECB: Bark No Bite

July 17, 2026 7:05 AM UTC

· The vigilance mantra means that the ECB will still have a broad caution against 2nd round effects and the risks that energy prices could push higher. We feel that the June inflation data, plus the prospect that Iran/U.S. could call a new truce (here) will be enough to make most on t

July 16, 2026

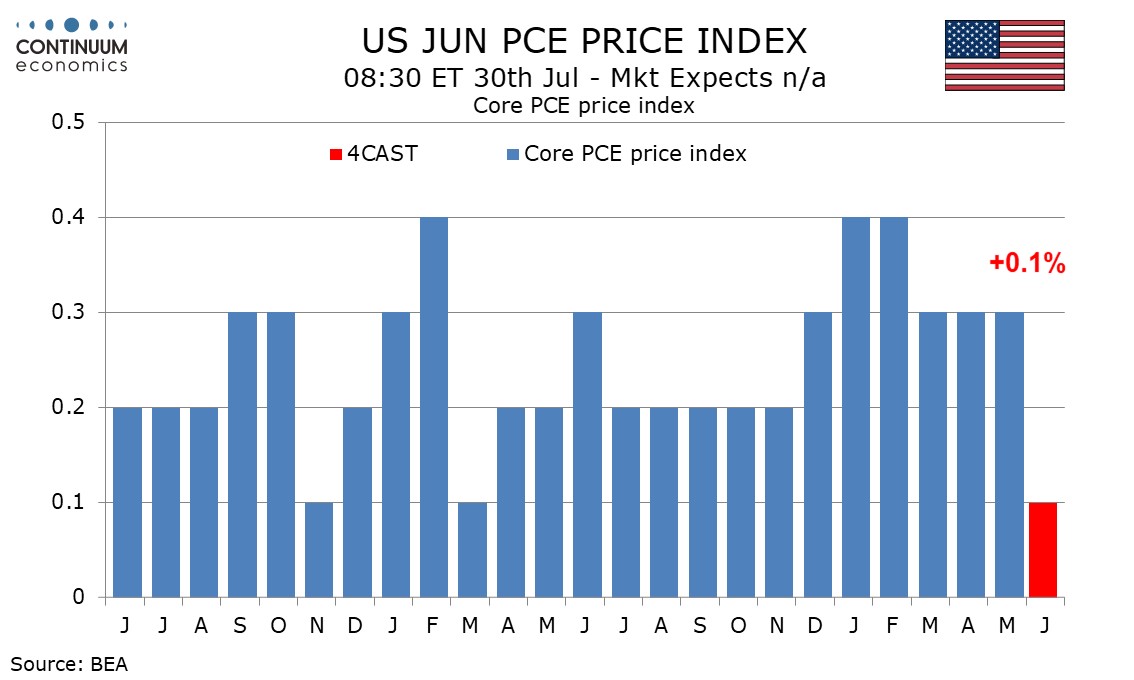

Preview: Due July 30 - U.S. June Personal Income and Spending - PCE Prices not quite as soft as CPI

July 16, 2026 4:22 PM UTC

June’s personal income and spending report may be overshadowed by the Q2 GDP report released at the same time. We expect a subdued 0.1% increase in core PCE prices, with overall PCE prices down by 0.1%, leaving gains of 0.3% in both personal income and personal spending looking respectable in real

Preview: Due July 30 - U.S. June Personal Income and Spending - PCE Prices not quite as soft as CPI

July 16, 2026 4:21 PM UTC

June’s personal income and spending report may be overshadowed by the Q2 GDP report released at the same time. We expect a subdued 0.1% increase in core PCE prices, with overall PCE prices down by 0.1%, leaving gains of 0.3% in both personal income and personal spending looking respectable in real

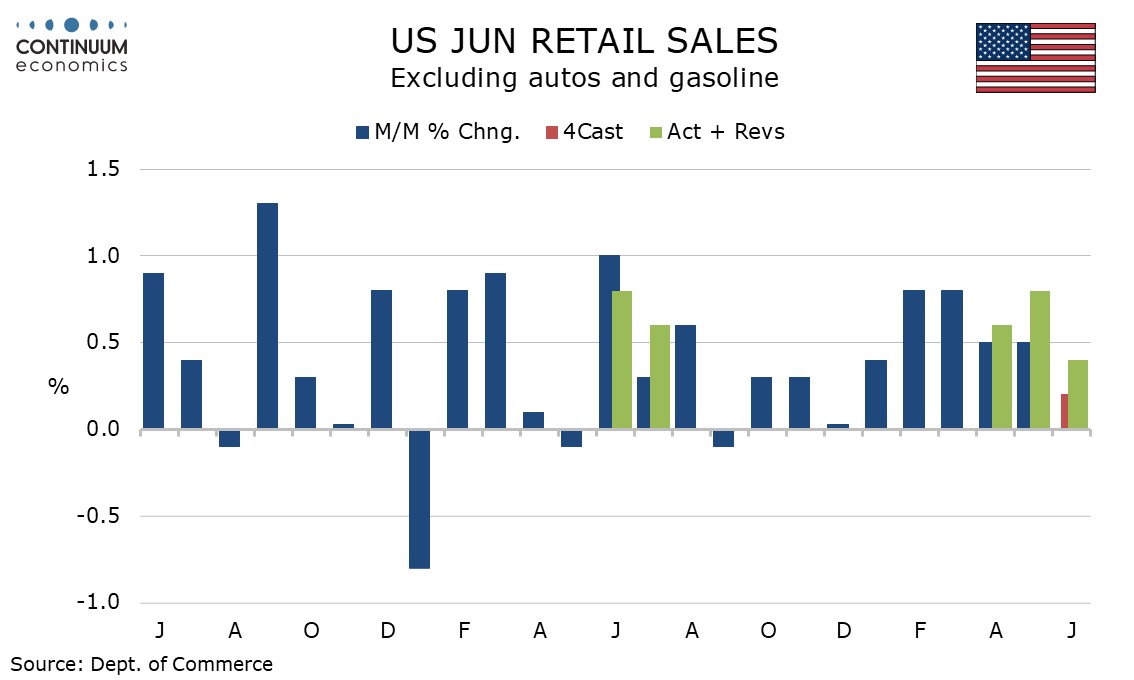

U.S. June Retail Sales - Underlying resilience persists, Initial Claims fall and Philly Fed surges

July 16, 2026 1:11 PM UTC

The latest US data is on the firm side of expectations. June retail sales are in line with expectations with a 0.2% increase and a gasoline-led 0.2% decline ex autos., but the control group that contributes to GDP maintains underlying strength with a rise of 0.5%. Weekly initial claims at 208k from

U.S. June Retail Sales - Underlying resilience persists, Initial Claims fall and Philly Fed surges

July 16, 2026 1:09 PM UTC

The latest US data is on the firm side of expectations. June retail sales are in line with expectations with a 0.2% increase and a gasoline-led 0.2% decline ex autos., but the control group that contributes to GDP maintains underlying strength with a rise of 0.5%. Weekly initial claims at 208k from

July 15, 2026

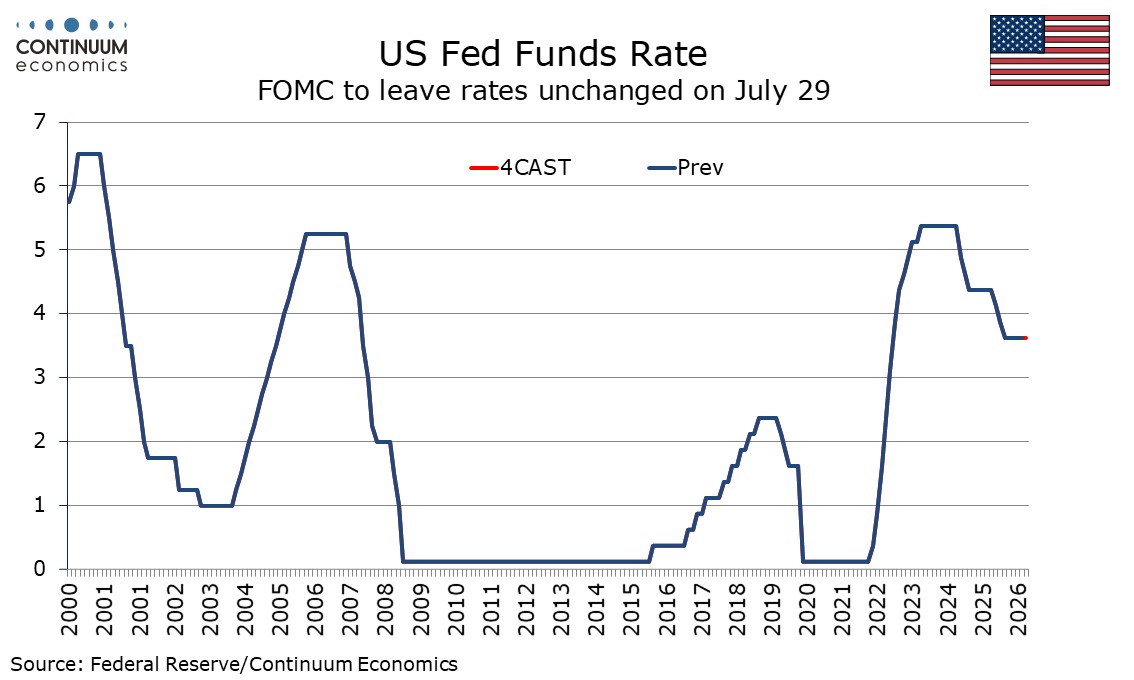

FOMC Preview for July 29: Unchanged policy with an unspoken tightening bias

July 15, 2026 3:52 PM UTC

The FOMC meets on July 29 in a meeting that will see no update to the dots or economic forecasts. With forward guidance now becoming limited all meetings should be seen as live, but after softer than expected June non-farm payroll and more importantly CPI data, a change in policy looks unlikely at t

FOMC Preview for July 29: Unchanged policy with an unspoken tightening bias

July 15, 2026 3:49 PM UTC

The FOMC meets on July 29 in a meeting that will see no update to the dots or economic forecasts. With forward guidance now becoming limited all meetings should be seen as live, but after softer than expected June non-farm payroll and more importantly CPI data, a change in policy looks unlikely at t

AI Optimism and Credit Markets?

July 15, 2026 8:05 AM UTC

· The AI trade in financial markets is also a question of credit markets, given the scale of financing needs is using up hyperscalers free cash flow at a rapid rate and the AI labs heavy financing requirements. Credit markets could become more sensitive, if the AI labs revenue growth sl

July 14, 2026

FOMC Preview for July 29: Unchanged policy with an unspoken tightening bias

July 14, 2026 5:14 PM UTC

The FOMC meets on July 29 in a meeting that will see no update to the dots or economic forecasts. With forward guidance now becoming limited all meetings should be seen as live, but after softer than expected June non-farm payroll and more importantly CPI data, a change in policy looks unlikely at t

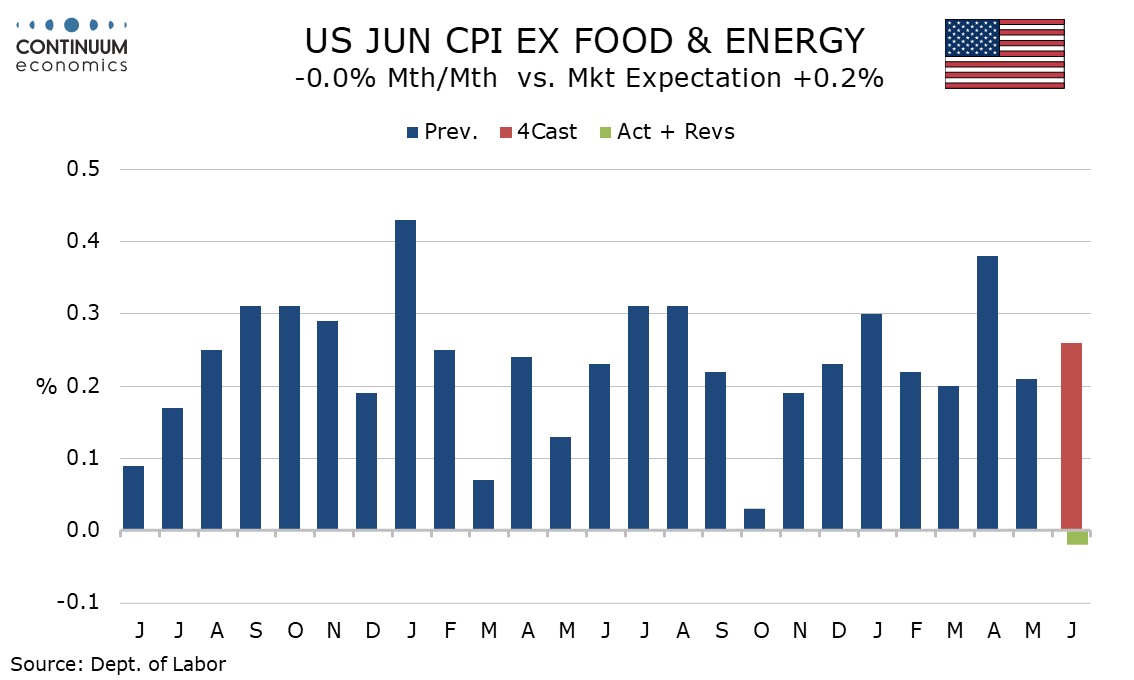

U.S. June CPI - Some volatile moves, but a clear relief for the Fed

July 14, 2026 3:16 PM UTC

June CPI is significantly softer than expected, both on the -0.4% headline and an unchanged outcome ex food and energy, with the respective figures before rounding being -0.422% and -0.017%. While there are a number of volatile declines in the breakdown and recent events in the Middle East present r

U.S. June CPI - Some volatile moves, but a clear relief for the Fed

July 14, 2026 1:12 PM UTC

June CPI is significantly softer than expected, both on the -0.4% headline and an unchanged outcome ex food and energy, with the respective figures before rounding being -0.422% and -0.017%. While there are a number of volatile declines in the breakdown and recent events in the Middle East present r

Iran/U.S.: A New War or Escalating to Deescalate?

July 14, 2026 10:40 AM UTC

· Our baseline remains that the MOU will hold and that the Strait of Hormuz will reopen. Iran can be pressured economically by the U.S. naval blockade being re-established. Additionally, President Trump loves to escalate to de-escalate to get a deal. This is a 60% probability scenar

July 13, 2026

Mexico: Fiscal Consolidation and Reducing Real Yields

July 13, 2026 9:55 AM UTC

· 10yr real yields in Mexico are currently high at 5%, given a moderate fiscal trajectory and some government action towards fiscal reform (though the judicial reforms have been criticized by global investors, the reality is no major political manipulation). 10yr nominal yields could

July 07, 2026

China LGFV Repair Rather Than Reboot

July 7, 2026 9:45 AM UTC

• Our assessment is that this ongoing exercise will likely have a small boost to GDP growth. LGFV’s debt restructuring could allow some new borrowing, but the big issue is that LGFV and LG finances are dependent on one off property taxes with the building of new property. The overhang

July 06, 2026

July 03, 2026

EM Government Debt Sinners and Saints

July 3, 2026 1:05 PM UTC

· Overall, the clearest EM fiscal sinner is Brazil, given its tax revenue/GDP ratio is already very high and requires politically sensitive expenditure cuts after the October election to increase the primary surplus to stabilize the government debt/GDP trajectory and get real bond yield

July 02, 2026

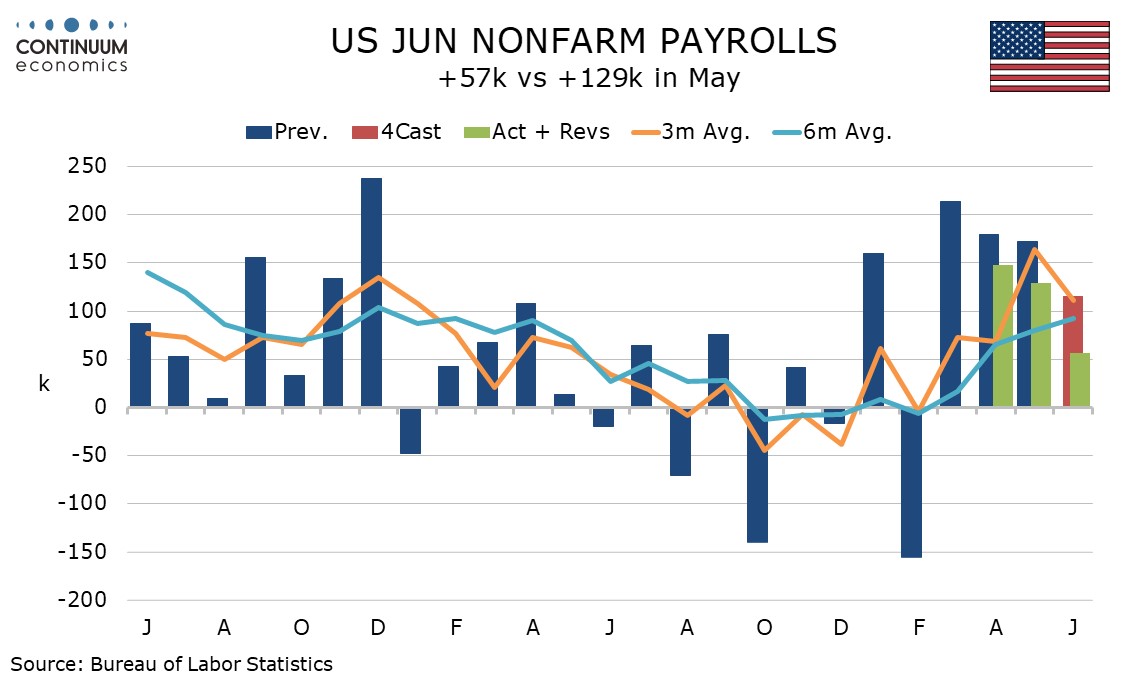

U.S. June Employment - Upside May surprise offset, but unemployment falls on lower labor force

July 2, 2026 1:20 PM UTC

June’s non-farm payroll is weaker than expected with a 57k increase, 49k private, with downward revisions to April and May. The slowing is consistent with an upturn in the initial and continued claims trends, though both were almost unchanged (-1k to 215k and +2k to 1.814m respectively) in the l

U.S. June Employment - Upside May surprise offset, but unemployment falls on lower labor force

July 2, 2026 1:12 PM UTC

June’s non-farm payroll is weaker than expected with a 57k increase, 49k private, with downward revisions to April and May. The slowing is consistent with an upturn in the initial and continued claims trends, though both were almost unchanged (-1k to 215k and +2k to 1.814m respectively) in the l

July 01, 2026

EZ HICP Review: Absence Second-Round Effects Continues

July 1, 2026 1:42 PM UTC

Contrary to some thinking, EZ HICP inflation continues to behave, both absolutely and relatively – ie to what looks ever excessive ECB price thinking. The question must be if and when the ECB chooses to note friendlier price and costs signals, rather than pander to the upside prices risks that o