View:

Preview: Due August 11 - U.S. July Existing Home Sales - Surveys suggest slippage

July 30, 2026 7:43 PM UTC

We expect July existing home sales to see a second straight monthly fall, by 1.5% to 4.03m, as fears that the next Fed move is likely to be a hike pick up, while remaining in the year to date range.

Preview: Due August 4 - U.S. June Trade Balance - Deficit to correct lower, but remain large

July 30, 2026 2:38 PM UTC

We expect a June trade deficit of $73.5bn, down from $77.6bn in May which was the widest since a record pre-tariff deficit in March 2025, but still significantly above the deficits seen in the first four months of 2026, each of which was close to $55bn.

Preview: Due July 31 - U.S. Q2 Employment Cost Index - Losing momentum

July 30, 2026 1:57 PM UTC

We look for the Q2 employment cost index (ECI) to increase by 0.7%, slower than Q1’s 0.9% but matching the Q4 outcome. This would see the yr/yr pace slow to 3.2% from 3.4%, reaching its slowest since Q2 2021.

CHF/JPY and the carry question

July 30, 2026 1:39 PM UTC

· CHF/JPY has become interesting from several directions: extreme relative valuation, changing carry rankings, opposing official preferences over currency direction, and the beginnings of a possible technical rollover. When things align, they can encourage some migration in positioning

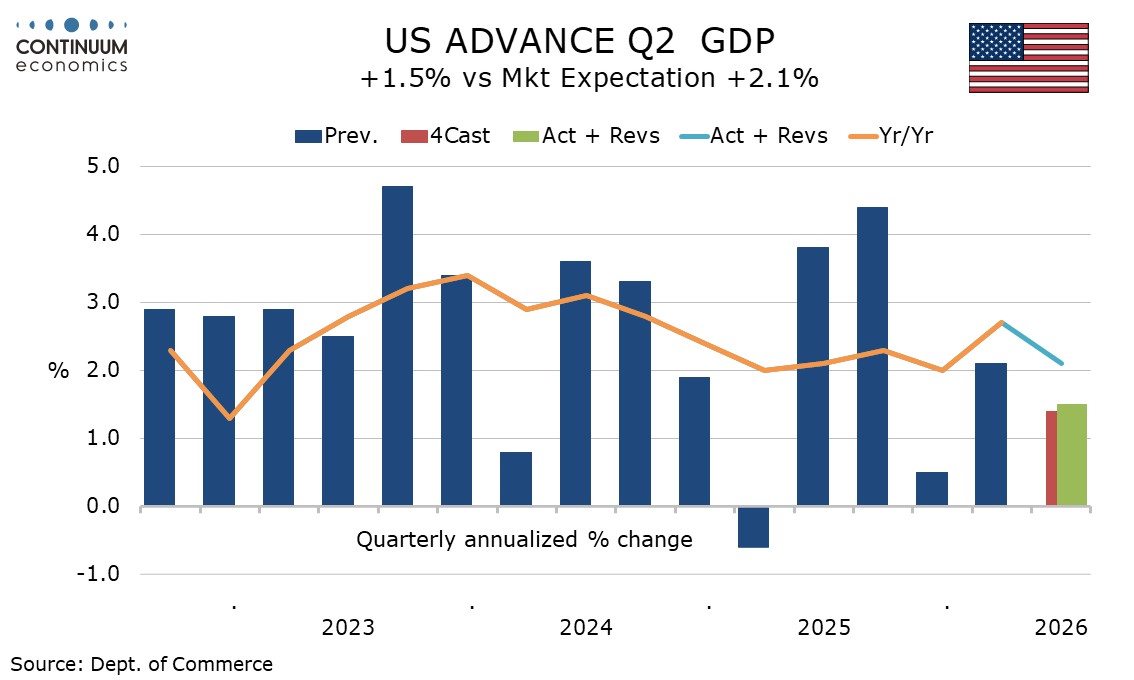

U.S. Q2 GDP strong outside net exports, inventories and government

July 30, 2026 1:28 PM UTC

The advance estimate of Q2 GDP at 1.5% annualized is weaker than the market expected but in line with our 1.4% call. The detail is also broadly in line with our expectations, healthy excluding negatives from inventories and net exports, with final sales to domestic buyers (GDP ex inventories and net

U.S. Q2 GDP strong outside net exports, inventories and government

July 30, 2026 1:28 PM UTC

The advance estimate of Q2 GDP at 1.5% annualized is weaker than the market expected but in line with our 1.4% call. The detail is also broadly in line with our expectations, healthy excluding negatives from inventories and net exports, with final sales to domestic buyers (GDP ex inventories and net

BOE: Split Does Not Mean September Hike

July 30, 2026 12:45 PM UTC

. · Overall, the July MPC minutes and monetary policy report/press conference suggest that the MPC is not convinced of a September hike and a worsening of energy price rises and/or 2nd round effects would be required to shift the voting to a 25bps hike. While the MPC has a hawkish

BOE: Split Does Not Mean September Hike

July 30, 2026 12:44 PM UTC

· Overall, the July MPC minutes and monetary policy report/press conference suggest that the MPC is not convinced of a September hike and a worsening of energy price rises and/or 2nd round effects would be required to shift the voting to a 25bps hike. While the MPC has a hawkish bias