View:

August 11, 2026

Taylor Rules for Uncertain Times

August 11, 2026 2:44 PM UTC

* The Fed’s rate puzzle has three awkward-shaped pieces: which inflation measure to trust, how much slack remains, and where r* now sits.

* Taylor rules may be deeply unfashionable, but they force those hidden assumptions into the open.

* Change only the inflation measure and the same rule can make

Preview: Due August 12 - U.S. July CPI - Another subdued month, if less so than June

August 11, 2026 12:50 PM UTC

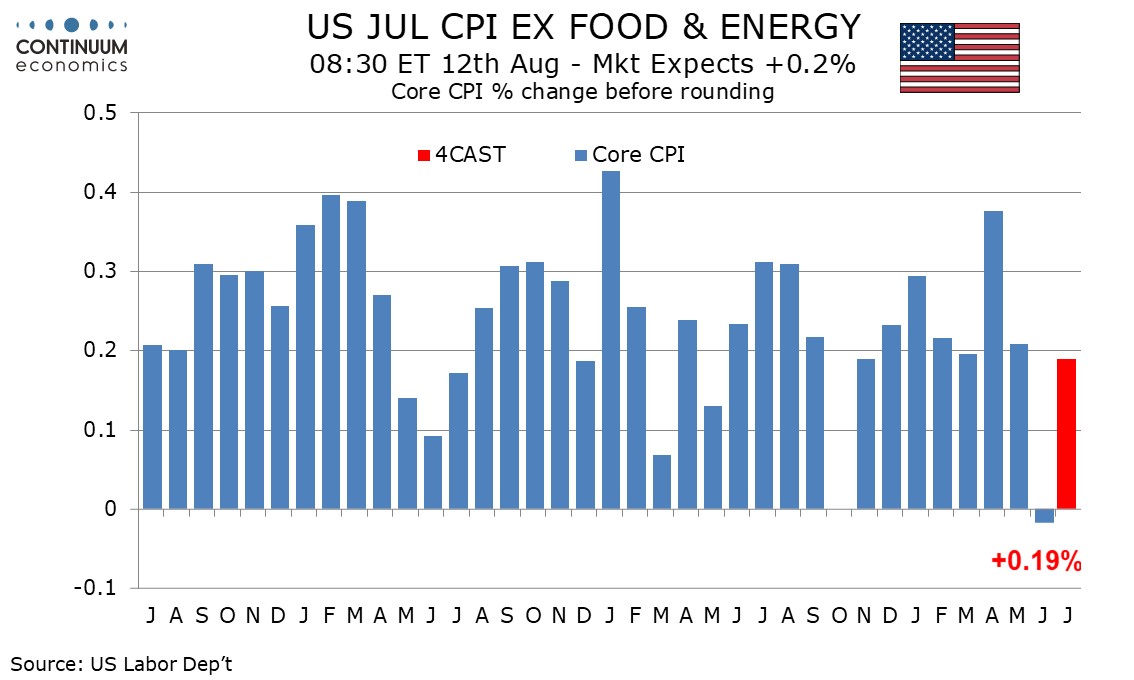

We expect a subdued July CPI, up by 0.1% overall and 0.2% ex food and energy, with the respective gains before rounding being only 0.06% and 0.19%. This will however be less weak than June’s 0.4% decline overall, with the June core rate ex food and energy having been unchanged.

Preview: Due August 12 - U.S. July CPI - Another subdued month, if less so than June

August 11, 2026 12:49 PM UTC

We expect a subdued July CPI, up by 0.1% overall and 0.2% ex food and energy, with the respective gains before rounding being only 0.06% and 0.19%. This will however be less weak than June’s 0.4% decline overall, with the June core rate ex food and energy having been unchanged.

U.S. July NFIB survey - Optimism on both labor market and prices

August 11, 2026 11:21 AM UTC

July’s NFIB survey of Small Business Optimism shows the optimism index at its highest since August 2025 at 99.8 from 97.4. Despite July’s weak payroll, respondents are more optimistic about the labor market while seeing reduced inflationary pressure.