Outlook

View:

July 06, 2026

June 25, 2026

June 24, 2026

Outlook Overview: Cyclical and Structural Forces

June 24, 2026 7:00 AM UTC

· The difference between 2nd round inflation effects from higher energy prices and 1st round effects that central banks can look through swings on whether the Straits of Hormuz will remain open in the coming months after the U.S./Iran interim agreement (here). Despite some tensions, we

China and EM Asia Outlook: Divergent Trends

June 24, 2026 6:22 AM UTC

· China’s growth momentum is being sustained by AI/tech and green energy production and investment. However, growth is imbalanced with modest consumption growth, due to adverse housing wealth effects and slow wage/job growth. Overall, we forecast 4.4% for 2026 and 4.2% for 2027. Chi

June 23, 2026

Commodities Outlook: The War and Its Reversal

June 23, 2026 10:05 AM UTC

The US-Iran memorandum marks a turn, but a fragile one. We attach 80% probability to the Strait of Hormuz reopening over June/July and staying open through 2027, and 20% to a second-half reclosure if Israel-Hezbollah tensions draw Iran back in (here). Most of the war premium has already unwound, and

DM Rates Outlook: Tightening or Easing?

June 23, 2026 8:15 AM UTC

· With the U.S./Iran interim agreement likely to hold and energy prices softening, our projected consumer slowdown will likely tilt the Fed not to hike in H2 2026 and to actually ease by 50bps in 2027, with 25bps moves in both Q2 and Q3. With 2yr yields consistent with a hike, the tra

DM and EM FX Outlook: Cross-Currents for H2 and 2027

June 23, 2026 8:00 AM UTC

· Our baseline for the coming quarters is that global FX is moving through a period of dollar bounce and cross-current positioning adjustment, rather than a clean return to the dollar downtrend. The near-term driver is the market's (over) hawkish reading of the June FOMC/Summary of Econ

DM ex U.S. EZ Outlook (Japan and Western Europe): Navigating the Post Iran War Period?

June 23, 2026 7:43 AM UTC

· We have revised 2026 Japan GDP only slightly lower to 0.8% as wage growth is solidly above 3%, which will support consumption for the rest of 2026/27. The extension of energy stimulus will cap headline inflation for Q2/Q3 2026. For the BOJ, despite hawkish forward guidance, the 1% r

June 22, 2026

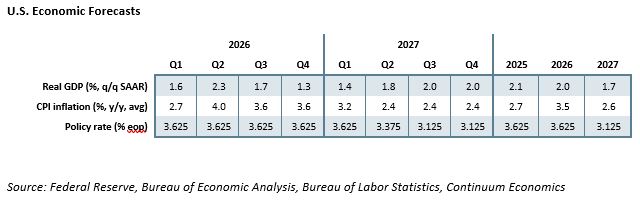

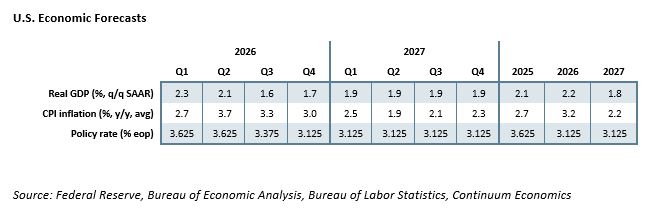

U.S. Outlook: Consumers Looking Vulnerable

June 22, 2026 2:17 PM UTC

• The US economy is showing resilience with strength in investment offsetting a gradual slowing in consumption, though consumer spending, which is running well ahead of real disposable income, looks set to slow further. This is likely to see the economy slow in the second half of 2026 even

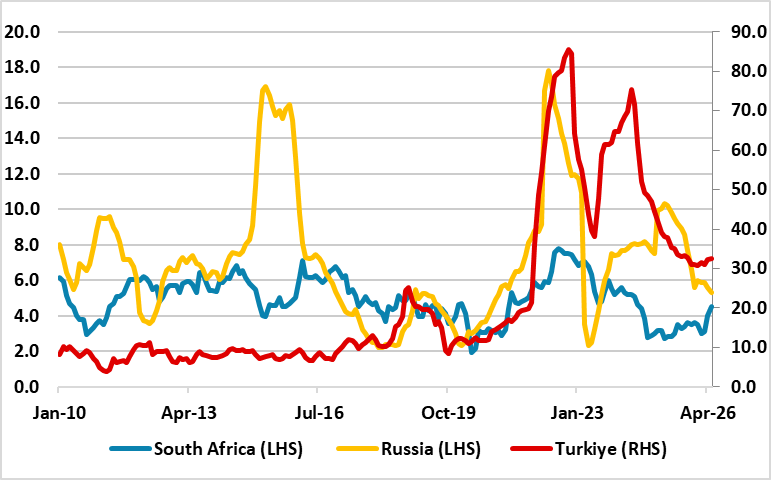

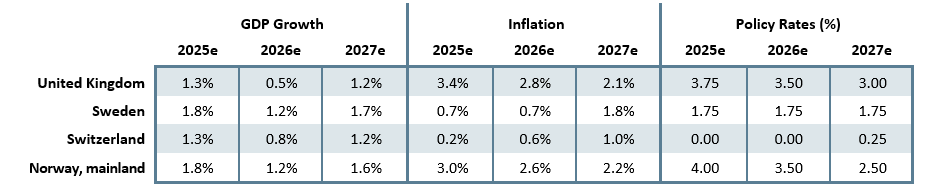

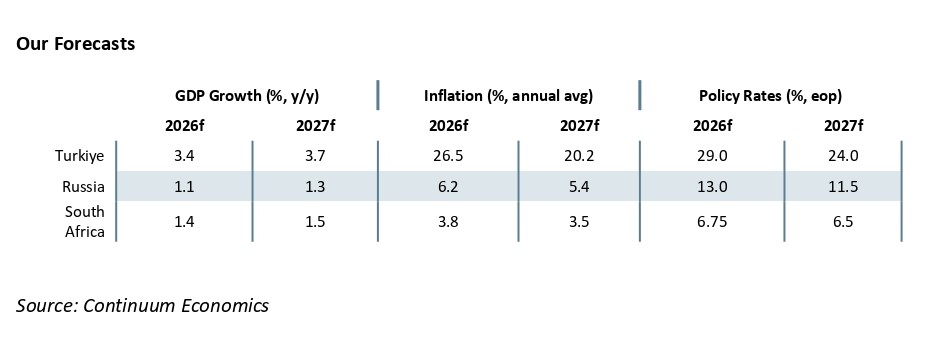

EMEA Outlook: Domestic Uncertainties Dominate

June 22, 2026 1:00 PM UTC

· In South Africa, we foresee average headline inflation will stand at 4.4% and 3.9% in 2026 and 2027, respectively. This baseline assumes easing energy prices starting in Q3, though second-round inflationary pressures from the Iran conflict will linger for some time. Accordingly, we foreca

Eurozone Outlook: Has Inflation Peaked Already?

June 22, 2026 11:35 AM UTC

· Under our only slightly updated view of no further fighting in the Middle East, we see oil and gas prices largely consolidating recent falls before falling afresh from mid-2027.The current situation is very different from that of 2022 and the Ukraine War in which the EZ lost access to

Germany/France/Italy and Spain: Growth and Inflation Outlooks

June 22, 2026 10:25 AM UTC

· We have retained our 2026 GDP picture of 0.3% (Our Forecasts below) and actually pared back that for next year, with more and more signs that China is continuing to ship cheap products to Germany (lower energy prices post Iran war still help 2027). For France, we have made a 0.3% do

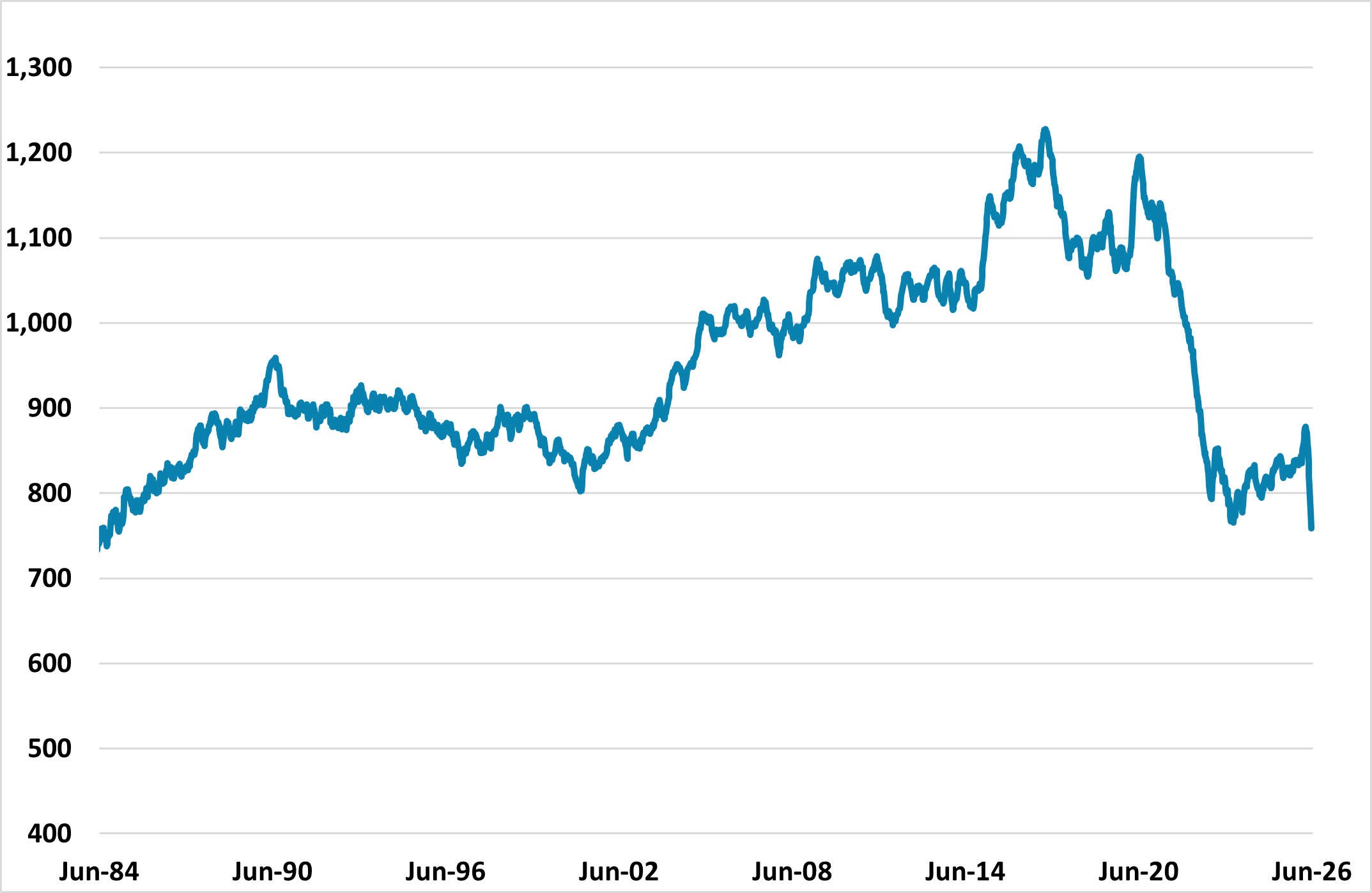

Equities Outlook: AI Optimism, But Caution Elsewhere in DM economies

June 22, 2026 7:05 AM UTC

· In terms of the S&P500, we remain less concerned about high valuations in the tech sector provided AI labs growth remains fast. 12mth fwd information technology are mid-range in the 2020-26 experience rather than at the highs. Even so, heavy equity issuance by tech companies and a s

March 30, 2026

Markets: Short vs Long Iran War

March 30, 2026 8:00 AM UTC

· For a 4-8 week war and 3-4 quarters of energy price normalisation, we see a 10% U.S. equity market correction in H1 2026 driven by the current Iran war and/or consumption slowing due to lower (real) wage growth, alongside still stretched valuations in equity and equity-bond terms. T

March 26, 2026

Asia/Pacific (ex-China/Japan) Outlook: The Iran War Shock

March 26, 2026 7:10 AM UTC

· The Iran war macro impact on Asia depends on length of the conflict and impact on energy flows. Our baseline is for a 4-8 week Iran war, with WTI down to USD80-85 by June; USD65-70 end 2026 and USD60 by Q3 2027 (here).

· India GDP growth has been revised down slightly

March 25, 2026

EM FX Outlook: Weathering the Storm

March 25, 2026 8:45 AM UTC

· EM currencies have seen a correction against the USD since the risk off prompted by the Iran war, but our baseline remains for a 4-8 week war (here) followed by energy prices only returning to pre-war levels by 2027 -- with WTI down to USD80-85 by June; USD65-70 end 2026 and USD60 by

DM FX Outlook: The Rest of 2026

March 25, 2026 7:55 AM UTC

Our baseline is for a 4-8 week Iran war, with WTI down to USD80-85 by June; USD65-70 end 2026 and USD60 by Q3 2027. This should see the USD return to a weaker profile later in the year. In our December Outlook, our favorites were the AUD and NOK based on yield spreads, but it is also worth noting th

EMEA Outlook: Adverse Global Developments and Domestic Uncertainties Dominate

March 25, 2026 7:00 AM UTC

· In South Africa, we foresee average headline inflation will stand at 3.8% and 3.5% in 2026 and 2027, respectively based on our baseline of a 4-8-week war in Iran and energy prices easing from Q2. Upside risks to inflation remain such as 2nd round effects of oil price hikes, utility costs,

March 24, 2026

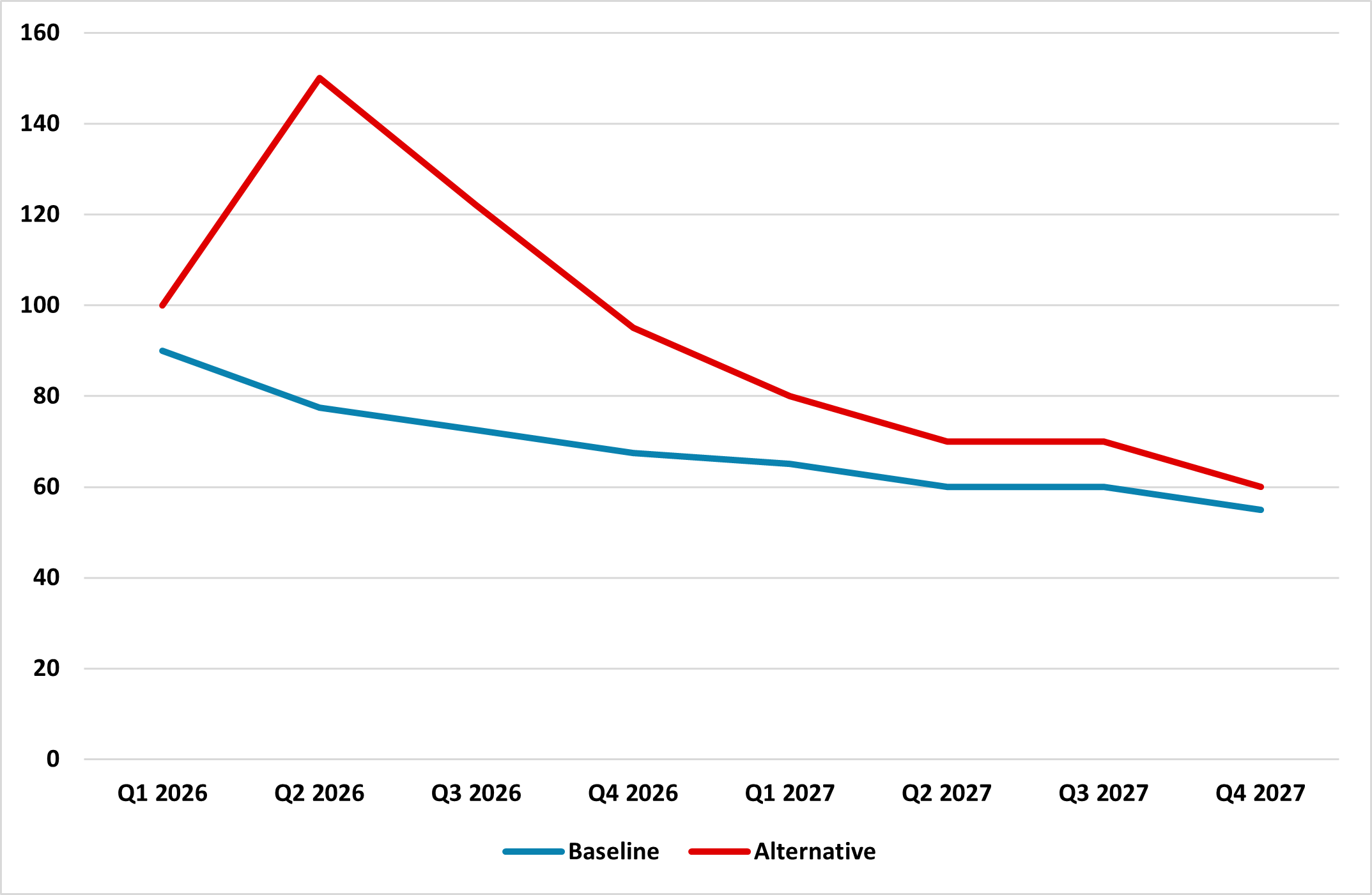

Commodities Outlook: The War in Action

March 24, 2026 2:30 PM UTC

Oil markets in 2026 have been extremely volatile due to the conflict in Iran and disruptions in the Strait of Hormuz. Under our baseline scenario of a 4-8 week war (here), we project WTI to average between USD 65 and 70 by year-end. In an alternative scenario of a prolonged multi-month conflict, pri

U.S. Outlook: Investment to Lead Growth, Underlying Inflation Set to Slow

March 24, 2026 12:15 PM UTC

• The crisis in the Middle East poses upside risks to headline inflation and downside risks to activity and our baseline assumes a 4-8 week war with a partial reversal of energy prices by end Q2 (here). Our forecasts (below) include a soft patch in H2 2026. Entering 2026 however, the U.S. e

Eurozone Outlook: Conflicts of Interest

March 24, 2026 9:55 AM UTC

· Under our more likely view of limited further fighting in the Middle East, we see oil and gas prices largely falling back to the pre-war levels within a year, with the current situation very different from that of 2022 and the Ukraine War in which the EZ lost access to Russian gas as

DM Rates Outlook: Mixed Policy Rate and Yield Paths

March 24, 2026 8:46 AM UTC

· The multi quarter outlook for DM rates depends on the length of the Iran war Our baseline is that it will be a 4-8 week war (here) and a 3-4 quarter retracement of oil prices back to pre-war levels – longer from Europe and Asian gas prices. We forecast WTI down to USD80-85 by June

Western Europe Outlook: Economies Slip on Oil

March 24, 2026 8:00 AM UTC

· In the UK, even without the Middle East impact we were suggesting a sub-consensus 2026 GDP picture which now has even greater downside risks attached. Our baseline is for 4-8 week war and a reversal of oil prices over 3 quarters. The BoE has a symmetric stance between 2nd round effe

China Outlook: Cyclical and Structural Headwinds

March 24, 2026 7:30 AM UTC

· Our baseline scenario of a 4-8 week war (here) is not a problem, aside from higher prices. We have pushed up our 2026 CPI forecast to 1.4% from 0.5% (higher food prices are also an issue), but as oil/gas prices come down, this suggests very subdued 2027 inflation, which we have cut

Japan Outlook: A Perfect Window

March 24, 2026 3:59 AM UTC

• Private consumption is supported by real wage turning positive in 2026. The trend is solidified by early spring wage negotiation results, which major firms agree to hike stronger than 2025 levels. We revised 2026/27 GDP to +1% as wage gains likely to accelerate. We expect 2026 CPI to be s

March 23, 2026

Outlook Overview: Iran War and AI Challenges

March 23, 2026 4:39 PM UTC

· The Iran war macro impact depends on length of the conflict and impact on energy flows. Our baseline is for a 4-8 week Iran war, with WTI down to USD80-85 by June; USD65-70 end December and USD60 by Q3 2027 (here). The jump in oil and gas prices mean at least a temporary increase in

Equities Outlook: Navigating Cyclical and Structural Forces

March 23, 2026 4:15 PM UTC

· For global equities, our baseline (here) is for a 4-8 week Iran war, with WTI down to USD80-85 by June; USD65-70 end 2026 by June and USD60 by Q3 2027. A fragile situation will mean it will take until 2027 for energy prices to return to pre-war levels. On a multi-quarter basis thi

February 10, 2026

EUR/USD: Europe’s Counter Threats to Trump

February 10, 2026 11:05 AM UTC

· Europe is highly unlikely to weaponize its existing portfolio holdings or new flows into the U.S., as Europe is dependent on the U.S. nuclear umbrella and as EZ/EU decision making is slow and modest in action. Such a move would be strongly opposed by EZ/European investors. Even so,

January 06, 2026

Markets 2026

January 6, 2026 9:58 AM UTC

• For financial markets, the muddle through for global economics and policy provides support for risk assets, combined with solid earnings prospects from some of the magnificent 7. However, U.S. equities are once again significantly overvalued and we look for a 5-10% correction in 2026, b

January 05, 2026

AI and U.S. Productivity

January 5, 2026 8:04 AM UTC

· Structural labor and overall productivity will be boosted if current AI adoption is sustained at a pace quicker than the adoption of the internet. However, not all areas of the U.S. economy are exposed to AI benefits, as manual work can only be replaced by humanoid robots with maj

December 19, 2025

Western Europe Outlook: Underlying Price Pressures Ebbing

December 19, 2025 9:34 AM UTC

· In the UK, we have upgraded 2025 GDP growth by 0.1 ppt to 1.3%, but pared back that for next year by a two notches to a very sub-par 0.6%. We think the weak(er) labor market will accentuate somewhat refreshed disinflation allowing the BoE to ease further in 2026 by around 75 bp to 3.0

Japan Outlook: Putting One Foot in Front

December 19, 2025 7:15 AM UTC

· Private consumption growth is hindered by negative real wage in Q3 2025 yet Japan continues to demonstrate the structural change in both higher business price/wage setting and consumer behavior. Early signs for 2026 spring wage negotiation are upbeat and should see wage growth at

December 18, 2025

DM FX Outlook: Scope for USD decline against JPY, AUD and NOK

December 18, 2025 2:31 PM UTC

· Bottom Line: We expect some modest USD losses across the board over the next couple of years, but there is much more scope for losses against the JPY, AUD and NOK than the other G10 currencies, as yield spreads have moved dramatically in favour of these currencies, and the currencies

EM FX Outlook: High Real Yields Still Help

December 18, 2025 12:14 PM UTC

• EM currency 2026 prospects come against a backdrop of a further but slower USD depreciation against DM currencies, but inflation differentials, domestic central bank policy and politics also matter. We forecast the Mexican Peso (MXN) will likely be more volatile, as President Donald Tru

December 17, 2025

DM Rates Outlook: 2026 Yield Curve Steepening Before 2027 Flattening

December 17, 2025 9:21 AM UTC

· Multi quarter, we still look for 50bps of further Fed easing by end 2026, which will likely initially bring 2yr yields down to 3.35%. However, once the Fed Funds rate get closer to 3.0-3.25% and the assumed slowdown turns into a soft landing, the 2yr will likely move to a premium ve

Outlook Overview: Turbulent Times

December 17, 2025 7:44 AM UTC

· The U.S. slowdown remains in focus as the lagged effects of President Trump’s tariff increases continues to feedthrough, though our baseline is for a 2026 soft-landing. The Supreme court will likely rule against part of Trump’s reciprocal tariffs, which will create short-term

December 16, 2025

Asia/Pacific (ex-China/Japan) Outlook: Managing Slower Growth Without Losing the Cycle

December 16, 2025 2:43 PM UTC

· Asia’s 2026 growth is normalizing, not weakening, though the growth outlook reflects resilience under mounting strain rather than acceleration. Larger investment-led economies such as India and Malaysia are sustaining momentum through public capex, infrastructure pipelines, and indu

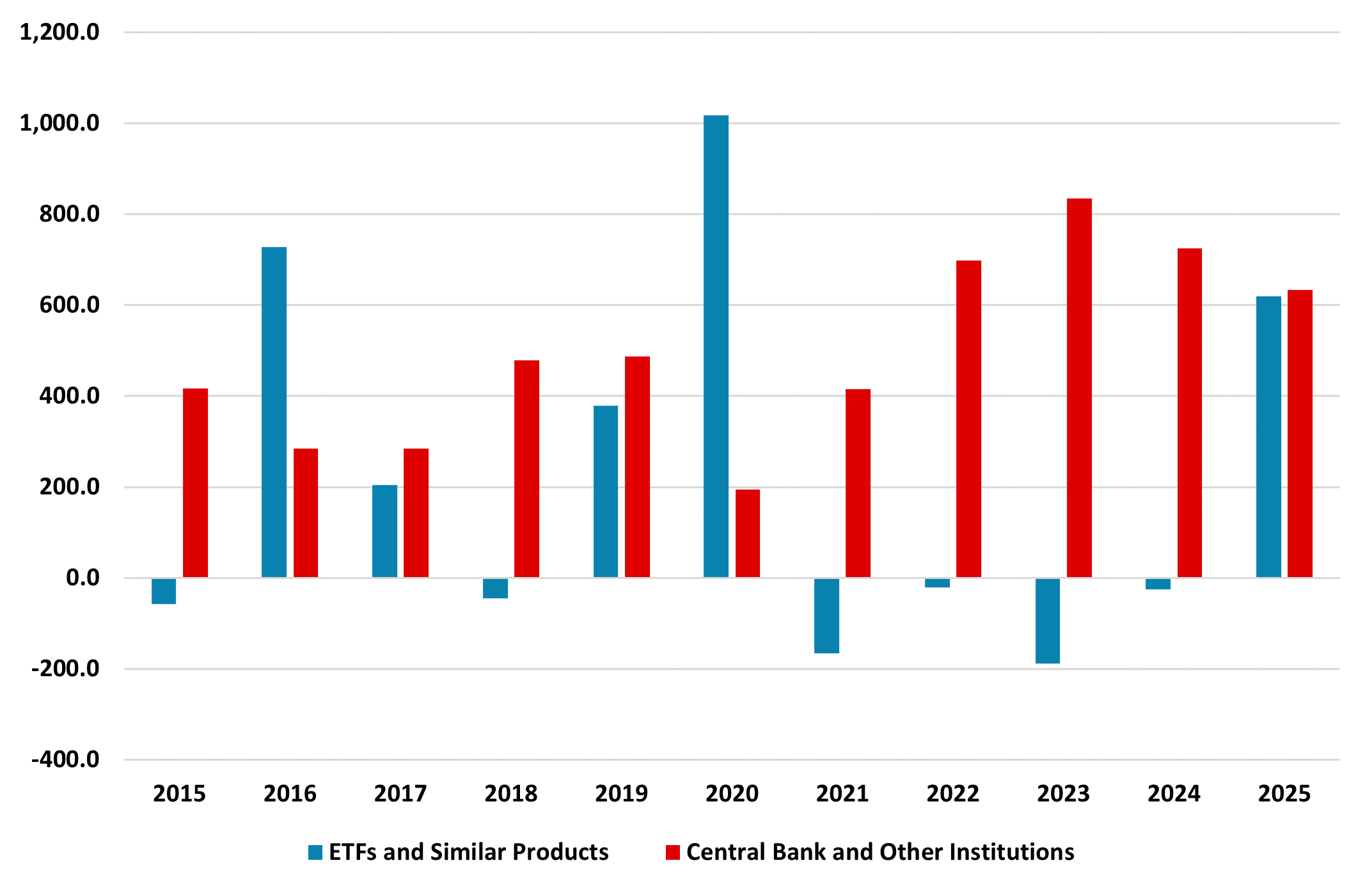

Commodities Outlook: A Balancing Act

December 16, 2025 10:15 AM UTC

Global oil demand is expected to be modest, with weak consumption in the U.S. and China, while India will support demand in 2026 and 2027. Non-OPEC supply is expected to expand moderately in 2026, whereas OPEC’s policy will respond to demand but remains puzzling. Supply trends in 2027 are likely t

EMEA Outlook: Uncertainties Give Mixed Signals

December 16, 2025 7:00 AM UTC

· In South Africa, we foresee average headline inflation will stand at 3.8% and 3.5% in 2026 and 2027, respectively. Upside risks to inflation remain such as, utility costs, and supply chain destructions. We see growth to be 1.4% and 1.5% in 2026 and 2027, respectively. Risks to the growth

December 12, 2025

U.S. Outlook: Consumers Vulnerable, but Recession Unlikely

December 12, 2025 4:38 PM UTC

• US GDP growth is likely to look solid in Q3 2025 supported by resilient consumer spending, but with slowing employment growth and resilient inflation weighing on real disposable income that will be difficult to sustain. However, while consumers look vulnerable, business investment looks h

Equities Outlook: Choppy Up For 2026 and Down for 2027?

December 12, 2025 8:05 AM UTC

· The U.S. equity market is underpinned by the bullish AI/tech story and a soft economic landing into 2026. However, overvaluation is clear and this leaves the market vulnerable to a 5-10% correction on moderate bad news e.g. economic data. We see the S&P500 having a choppy year a

December 11, 2025

China Outlook: Headwinds Get Stronger

December 11, 2025 10:30 AM UTC

· Private domestic demand remains modest, with consumption ranging from modest to moderate (slowed by the housing wealth hit and soft jobs/wage growth) and investment further impacted by the ongoing adverse drag of the residential property bust. China’s authorities prefer a long and

Eurozone Outlook: Running to Keep Fiscally Still?

December 11, 2025 10:09 AM UTC

· Amid what may still be tightening financial conditions and likely protracted trade uncertainty, we retain our below consensus activity forecast for 2026 but see a fiscally driven pick-up into 2027. However, the picture this year appears to be slightly better but the economy has actual