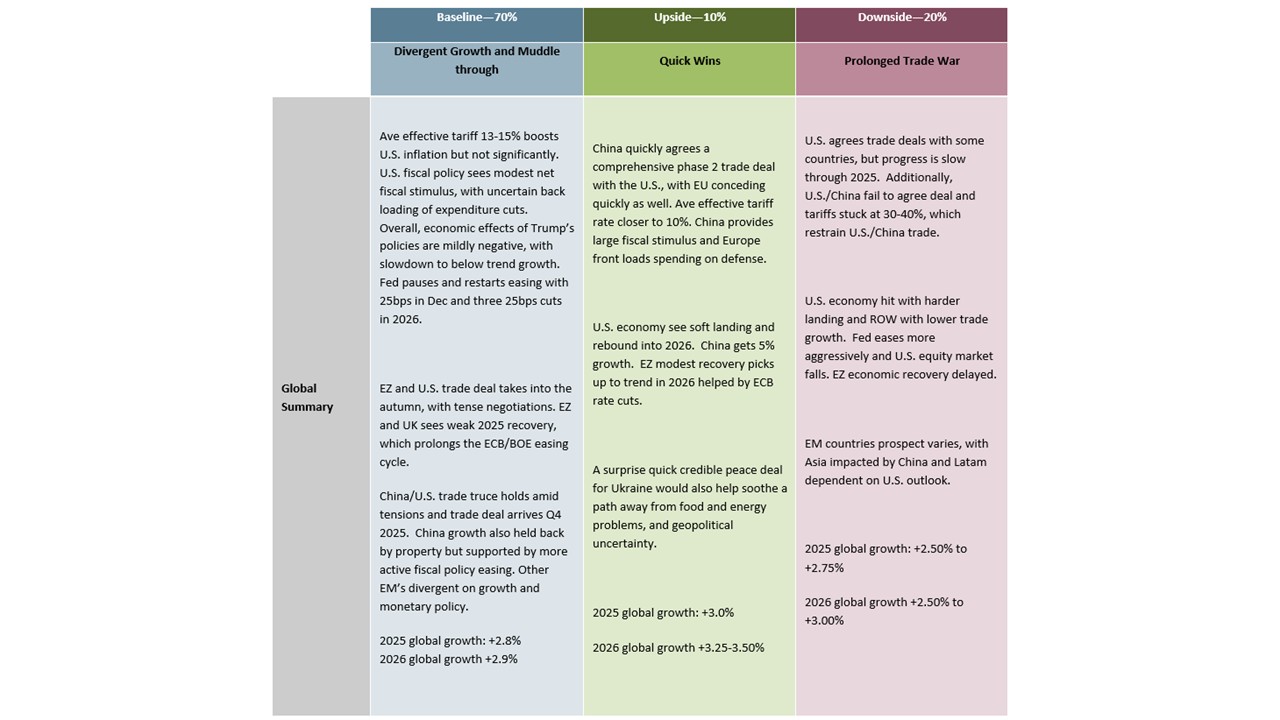

Outlook Overview: Trump’s Fluid Policies

· Other DM countries face an adverse disinflationary hit from U.S. tariffs, as counter tariffs are virtually zero. Lagged monetary easing will help support growth into late 2025/2026 in the EZ however and multi-year fiscal spending on defense is set to increase – though the June NATO deal is for 3.5% of GDP for hard military spend by 2035. The ECB and BOE also still have some further easing to deliver. Japan is impacted by the trade crosscurrent, but also a less accommodative backdrop as the BOJ slowly normalizes interest rates.

· For EM countries, China should see reasonable growth just below 5%, with our baseline scenario being a 65% probability of a trade deal eventually being reached between the U.S. and China and trade (here) and residential investment being less of a headwind into 2026 – though growth will still be unbalanced. Other EM countries will see divergent growth prospects, given differing levels of U.S. tariffs and also a variable pace to when trade deals are agreed with the U.S. We think Mexico sees the deepest hit in 2025, before modest recovery in 2026. EM monetary easing will also differ, as progress towards inflation targets varies.

· Geopolitically, re the U.S. attack on Iran, our baseline oil view remains that the effect will be temporary and that oil prices will move to USD63 by end 2025. Meanwhile, the Ukraine war now looks like it will continue due to Putin’s stubbornness, with a peace deal less likely in 2025 and the U.S. being reluctant to commit new financing to Ukraine. However, the June NATO summit agreement has reduced European security fears. Elsewhere, we still feel that the risk on an invasion of Taiwan in the next 2 years is very low, both as China military is not strong enough, and President Xi would invade only if China was assured of success (here).

· For financial markets, DM government bonds will likely see yield curve steepening, with some rate cuts helping the short end but debt issuance pressures at the long-end in the U.S. and a number of other countries. The outlook at the long-end of the curve is volatile, with the prospect of a 7% U.S. budget deficit in 2026 and we have revised up our 10yr U.S. yield forecast to be centered around 4.5% for the next 6-18 months. The overvaluation of U.S. equities still leaves it vulnerable to major bad news, especially if any hard landing fears appear. We see a further correction before an end of year recovery. Other global equity markets will likely follow the U.S. on any selloff.

· The USD can see further losses against DM currencies, as foreign investors are worried about overweight US asset positions in the face of adverse and erratic policymaking and an overvalued USD. Interest rate differentials will have less of an impact. The USD trends against EM currencies will be more mixed, depending on starting points in currency valuation terms and inflation differentials versus the U.S. However, we could see some further recovery in the oversold Brazilian real that benefit from a high carry versus the U.S.

· Risks to our views: A hard landing in the U.S. economy would spillover globally in GDP terms. While this would likely trigger more aggressive Fed easing, it could still prompt a bear market in U.S. equities and a noticeable decline in the USD.

Figure 1: Economic Scenarios

Source: Continuum Economics

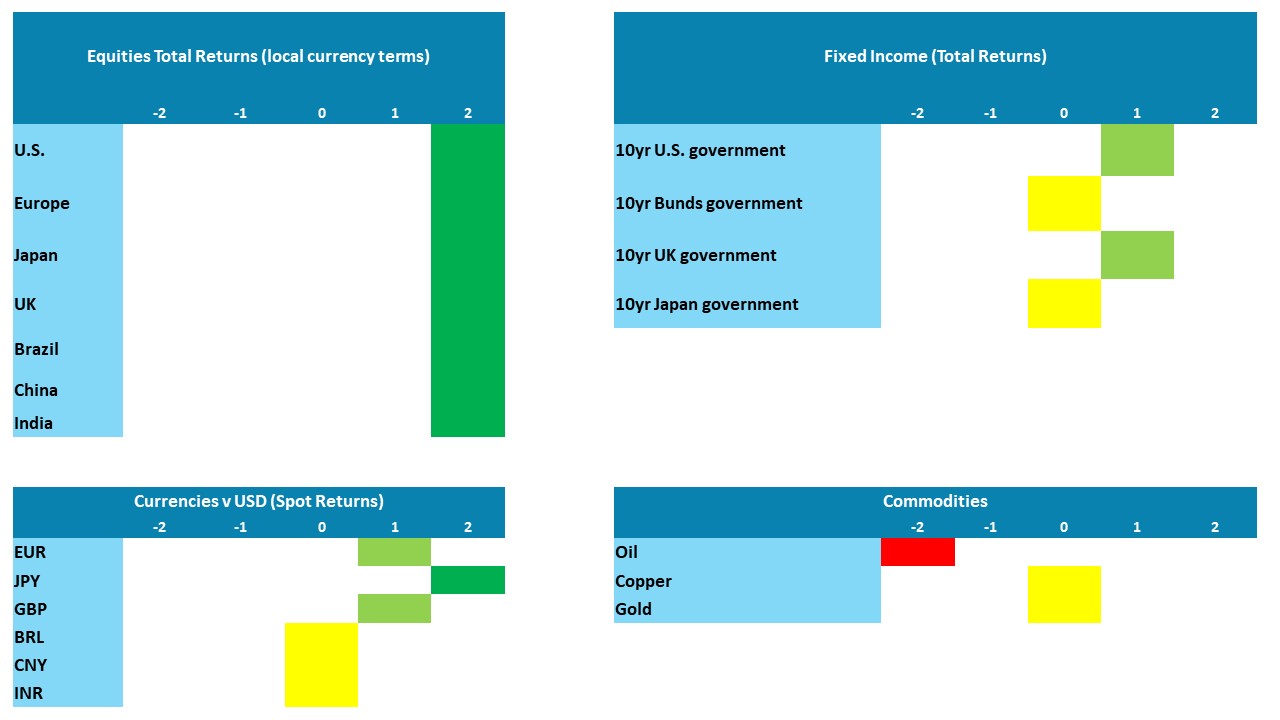

Market Implications

Figure 2: Asset Allocation for the Next 18 Months

Source: Continuum Economics Note: Asset views in absolute total returns from levels on June 23 2025 (e.g., 0 = -5 to +5%, +1 = 5-10%, +2 = 10% plus).

· Government Bonds. We see 10yr U.S. Treasuries at 4.40% by end 2025, due to a tug of war between a soft landing in the economy and persistently large issuance. We see 10yr Bund yields at 2.45% by end 2025. Finally, 10yr JGB yields will likely peak 1.75-2.00% region, as we see one further 2025 hike followed by a 25bps hike in Q1 2026.

· Equities. Softening of hard economic data can cause a new correction in U.S. equities, alongside Trump intermittent trade action. Recovery should be seen by end 2025 to 6000, before 6500 end 2026 – Fed rate cuts, soft landing and share buybacks. Other markets will follow any selloff. We see little sustainable outperformance versus the U.S. in H2 2025, with gains all coming in 2026 (Figure 2). India can track other markets in H2 2025, but should outperform the U.S. by 5% in 2026.

· FX. Prospects remain for DM currencies to make further gains versus the USD in H2 2025 and 2026. Foreign investors are concerned about being overweight U.S. assets, with erratic Trump administration policymaking and overvalued USD and U.S. equities. EM currencies will be more divergent, with Turkish Lira falling on stubborn inflation, but the oversold Brazilian Real likely to gain ground versus the USD.

· Commodities. We do not see a lasting disruption to oil supply from the missile war between Israel and Iran, and we think the market will return to fundamentals since we do not expect a full scale war. Oil demand growth remains moderate with the slowdown in the world economy. Combined with OPEC+ keenness to scale down voluntary production cuts, this can see a return to soft oil prices soft later in 2025. We see WTI at USD63 by end 2025 and USD58 by end 2026.

Figure 3: Key Events

| From July 2025 | French Parliamentary Election | The surprise snap parliamentary election last July, much to President Macron’s consternation actually made his minority government even weaker, instead creating three clear factions with the legislature. A fresh government has been formed but faces key battles over immigration, pension reform and the budget any of which could see it toppled. Opinion polls suggest that if/when a fresh election occurs (which cannot occur before July due to the constitution) this will not change materially with adverse fiscal and economic implications. President Macron has ruled out fresh elections but only for the next couple of months. Regardless, he may come under pressure to resign, but is likely to try and complete his term which runs to 2027. But the political impasse, via any possible fiscal and economic crunch could yet trigger further political upheaval. | ||

| July 20, 2025 | Japan House of Councillors election |

| ||

| September 8, 2025 | Norway Parliament election | Parliamentary elections are scheduled to be held in Norway on 8 September 2025 to elect the members for the 2025–2029 parliamentary term. A fresh coalition is inevitable. | ||

| October 26, 2025 | Argentina Legislative Election | Argentina will hold legislative election in October 2025. Half of the Chamber of Deputies (127 seats from 257) will be renovated for a four-years mandate. Additionally, one third of the Senate (24 seats for 74) will also be renovated for a 6-years mandate. Most of the polls are pointing that President Javier Milei party will increase the participation of his far-right party, La Libertad Avanza, in both houses while other centre-right parties, such as PRO, will likely lose seats. The left and centre-left are expected to diminish in seats and they will likely be more fragmented than before. | ||

| September 13, 2026 | Sweden General Election | The current right-wing coalition still has very slim effective majority in parliament even with the far-right Sweden Democrats offering support. This is all the result of the 2022 election which brought a fragmented result but locking out the Social Democrats even though they are the largest party. This fragmentation was a result of a more polarized parliament and polls suggest more of the same, but with a general drip more to the left. But even if left-leaning parties return to power, it unlikely to change much given the current focus on defence but where an election issue may be a speedier defence build-up. | ||

| October 4 and 26, 2026 | Brazil General Election | In 2026, Brazil will hold general elections to elect the next President, renew all the Chamber of Deputies seats, and two-thirds of the Senate, while also electing the governors of all Brazilian states. Lula will likely seek re-election, while opinion polls suggest Lula will likely face Freitas (an ex Bolsonaro minister here). However, an irrational decision by Bolsonaro, such as nominating his wife or son for the presidency resulting in a fragmented opposition, cannot be ruled out. | ||

| November 3, 2026 | U.S. Mid Term Elections | All seats in the House and a third of the seats in the Senate will be up for election. With the current Republican majority in the House of five seats being marginal even a modest level of disappointment in the Trump administration could see the Democrats gain control of the House, but it will be a lot harder for the Democrats to make the necessary gain of 4 seats in the Senate. A recession may be required to see the Democrats take the Senate. |

Source: Continuum Economics