EMEA Outlook: Global Uncertainties and Domestic Dynamics Continue to Dominate

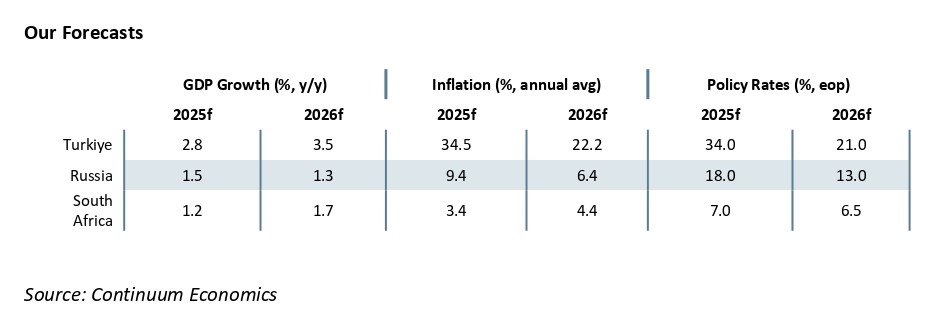

· In South Africa, we foresee average headline inflation will stand at 3.4% and 4.4% in 2025 and 2026, respectively, despite upside risks to inflation such as power cuts (loadshedding), tariff hikes by Eskom, spike in food prices, and global uncertainties. We see growth to be 1.2% and 1.7% in 2025 and 2026, respectively. Risks to the growth outlook are broadly balanced, with faster reform implementation representing an upside risk to growth while uncertainty about the U.S. economy, tariff wars and adverse global developments could cause problems. Our end-year policy rate prediction remains at 7.0% for 2025 and 6.5% for 2026.

· In Turkiye, the arrest of mayor of Istanbul Ekrem Imamoglu on March 23 due to fraud allegations risked the disinflationary process as TRY plunged in April. We now foresee upside risks emanating from domestic uncertainties, stickiness of services inflation, and adverse geopolitical impacts leading average inflation forecast to stand at 34.5% and 22.2% in 2025 and 2026, respectively. We think Central Bank of Republic of Turkiye (CBRT) will likely cut the rate to 34% by the end of 2025. We forecast the economy to expand by 2.8% in 2025 and 3.5% in 2026 considering high inflation and tighter fiscal stance continue to dent growth.

· In Russia, the war in Ukraine continues to create high military spending, strong fiscal stimulus in addition to aggravation of staff shortages. Our baseline view is for continued war rather than a peace deal in 2025. Our 2025 average headline inflation projection has increased when compared with the March outlook from 8.6% to 9.4% due to an overheated economy. Our end-year policy rate prediction stands at 18% for 2025 and 13% for 2026 as we foresee Central Bank of Russia (CBR) to consider cutting rates unless inflation picks up and RUB loses value significantly in H2. We envisage growth to hit 1.5% and 1.3% in 2025 and 2026, respectively.

Forecast changes: From our March outlook, we have lifted our 2025 average inflation forecast for Russia to 9.4% due to continued military spending. We have also hiked 2025 average inflation forecast for Turkiye to 34.5% particularly due to heightened price pressures after Istanbul mayor Imamoglu’s arrest. We now consider that end-year key policy rate for Turkiye will be 34.0% taking into account that CBRT hiked the policy rate from 42.5% to 46% during the MPC on April 17, and held it stable at 46% on June 19 due to global uncertainties and risks related to domestic politics. We revised our 2025 GDP growth prediction for South Africa to 1.2% YoY from 1.6% YoY since we think loadshedding, U.S. tariffs, and uncertain global environment will be important downside risk factors.

EMEA Dynamics: Global Uncertainties and Diverse Domestic Dynamics Rule

Uncertainty about the global economy, tariff wars, country specific factors, and inflationary pressures continue to rule the EMEA outlook. We think volatile U.S. economy, trade tariffs and adverse geopolitical developments could risk greater uncertainty over the EMEA medium-term prospects. We think EMEA countries will see divergent growth prospects, given differing levels of U.S. tariffs and also a variable pace to when trade deals are agreed with the U.S. EMEA monetary easing will also differ, as progress towards inflation targets and domestic factors vary.

Inflation remains the major concern for EMEA economies since they remain elevated in Russia and Turkiye despite aggressive monetary tightening cycles are still feeding through. Taking into account that the inflation remains below the midpoint target of 4.5% and core inflation hit 3.0% in April and May which is the lowest since July 2021, South Africa continues its easing cycle and reduced the key rate from 7.75% to 7.25% in the last 6 months. We feel Russia will be waiting for the right time to further cut rates in H2 which will depend on the inflation trajectory. Turkiye will likely continue its cutting cycle (unless a spike in inflation is seen and/or adverse domestic political developments occur).

When compared with the March outlook, we decided to revise our inflation trajectories for EMEA countries. We increased our average inflation forecasts for Russia to 9.4% and 6.4% in 2025 and 2026, respectively, as military spending remains elevated, domestic demand continues to outstrip domestic capacity, fiscal support to military staff and their families remain strong while the probability of a peace deal in Ukraine has recently decreased. We feel there are no signs of a significant inflation slowdown in the horizon yet until a full-scale peace deal in Ukraine could lower Russia’s military spending and relieve price pressures. In Turkiye, the arrest of mayor of Istanbul Ekrem Imamoglu has risked the disinflationary process (via TRY instability) and we lifted our average headline inflation forecast for Turkiye from 32.1% to 34.5% due to domestic politics and geopolitical uncertainties. Moving to South Africa, we revised down our average inflation forecast to 3.4% for 2025 since inflation continues to remain below South African Reserve Bank’s (SARB) target band of 3% to 6% supported by lagged impacts of previous tightening, and a relatively stable ZAR.

We think uncertainties about the DM economies coupled with the extent to which tariff increases are imposed and sustained could darken the EMEA growth prospects in 2025 and 2026. The content and the timing of U.S.- China trade truce will be a significant factor for EMEA trajectory. (Note: According to our baseline scenario, there is a 65% probability that a trade deal eventually will be reached between the U.S. and China (here)). Peace deals in Ukraine and Gaza coupled with lowered tension between Iran and Israel could particularly help Russian and Turkish economies to feel relieved, though our baseline is conflicts in Ukraine and Gaza to remain during the rest of 2025.

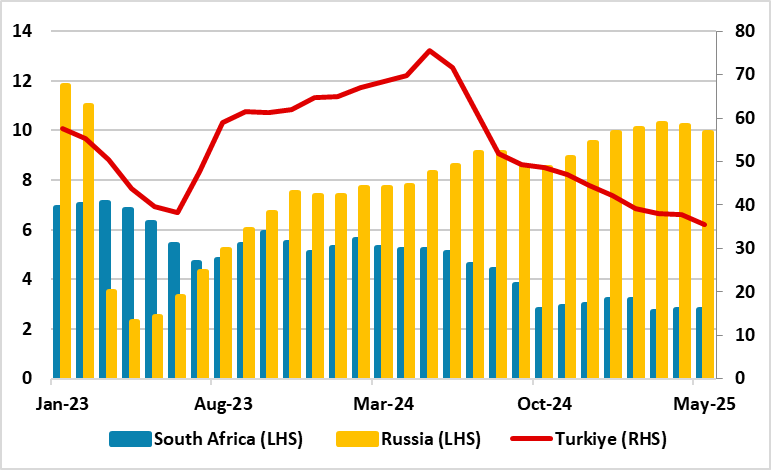

Figure 1: South Africa, Russia (LHS) and Turkiye Inflation (RHS) (%, YoY), January 2023 – May 2025

Source: Continuum Economics, Datastream

South Africa

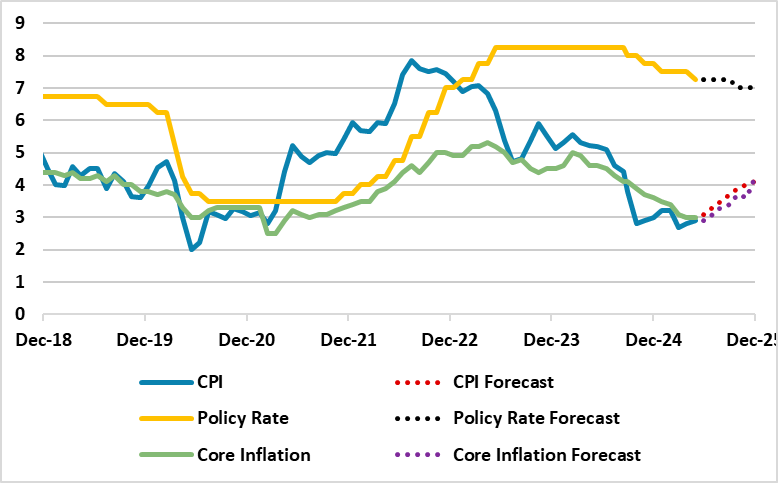

Despite South Africa facing challenges such as declining real per capita growth, rising level of public debt coupled with high unemployment and poverty rates, the economy continues to enjoy inflation remaining below SARB’s midpoint objective of 4.5%. Annual inflation stood at 2.8% YoY in May remaining close to the lower bound of SARB’s target range of 3% to 6%, while core inflation hit its the lowest level since December 2021, with 3.0% YoY in May. (Note: After positive news from the inflation front, SARB MPC signaled a potential shift towards a lower inflation target of 3% on May 29 (this would need to be agreed with the Treasury), down from the current 4.5% midpoint objective, which could limit rate cuts in the future).

Figure 2: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), December 2018 – December 2025

Source: Continuum Economics

Despite this, there are some worrying signals about the course of the inflation, and we consider it is set to move above 3% during the remainder of the year. First, we think the major risk on the inflation trajectory is the return of loadshedding in late Q1. Eskom announced on May 13 that Stage 2 loadshedding was implemented following a Stage 3 loadshedding on April 24, which suggest serious issues. Energy experts warn that the recent power cuts are a reminder that rolling blackouts are still a threat since Eskom’s generation capacity remains unreliable and unpredictable. We foresee further power disruptions are likely, particularly with the onset of winter when energy demand rises.

Additionally, SARB emphasized in its MPC report on May 29 that that rising trade tensions and abrupt shifts in long-standing geopolitical relationships coupled with domestic uncertainties continue to put favorable trends at risk. Taking into account that the oil price spiked recently amid concerns of Iran-Israel unrest, this could negatively affect the domestic economy if the conflict prolongs, despite our baseline scenario is that the tension will soften. Another risk factor is the U.S. additional tariffs. South Africa has formally requested that the 30% reciprocal tariff on South Africa stays suspended, but it remains unclear what the U.S. decides in that regard. However, this is disinflationary, as it would hurt S Africa exports and output/employment.

In addition to these, 12.7% tariff hike by Eskom for 2025/26, which came into force as of April 1, coupled with recent spike in food and housing prices could lift CPI over expectations in H2. It was positive to see that previously proposed 1% increase in VAT was cancelled, and the National Assembly adopted the fiscal framework, which was an important step in completing the adoption of Budget 3.0.

Under current circumstances, we foresee average inflation will hit 3.4% and 4.4% in 2025 and 2026, respectively, supported moderately by lagged impacts of previous tightening, and a relatively stable ZAR. (Note: SARB also revised its end-year inflation forecast for 2025 from 3.6% YoY to 3.2% YoY on May 29). The key for the inflation trajectory will be the global developments, tariffs, and government’s determination to address the electricity shortages and financing needs.

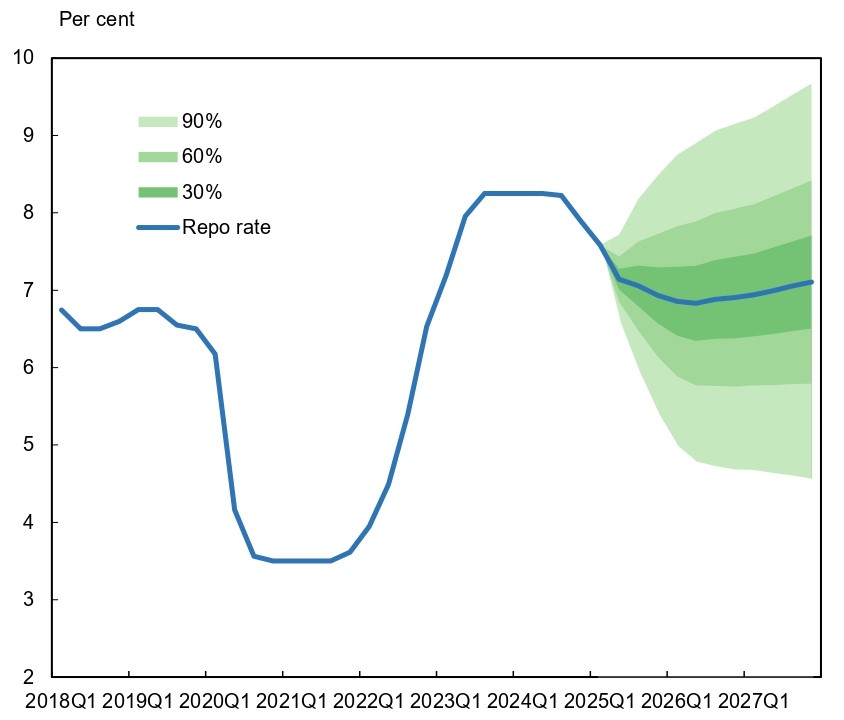

Taking into account that SARB reduced the policy rate by 25bps to 7.25% on May 29 highlighting that annual inflation remains below SARB’s current inflation target range we believe the continuation of the easing cycle was a partial relief for the consumers facing high costs of loans, as well as the automotive industry and the property sectors which have been hit by the elevated interest rates. We think cautious and data-dependent SARB will likely halt cutting cycle in early H2 due to global uncertainties including the Iran conflict coupled with a likely inflation spike in H2. We expect one 25 bps cut late Q3/Q4, if domestic inflation and the global outlook allow. SARB will continue cutting the rates in 2026, -with a slower pace due to global uncertainties-, and cut by 25 bps in each half of 2026. Our end-year key rate predictions remain at 7.0% and 6.5% for 2025 and 2026, respectively. If SARB do shift to a 3% inflation target, then this could complicate easing in 2026, given our inflation forecast.

Figure 3: SARB Interest Rate Forecast (%), 2018 – 2027

Source: SARB Forecast Report (May 2025)

South African economy grew modestly by 0.1% QoQ and 0.8% on a year-on-year basis in Q1 2025 driven by performances by agriculture, transport and finance, despite a strain on the mining and manufacturing industries continued to drag on growth. Private fixed investment declined in Q1 after a brief glimmer of activity at the end of last year. SARB Governor Kganyago echoed that the GDP data is not a pretty picture highlighting the country’s vulnerability to global risks. Regarding this, SARB decided to downgrade its GDP growth forecast for 2025 from 1.7% YoY to 1.2% YoY, which is lower than Finance Minister Godongwana’s anticipated 1.4% YoY.

We assess the economy will grow by 1.2% and 1.7% in 2025 and 2026, respectively, supported by improved consumer sentiment, low inflation, and interest rate cuts despite power cuts coupled with uncertain global environment, geopolitical tensions and slowing global demand will be important downside risk factors.

On the manufacturing front, Absa PMI decreased to 43.1 points in May from 44.7 points in April, remaining in contractionary territory for a seventh consecutive month while business confidence declined for the first time in over a year decelerating by five points to 40 in Q2 as the recovery that started in Q2 2024 stalled. As mentioned, we feel uncertainty about U.S. tariffs presenting risks over the growth trajectory. Additional tariff decisions by the Trump administration will be critical for South Africa, particularly if the U.S. implements 30% additional tariffs on imports from South Africa following the 90-day pause.

Turkiye

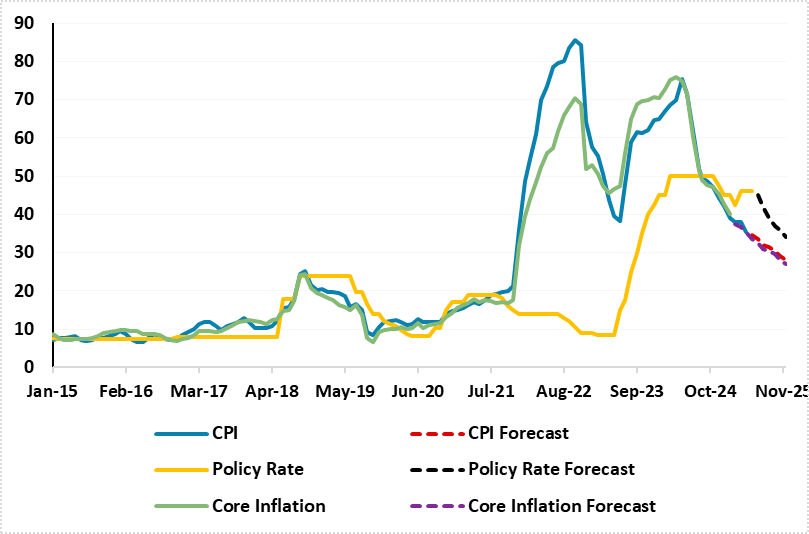

Despite decelerated less-than-expected, inflation in Turkiye continued to soften particularly in H1 backed by lagged impacts of the tightening cycle, relative slowdown in credit growth, and tighter fiscal stance. CPI cooled down to 35.4% YoY in May. We expect the slowdown to continue, but with a slower pace in H2 while the extent of the decline will be determined by TRY volatility, food inflation, energy prices and administrative price adjustments such as wages. On the upside, falling headline inflation in H2 could feed into backward-looking inflation expectations, easing price pressures. We envisage it will be difficult to grind sticky inflation from 30%s to 10%s rapidly, taking into account that inflation becomes stickier requiring high interest to remain for some time. It appears it would be necessary to make concessions on growth, particularly in 2025.

Istanbul mayor Ekrem Imamoglu’s arrest late March was a key and unexpected development which caused a temporary turbulence and high currency volatility particularly in April and May. According to sources, CBRT burnt around 50 billion USD worth reserves to restrain TRY losing value. The arrest of Imamoglu triggered market losses, loss in investor confidence, and had inflationary impacts which caused the CBRT to first hike the key rate from 42.5% to 46% on April 17 and then keeping the policy rate unchanged at 46% during the MPC on June 19. (Note: CBRT highlighted on June 19 tight monetary stance will be maintained until price stability is achieved via a sustained decline in inflation, signaling CBRT wants inflation to be under control before any rate cut decisions).

Due to political instability, our forecasts for the annual average headline inflation has slightly increased to 34.5% in 2025 from 32% in March outlook. We anticipate the wage-inflation spiral, deteriorated pricing behavior, stickiness of services inflation, and geopolitical risks will keep inflation pressures alive in 2025 and 2026. If the Ukraine-Russia war will come to end and tension in Gaza will ease, this will be positive for Turkish inflation outlook, while these are not our major scenarios.

It is worth noting that the CBRT released the second quarterly inflation report of the year on May 22, and maintained its end year-end inflation forecast at 24% despite uncertainties. Inflation forecast was set at 12% for 2026, 8% for 2027. CBRT governor Karahan also indicated that CBRT maintained its forecast range for this year between 19% and 29%. We anticipate domestic and geopolitical risks will keep inflation pressures alive for a longer period, and it will be unlikely to reach single digit inflation target by 2027.

We expect a cautious CBRT will continue its cutting cycle in H2 2025 unless there is a sustained surge in the underlying trend of monthly inflation is observed and heightened political instability. Our end year key rate prediction for 2025 and 2026 are at 34% and 21%, a bit higher than the March outlook since CBRT decided to increase the rate unexpectedly from 42% to 46% after social upheavals following Imamoglu arrest, and this caused a pause to the easing cycle. We envisage CBRT will continue cutting rates in 2026 to 21%, but with a slower pace due to global economic uncertainties and geopolitical risks. We expect the monetary easing cycle to support a continued normalization of funding cost towards the policy rate. MoM inflation readings will also be key, as CBRT will want to avoid reigniting inflation with too aggressive rate normalization.

Another headwind for the Turkish economy in addition to inflation is the wage-inflation spiral. More than half of Turkiye’s working class earns the minimum wage, and Turkish workers continue to suffer from galloping inflation since the government increased minimum wages by 30% in Q1, which was below the inflation rate, to reduce aggregate demand and restrain price pressures. Despite Turkish employees pushing for an additional hike in minimum wages to cope with higher cost-of-living in July, Minister of Labor and Social Security did not signal an additional wage hikes yet, which is good for the inflation projection but not for Turkish citizens.

Figure 4: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2015 – December 2025

Source: Continuum Economics

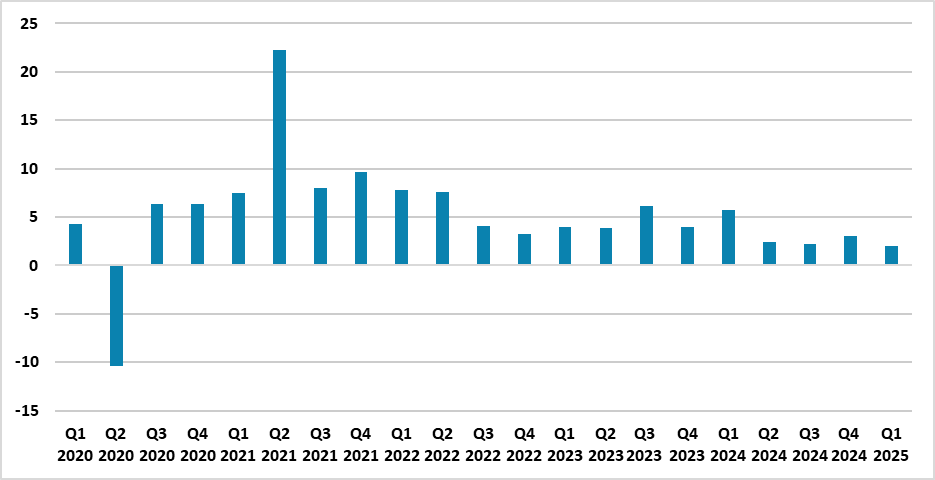

When it comes to growth, after Turkish economy expanded by 3.2% YoY in 2024, it grew by a mere 2.0% in Q1 2025 backed by private consumption. The growth rate hit below expectations due to the weight of high interest rates, sluggish demand abroad weakening exports and adverse geopolitical developments. (Note: Investments slowed significantly by increasing 2.1% YoY in Q1 after expanding by 6.1% YoY in Q4). We feel tight policies will continue to suppress domestic demand the rest of 2025 bringing growth to 2.8%. (Note: IMF and the EU envisage Turkish economy to expand by 2.7% and 2.8%, respectively, in 2025).

Growth will remain under pressure in H2 due to high interest rates, contractionary fiscal actions and additional macro prudential policies to fight against the elevated inflation coupled with adverse global outlook. Additionally, adverse geopolitical developments including continuation of Russia-Ukraine conflict will be an important risk factor. Another risk factor is the U.S. additional tariffs. Turkiye requested that the additional beyond the baseline 10% reciprocal tariff on Turkiye stays suspended, but it remains unclear what the U.S. decides in that regard after 90 days’ pause. A drop in the inflation rate and rate cuts could boost confidence, and growth would rise back toward potential of 3.5%-4% after 2026.

There is still a downside risk that growth can be lower than expected, particularly considering all tightening measures in place. 2026 growth will be likely be higher than 2025, hitting 3.5% YoY in 2026, supported by positive impacts of the rate cuts and increasing business confidence assuming no dramatic impact from weaker external demand.

Figure 5: GDP Growth (%, YoY), Q1 2020 – Q1 2025

Source: Continuum Economics

Russia

Russian economy continues to be restrained due to high inflation, military spending and labor constraints. The war in Ukraine remains determinant for all outlooks as it creates an increasing financial burden on Russia. The overall environment for doing business in and with Russia remains unfavorable.

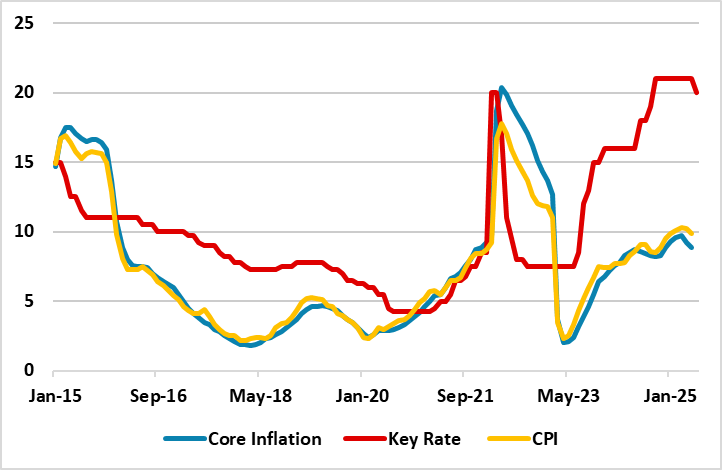

On the inflation front, average inflation hit 10.1% in Q1, and 9.9% YoY in May. We increased our CPI forecasts to 9.4% and 6.4% in 2025 and 2026, respectively, when compared to March outlook as war in Ukraine and sanctions dominate the economy igniting labor shortages, and supply-chain disruptions and import suppression causing upward pressure on prices. Additionally, there are constant surges in services and food prices. Despite the lagged impacts of monetary tightening, the economy remains overheated as the growth in domestic demand is still significantly outstripping the capabilities coupled with strong fiscal support to military staff and their families and elevated inflation expectations. Inflation is projected to moderately slowdown in Q3/Q4 as tight monetary policy will likely affect bank lending and private consumption, but slowly. High military spending, likely deterioration in the terms of external trade during ongoing trade wars and rising wages do not signal a significant permanent inflation slowdown in the horizon yet, and we continue to feel reaching 4% target will be very tough even in 2026, since cooling off inflation will take longer than CBR anticipates.

Despite inflation stays elevated, CBR surprisingly decided to cut the key rate by 100 bps to 20% per annum on June 6, highlighting current inflationary pressures, including underlying ones, continue to decline. CBR stated that it will maintain monetary conditions as tight as necessary to return inflation to the target in 2026. We think CBR will likely consider cutting rates (moderately) in H2 if inflation continues softening, RUB stabilizes and inflation expectations would converge to CBR’s forecasts; despite rates having to stay high for a longer period, as announced the CBR. Our 2025 end-year key rate forecast is 18% and 13% for end-2026.

The inflation trajectory and rate decisions will depend on how peace negotiations will proceed in H2 2025. A full-scale peace deal in 2025 could have helped Russian economy to feel relief since RUB will likely strengthen, average headline inflation will soften, and fiscal pressure will ease, particularly if sanctions will be lifted. However, the war will likely continue due to president Putin’s stubbornness, and the U.S. being reluctant to commit new financing and military support to Ukraine as Ukraine remains in a weaker negotiating place. After Trump-Putin call early June, we decided to increase the probability of war continuing to 70% from 50% when compared to March outlook, considering peace negotiations continue to develop very slowly, and there are no significant moves expected by president Trump such as implementation of secondary tariffs on Russia oil buyers. We continue to feel if no balance is struck, Europe could step up and help Ukraine financially and militarily. Europe could partly fill the U.S. financial gap for a number of years, but without U.S. military support a Ukraine win will be almost impossible.

Our second scenario is based on a Russia-friendly peace deal (30% probability) with Russia annexing areas in and around four Ukrainian oblasts that it occupied, securing no NATO membership for Ukraine and no foreign troops in Ukrainian territory.

Figure 6: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2015 – June 2025

Source: Continuum Economics

When it comes to growth, the main driver for Russian GDP growth remains the surge in military spending, supported by the improved consumer demand amid greater outlays on social support, higher wages and strong fiscal stimulus. There remains increased public spending in war-related industries and construction in Russia. Despite underpinnings, Russia's GDP expanded by 1.4% YoY in Q1, partly due to gradual slowdown in domestic demand growth, marking the slowest pace of growth since the economy resumed expansion in Q2 2023.

The Ministry of Economic Development of Russia now projects annual growth of 2.5% for 2025, while the CBR offers a more cautious outlook, predicting growth between 1% and 2%. The World Bank (WB) recently revised upward its forecast for 2025 GDP growth from 1.2% to 1.4%. We envisage growth to hit 1.5% and 1.3% in 2025 and 2026, respectively, which are significantly less than 2024 figure, as aggressive tightening cycle is still feeding through, capacity utilization reached its maximum in years, and labor force deficit is unlikely to change in the short term. More importantly, sanctions, high interest rates, supply side constraints and higher price pressures remain restrictive.