Eurozone

View:

August 20, 2025

U.S./China Trade Deal: Slow Progress

August 20, 2025 10:25 AM UTC

· Overall, we would attach a 50% probability to a trade framework deal being announced in Q4, though this is unlikely to be comprehensive and could merely be a collection of measures. Even so, the risk also exists of trade negotiations dragging onto 2026 and then reaching a deal or fa

August 19, 2025

China Slow Diversification: Gold And Others

August 19, 2025 8:05 AM UTC

China’s diversification from U.S. Treasuries appears to be at a slow pace. Gold is the obvious alternative if geopolitical tensions were to rise or skyrocket in the scenario of a China invasion of Taiwan. However, Gold holdings are merely creeping higher and suggesting no urgency from China

August 18, 2025

U.S. Strategic Fiscal Comparisons

August 18, 2025 9:05 AM UTC

The U.S. short average term to maturity is a structural fiscal weakness if higher rates lift U.S. government interest costs close to the nominal GDP trend. Hence, Trump’s pressure for fiscal dominance of the Fed to deliver lower policy rates and reduce U.S. government interest rate costs. Howeve

August 05, 2025

DM Rates: Slowdown Debate Trump’s Independence Question for Now

August 5, 2025 9:50 AM UTC

U.S. Treasury spreads versus other DM government bond markets or 10-2yr U.S. Treasuries are not yet showing a risk premium from the Trump administration attacks on the Fed and economic data. Debate over whether the U.S. is seeing a soft or hard landing are reemerging and this will dominate the outlo

August 04, 2025

Trump Tougher Posture with Russia

August 4, 2025 8:31 AM UTC

We suspect that Trump will not follow-through with an across the board secondary sanction on importers of Russia oil, as it would freeze U.S./China trade again and could boost U.S. gasoline prices – high inflation is one main reason for Trump’s softer approval rating. Trump could agre

August 01, 2025

Reciprocal Tariffs: Some Hikes, Deals and Delays

August 1, 2025 8:40 AM UTC

Though high reciprocal tariffs with some countries catches the headline, five of the top 10 countries with large bilateral deficits have reached framework trade deals, two have delays and three have higher tariffs imposed. With exemptions on some USMCA Canada/Mexico goods, plus phones/ semicondu

July 30, 2025

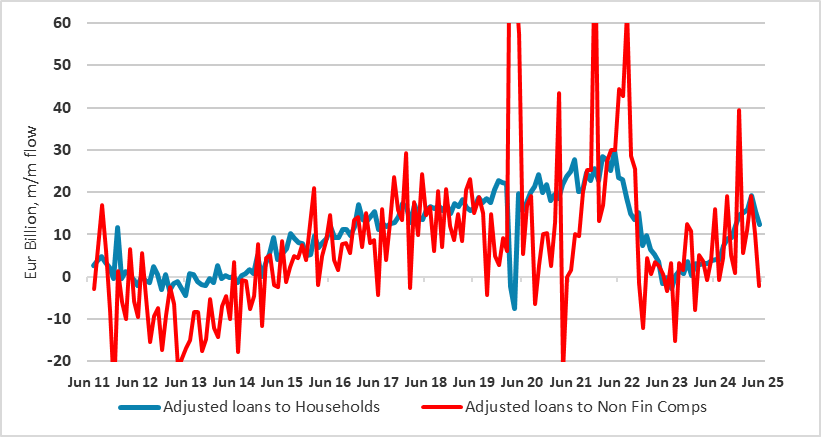

DM Household Sluggish Borrowing

July 30, 2025 10:45 AM UTC

· Overall, restrained credit supply from banks; abundant employment/income or wealth for most households but restrained financial conditions for low income households could have restrained household lending growth to GDP. However, the surge in government debt and ensuing fear of fut

July 28, 2025

U.S.-EU Trade Agreement: More a Framework Than a full Deal

July 28, 2025 9:08 AM UTC

In what seems to have been a fully-fledged political capitulation to the U.S. the EU, it seems, is accepting an agreement that would see an almost-blanket reciprocal 15% tariff on its exports to the U.S. But there still some imponderables, not least the range of sectoral concessions, whether EU me

July 24, 2025

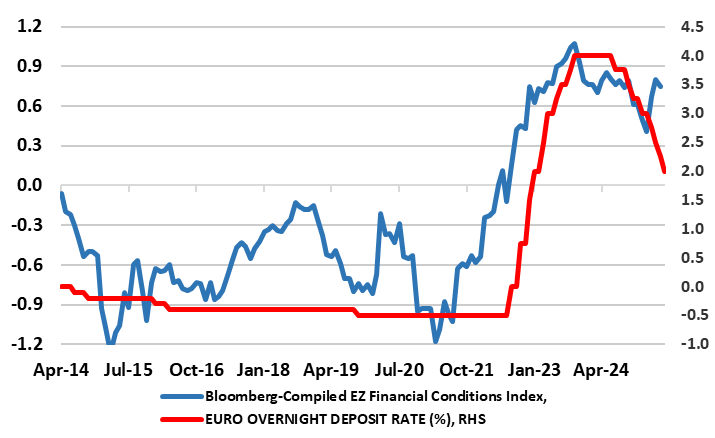

ECB Review: Policy ‘On Hold’ Leaves Easing Door Open

July 24, 2025 1:48 PM UTC

Given the uncertainty overhanging policy makers worldwide, let alone in the EZ, the ECB was always likely to revert to stable policy after seven consecutive cuts which have taken the discount rate to its current 2%. In a much shortened statement, but which was more willing to highlight disinflatio

July 23, 2025

Trump Deals: Japan, Philippines and Indonesia

July 23, 2025 8:26 AM UTC

• Other countries cannot be guaranteed to get a Japan style deal, both as Japan is the key geopolitical ally in the Asia pivot against China and as Trump is keen to agree deals by August 1. India and Taiwan are trying to finalize deals, but the EU is more difficult. China 90 day deadlin

July 22, 2025

DM Rates: QT adds to Budget Deficits Pressures

July 22, 2025 10:05 AM UTC

· Heavy issuance due to the U.S. budget deficit, plus Fed rate cuts will help further yield curve steepening in H2 2025. In EZ and UK, ECB and BOE QT is large and amplifies the amount of debt that the rest of the market has to absorb, which will also drives yield curve steepening al

July 21, 2025

2yr Germany and ECB Expectations

July 21, 2025 10:07 AM UTC

· Money markets are putting too much weight on ECB communications and we feel that a softening labour market/financial conditions and more tariffs from the U.S. will be enough to shift the ECB to deliver two final 25bps cuts in H2 2025. Though the 2yr Germany to ECB depo rate spread w

July 17, 2025

Trump’s Tariffs and Markets

July 17, 2025 12:00 PM UTC

The assumption in financial markets is that some trade framework deals will be done by August 1; some countries will make enough progress to be given an extra 30 days and some countries could have higher tariffs implemented. This would be broadly consistent with the average 15% tariff that is widely

July 16, 2025

ECB Preview (Jul 24, Part Two): Policy Pause Despite Tighter Financial Conditions

July 16, 2025 1:07 PM UTC

The next ECB Council meeting decision on Jul 24 looms but (as we noted in the part one preview) markets (understandably) sees no further cut, at least at that juncture. However, we think that the ECB will ultimately still have to ease further - two more 25 bp cuts in H2 - and would not even rule o

July 15, 2025

ECB Preview (Jul 24, Part One): Labor Market Looking Softer than Council Thinking

July 15, 2025 8:45 AM UTC

The next ECB Council meeting decision on Jul 24 looms but where market (understandably) sees no further cut, at least at that juncture. Indeed, the ECB may signal signs of economic resilience albeit noting that the added uncertainty emanating from the latest U.S. tariff threat warrants more circum

July 14, 2025

Tariffs: Seeking a Trigger for the TACO Trade

July 14, 2025 4:28 PM UTC

It has been fairly clear for some time that 10% represented a likely floor for the eventual Trump tariff regime. However, expectations that Trump would not be willing to go dramatically above that are being tested. A rate in the mid-teens still looks the most likely outcome, as the economic damage t

July 03, 2025

June ECB Council Meeting Account Review: Divides Continue if Not Widen

July 3, 2025 12:24 PM UTC

The account of the June 3-5 Council meeting just about left the door open for a move at the July 24 policy verdict given the array of news (probably negative particularly regarding tariffs but also bank lending) due beforehand. But the account adds to the impression we has initially that a pause

U.S. Assets and Valuation

July 3, 2025 9:30 AM UTC

The U.S. equity market has returned to be clearly overvalued on equity and equity-bond valuations measures and is vulnerable to a new correction in H2 on any moderate bad news (e.g. further economic slowing and corporate earnings downgrades). In contrast, U.S. Treasuries are at broadly fai

July 02, 2025

DM Central Banks: Overlooking Lagged 2021-23 Tightening and QT?

July 2, 2025 8:30 AM UTC

We are concerned that DM central banks are underestimating the lagged impact of 2021-23 tightening and ongoing QT, which impacts the transmission mechanism of monetary policy. Central banks need to consider cyclical and structural issues, but also need a more rounded view of the stance and implica

July 01, 2025

Trump Tariffs: Poker Face?

July 1, 2025 12:55 PM UTC

Our central scenario (but less than 50%) is towards a scenario of compromise, with some agreements in principle or trade framework deals, delays for most other negotiating in good faith but with one or two countries seeing a reciprocal tariff rise e.g. Spain and/or Vietnam. This could still be fol

June 26, 2025

June 25, 2025

June 24, 2025

Equities Outlook: Choppy Then 2026 Gains

June 24, 2025 8:15 AM UTC

Though the U.S. equity market has rebounded, we still scope for a fresh dip H2 2025 to 5500 on the S&P500 as hard data softens further to feed into weaker corporate earnings forecasts and CPI picks up and delays Fed easing. However, the AI story is still a positive, while share buybacks

DM FX Outlook: USD uncertainty increases as Trump changes the rules

June 24, 2025 7:05 AM UTC

· Bottom Line: After making initial gains after the election, the USD has followed a similar path to the first Trump presidency, falling back steadily this year as optimism on the economy has faded, with the introduction of tariffs contributing to more negative sentiment. Much as in the

June 23, 2025

Iran: Measured Next Steps?

June 23, 2025 3:17 PM UTC

A measured or modest Iran retaliation could be used by the U.S. to seek a path back towards negotiation. Israel would likely want to continue to degrade Iran nuclear and military facilities, but the U.S. could eventually pressure Israel to stop. This is our baseline, though the military attac

DM Rates Outlook: Yield Curve Steepening?

June 23, 2025 8:30 AM UTC

• We see the U.S. yield curve steepening in the next 6-18 months. 2yr U.S. Treasury yields can step down with cautious Fed easing on a modest/moderate growth slowdown and also if the Fed keeps an easing bias in H2 2026. 10yr U.S. Treasury yields face a tug of war between lower short-dated y

June 20, 2025

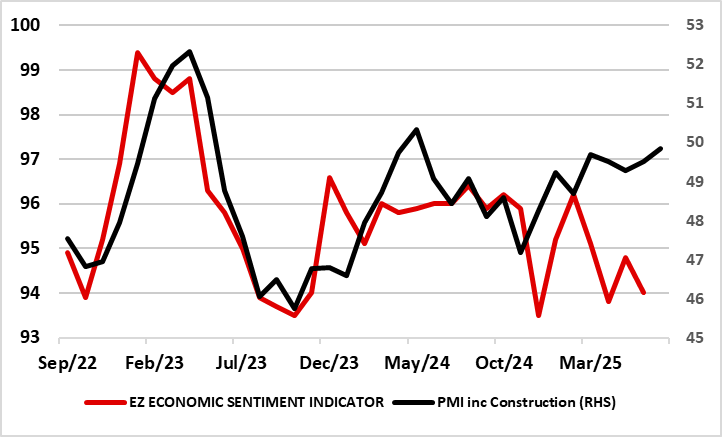

Eurozone Outlook: In Tariff Limbo Land?

June 20, 2025 9:24 AM UTC

· Amid what may still be tightening financial conditions and likely protracted trade uncertainty, we have pared back the EZ activity forecast for 2026. However, the picture this year appears to be slightly better but this is largely a distortion and we think that the economy has instead

June 12, 2025

Trump Tariffs: China and July 9 Reciprocal Deadline

June 12, 2025 7:17 AM UTC

We attach a 65% probability to a U.S./China reaching a new trade deal that reduces the minimum overall tariff to 15-20% imposed by the U.S., most likely agreed in Q4 2025 and to be implemented in 2026. However, a 35% probability exist of no deal and this could eventually mean higher tariffs (Fig

June 10, 2025

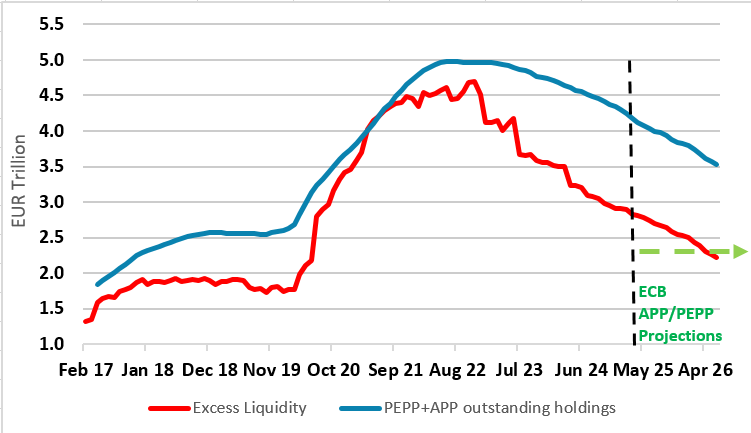

ECB: Time to Reassess and Slow QT?

June 10, 2025 2:25 PM UTC

Further ECB easing is on the cards, the question being whether this should start to encompass toning down quantitative tightening (QT) plans too! Notably, the two ppt fall in the discount rate cuts has come against a backdrop where the ECB has continued unconventional tightening by scaling back its

U.S. Deficit and Government Debt Concerns

June 10, 2025 9:00 AM UTC

The large U.S. budget deficit has helped push up 10yr real yields to 2% in 2024/2025, but both the budget deficit (heavy issuance) and government debt trajectories (sustainability and rating concerns) are key going forward if the 10yr budget bill passed is similar to the House Bill. Foreign acco

June 05, 2025

ECB Council Meeting Review: Easing Window Stays Open

June 5, 2025 1:58 PM UTC

This widely seen 25 bp deposit rate cut (to 2.0%) now means the previous degree of tightening has been effectively halved. Notably, it comes alongside an ECB policy and economic outlook/bias little changed from that of recent months. The door is thus left open for a move at the July 24 policy ve

June 04, 2025

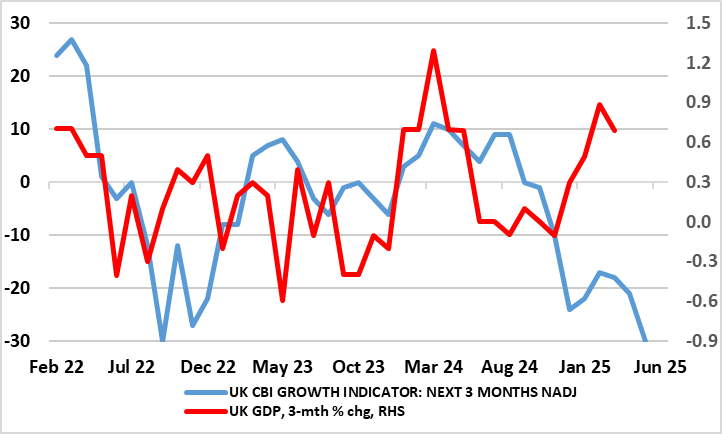

UK GDP Preview (Jun 12): GDP Still Overstating Activity?

June 4, 2025 10:20 AM UTC

After two successive monthly upside surprises, a correction back in GDP could be expected for the upcoming April data, especially as Q1 numbers may have been boosted by added production destined for the U.S in anticipation of tariffs. In addition, real estate activity seems to have slumped after t

June 03, 2025

Nato Summit 5% Target and Trump

June 3, 2025 10:48 AM UTC

Trump’s natural instincts will likely see extra pressure applied on Europe in the coming weeks to commit to 5%, but we do not see existential threats from Trump. In the end, our baseline is that NATO will agree a “soft” aim of 5% (3.5% hard military spending and 1.5% infrastructure/cybersecu

June 02, 2025

Trump’s 50% Steel And Aluminum: Negotiating Leverage?

June 2, 2025 7:42 AM UTC

• President Donald Trump increase in steel and aluminum tariffs from 25% to 50% is not just about boosting the steel and aluminum industry. It also a demonstration that Trump remains in control of tariffs and can aggressively change tariffs to increase negotiating leverage. It is a mess

May 30, 2025

Tax Foreigners Assets: How To Lose Friends

May 30, 2025 9:12 AM UTC

Increasing taxes on dividends on U.S. equities and corporate bond coupons would alarm foreign investors and hurt the USD and U.S. equities, as it would amplifies foreign investors concerns that they are overweight U.S. assets and the USD. Starting a capital war with investors into the U.S. is

May 29, 2025

Court Stops Trump Reciprocal and Fentanyl Tariff

May 29, 2025 7:18 AM UTC

• The Trump administration will likely follow a multi-track response by appealing the judgement but also fast-tracking section 232 product tariffs for pharmaceuticals and semiconductors. The administration could also consider section 301 or 122 tariffs (the latter 15% for 150 days against c

May 28, 2025

ECB Council Meeting Preview (Jun 5): Much Earlier Sub-Target Inflation Outlook?

May 28, 2025 2:30 PM UTC

What is widely seen as an eighth 25 bp deposit rate cut in the current cycle on June 5 may be overshadowed by the ECB’s implicit if not explicit shift about the outlook thereafter. The door will be left open for a move at the July 24 policy verdict given the array of news (probably negative part

May 27, 2025

May 22, 2025

ECB April Account: Neutral Rate Not Necessarily a Terminal Rate

May 22, 2025 12:46 PM UTC

The account of the April 16-17 ECB Council meeting suggested that the policy decision was more of a clearly agreed consensus, this papering over continued divides regarding the outlook; the risks from tariffs; and where inflation risks lie. The seventh and widely expected 25 bp deposit rate cut (w

May 21, 2025

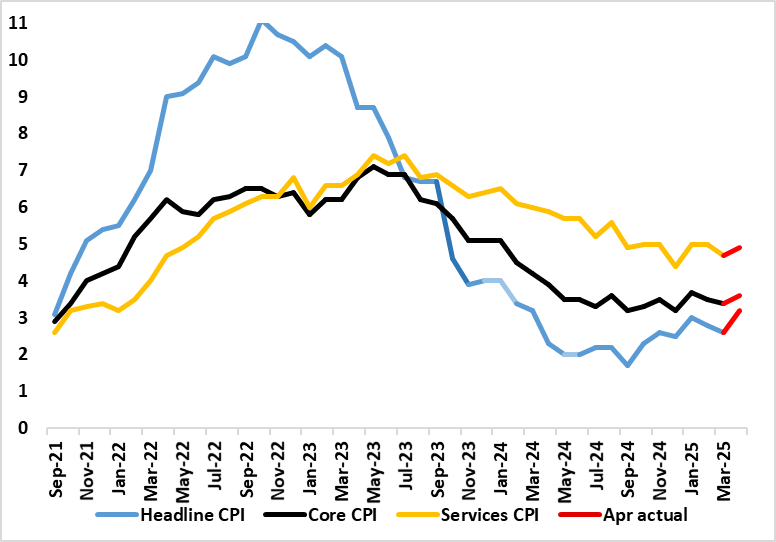

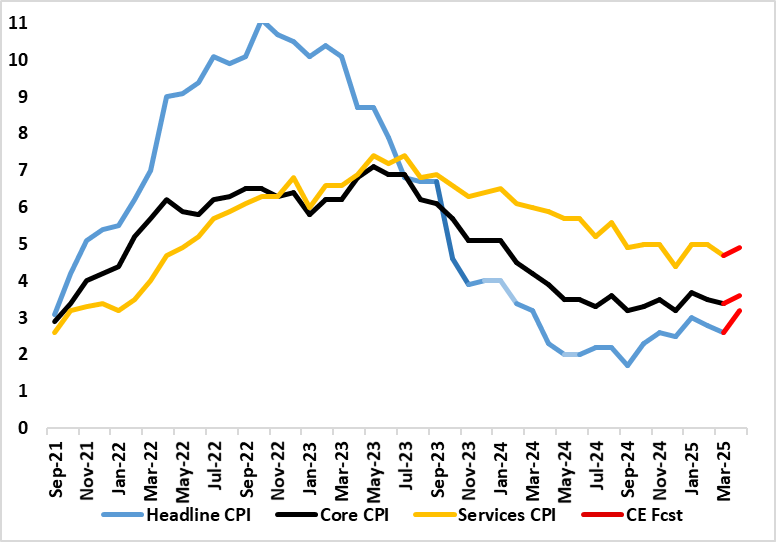

UK CPI Review (May 21): How Durable a Surge?

May 21, 2025 6:50 AM UTC

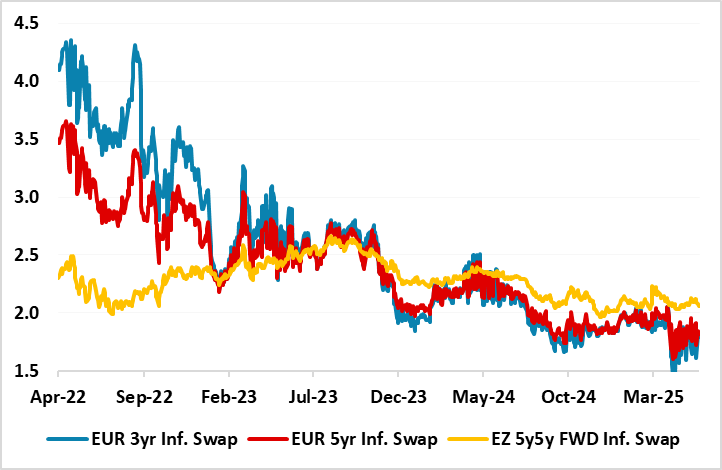

The UK and the rest of the DM world are now decoupling, at least in terms of inflation, where the UK is seeing a surge, (largely home-grown) just as W European sees their respective inflation fall back to, if not below, targets – although some measures if underling EZ inflation have started to edg

May 19, 2025

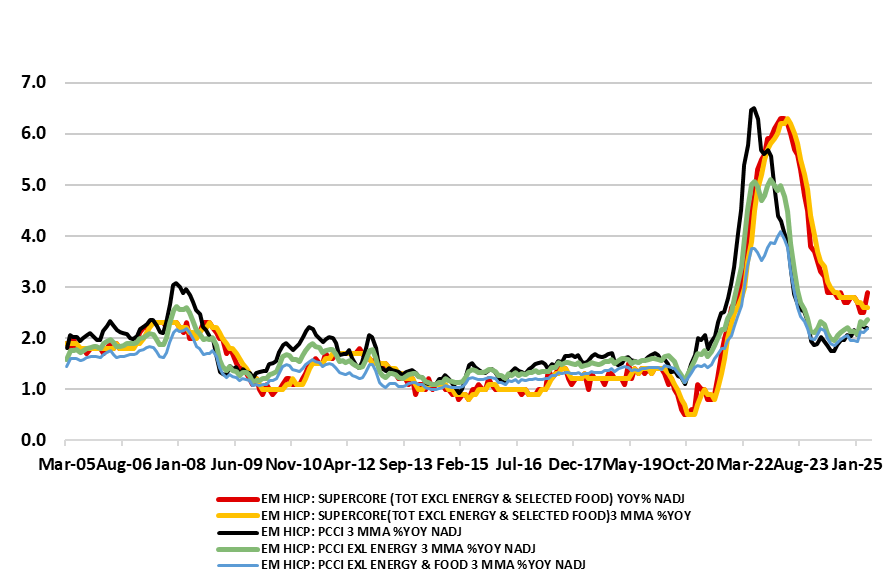

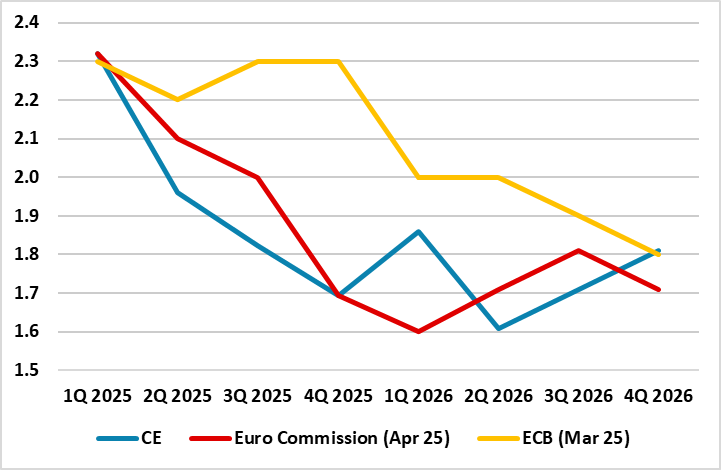

Eurozone: The European Commission Diverges From the ECB on Inflation

May 19, 2025 10:07 AM UTC

The European Commission (EC) Spring Forecast projects real EZ GDP growth in 2025 at 0.9%, some 0.4 ppt below its previous (autumn) view. There is also a downgrade to the 2026 growth picture by 0.2 ppt to 1.4%, projections that carry downside risks and where we think they are still too optimistic

May 15, 2025

UK GDP Review: Q1 GDP Jumps But Erratic and Overstating Activity

May 15, 2025 7:17 AM UTC

National account data delivered yet another upside surprise both in terms of the latest monthly figure and also the associated Q1 update. Indeed, February GDP, rather than consolidating in the March GDP release with a flat m/m reading, instead grew by 0.2% (Figure 1), a fifth successive non-negati

U.S./China Trade Truce Reduce Downside and Extra Stimulus Prospects

May 15, 2025 7:15 AM UTC

The alternative hard landing scenario in China has been reduced significantly with the trade truce with the U.S. However, China will still have to cope with a minimum 30% overall tariff, with only around a 10% reduction in the fentanyl tariff likely to be agreed in the coming months. Our baselin

May 14, 2025

Europe Portfolio Leverage Over Trump

May 14, 2025 9:05 AM UTC

The U.S. will likely introduce a 25% tariff on pharmaceuticals, which will increase pressure on the EU and other European countries (e.g. Switzerland) and also delay serious negotiations close to the 90 day reciprocal tariff deadline on July 9, adding to pressure on Europe by deliberately prolonging

May 13, 2025

Markets: Less U.S. Recession Risk, But Trade Headwinds

May 13, 2025 9:38 AM UTC

Though we had expected a U.S./China trade truce, the terms are more favorable to U.S. growth than we anticipated. Combined with the UK framework deal, we have revised down the probability of a U.S. recession from 35% to 20%. In turn we have revised up the end 2025 and end 2026 S&P500 forecasts t

May 12, 2025

UK CPI Preview (May 21): How Big and Durable a Surge?

May 12, 2025 2:32 PM UTC

The UK and the rest of the DM world are about to decouple, at least in terms of inflation, where the UK faces a surge, (largely home-grown) just as W European sees their respective inflation fall back to, if not below, targets. Although relegated by current market ructions and tariff threats, the

Trump Tariffs: China and UK Precedents

May 12, 2025 8:02 AM UTC

The U.S./China have announced major reductions in reciprocal tariffs to 10% with other measures postponed for 90 days. Though the U.S. is still imposing an extra 20% due to fentanyl, China will likely make some moves that could also help to reduce this. This is in line with our previous thinki

May 09, 2025

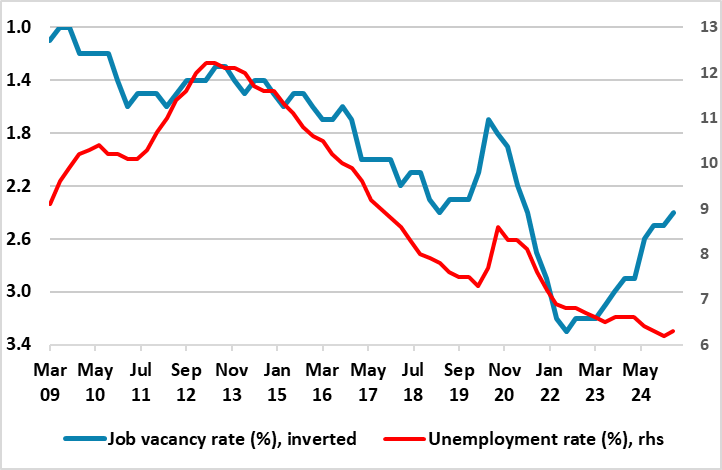

Household Divergence Into the Downturn?

May 9, 2025 10:55 AM UTC

Overall, the shock faced by the U.S. from tariffs is a negative supply shock, which can then be followed by job losses and restrained income and consumption growth. This 2 round can be amplified if a hard landing is seen and quickens job losses, which would really hurt low income households. Howev

UK GDP Preview (May 15): Q1 GDP Jumps But Underlying Picture Nearer Zero

May 9, 2025 9:32 AM UTC

We see the surprise and sizeable February GDP jump consolidating in the March GDP release with a flat m/m reading, this coming after that 0.5% jump (Figure 1). But there are downside risks given the possible (marked) correction back that may occur after what seems to be a very erratic February jum