Eurozone Outlook: In Tariff Limbo Land?

· Amid what may still be tightening financial conditions and likely protracted trade uncertainty, we have pared back the EZ activity forecast for 2026. However, the picture this year appears to be slightly better but this is largely a distortion and we think that the economy has instead been growing timidly on an underlying basis, with downside risks persisting and where some such risks may be materializing.

· All of this reflects the competing forces of planned defense and infrastructure-induced fiscal expansion in the EU against the activity and possible disinflation damaging tariff threat by the U.S. This juxtaposition of near terms risks and medium-term hopes has not dissuaded the ECB from continuing its easing but we forecast two more cuts in this cycle to a 1.5% ECB deposit rate, possibly at slower pace than of late.

· Details of the well-flagged fiscal expansion are still unclear but we feel it may be less sizeable, take longer to exercise and be less broadly spread across the EZ than perhaps the European Commission would have us believe. It may not trigger a fiscal crisis but could mean financial conditions remain tighter for longer than otherwise!

· Forecast changes: Compared to the last outlook, we have on balance downgraded the overall EZ growth outlook, with a slightly less-fragile further recovery for 2025 but a paring back for growth in 2026. More notable, then is the hardly-revised and still-soft EZ HICP inflation outlook in which the target is undershot on a sustained basis into 2025 and beyond. As a result of the growth revision, we now envisage deeper ECB policy rate cuts this year.

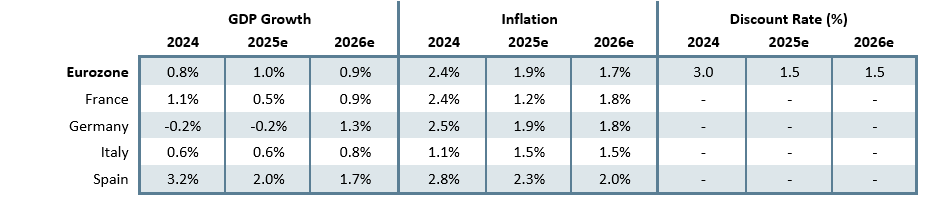

Our Forecasts

Source: Continuum Economics, Eurostat

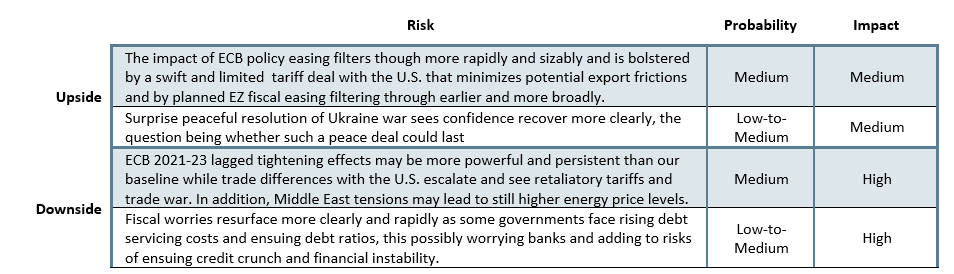

Risks to Our Views

Source: Continuum Economics

Eurozone: Will the EU be Made Trump’s ‘Whipping Boy’?

The EU and the EZ are facing complex negotiations with the U.S. on trade, defence and security as they seek to avert a transatlantic trade war while keeping Washington committed to Europe’s defence and engaged on Ukraine. The upcoming NATO Summit may see some overt progress with aspirations of Europe reaching for 5% of GDP defence and infrastructure spending, albeit not until the next decade. But the tariff situation remains and with signs that the EU could be signaled out by the US for ‘not playing ball’. This is despite that the EU’s sizeable surplus with the US being much more balanced once services are included and where EU offering carrots as well as sticks by buying more US energy, military and agricultural goods as a concession, even though the latter may be somewhat contentious has fallen on deaf U.S. ears as have the EU joining in blaming China. Indeed, the EU has refused to hold a flagship economic meeting with Beijing next month (known as the EU-China High-Level Economic and Trade Dialogue) because of a lack of progress on numerous trade disputes.

Indeed, the U.S. has indicated that countries would be informed before end-June about the reciprocal tariffs that would exist after the 90-day deadline on July 9. These are likely to be higher than the minimum 10%. However, the U.S. has admitted that the EU negotiations are unlikely to be completed by then, with the Commerce Department showing no urgency with ensuing expectations that Trump will delay for a further 30 or 60-day delay and possibly 90 days. Additionally, with the recovery in the U.S. equity market and still orderly CPI numbers, Trump could feel that the cost of extra tariffs could be lower than when he was recently forced into a U-turn. This could be done by imposing higher reciprocal tariff on one big surplus country. The obvious target is the EU and we attach a near evens probability that reciprocal tariffs are lifted to 20% after if not before July 9, both on the pretext that the EU is not caving in to U.S. pressure and as an example to other countries. The effective overall tariff rate would be even higher given already known tariffs on cars and steel and a likely similar 25% tariff on pharmaceuticals.

As for the economic impact, the ECB baseline scenario released earlier this month, which sees GDP growth of 0.9% this year and 1.1% next, assumes that all tariffs that were in place as of the cut-off date for the forecasts (May 14) remain in place. Specifically, that means US tariffs on goods from the EU increase from almost zero by 10 ppt and the EU doesn’t retaliate but also that trade policy uncertainty persists into 2027. But an alternative and more adverse scenario has US tariffs at 20% and where all tariff exemptions are eliminated and the EU responds with tariffs of about 10% on US goods. They knock 0.4 ppt off GDP growth in 2025 and 2026 and 0.2 ppt in 2027 from the baseline figures but with only modest. (0.1 ppt in 2026 and by 0.2 ppt 2027) disinflation results. These assumptions still look optimistic, helping rationalize our relatively soft(er) growth and inter-related inflation outlook even with a possible perkier consumer spending backdrop through this year and next, albeit at just over 1%.

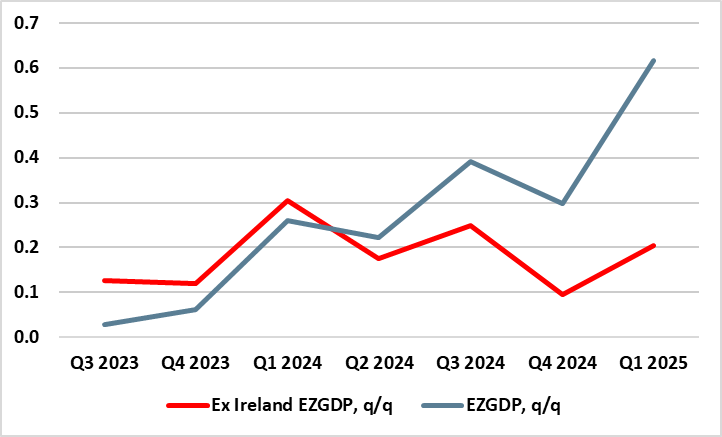

Even so, having lifted the EZ 2026 GDP outlook by 0.2 ppt to 1.3% three months ago, that forecast has been pared back to 0.9% - the 0.1 ppt upgrade for this year (to 1.0%) is more to do with the surge in Irish GDP in Q1 which tripled EZ Q1 q/q growth to 0.6%. But this Q1 jump is tariff-anticipation driven featuring clear export surges across the EZ. Notably these are not only unsustainable but likely to reverse in this and the coming quarter while the Irish-induced surge that has boosted EZ for some time now (Figure 1) hardly affects spare capacity (ie a negative output gap of around 0.5% of GDP this year) in the EZ as it reflects largely profits of multinationals which have seen a significant increase in factor income outflows – NB even the ECB sees a contraction in either this or next quarter. Our still soft outlook reflects a host of imponderables, some to do with the timing of likely fiscal and defense initiatives; some to do with to what degree they may boost EZ growth only modestly due to the likely large import content to begin with and also the extent to which they may be tempered by what may be more sustained tightening in financial conditions due to interest and exchange rates being higher than otherwise would be the case. There is also increased uncertainty emanating very much from political divides and policy paralysis in several countries (clearly France) and where, as suggested above, greater fiscal consolidation measures from several countries that will continue beyond next year this even if EU-wide fiscal rules are loosened as even Germany is now calling for.

As far as defence is concerned, fiscal restraints are clearly to the fore and hindering a fiscal boost that is hoped for. ReArm is partly to be financed by relaxed EU fiscal rules allowing the use of national escape clauses for up to 1.5% of GDP per year for defence purposes, allegedly enabling additional spending of about EUR 650 billion (4.3% of euro area GDP) over the next four years. But to date only a third of EU member states have signed up due to fiscal constraints, suggesting more than two-thirds of the EU GDP will not be making any use of this initiative!

In terms of our forecast the impact could be much more sizeable. US tariffs on steel and aluminium of 25% will hit already recession-bound EZ manufacturers, which export some EUR 3bn of steel and some EUR 2bn of aluminium, thus affecting approximately 1% of total goods exports with the US. But the damage could be much larger given the threat of tariffs based around so-called trade reciprocity. At this juncture we continue to consider the downside from actual tariffs as much as a sizeable risk than a quantifiable reality, but (as suggested above) cannot ignore the likely sustained impact of uncertainty weighing on activity into 2026.

Figure 1: The Irish Tail Wagging the EZ Dog

Source; Eurostat, CE

Fiscally, having tightened significantly in 2024 on account of the withdrawal of a large part of the energy and inflation support measures, we no longer see the fiscal stance continuing to tighten into 2026, the question being the extent of any rebound from the circa 3%-plus of GDP the budget deficit may reach this year. Thus, with an EZ headline budget gap that may rise into 2026, the fall in the EZ government debt ratio to 88.5% of GDP last year will likely soon be followed by a rise to above 91% in 2026. This is especially given that the EU Commission’s fiscal plan could ultimately mean the EZ primary deficit rising from just over 1% of GDP this year towards 3% raising question about fiscal sustainability afresh.

As for the trade balance, the anticipated cyclical, and possibly structural, recovery in imports into 2025 as well as what may be a weak global economy weighing on exports will also mean that the improvement in the current account surplus last year (at around 2.7% of GDP) may reverse into 2026. This is also a headwind to GDP growth.

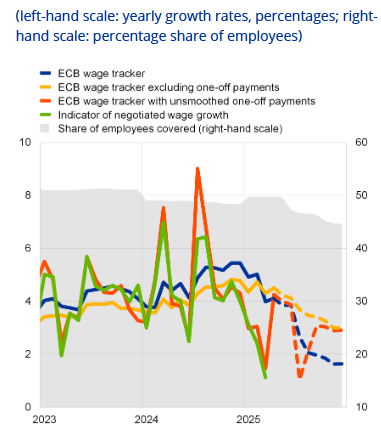

Amid what has been a disinflation process so far very much supply driven, but encompassing what has already been a marked softening of underlying inflation, we still envisage headline HICP staying below 2% more durably into next year with the core not far behind and then remaining below target through 2026. This picture is little changed compared to the previous Outlook, but encompasses evidence of softer cost pressures, especially in regard to wages (Figure 2). Indeed, the omens point to services inflation slowing even further in due course, something we think will emerge more visibly into 2025 as wage growth slows to pace consistent with the inflation remit.

Figure 2: ECB Numbers Further Suggest Wage Pressures Moderating Clearly

Source: ECB

ECB: Nearing the End?

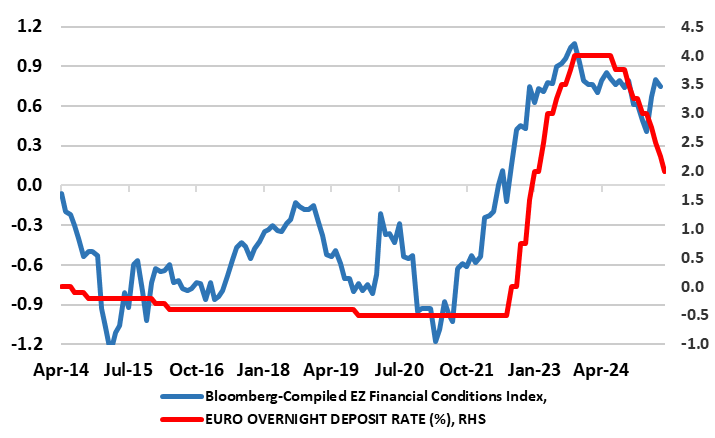

This widely seen 25 bp deposit rate cut earlier this month (to 2.0%) now halves the previous degree of official rates. Notably, it comes alongside an ECB policy and economic outlook/bias little changed from that of recent months. The door is thus left open for a move at the July 24 policy verdict given the array of news (probably negative particularly regarding tariffs but also bank lending) due in the interim. But we get the impression given that a pause may be due after what have been seven successive cuts, this also reflecting what may be clear(er) Council divides over the extent and direction of inflation risks – this explaining the apparent dissent. Regardless, the ECB’s updated forecast now show a much earlier drop in HICP inflation to below target, albeit with largely unchanged forecasts at around target for 2027 and what are also largely unchanged growth assumptions. Moreover, the ECB also draws comfort that more favorable financing conditions should make the economy more resilient to global shocks, this puzzling when such conditions have actually tightened of late (Figure 3), only partly due the exchange rate.

Figure 3: Policy Rates and Financial Conditions Diverging

Source: Bloomberg, ECB

As for market thinking about policy we think is fully justified enough to mean up to two more 25 bp cuts in H2 this chiming and then staying in place into 2027. Moreover, the ECB may/should even have to revisit the QT outlook. With this mind, we envisage that by the autumn the ECB may be flagging a slowing to QT, this encompassing some return to reinvesting maturing bonds.

Germany: Tariffs vs Fiscal Expansion

Along with many other forecasters we have returned to downgrading the German GDP outlook at least for this year and next. The U.S. tariff threat looms large and adversely in both size and possibly protracted) uncertainly features while the hopes for marked fiscal expansion alongside a distinct defence build-up looks more a story for late next year and into 2027 – NB: forecasts for that year are still being revised higher. Regardless, an agreement by Germany’s coalition partners and the Greens has amended the so-called debt brake and thus provides the economy with both fresh fiscal scope and new economic aspirations. But little is on the way just yet. While there is talk of a EUR 46bn multi-year package of corporate tax breaks over the summer this is still small beer (a cumulative 1% of current GDP by 2029). As for firm plans, Germany’s new fledging government has not yet presented any concrete budget plans with the risk that any eventual fiscal expansion could ultimately be weaker and/or delayed; expenditure on defence and public infrastructure growth could be hindered on the extent due to non-financial obstacles, for instance with regard to regulation and approval processes. Moreover, even under current ‘plans’ in terms of size, the planned deficit-financed infrastructure fund worth EUR 500bn (ie around 11% of GDP) is to be spread over a ten-year period.

The bottom line is that a German budget gap that looked to be around 2% of GDP could turn into one of well over 4% probably not this year but into and beyond 2026. As a result, the government debt ratio would rise from its current 63% of GDP to above 80% over the next decade possibly without negative repercussions – not least as Germany has already suggested EU-wide fiscal rules (which this initiative compromises) need to be relaxed. But added government spending will boost imports even if defense has an aspiration attached of being directed towards domestic/European producers. As a result, it looks very likely that the circa-6% of GDP current account surplus likely this year will be reduced down towards 4% in 2026 – both helping growth elsewhere and politically speaking addressing the source of what may be growing trade tensions and trade wars.

We see German GDP picking up to 1.3% next year (0.2 ppt lower than than envisaged in the last Outlook) after a lame and downwardly revised drop of 0.2% this year, but there are many imponderables over and beyond a tariff threat which Germany is very exposed to. A likely eventual 20%-plus tariff would hit GDP by at least a 0.4% drop in GDP. But added uncertainties include the stronger euro (particularly perturbing the Bundesbank, but also reflect several factors more peculiar to Germany at this juncture, the most notable being that not only will it take time for the additional spending on both defense and infrastructure to take effect but there is little spare capacity, certainly in the German labor market – the exception may be the recession-bound construction sector – NB; In 2025, actual earnings will still see weaker growth than negotiated wages, the latter down to 3% from 4% last year, mainly a result of lower performance bonuses.

As for inflation we have not altered our below target projections for this year and next and await more details; fiscal moves may possibly boost Germany’s lame potential growth rate. But the tariffs pose added downside risks to inflation (Figure 4). These uncertainties make any GDP breakdown outlook harder to estimate. But better real income growth may see consumer spending growth recover.

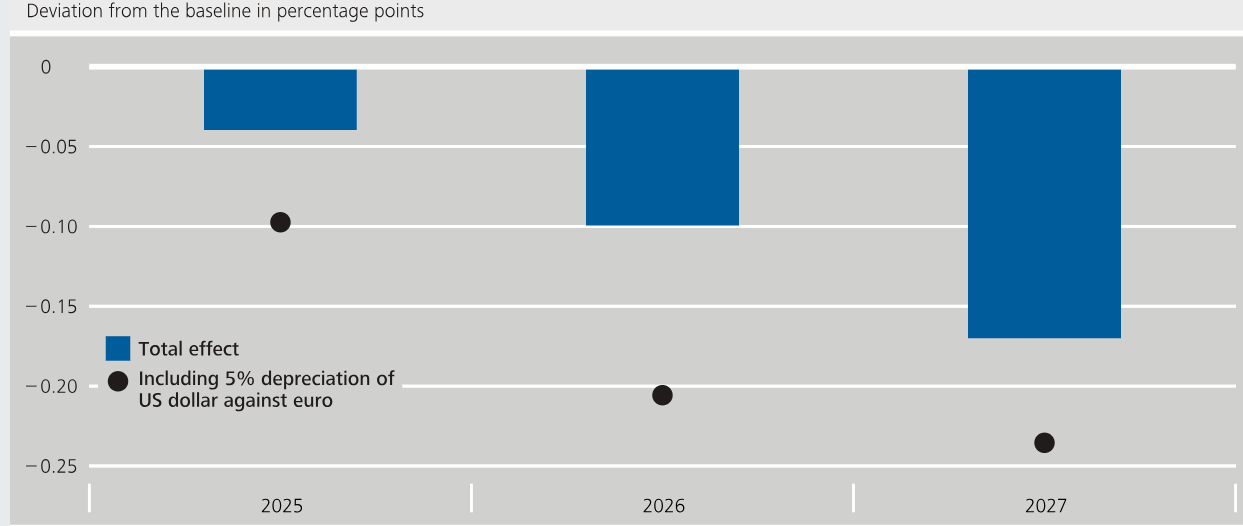

Figure 4: Alternative Scenarios for German CPI Inflation on Added Tariff Imposition

Source: Bundesbank – total effect is purely from tariff

France: A Political (and Fiscal) Crisis Still Bubbling on the Back Burner

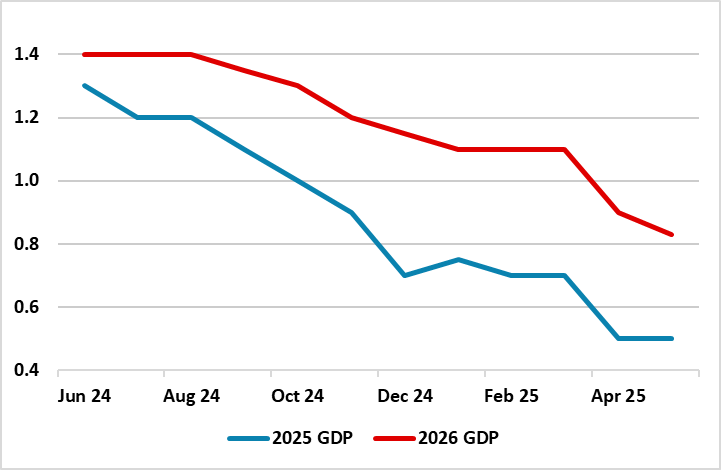

Yet again, we have made little change to the French economic outlook for this year or next, albeit seeing GDP growth being pared back from 0.7% and then 1.1% three months ago to 0.5% and 0.8% for 2025 and 2026 respectively. These are similar to current consensus thinking, albeit where the latter has undergone a much more protracted downgrade in recent months (Figure 5). But there is an array of factors at work, mostly negative. Admittedly, the planned German fiscal expansion was and remains very good news for France. As important was Germany’s call for EU-wide fiscal rules to be relaxed, this all the more important given the large budget deficit that France is facing as fiscal restraint continues to be the underlying theme. In fact, we do not see France being a major part of any clear defense-based fiscal expansion given its adverse budgetary backdrop and outlook. Indeed, the European Commission has made clear that countries should consider ramped up defense spending – ‘if they have the fiscal space’. And even with what may soon be watered down EU fiscal rules, a French budget gap (both headline and structural) that may be over 5% of GDP even beyond next year risks seeing the debt ratio (likely to rise to toward 120% of GDP next year) rise even further on the back of high primary deficits and rising interest payments, whereas the debt-reducing effect stemming from nominal growth is projected to moderate compared to recent years. In addition, the political situation hardly bodes well for the fiscal picture. Admittedly, February did see the minority administration force through a budget bill, thereby avoiding the fall of the government and ensuing accentuating political uncertainty. But the cost was that planned fiscal consolidation has been scaled back so that the 5% of GDP aspiration has now turned into a planned gap of 5.4% this year and as suggested above, we (and many others) see upside risks, not least given the concessions required to secure political support for the budget amid both parliamentary fragmentation and an absence of broad-based popular support. Indeed, we still see the risk that the fragile government may be toppled after July when fresh parliamentary elections can be called.

With this in mind we reiterate that France does not (yet) face a fiscal crisis but still faces a tighter fiscal stance into 2026 and beyond. Admittedly, given France’s large defense industry (providing almost 10% of global arms exports), it should be beneficiary of added EU spending – hence its demands that the EUR 150 bln proposed loans from the EU be not be frittered by buying from outside the EU.

Regardless, the 2025 GDP picture is partly distorted by weakness from late-2024, but Q4 2025 y/y growth will also be around 0.5%. As for details, this year’s growth weakness reflects both the contractionary fiscal stance coupled with economic and policy uncertainty, both domestic and from the global environment. A recovery in imports will detract from GDP growth in 2025, while private investment is projected to be subdued, as the surge in uncertainty weighs on capital expenditure. In contrast, consumption is expected to be bolstered by increases in real wages, but the saving rate should remain high at over 17%, against the background of stagnant consumer confidence. Next year, activity should gain a little more momentum, on the back of declining credit cost and a slightly less contractionary fiscal stance.

However, this soft growth outlook will reinforce the broad disinflation already very much evident. In fact, price pressures have fallen more than we thought three months ago and we now envisage CPI inflation at 1.2% this year (ie pared back by 0.6 ppt and likely to stay under 2% through 2026, albeit with risks on the upside from possible fiscal measures. This inflation picture will not help the fiscal side and reflects a continued reining in pricing power and a rise in the unemployment rate back toward 8% through 2025 and perhaps 2026 and where companies are likely to see profit margins fall further!

Figure 5: GDP Outlook Poorer as Consensus Tallies With Our Gloom

Source: Bloomberg, % chg y/y

Italy: Staying Out if the Policy Limelight

We see little rationale to alter our growth outlook save for the 0.1 ppt upgrade to this year due a slightly better than expected Q1 GDP outcome. Admittedly, this year’s projection of 0.6% would be up on the miserly 0.5% of last year but this is partly base effects as crucial in this outlook is the consumer, where spending last year was anemic due to restrictive financial conditions but mainly to the wind-down of the Superbonus building tax credit (a generous tax incentive for housing renovation). But amid what has been a still-falling jobless rate (despite record-high labor force participation) and actual real wage growth (nominal gains of over 3% are seen again in 2025), the consumer should bounce back – something like 1% gains are possible in both the coming two years, even given CPI inflation picking up slightly to 1.5% this year and something similar into 2026 (both little changed from three months ago). The question is whether this recovery will fuel a pick-up in imports, this one reason for a small downgrade to the 2026 GDP picture to 0.8%. As a result, even given a consumer-related pick-up in import growth, we see the current account surplus staying just over 1% of GDP in the coming two years but with upside risks at time goes by as Italy’s large arms exports (5% of the global market) benefits from rising EU defense spending.

These forecast are very similar to those updated by the Bank of Italy (BoI) earlier this month, and chime with the consensus, albeit where the latter has seen clear downgrades now to match our thinking. In this regard, and as we underlined three months ago, Italy is unlikely to be major victim of any U.S. trade restrictions in the coming two years, save for some damage to its transport sector. But the outlook is still sobering an outlook very much squaring with current and somewhat soft business survey data but also bank lending showing still negative growth in the corporate sector. But there are downside risks; BoI estimates suggest should U.S. tariffs rise to the levels announced on 2 April and uncertainty remain high, GDP growth might be around 0.2 percentage points lower than under the baseline scenario for the current year.

But another downside risk is that the wind-down of the Superbonus triggers a larger and more persistent contraction in housing investment, the latter having been a key source of growth over 2021-23. But on the upside, the acceleration in public investment related to the National Recovery and Resilience Plan could boost growth in 2025-26 more than expected, not least as a full utilization of New Generation EU funds implies that such-related spending needs to be ramped up from about 1% of GDP in 2024 to about 2.5% of GDP on average over 2025-26.

As was the case three months ago, fiscal worries seem contained, although the any fall in sovereign spreads vs Germany at a 10-year horizon compared to the last Outlook is as much a German story than matters Italian. Partly this reflects genuine fiscal improvements, albeit largely a one-off result of the unwind the Superbonus scheme. However, the budget deficit is forecast to edge down a further notch to 3.3% of GDP, on the back of a marginal improvement in the primary surplus and unchanged interest expenditure as a share of GDP and a small rise in the tax burden is expected to rise marginally. In 2026, the deficit is expected to fall to 2.9% of GDP and the primary surplus to reach as high as 1.1% of GDP on the back of moderate primary expenditure growth. Even so, the European Commission warn that even into 2026, a continued rise in interest expenditure to 4% of GDP will mean the debt-to-GDP ratio is expected to increase one ppt in both 2025 and 2026 to over 138%. Thus, we still feel the current sovereign spread is too low but not significantly so.

Spain: Slowing Signs Emerging Across the Board?

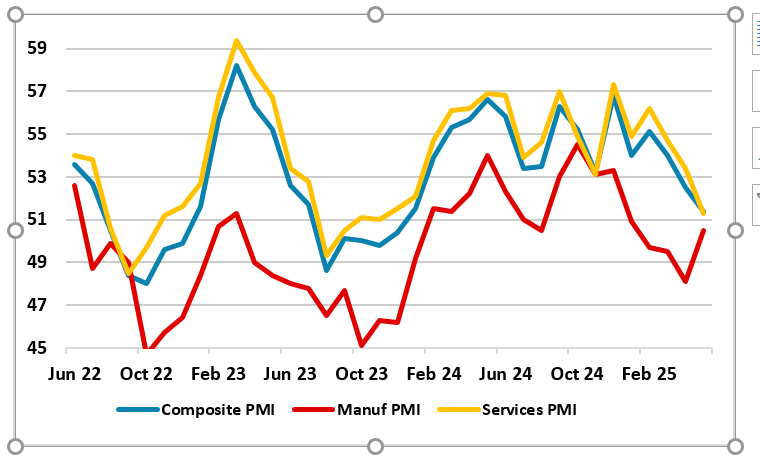

Business survey data suggest that the modest slowing in GDP growth in Q1 will not only continue but probably intensify, with the main worry being the extent to which hitherto robust service sector activity, that has been the backbone of recent GDP growth, is falling away. In this regard, May’s headline composite PMI slipped further and to just above the apparent growth threshold, largely due to weak activity in the service sector (Figure 6), also the softest performance since late 2023 and seemingly reflected to uncertainty stemming from tariffs. This is all more notable and concerning in two ways. Firstly, Spain has been considered to be less vulnerable to likely US tariffs with less than 1% of GDP stemming from exports to the U.S., less than half the EZ average. Secondly, given that the EZ more recently has been driven solely by services and it is the fact that Spain’s economy has a much larger share of services in its make-up compared to the EZ average (75% vs 70%) that has helped the country to out-perform. Some of this reflects a tourist backdrop which has seen a 6%-plus y/y rise in international visitors but where the growth may now have peaked, not least due to high prices, over-crowding and the growing resistance from locals regarding apparently excessive overseas visitors. But this is not the whole story as service exports have led the way in the recent past, led in particular by banking to engineering services.

All of which has helped persuade us to downgrade the GDP picture for the first time in several Outlooks. Admittedly, still very much at the top end of the EZ growth ladder and where Spain’s economy by end 2026 is likely to over 10% larger than it was by end-2019, twice that of the rest if Eurozone. That gap may increase further, not least after a 3.2% GDP surge in 2024, growth slows to ‘only’ a 2.0% in 2025 (pared back 0.2 ppt) and then to an unchanged 1.7% in 2026, albeit where base effects still pull up the 2025 figure and help mask an actual slight pick-up in q/q rates through 2026. But over and beyond other factors also explain a slowing, these more accounting for the weak 2026 picture. There is going to be no rapid defence build-up, amid an aversion to the military – this largely explains why the country is at the bottom of the NATO ladder in spending just 1.3% of GDP on defense. This aversion is clearest among the current minority Socialist administration, but it has succumbed to EU pressure to lift such spending to 2% - now suggesting it will try to reach this in 2025 but with still with clear reservations. But this is complicated as Spain may face snap elections amid the current corruption scandals and still has its own fiscal problems with structural budget gap of just over 3% of GDP last year widely seen persisting into 2026, all keeping the debt ratio at around 101% of GDP.

But there is also an emerging shift in demographics. To date, Spain has seen a robust labor backdrop which has seen a marked rise in the Spanish workforce (largely a reflection of returning emigration) enough to have effectively increased the economy’s potential growth rate. But that workforce rise has started to reverse and that this may continue. In addition, there are questions about productivity. As the IMF has noted, Spain's GDP per capita shortfall with high-income EZ economies and the U.S. is mainly due to a productivity underperformance, where Spanish tech firms lag in productivity and innovation, partly due to weaker R&D investment with little sign of any looming improvement not least given a poor infrastructure backdrop the latter highlighted by April’s electricity blackout!

Figure 6: Surveys Suggest Some Slowing Underway – Even in Services?

Source: Markit

As for details, additional housing wealth, lower inflation and still solid jobs growth may mean that household spending becomes the mainstay of growth this year, partly offsetting the lags likely from net trade and the public sector. Indeed, the unemployment rate may continue to fall, although its reduction will be moderate from 11.4% in 2024 and below 10.5% in 2026. Regardless, we still see a largely unchanged current account surplus of just over 2.5% of GDP both this year and through 2026.

On the inflation side, we expect the underlying trend to be one of more modest moderation, if not consolidation. Indeed, we see inflation slowing to an average of 2.4% this year (a slight upgrade due to swings in energy prices) but with the projection of 2.0% for 2026 intact. This reflects some slowing in terms of services inflation, reflecting a limited impact of the so-called second-round effects.