Trump Tariffs: China and July 9 Reciprocal Deadline

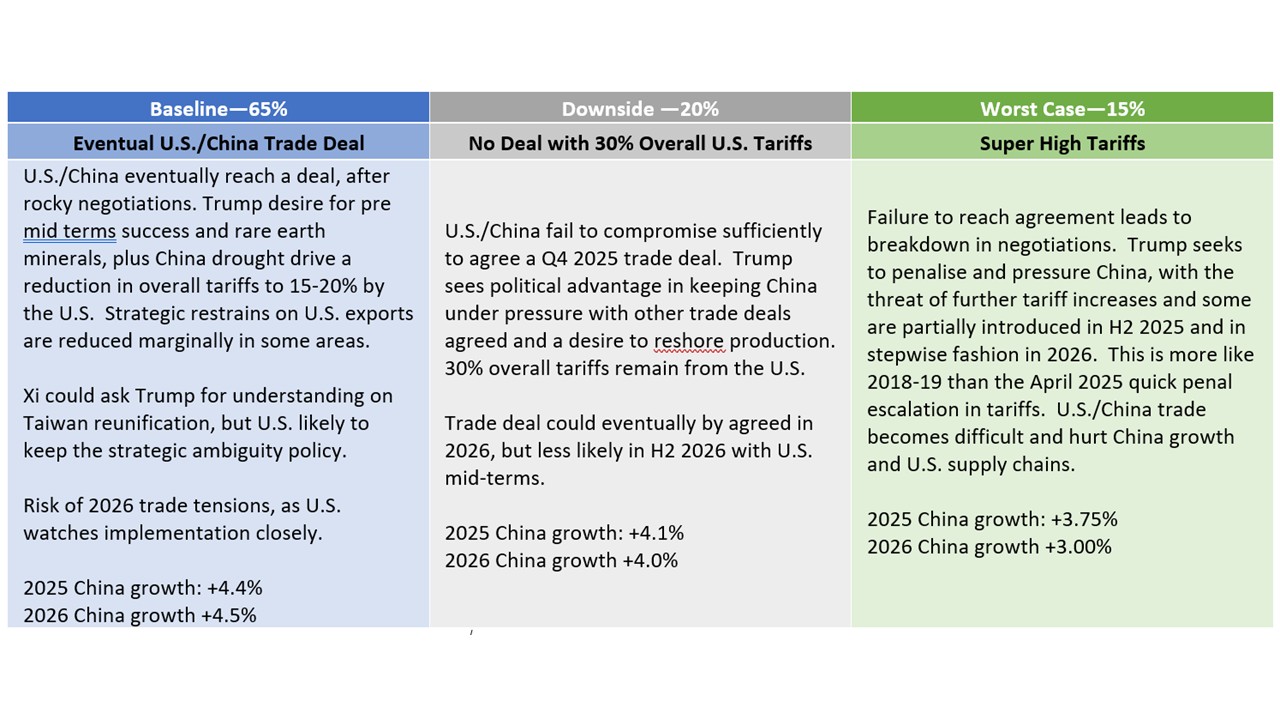

We attach a 65% probability to a U.S./China reaching a new trade deal that reduces the minimum overall tariff to 15-20% imposed by the U.S., most likely agreed in Q4 2025 and to be implemented in 2026. However, a 35% probability exist of no deal and this could eventually mean higher tariffs (Figure 1). Meanwhile, the Trump administration sending out post July 9 reciprocal tariff rates is more than a negotiating tactic before a further 90-day delay. The delay could be less than 90 days or the EU could be singled out with a 20% reciprocal tariff after July 9 to pressure the EU and other countries.

· Figure 1: U.S./China Trade Scenarios

Source: Continuum Economics

President Donald Trump is proclaiming a trade deal with China, whereas it a trade truce before difficult negotiations in the next 6 months on a phase 2 trade deal. Meanwhile, Trump on Wednesday threatened higher reciprocal tariffs after July 9 if trade deals are not done. Key points to note

· China. Trump has proclaimed victory in a trade deal with China, with reassurance on rare earth exports from China. The trade deal in reality is a trade truce, as it largely reverses the April spiral of tariffs. The trade truce in Geneva and reaffirmed in London means that exports to the U.S. have restarted and the fragile nature of U.S./China relations means that an incentive now exists for China to speed exports to the U.S. at the current 30% tariffs. The real discussions on a trade deal can now start. The U.S. and China want to avoid a hard break in trade, due to supply chain problems and a hit to growth. However, negotiations will likely be prolonged like 2019, as the U.S. wants more commitments than the phase 1 deal. The two sides have big differences on how much the trade surplus should be introduced and whether financial penalties should be imposed if targets are not meet. Even so, Trump has to show progress before the November 2026 mid-terms, while also having a weakness for China rare earth minerals. China also needs to import more food given the current drought. A compromise by both sides is likely in the end and we attach a 65% probability to a phase 2 deal being reached (Figure 1). This would most likely be Q4 2025. However, the other two scenarios are for no deal (Figure 1), as the U.S. and China could find it difficult to reach the necessary compromises. This could be with either 30% tariffs or super high tariffs, which would have adverse consequences for the Chinese and U.S. economies.

· July 9 Reciprocal tariff threats. Trump on Wednesday indicated that countries would be informed in the next 2 weeks about the reciprocal tariffs that would exist after the 90-day deadline on July 9. These are likely to be higher than the minimum 10%, but could be lower than the maximum. This is classic Trump negotiations of a threat and using a deadline as pressure to get a deal. The U.S. is reported to be in active negotiations with Japan/S Korea/India/Taiwan and Vietnam and deals could be reached in the next 3-4 weeks. However, the U.S. has admitted that the EU negotiations are unlikely to be completed by then, with Commerce secretary Lutnick yesterday suggesting they are towards the back of the queue. Expectations that this is a Trump bluff could slow negotiations however, on the assumption that Trump will delay for a further 90 days until Oct 9. This could be a dangerous assumption, as Trump likes unpredictability and negotiating leverage. One option could be a 30 or 60 day delay rather than 90 days. Additionally, with the recovery in the U.S. equity market and controlled monthly core CPI numbers, Trump could feel that the cost of extra tariffs could be lower than when he was forced into a U turn. This could be done by impose higher reciprocal tariff on one big surplus country. The obvious target is the EU and we attach a 40% probability that reciprocal tariffs are lifted to 20% after July 9, both on the pretext that the EU is not caving in to U.S. pressure and as an example to other countries.