North America

View:

July 01, 2026

Macro and Market Implications of 'Super' El Nino Risks

July 1, 2026 8:08 AM UTC

El Nino, and a potentially severe one, is increasingly looking like a central scenario rather than a tail risk for 2026-27.

2026-27 El Nino is shaping up to be strong enough to matter, at least for scenario planning.

The key facts are broadly: Australia, New Zealand, Indonesia and South Africa are l

June 30, 2026

AI Boom and Bust?

June 30, 2026 10:45 AM UTC

• While some are becoming wary that AI bust could arrive in coming quarters, AI labs revenue growth has been explosive and this sustains the vertical chain of datacenter demand and commitments for the hyperscalers and also buoyant semiconductor demand. For 2027 and 2028 capital markets re

June 26, 2026

U.S. Trimmed Mean and Median PCE Price Indices not as strong as Core PCE

June 26, 2026 7:05 AM UTC

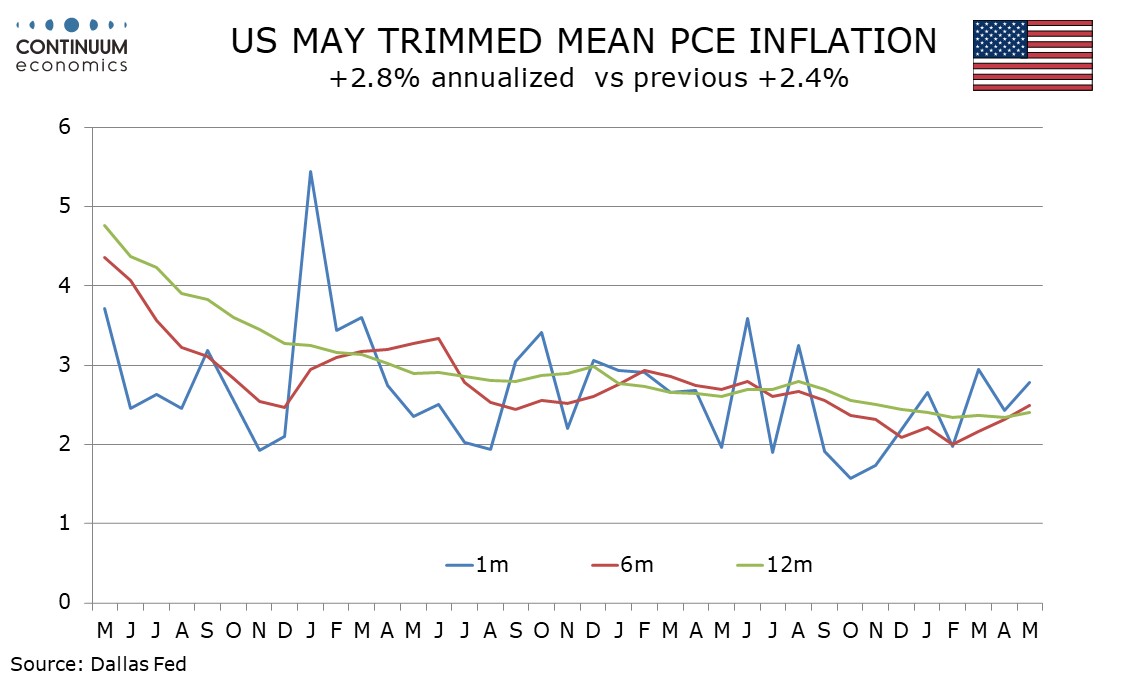

The Dallas Fed’s Trimmed Mean PCE inflation index, which is reported to be a series favored by Fed Chair Kevin Warsh, as well as the Cleveland Fed’s Median PCE price index, look a little less alarming than the Fed’s officially targeted Core PCE price index. This could be used as an argument ag

June 25, 2026

U.S. Trimmed Mean and Median PCE Price Indices not as strong as Core PCE

June 25, 2026 6:19 PM UTC

The Dallas Fed’s Trimmed Mean PCE inflation index, which is reported to be a series favored by Fed Chair Kevin Warsh, as well as the Cleveland Fed’s Median PCE price index, look a little less alarming than the Fed’s officially targeted Core PCE price index. This could be used as an argument ag

June 23, 2026

DM Rates Outlook: Tightening or Easing?

June 23, 2026 8:15 AM UTC

· With the U.S./Iran interim agreement likely to hold and energy prices softening, our projected consumer slowdown will likely tilt the Fed not to hike in H2 2026 and to actually ease by 50bps in 2027, with 25bps moves in both Q2 and Q3. With 2yr yields consistent with a hike, the tra

June 22, 2026

U.S. Outlook: Consumers Looking Vulnerable

June 22, 2026 2:17 PM UTC

• The US economy is showing resilience with strength in investment offsetting a gradual slowing in consumption, though consumer spending, which is running well ahead of real disposable income, looks set to slow further. This is likely to see the economy slow in the second half of 2026 even

Equities Outlook: AI Optimism, But Caution Elsewhere in DM economies

June 22, 2026 7:05 AM UTC

· In terms of the S&P500, we remain less concerned about high valuations in the tech sector provided AI labs growth remains fast. 12mth fwd information technology are mid-range in the 2020-26 experience rather than at the highs. Even so, heavy equity issuance by tech companies and a s

June 15, 2026

U.S./Iran Interim Deal and Reopening Strait of Hormuz

June 15, 2026 12:32 PM UTC

· Our baseline (80%) is that the Strait of Hormuz will reopen in H2 2026 and remains open through 2027. However, logistics dislocation plus a switch from commercial inventory rundown to rebuilding will likely slow the decline in oil prices back towards normal levels (Figure 1). O

June 12, 2026

Fed Tightening and U.S. Treasury Yields: 1994, 1999 and 2022 Redux

June 12, 2026 7:05 AM UTC

Our baseline involves no Fed hike, but 50-75bps is feasible in a plausible adverse scenario. In this alternative scenario of 50-75bps of Fed tightening it is easy to build the case for 2yr yields going to 4.30-4.40% area, before thoughts turn to H2 2027/28 involving modest Fed rate cuts. 10yr

June 10, 2026

Financial Markets/Policymakers and the Strait of Hormuz Question

June 10, 2026 8:05 AM UTC

· Though the U.S. and Iran have attacked each other June 10, talks to reopen the straits of hormuz still continue. An Iran/U.S. agreement to reopen the Straits of Hormuz could cure the risk of a demand/supply oil market imbalance and produce some psychological relief that could knock USD

June 08, 2026

DM Government Bonds: Risks of Higher Long End Premia?

June 8, 2026 2:10 PM UTC

· Our baseline is for DM government bond yields ex Japan to remain elevated, but controlled. Japan extra risk premium is driven by BOJ QT at 6% of GDP, more than long-term debt fears. Major catalysts could drive a regime change to higher risk premia and steeper yield curves, but non

June 01, 2026

AI Labs IPO Fever

June 1, 2026 12:58 PM UTC

· Space X could get an initial good reception, but then go flat waiting for the Open AI and Anthropic IPO’s. Space X is an AI enterprise play rather than space and xAI is lagging. This could mean a modest correction in the U.S. equity market at some stage in the summer, but then the

April 17, 2026

Equities: Still a Rocky Road in 2026

April 17, 2026 12:49 PM UTC

· Any deal between the U.S. and Iran would still be seen as a positive win in equities, as it would raise hopes that it could be followed by a multi-year settlement that could include more Iran oil and gas into the global energy markets and lower energy prices. No deal is also feasible,

March 26, 2026

March 24, 2026

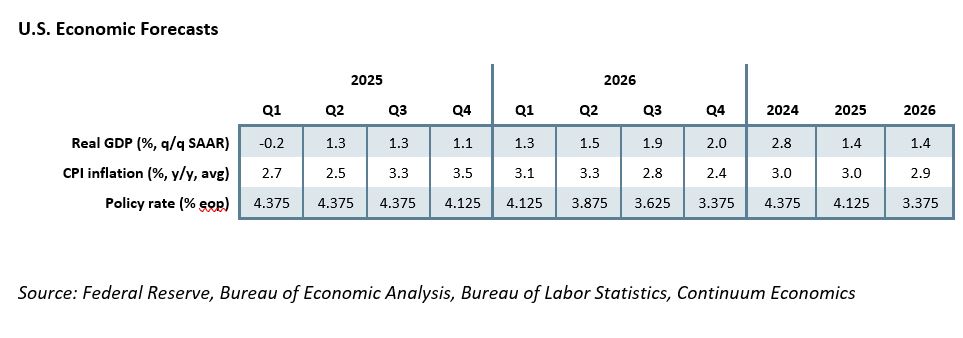

U.S. Outlook: Investment to Lead Growth, Underlying Inflation Set to Slow

March 24, 2026 12:15 PM UTC

• The crisis in the Middle East poses upside risks to headline inflation and downside risks to activity and our baseline assumes a 4-8 week war with a partial reversal of energy prices by end Q2 (here). Our forecasts (below) include a soft patch in H2 2026. Entering 2026 however, the U.S. e

DM Rates Outlook: Mixed Policy Rate and Yield Paths

March 24, 2026 8:46 AM UTC

· The multi quarter outlook for DM rates depends on the length of the Iran war Our baseline is that it will be a 4-8 week war (here) and a 3-4 quarter retracement of oil prices back to pre-war levels – longer from Europe and Asian gas prices. We forecast WTI down to USD80-85 by June

March 23, 2026

Equities Outlook: Navigating Cyclical and Structural Forces

March 23, 2026 4:15 PM UTC

· For global equities, our baseline (here) is for a 4-8 week Iran war, with WTI down to USD80-85 by June; USD65-70 end 2026 by June and USD60 by Q3 2027. A fragile situation will mean it will take until 2027 for energy prices to return to pre-war levels. On a multi-quarter basis thi

January 14, 2026

DM Government Debt: 2026 Supply & Voters’ Resistance To Fiscal Consolidation

January 14, 2026 11:55 AM UTC

· We see the most persistent issue being supply (budget deficit + QT) in 2026, which should lessen into 2027 with a slowdown in ECB/BOE QT and a partial U turn by the BOJ. However, governments are also struggling with electorates that are resistant to higher taxes or lower governmen

January 05, 2026

AI and U.S. Productivity

January 5, 2026 8:04 AM UTC

· Structural labor and overall productivity will be boosted if current AI adoption is sustained at a pace quicker than the adoption of the internet. However, not all areas of the U.S. economy are exposed to AI benefits, as manual work can only be replaced by humanoid robots with maj

January 02, 2026

December 22, 2025

December 17, 2025

DM Rates Outlook: 2026 Yield Curve Steepening Before 2027 Flattening

December 17, 2025 9:21 AM UTC

· Multi quarter, we still look for 50bps of further Fed easing by end 2026, which will likely initially bring 2yr yields down to 3.35%. However, once the Fed Funds rate get closer to 3.0-3.25% and the assumed slowdown turns into a soft landing, the 2yr will likely move to a premium ve

December 12, 2025

U.S. Outlook: Consumers Vulnerable, but Recession Unlikely

December 12, 2025 4:38 PM UTC

• US GDP growth is likely to look solid in Q3 2025 supported by resilient consumer spending, but with slowing employment growth and resilient inflation weighing on real disposable income that will be difficult to sustain. However, while consumers look vulnerable, business investment looks h

Equities Outlook: Choppy Up For 2026 and Down for 2027?

December 12, 2025 8:05 AM UTC

· The U.S. equity market is underpinned by the bullish AI/tech story and a soft economic landing into 2026. However, overvaluation is clear and this leaves the market vulnerable to a 5-10% correction on moderate bad news e.g. economic data. We see the S&P500 having a choppy year a

December 08, 2025

AI and U.S. Equities

December 8, 2025 8:50 AM UTC

· The AI story has driven broad momentum in the U.S. equity market, but will likely become narrower driver in 2026 and 2027, as not all big AI/tech companies will generate clear explosive revenue from areas outside cloud computing and semiconductor chips. Companies that are also depende

November 26, 2025

U.S. Corporate Bonds Into 2026

November 26, 2025 10:15 AM UTC

· Though U.S. corporate bond spreads are tight, absolute yield levels are reasonable due to higher U.S. Treasury yields than most of the post GFC period. The main risk remains of a U.S. recession, though economic data is more consistent with a soft landing and we have reduced the prob

November 24, 2025

Japan Aging: Consumption Lessons for Eurozone/China?

November 24, 2025 10:55 AM UTC

· China will likely suffer slowing consumption from population aging in the coming years, as consumption per head falls for over 55’s and large scale immigration is not a likelihood. China’s household wealth is also heavily concentrated in falling illiquid residential property. Chin

November 17, 2025

Financial Stability Risks: Vulnerable To A Recession

November 17, 2025 1:00 PM UTC

The November Fed financial stability review highlights continued concern over hedge funds and insurance company leverage, while the IMF GSFR is concerned about U.S. equity market overvaluation and growing links between banks and non-bank financial intermediaries. However, the main adverse shock wo

November 06, 2025

U.S. Equities: Smaller Correction But Still Overvalued

November 6, 2025 10:25 AM UTC

· We are revising up our end 2025 S&P500 forecast from 6000 to 6500 for a number of reasons. Private sector data shows the risk of a U.S. hard landing is lower than a couple of months ago, with economic data more consistent with a soft landing. Additionally, the tech/AI optimism has n

November 04, 2025

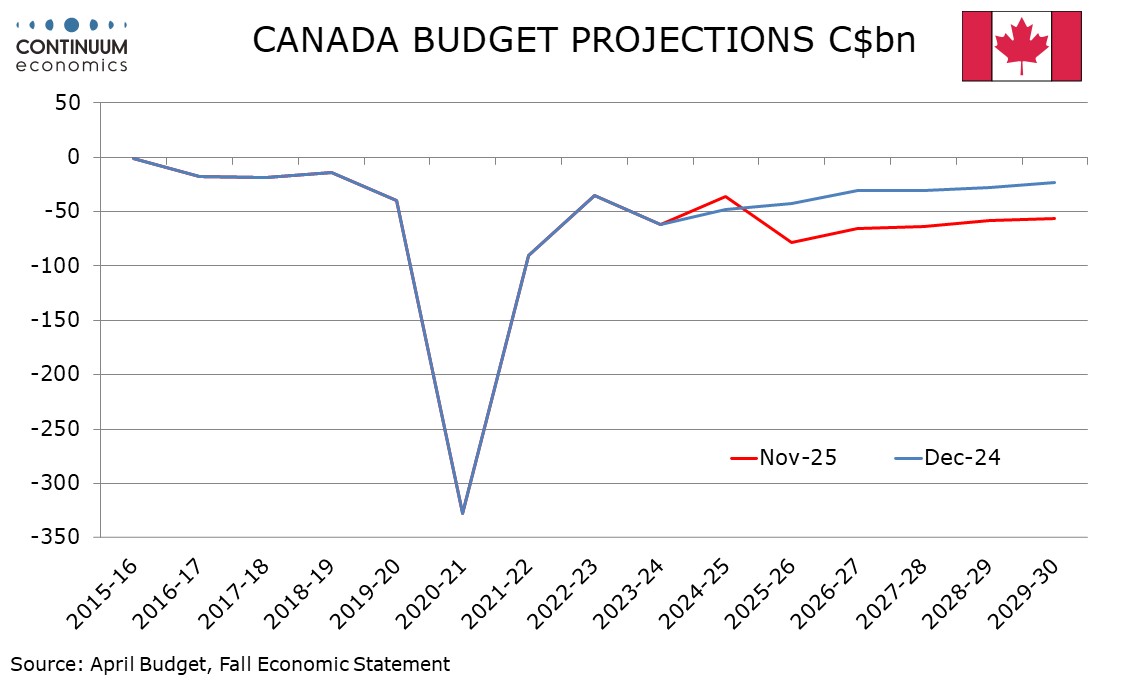

Canada Budget Sees Larger Deficits, Slower Growth

November 4, 2025 9:58 PM UTC

Canada’s budget has seen the deficit for 2025-26 revised up to C$78.3bn from C$42.2bn in the December 2024 statement, which will now be 2.5% of GDP versus 1.3%, still a level that is quite small compared to many other developed countries. The deficit is projected to slip after that, reaching C$56.

October 02, 2025

DM Central Banks: Wider-Ranging Conditions More Than Neutral Rates

October 2, 2025 6:55 AM UTC

· Neutral policy rate estimates and forward guidance provide some help at the start of easing cycles, but less so at mid to mature stages. For the Fed, ECB and BOE we look at a wider array of economic and financial conditions, alongside our own projections over the next 2 years to m

October 01, 2025

AI/Humanoid Robots and Disinflation?

October 1, 2025 9:40 AM UTC

· Overall, a number of forces from the AI wave will impact inflation. Power demand could push up power prices, but productivity enhancements and product innovation could be disinflationary like Information and Communications technology (ICT). One other key uncertainty on a 1-5 year

September 26, 2025

September 25, 2025

September 23, 2025

DM Rates Outlook: Steepening Yield Curve The Old Normal?

September 23, 2025 7:53 AM UTC

• We continue to forecast further yield curve steepening across the U.S./EZ and UK, driven by cumulative easing. For the U.S. this can see a modest further decline in 2yr yields, but the prospect is for a move to a premium of 2yr to Fed Funds (unless a hard landing is seen). 10yr yields

Equities Outlook: Correction Then Up In 2026

September 23, 2025 7:15 AM UTC

• The U.S. equity market’s bullishness reflects good corporate earnings reality, buybacks and the AI story. However, we feel that the U.S. economy can deteriorate still further in the coming months, as the lagged effects of tariffs boost inflation and restrain spending/hurt corporate ea

September 22, 2025

U.S. Outlook: Fed Easing to Prevent Recession, but May Also Keep Inflation Above Target

September 22, 2025 10:15 AM UTC

• GDP growth, supported in particular by business investment, was resilient in Q2, but growth in employment is now minimal and that will weigh on consumer spending, particularly with tariff-supported inflation set to restrain real wage growth. Recession is a risk if we see a vicious circle

September 16, 2025

Succession and Strongmen Leaders

September 16, 2025 10:53 AM UTC

In the unexpected scenario of an early death, Putin and Xi have no clear successors, and any new Russia or China leader would have to spend time building domestic strength and compromising on external goals. Erdogan also has no clear successors, which could create political uncertainty. For Trump su

September 01, 2025

Aging: Slow Growth for Some in 2020’s

September 1, 2025 8:35 AM UTC

Population aging always seems to be beyond the market horizon, but the 2020’s are already seeing population aging in some countries. What is the economic impact? Aging is already causing a peak in labor force in China and the EU. Meanwhile, the population pyramid also means less consumptio

August 04, 2025

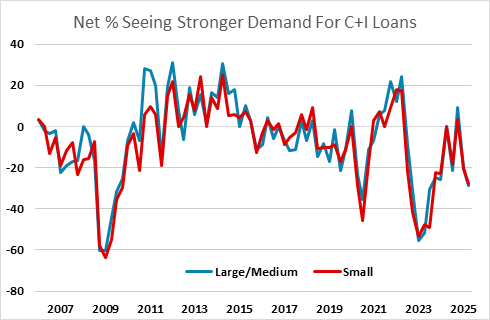

Fed Senior Loan Officer Opinion Survey Suggests Weaker Demand For Business Investment

August 4, 2025 6:44 PM UTC

The Fed’s July Senior Loan Officer Opinion Survey of bank lending practices suggests uncertainty is restraining investment demand, with supply signals on balance fairly neutral but demand signals weaker.

July 30, 2025

DM Household Sluggish Borrowing

July 30, 2025 10:45 AM UTC

· Overall, restrained credit supply from banks; abundant employment/income or wealth for most households but restrained financial conditions for low income households could have restrained household lending growth to GDP. However, the surge in government debt and ensuing fear of fut

July 03, 2025

U.S. Assets and Valuation

July 3, 2025 9:30 AM UTC

The U.S. equity market has returned to be clearly overvalued on equity and equity-bond valuations measures and is vulnerable to a new correction in H2 on any moderate bad news (e.g. further economic slowing and corporate earnings downgrades). In contrast, U.S. Treasuries are at broadly fai

July 02, 2025

DM Central Banks: Overlooking Lagged 2021-23 Tightening and QT?

July 2, 2025 8:30 AM UTC

We are concerned that DM central banks are underestimating the lagged impact of 2021-23 tightening and ongoing QT, which impacts the transmission mechanism of monetary policy. Central banks need to consider cyclical and structural issues, but also need a more rounded view of the stance and implica

June 24, 2025

Equities Outlook: Choppy Then 2026 Gains

June 24, 2025 8:15 AM UTC

Though the U.S. equity market has rebounded, we still scope for a fresh dip H2 2025 to 5500 on the S&P500 as hard data softens further to feed into weaker corporate earnings forecasts and CPI picks up and delays Fed easing. However, the AI story is still a positive, while share buybacks

June 23, 2025

DM Rates Outlook: Yield Curve Steepening?

June 23, 2025 8:30 AM UTC

• We see the U.S. yield curve steepening in the next 6-18 months. 2yr U.S. Treasury yields can step down with cautious Fed easing on a modest/moderate growth slowdown and also if the Fed keeps an easing bias in H2 2026. 10yr U.S. Treasury yields face a tug of war between lower short-dated y

June 20, 2025

U.S. Outlook: Slowdown but not Recession, Cautious Fed Easing

June 20, 2025 2:14 PM UTC

• Policy uncertainty remains high and final details of the tariffs will depend on the decisions of the courts as well as those of President Trump. However the magnitude of the tariffs is becoming easier to predict than the detail. Trump looks set to insist on a minimum average tariff of at

April 11, 2025

Volatile Treasuries But Economic and Foreign Holdings Key

April 11, 2025 9:30 AM UTC

Long-dated U.S. Treasury yields were being pushed up by deleveraging among leveraged players, before the 90 days pause on reciprocal tariffs easing deleveraging. Multi quarter the key question for yields is whether real sector data sees a soft or hard landing. We see a slowdown to sub trend growth

March 26, 2025

Equities Outlook: Turbulence Ahead

March 26, 2025 9:05 AM UTC

· U.S. trade wars will likely hurt U.S. growth and raise inflation, with only small to modest Fed easing and a 10yr budget bill that will likely be neutral to negative for the economy. With valuations still very high (Figure 1), we see scope for a correction to extend into mid-year th