U.S. Outlook: Investment to Lead Growth, Underlying Inflation Set to Slow

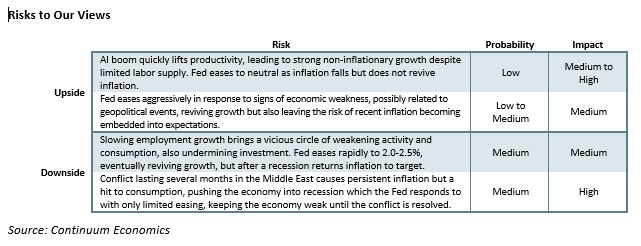

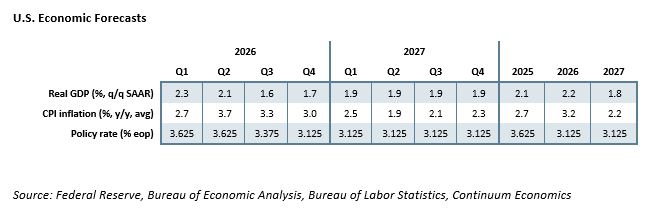

• The crisis in the Middle East poses upside risks to headline inflation and downside risks to activity and our baseline assumes a 4-8 week war with a partial reversal of energy prices by end Q2 (here). Our forecasts (below) include a soft patch in H2 2026. Entering 2026 however, the U.S. economy maintained significant momentum, led by strength in business investment, but with consumers looking vulnerable with spending outperforming growth in real disposable income. 2026 is likely to see some loss of momentum from consumer spending, but the economy continuing to expand, with the pace slowing below 2.0% on an annualized basis in the second half of the year. While President Trump will continue to try and impose tariffs, the Supreme Court decision is likely to mean that we are past the peak tariff impact and this is likely to cause underlying inflation excluding energy to slow in the second half of the year. This will give consumers some support. In 2027 we expect GDP to increase by close to potential around 1.9% while core PCE price inflation stabilizes marginally above the Fed’s 2.0% target. November’s midterm elections will be a key event, with Democrats looking likely to regain control of the House and the Senate now a close call.

• Incoming FOMC Chairman Kevin Warsh will struggle to impose a significantly more dovish stance on the FOMC, which may delay easing until Q3 of 2026 with energy prices adding to the difficulties of returning inflation to the 2.0% target. We expect two 25bps easings in 2026, in Q3 and Q4, which would take the Fed Funds target to 3.0-3.25% which is in line with where we see neutral. We expect the rate to remain there through 2027. This may be marginally more dovish than is appropriate in a less globalized world and stimulative U.S. fiscal policy. Warsh is also keen to reduce the size of the balance sheet but his ability to do so significantly may prove limited (here).

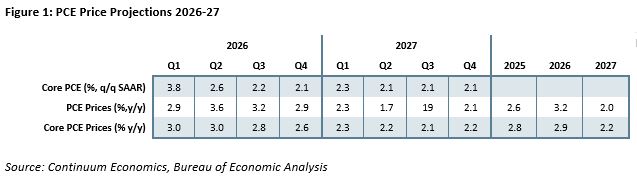

Forecast changes: We now see 2026 GDP at 2.2% rather than the 1.5% we saw in December but this is in part due to 2026 starting at a higher level due to stronger than expected GDP growth in the second half of 2025. Our 2027 view remains at 1.8%. On a Q4/Q4 basis we expect growth of 1.9% in both 2026 and 2027. We have revised our 2025 CPI view higher in 2026 to 3.2% from 2.8% but with 2027 revised down to 2.2% from 2.5% (as energy prices reverse from H2 2026). Our core PCE price forecast has been lifted to 2.9% from 2.7% for 2026 but with 2027 unrevised at 2.2%. We continue to expect the FOMC to deliver two 25bps easings in 2026, to a 3.0-3.25% target range, but now expect the moves to come in Q3 and Q4 rather than Q2 and Q3. We continue to expect policy to be kept steady through 2027.

U.S. Consumers Vulnerable, but Investment Strong

U.S. GDP surprised to the upside in the second half of 2025, largely in Q3, meaning that 2025 GDP increased by 2.1% rather than our December forecast of 1.8%, which was made with Q3 data still unavailable due to the to the impact of the government shutdown. While Q4 at 0.7% annualized was significantly slower than a 4.4% increase in Q3, slippage from the Federal Government, hit by the temporary effects of the shutdown, took 1.2% off the increase, suggesting that the economy maintained respectable underlying momentum entering 2026.

There are a number of special factors that complicate forecasts for early 2026. The ending of the government shutdown will be supportive for Q1 GDP, though this will be in part offset by bad weather in late January and much of February. Any negative from bad weather in Q1 is likely to be made up in Q2. Both Q1 and Q2 will see support from fiscal policy, with tax measures in the One Big Beautiful Bill passed in July 2025 likely to add around 0.3% to GDP in 2026, which will be felt most in the first half of the year. However, the lift to consumers from lower taxes could be more than fully offset, at least in the short term, by higher energy prices due to the conflict in the Middle East.

In December we saw US consumers as vulnerable to a slowing, but the outlook outside of consumer spending as more positive. That remains the case. Consumer spending increased by 3.5% annualized in Q3 of 2025 and 2.0% in Q4, but real disposable income rose by only 1.0% in Q3 and 0.2% in Q4, reflecting weak employment growth, and resilient inflation restraining real wage growth. Consumer spending looks set to lose momentum in 2026. The outlook for investment however, fueled in particular by AI, is looking increasingly positive. Trend in durable goods orders has picked up and the ISM manufacturing index has moved clearly above neutral in early 2026. The Fed’s Senior Loan Officer Opinion Survey shows demand for commercial and industrial loans picked up in the second half of 2025. Inventories, having corrected a pre-tariff surge in Q1 of 2025, are now quite lean. The impact of the other components of GDP is likely to be modest. Government will remain subdued, but the steep DOGE-fueled cuts seen in early 2025 will not be repeated and increased defense spending will be a positive for GDP. Housing, which declined in 2025, has shown signs of stabilization but has limited upside.

Underlying inflation to slow with tariffs having peaked

Net exports saw massive swings in the quarterly GDP data of 2025 but the trade deficit for 2025 as a whole was almost unchanged from that of 2024. Going forward we expect net exports to return to a long-term trend of being a modest negative in GDP. Strong US investment will fuel imports. The tariff situation remains highly uncertain with Trump determined to fight the Supreme Court ruling against his reciprocal tariffs in any way he can, and he has several options. However, his right to impose across the board 15% tariffs lasts for only 150 days before he will require the approval of Congress, which is unlikely to be forthcoming. This leaves the more complicated section 301 for negotiating leverage and to get existing trade framework deals codified. Tariffs will remain significant, but will be off the 2025 highs, and that will help underlying inflation excluding energy to fall in the second half of 2026, by when we assume energy prices will also be coming off their highs induced by the conflict in the Middle East.

We expect GDP to increase by an in line with potential 1.9% Q4/Q4 in both 2026 and 2027, a marginal slowing from 2.0% in 2025 Q4/Q4. However, given the strong second half of 2025, we now expect 2026 to average 2.2% y/y, up from 2.1% in 2025, before a slowing to 1.8% in 2027. We expect annualized gains slightly above 2.0% in the first half of 2026, with the second half falling below the 1.9% pace where we expect growth to stabilize through 2027. There are downside risks should conflict in the Middle East prove protracted.

We now expect inflation to average slightly more in 2026 than 2025 as a whole, with CPI at 3.2% and core PCE prices at 2.9% compared to 2.7% and 2.8% respectively in 2025, before 2027 sees both CPI and core PCE prices slowing to 2.2%. Annualized core PCE prices are likely to remain significantly above target in the first half of 2026 before slowing to only slightly above the 2.0% target in H2 2026, and that is where we expect the pace to remain through 2027. A less globalized world, the likelihood of Fed policy slightly more dovish than appropriate, and a continued expansionary fiscal policy suggest that the Fed will fail to quite reach its target, even as the impact of tariffs and the current energy shock fade.

Fed Policy and Political Risk

The term of current Fed Chair Jerome Powell ends in May but with a key Republican Senator threatening to delay approval of his nominated successor Kevin Warsh while legal action against Powell persists it is uncertain when Warsh will assume the position, though his eventual approval is not in serious doubt. Warsh will be eager to move the Fed in a dovish direction, on a view that AI-fueled investment will boost productivity and lower inflation, but many at the Fed have doubts over this view (here). Some feel that strong investment will increase the neutral rate, and there is tentative evidence in GDP price indices and the PPI that inflation for investment goods is accelerating ahead of consumer prices. The economy is entering 2026 with economic growth maintaining some momentum and inflation remaining above target. If activity data shows weakness, it will be difficult to distinguish the impact of short term and underlying factors, while gains in energy prices add to the risk of current inflation becoming embedded into expectations. We continue to expect the Fed to ease by 50bps in 2026 with core inflation likely to fall and labor market data to remain subdued, but we now expect the moves to come in Q3 and Q4, rather than Q2 and Q3. Our call is now for moves in September and December, though timing will be dependent on incoming data which will be sensitive to geopolitical events. A protracted war in the Middle East would be likely to delay easing further.

We expect policy to be held steady through 2027 with growth seen near potential and inflation seen near target, though marginally above, through that year. We believe the neutral rate is marginally above 3.0% but there is a wide range of views on this at the Fed. Warsh is also keen to reduce the size of the balance sheet, but other on the FOMC have different views. Previous attempts to reduce the balance sheet below current levels have created strains in the money market and that is something to watch for.

The key political event, assuming an end to the Middle East war, will be the November midterm elections. It looks highly likely that the Democrats will achieve the small net gain required to take control of the House. The Senate will be harder for them to win, needing a net gain of four seats and only two of the contested seats (Maine and North Carolina) being in states currently recognized as swing. However, should Trump become increasingly unpopular, a Democratic Senate, which would dramatically curb Trump’s power, is a real possibility. There are close races in Alaska and Ohio, with Texas also looking in play. Should Democrats gain five seats their majority would not be dependent on Pennsylvania’s John Fetterman, a Democrat who often sides with Republicans. This raises the risk of attempts by Trump to manipulate the elections, though it may be difficult for him to do so with elections still largely conducted by the states. However the elections go, they are likely to be accompanied by heated debate and probably significant legal challenges, bringing uncertainty that markets will not welcome. While uncertainty is troubling for markets, its impact on the current impressive strength of business investment is however likely to be modest.