Macro Strategy

View:

July 02, 2026

U.S. June Employment - Upside May surprise offset, but unemployment falls on lower labor force

July 2, 2026 1:20 PM UTC

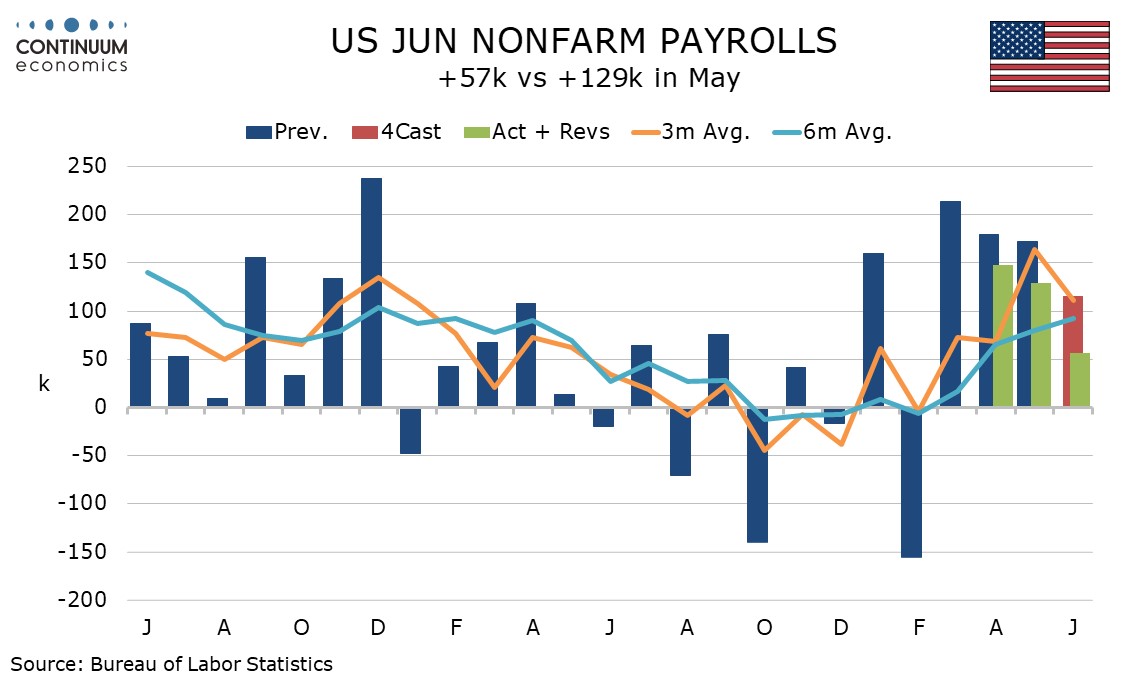

June’s non-farm payroll is weaker than expected with a 57k increase, 49k private, with downward revisions to April and May. The slowing is consistent with an upturn in the initial and continued claims trends, though both were almost unchanged (-1k to 215k and +2k to 1.814m respectively) in the l

U.S. June Employment - Upside May surprise offset, but unemployment falls on lower labor force

July 2, 2026 1:12 PM UTC

June’s non-farm payroll is weaker than expected with a 57k increase, 49k private, with downward revisions to April and May. The slowing is consistent with an upturn in the initial and continued claims trends, though both were almost unchanged (-1k to 215k and +2k to 1.814m respectively) in the l

July 01, 2026

Preview: Due July 14 - U.S. June CPI - Energy to correct lower, World Cup to support core

July 1, 2026 3:18 PM UTC

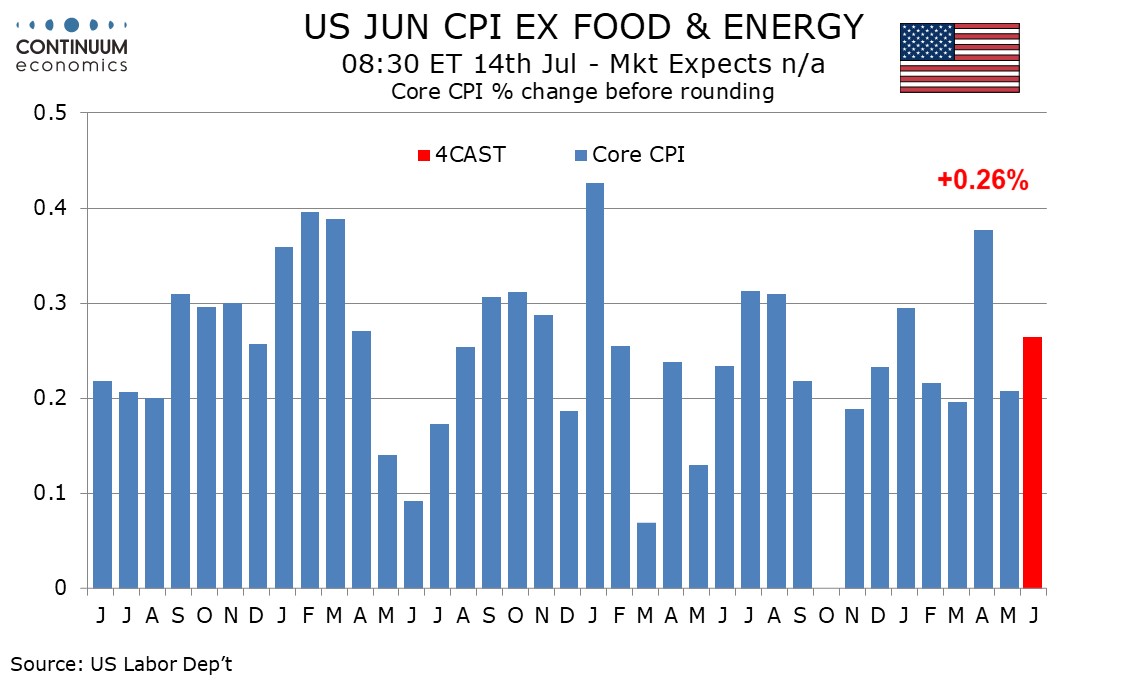

We expect June CPI to be unchanged overall as energy corrects from three straight strong gains while the core rate ex food and energy sees a slightly firmer 0.3% increase. Before rounding we expect respective outcomes of -0.02% and up 0.26%, with the World Cup having just enough impact to nudge the

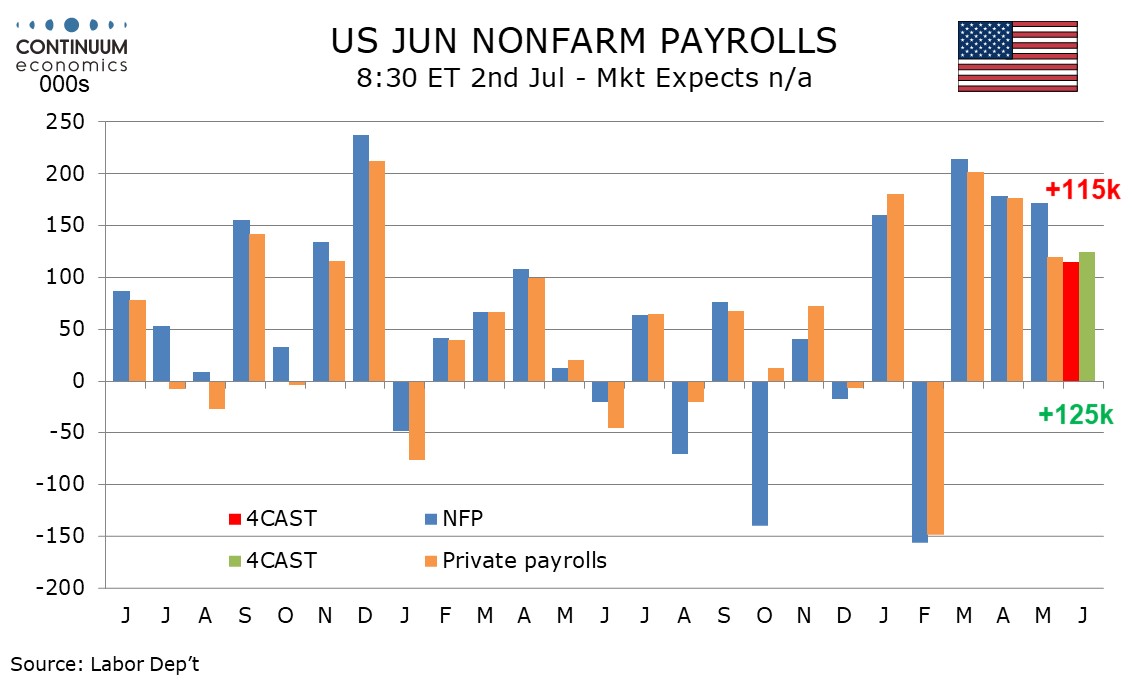

Preview: Due July 2 - U.S. June Employment (Non-Farm Payrolls) - World Cup boost versus underlying slowing

July 1, 2026 12:47 PM UTC

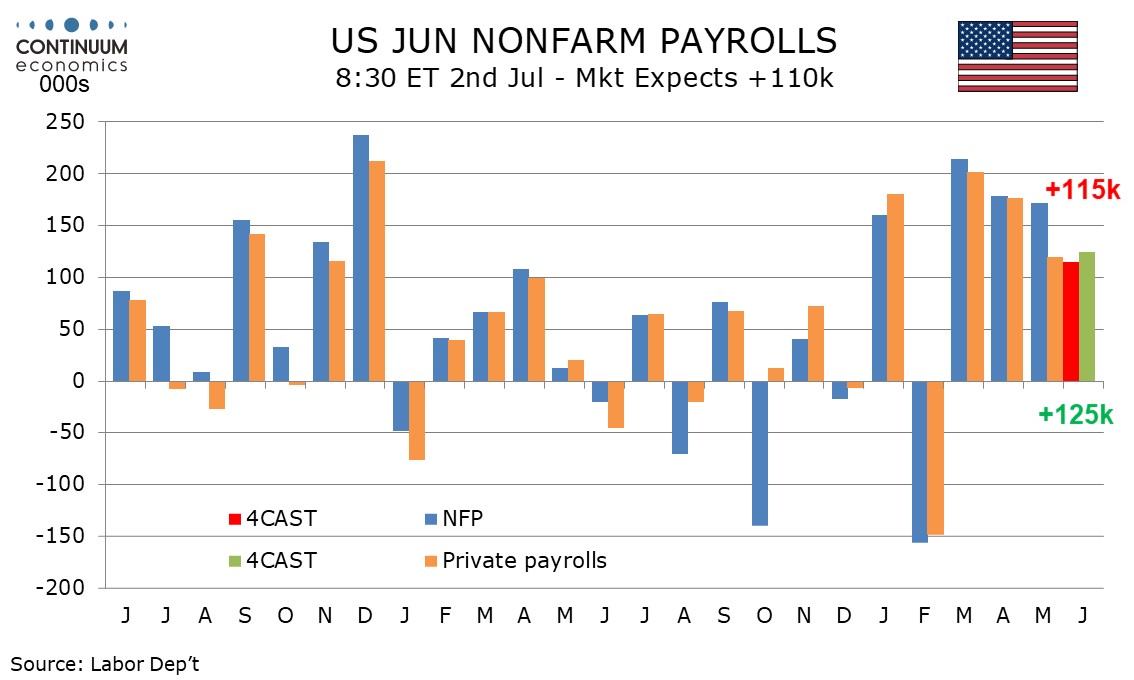

We expect June’s non-farm payroll to rise by 115k overall and by 125k in the private sector, the former a slowing from 172k in May but the latter marginally stronger than May’s 120k increase. We expect the unemployment rate to remain at 4.3% for a fourth straight month and an in line with trend

Macro and Market Implications of 'Super' El Nino Risks

July 1, 2026 8:08 AM UTC

El Nino, and a potentially severe one, is increasingly looking like a central scenario rather than a tail risk for 2026-27.

2026-27 El Nino is shaping up to be strong enough to matter, at least for scenario planning.

The key facts are broadly: Australia, New Zealand, Indonesia and South Africa are l

June 30, 2026

AI Boom and Bust?

June 30, 2026 10:45 AM UTC

• While some are becoming wary that AI bust could arrive in coming quarters, AI labs revenue growth has been explosive and this sustains the vertical chain of datacenter demand and commitments for the hyperscalers and also buoyant semiconductor demand. For 2027 and 2028 capital markets re

June 26, 2026

June 25, 2026

Preview: Due July 2 - U.S. June Employment (Non-Farm Payrolls) - World Cup boost versus underlying slowing

June 25, 2026 7:12 AM UTC

We expect June’s non-farm payroll to rise by 115k overall and by 125k in the private sector, the former a slowing from 172k in May but the latter marginally stronger than May’s 120k increase. We expect the unemployment rate to remain at 4.3% for a fourth straight month and an in line with trend

June 24, 2026

Outlook Overview: Cyclical and Structural Forces

June 24, 2026 7:00 AM UTC

· The difference between 2nd round inflation effects from higher energy prices and 1st round effects that central banks can look through swings on whether the Straits of Hormuz will remain open in the coming months after the U.S./Iran interim agreement (here). Despite some tensions, we

June 23, 2026

Preview: Due July 2 - U.S. June Employment (Non-Farm Payrolls) - World Cup boost versus underlying slowing

June 23, 2026 6:31 PM UTC

We expect June’s non-farm payroll to rise by 115k overall and by 125k in the private sector, the former a slowing from 172k in May but the latter marginally stronger than May’s 120k increase. We expect the unemployment rate to remain at 4.3% for a fourth straight month and an in line with trend

Commodities Outlook: The War and Its Reversal

June 23, 2026 10:05 AM UTC

The US-Iran memorandum marks a turn, but a fragile one. We attach 80% probability to the Strait of Hormuz reopening over June/July and staying open through 2027, and 20% to a second-half reclosure if Israel-Hezbollah tensions draw Iran back in (here). Most of the war premium has already unwound, and

DM Rates Outlook: Tightening or Easing?

June 23, 2026 8:15 AM UTC

· With the U.S./Iran interim agreement likely to hold and energy prices softening, our projected consumer slowdown will likely tilt the Fed not to hike in H2 2026 and to actually ease by 50bps in 2027, with 25bps moves in both Q2 and Q3. With 2yr yields consistent with a hike, the tra

DM and EM FX Outlook: Cross-Currents for H2 and 2027

June 23, 2026 8:00 AM UTC

· Our baseline for the coming quarters is that global FX is moving through a period of dollar bounce and cross-current positioning adjustment, rather than a clean return to the dollar downtrend. The near-term driver is the market's (over) hawkish reading of the June FOMC/Summary of Econ

June 22, 2026

U.S. Outlook: Consumers Looking Vulnerable

June 22, 2026 2:17 PM UTC

• The US economy is showing resilience with strength in investment offsetting a gradual slowing in consumption, though consumer spending, which is running well ahead of real disposable income, looks set to slow further. This is likely to see the economy slow in the second half of 2026 even

Equities Outlook: AI Optimism, But Caution Elsewhere in DM economies

June 22, 2026 7:05 AM UTC

· In terms of the S&P500, we remain less concerned about high valuations in the tech sector provided AI labs growth remains fast. 12mth fwd information technology are mid-range in the 2020-26 experience rather than at the highs. Even so, heavy equity issuance by tech companies and a s

June 15, 2026

U.S./Iran Interim Deal and Reopening Strait of Hormuz

June 15, 2026 12:32 PM UTC

· Our baseline (80%) is that the Strait of Hormuz will reopen in H2 2026 and remains open through 2027. However, logistics dislocation plus a switch from commercial inventory rundown to rebuilding will likely slow the decline in oil prices back towards normal levels (Figure 1). O

June 12, 2026

Fed Tightening and U.S. Treasury Yields: 1994, 1999 and 2022 Redux

June 12, 2026 7:05 AM UTC

Our baseline involves no Fed hike, but 50-75bps is feasible in a plausible adverse scenario. In this alternative scenario of 50-75bps of Fed tightening it is easy to build the case for 2yr yields going to 4.30-4.40% area, before thoughts turn to H2 2027/28 involving modest Fed rate cuts. 10yr

June 10, 2026

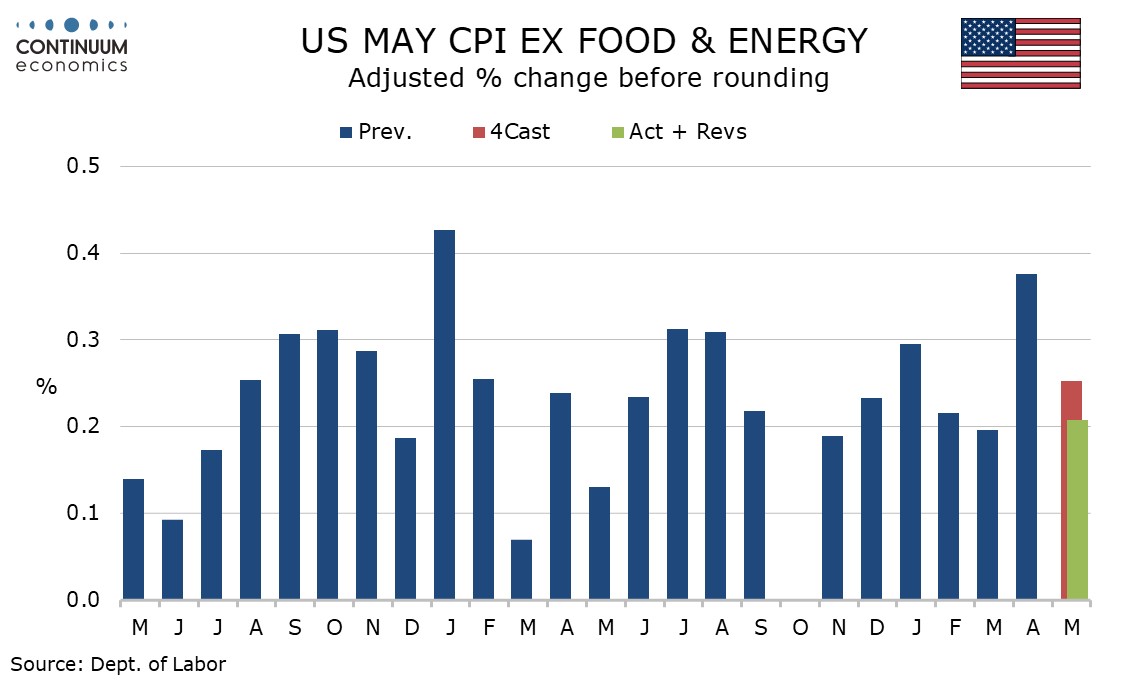

U.S. May CPI - Surprising fall in transport services despite continued gains in air fares

June 10, 2026 1:08 PM UTC

May CPI is in line with expectations at 0.5% overall but the core rate ex food and energy was softer than expected at 0.2%, with the rise before rousing being 0.208%. The most surprising restraint on the data was a 0.6% fall in transportation services, despite continued gains in air fares.

Financial Markets/Policymakers and the Strait of Hormuz Question

June 10, 2026 8:05 AM UTC

· Though the U.S. and Iran have attacked each other June 10, talks to reopen the straits of hormuz still continue. An Iran/U.S. agreement to reopen the Straits of Hormuz could cure the risk of a demand/supply oil market imbalance and produce some psychological relief that could knock USD

June 09, 2026

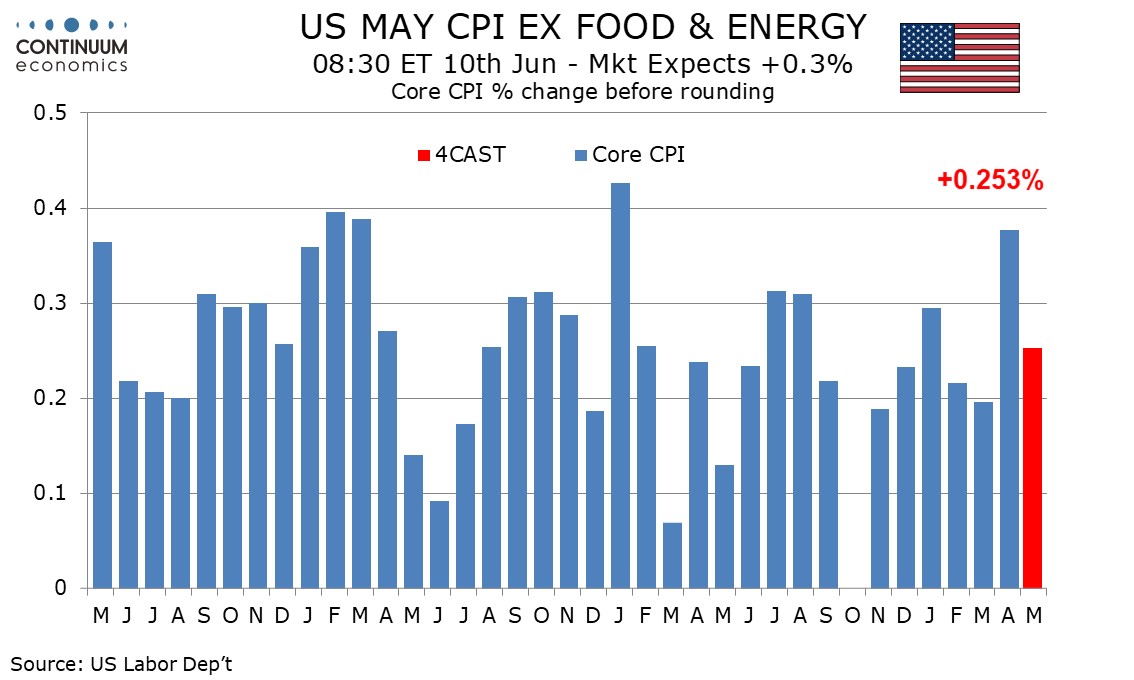

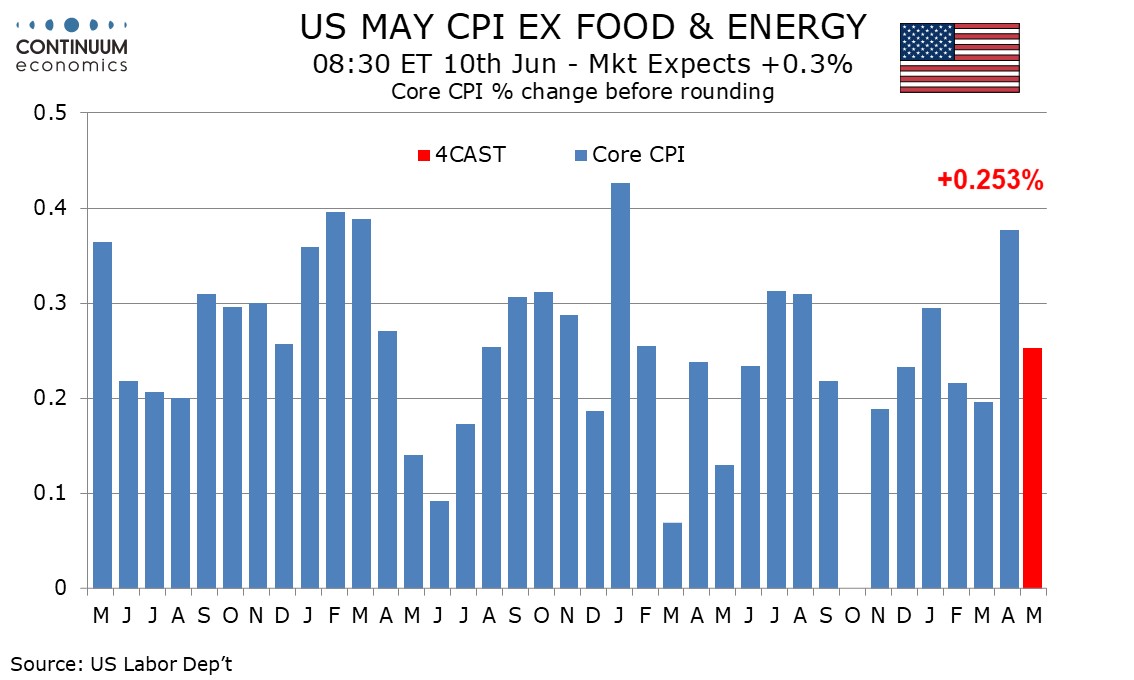

Preview: Due June 10 - U.S. May CPI - Energy and air fares to lead

June 9, 2026 1:39 PM UTC

We expect May CPI to increase by 0.5% overall and 0.3% ex food and energy, with respective gains before rounding being 0.527% and 0.253%, meaning that the core rate is a close call between 0.2% and 0.3% before rounding. The extent of the energy feed through to air fares may be the swing factor in th

June 08, 2026

DM Government Bonds: Risks of Higher Long End Premia?

June 8, 2026 2:10 PM UTC

· Our baseline is for DM government bond yields ex Japan to remain elevated, but controlled. Japan extra risk premium is driven by BOJ QT at 6% of GDP, more than long-term debt fears. Major catalysts could drive a regime change to higher risk premia and steeper yield curves, but non

June 05, 2026

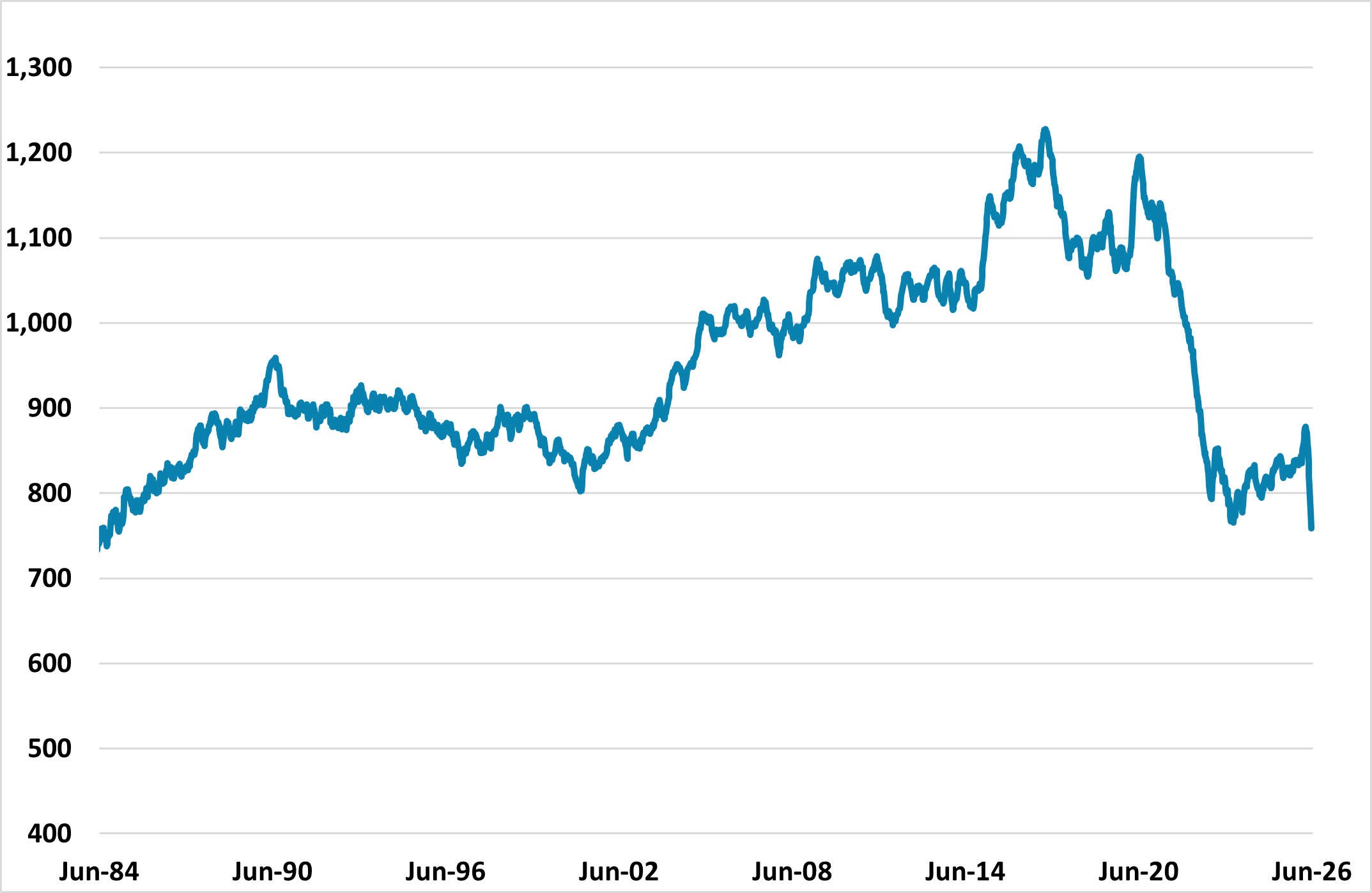

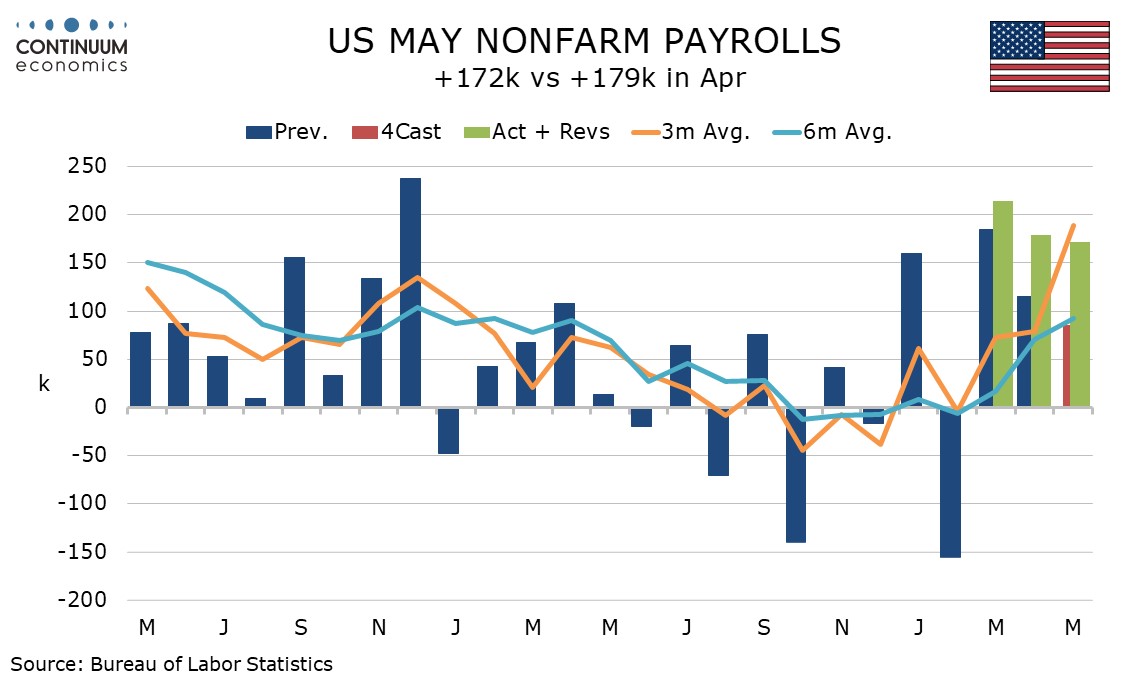

U.S. May Employment - Surprise came from local government and leisure and hospitality

June 5, 2026 1:19 PM UTC

May’s non-farm payroll is significantly stronger than expected with a rise of 172k though the private sector was less impressive at 120k, if still healthy. Upward revisions to March and April add to the positive message. In addition to government, leisure and hospitality with a 70k increase was

June 04, 2026

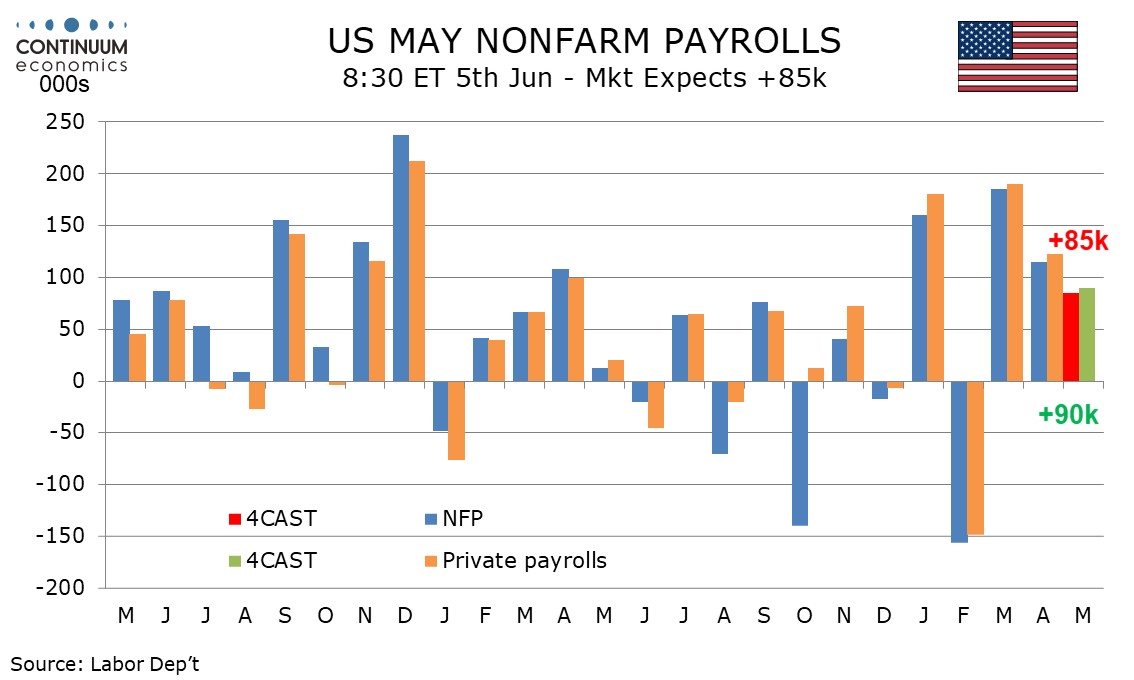

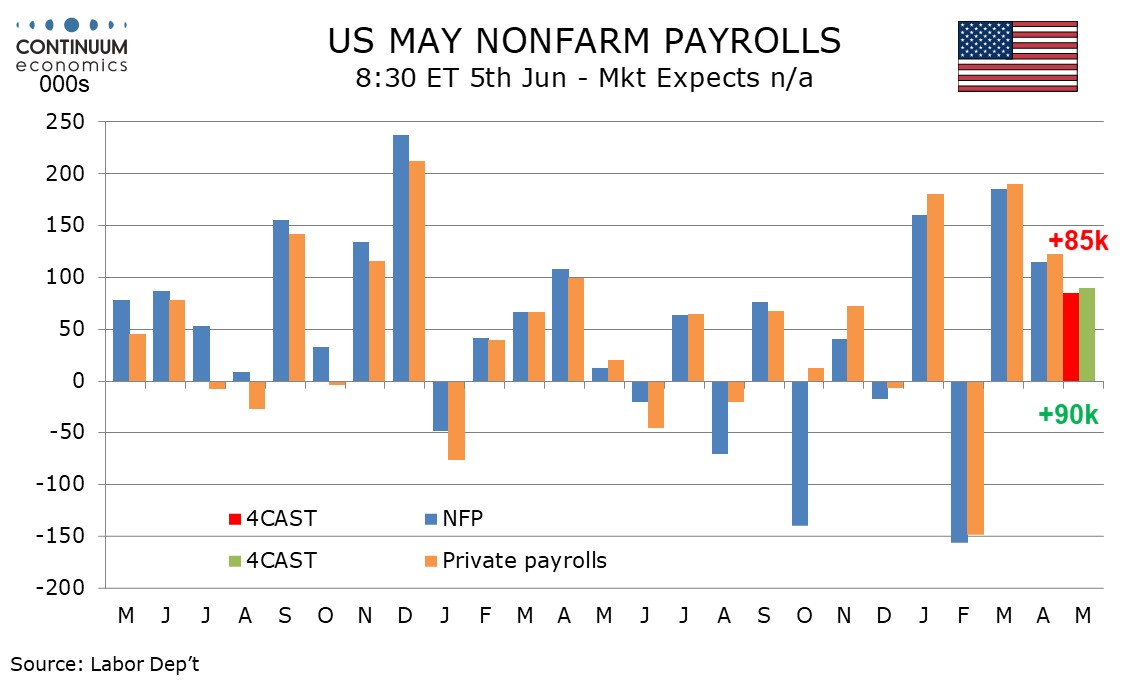

Preview: Due June 5 - U.S. May Employment (Non-Farm Payrolls) - Slightly slower but still healthy

June 4, 2026 1:26 PM UTC

We expect May’s non-farm payroll to rise by 85k overall and by 90k in the private sector, less strong than in March and April but still showing a healthy labor market given a lack of growth in the labor force, leaving unemployment at 4.3% for a third straight month. We expect a 0.3% rise in in ave

June 02, 2026

Preview: Due June 10 - U.S. May CPI - Energy and air fares to lead

June 2, 2026 3:20 PM UTC

We expect May CPI to increase by 0.5% overall and 0.3% ex food and energy, with respective gains before rounding being 0.527% and 0.253%, meaning that the core rate is a close call between 0.2% and 0.3% before rounding. The extent of the energy feed through to air fares may be the swing factor in th

June 01, 2026

AI Labs IPO Fever

June 1, 2026 12:58 PM UTC

· Space X could get an initial good reception, but then go flat waiting for the Open AI and Anthropic IPO’s. Space X is an AI enterprise play rather than space and xAI is lagging. This could mean a modest correction in the U.S. equity market at some stage in the summer, but then the

May 26, 2026

Preview: Due June 5 - U.S. May Employment (Non-Farm Payrolls) - Slightly slower but still healthy

May 26, 2026 4:13 PM UTC

We expect May’s non-farm payroll to rise by 85k overall and by 90k in the private sector, less strong than in March and April but still showing a healthy labor market given a lack of growth in the labor force, leaving unemployment at 4.3% for a third straight month. We expect a 0.3% rise in in ave

May 12, 2026

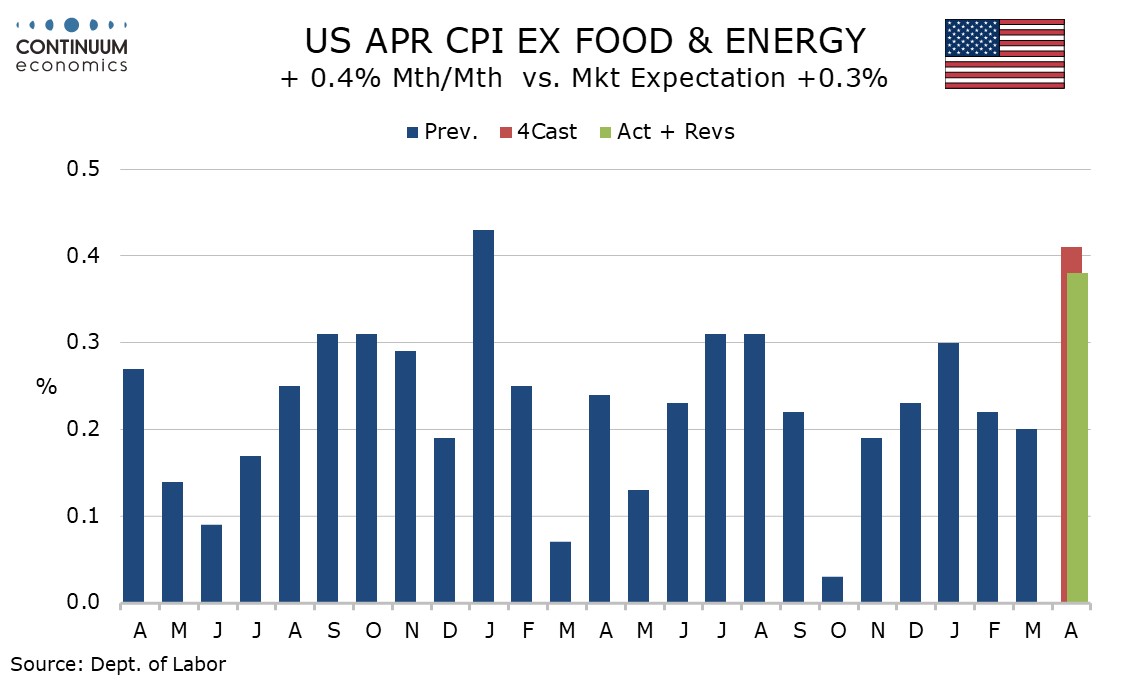

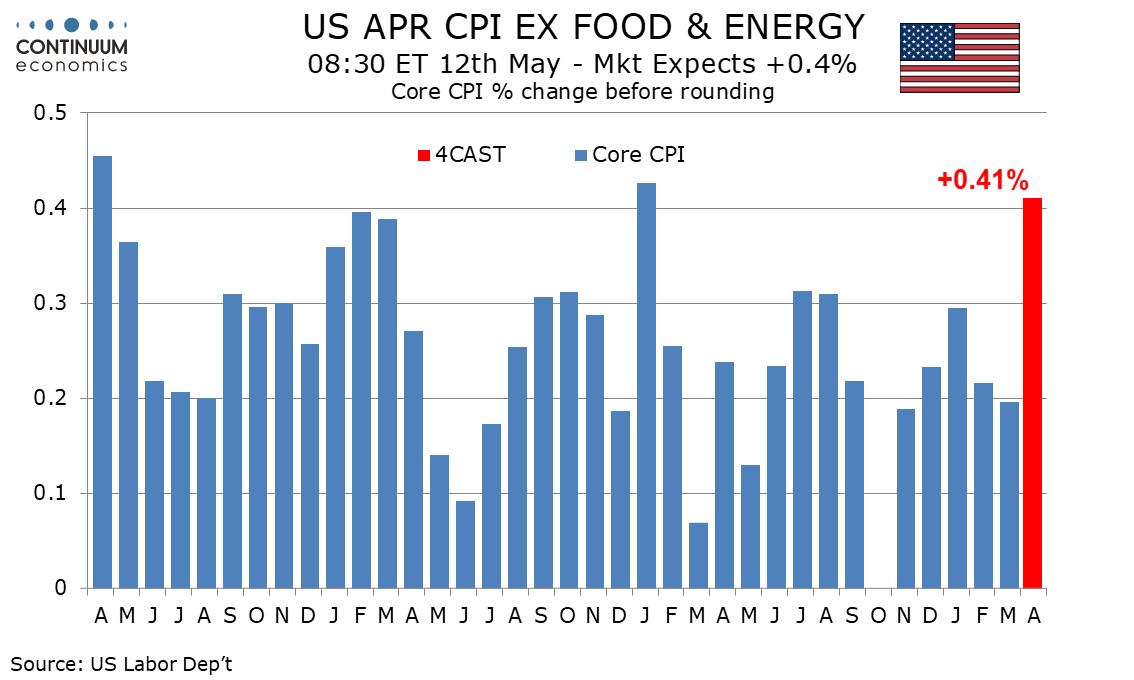

U.S. April CPI - Subdued ex food, energy and what looks like one-time strength in shelter

May 12, 2026 1:08 PM UTC

April CPI is only marginally stronger than expected on the core rate, up by 0.4%, 0.376% before rounding, and the data not alarming outside of a one-time distortion in housing. The headline gain of 0.6% was as expected, and here the rise was a little firmer at 0.64% before rounding.

May 11, 2026

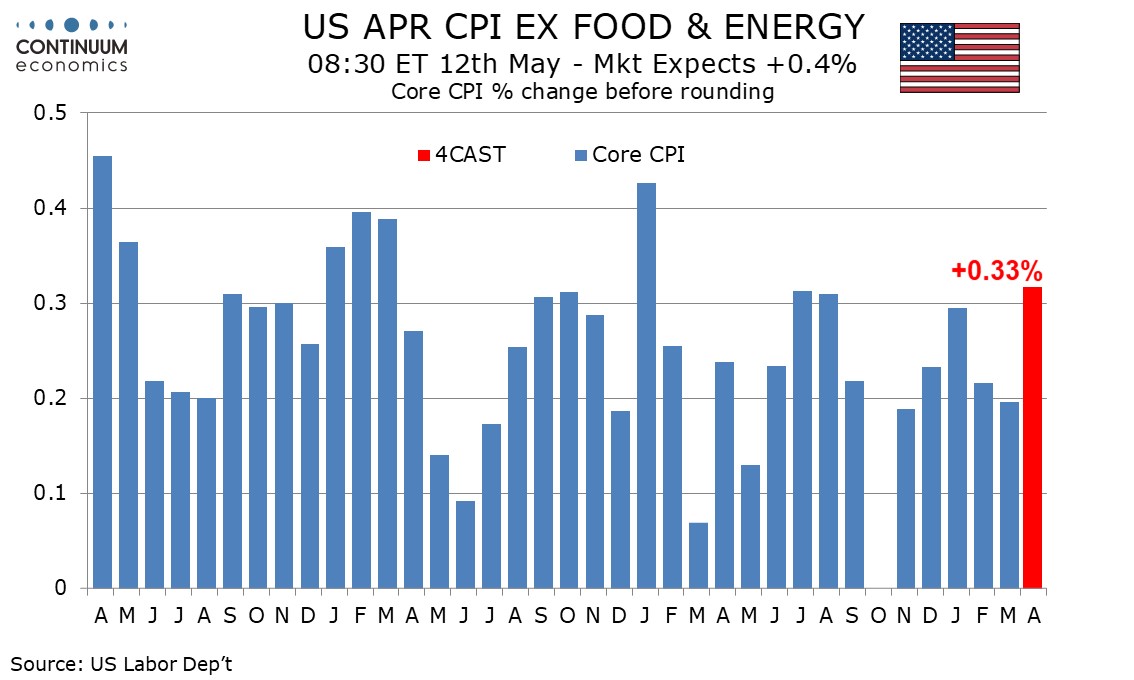

Preview: Due May 12 - U.S. April CPI - Energy, air fares and a housing distortion

May 11, 2026 12:28 PM UTC

We now expect April CPI to increase by 0.6% overall and 0.4% ex food and energy, with respective gains before rounding being 0.57% and 0.41%. Energy is likely to add close to 0.2% to the overall gain and feed through from energy is likely to add around 0.1% to the core, largely in air fares. There i

May 08, 2026

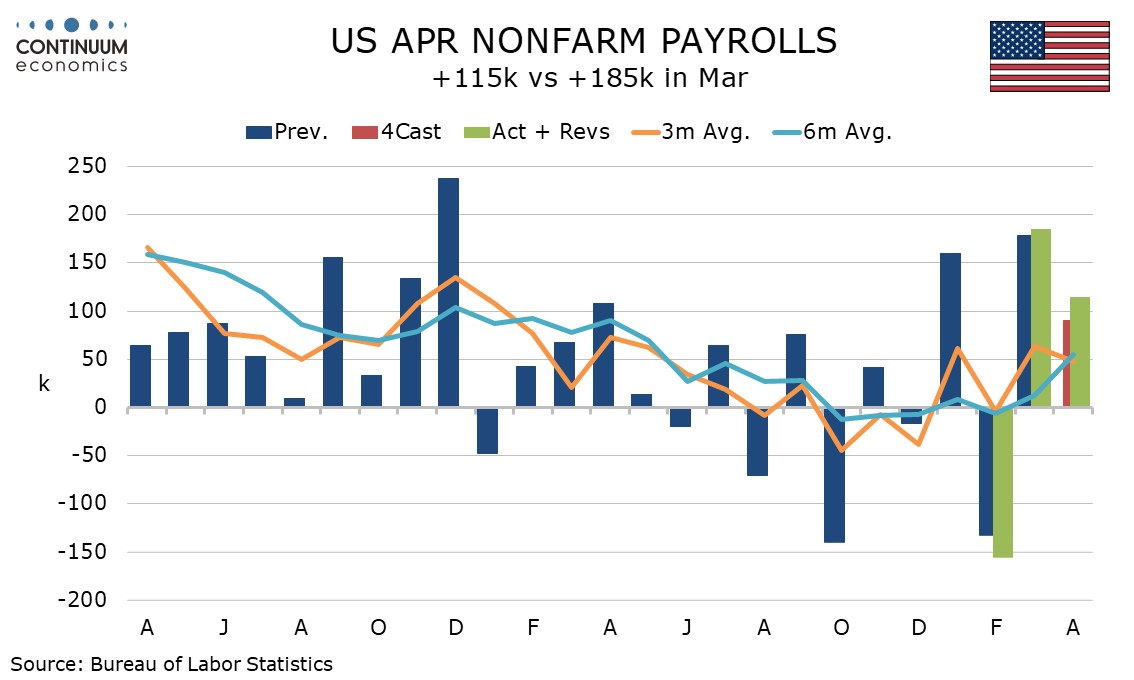

U.S. April Employment - Resilience should keep easing off the near term agenda

May 8, 2026 1:04 PM UTC

April’s non-farm payroll suggests the US economy continues to grow at a respectable pace in early Q2 with no signs of a hit from the oil shock yet. Payrolls increased by a stronger than expected 115k, with unemployment stable at 4.3% and the workweek stronger at 34.3 hours from 34.2. Average hourl

May 07, 2026

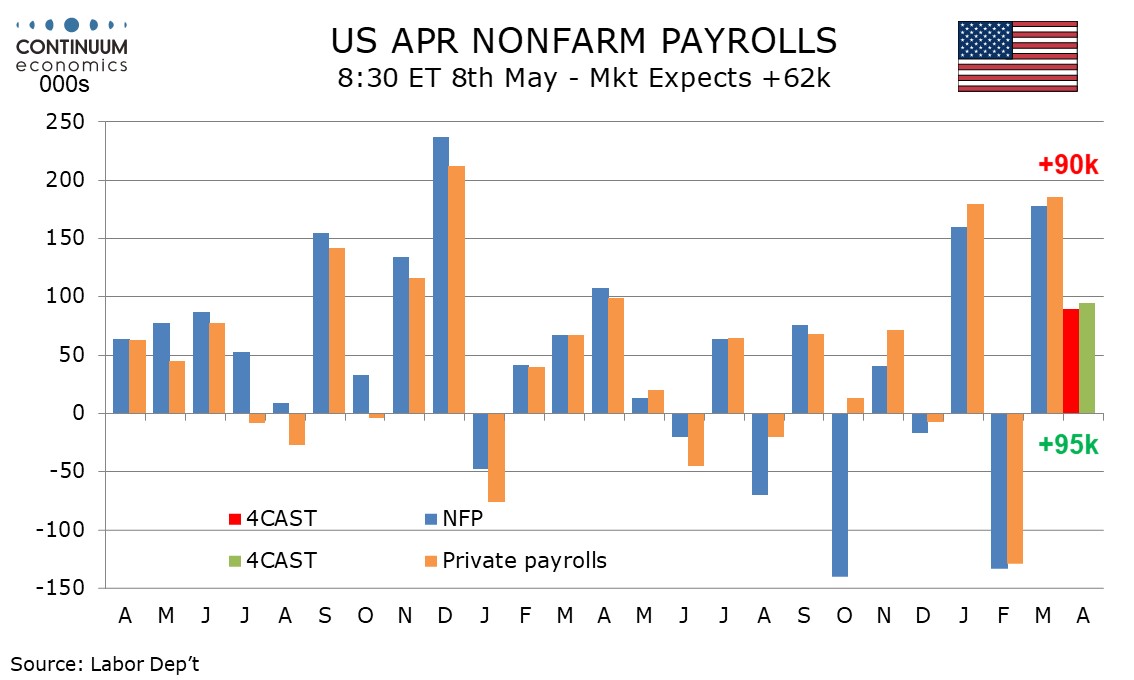

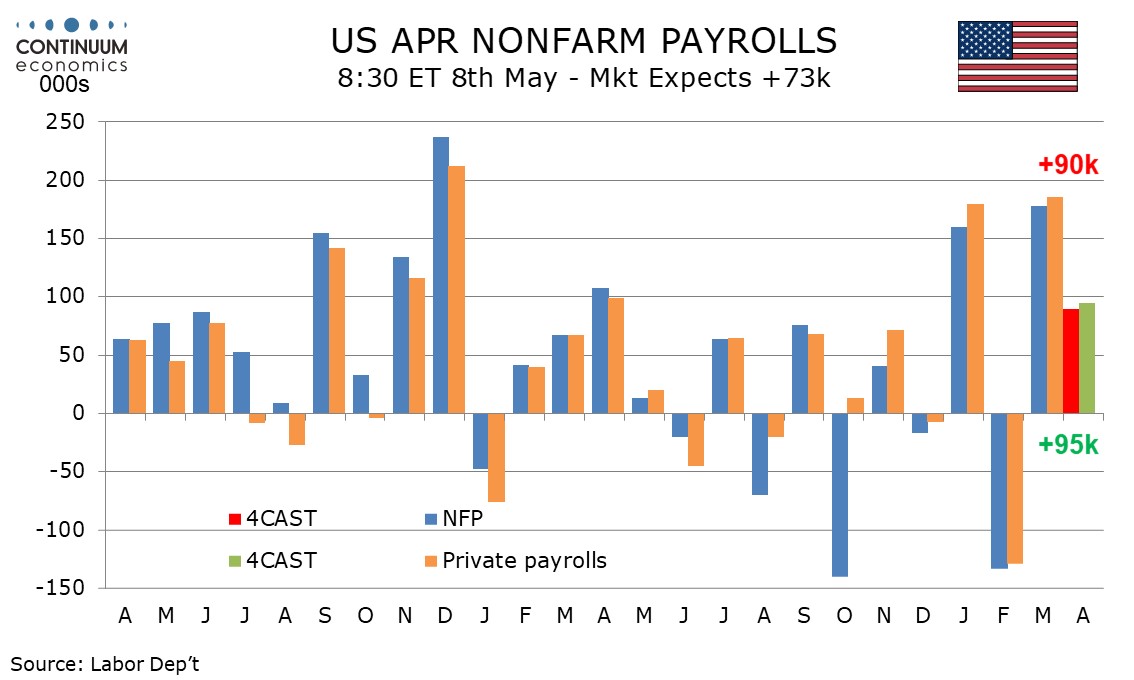

Preview: Due May 8 - U.S. April Employment (Non-Farm Payrolls) - Not as strong as March but some positive signals

May 7, 2026 1:15 PM UTC

We expect April’s non-farm payroll to rise by 90k overall and by 95k in the private sector, less strong than in March but implying some improvement in trend. We expect unemployment to slip to 4.2% from 4.3% and an in line with trend 0.3% increase in average hourly earnings.

May 05, 2026

Preview: Due May 12 - U.S. April CPI - Energy, air fares and a housing distortion (revised)

May 5, 2026 3:47 PM UTC

We now expect April CPI to increase by 0.6% overall and 0.4% ex food and energy, with respective gains before rounding being 0.57% and 0.41%. Energy is likely to add close to 0.2% to the overall gain and feed through from energy is likely to add around 0.1% to the core, largely in air fares. There i

May 04, 2026

Preview: Due May 12 - U.S. April CPI - Energy to rise less sharply than in March, but air fares to lift the core

May 4, 2026 3:56 PM UTC

We expect April CPI to increase by 0.5% overall and 0.3% ex food and energy, with the latter rising by 0.33% before rounding and the highest since January 2025. Seasonal adjustments will restrain the increase in gasoline but we expect feed through of energy prices to air fares to be factor in liftin

April 30, 2026

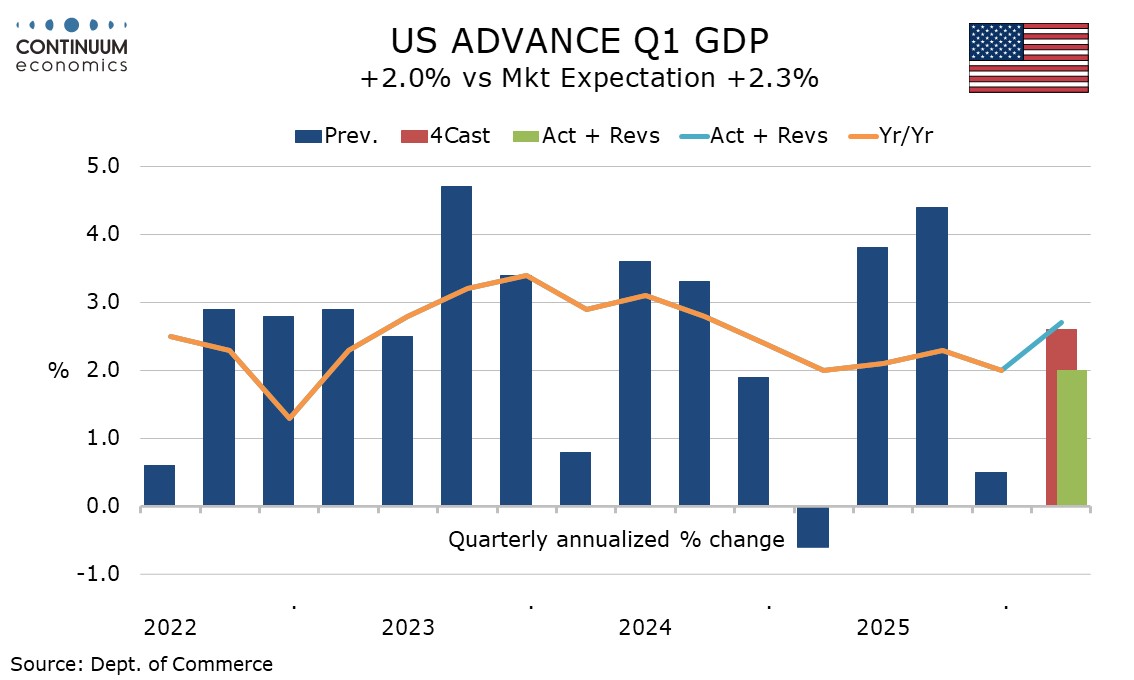

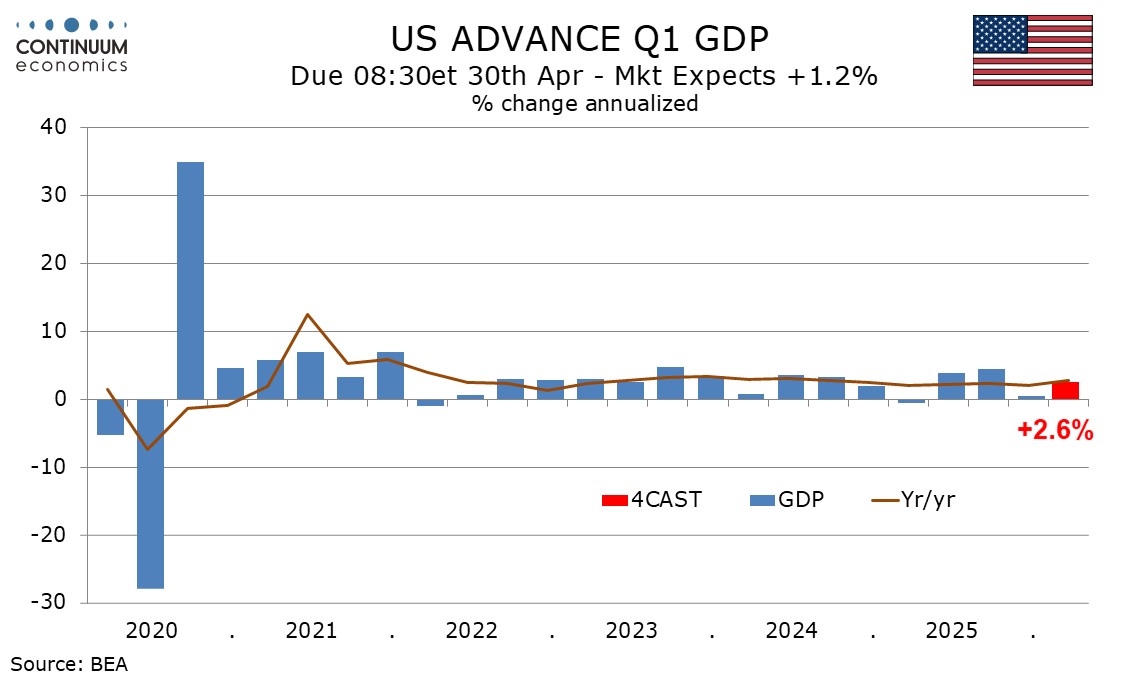

U.S. Q1 GDP shows solid underlying momentum and continued inflationary pressure

April 30, 2026 1:41 PM UTC

The advance estimate of Q1 GDP at 2.0% annualized is slightly weaker than expected and not an impressive bounce from Q4’s 0.5% which was restrained by a government shutdown. However the detail suggests respectable growth, as do stronger than expected March personal income and spending, and most im

April 29, 2026

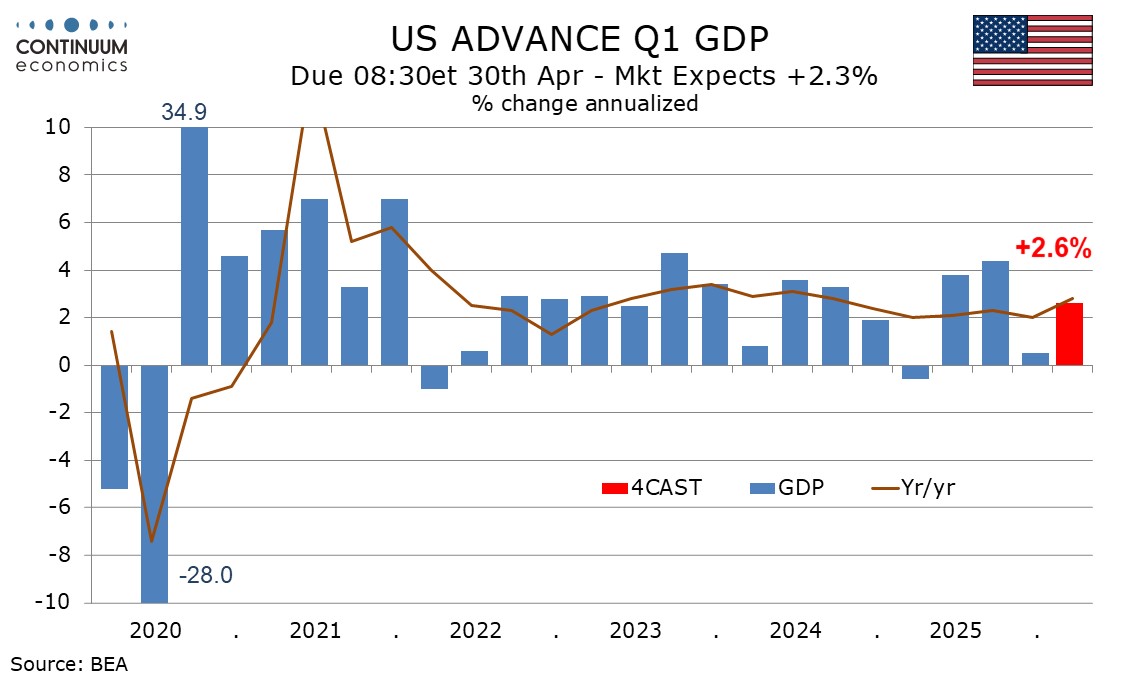

Preview: Due April 30 - U.S. Q1 GDP - Government to lead bounce from weak Q4, Core PCE prices stronger

April 29, 2026 1:24 PM UTC

We expect a 2.6% annualized increase in Q1 GDP, improved from a weak 0.5% in Q4 largely due to a rebound in government from Q4 data that was depressed by a shutdown. Excluding government we expect a second straight quarter close to 1.5%. We expect a significant acceleration in core PCE prices, to 4.

April 28, 2026

Preview: Due May 8 - U.S. April Employment (Non-Farm Payrolls) - Not as strong as March but some positive signals

April 28, 2026 5:12 PM UTC

We expect April’s non-farm payroll to rise by 90k overall and by 95k in the private sector, less strong than in March but implying some improvement in trend. We expect unemployment to slip to 4.2% from 4.3% and an in line with trend 0.3% increase in average hourly earnings.

Big EM: Diverging Fiscal Trends

April 28, 2026 12:35 PM UTC

· EM government bond spreads are controlled as 2nd round inflation effects are likely to be less than 2022, due to less buoyant domestic demand/slacker labour markets and less global supply chain pressure ex oil/oil products. Brazil is expected to cut rates and others will likely not

April 21, 2026

Preview: Due April 30 - U.S. Q1 GDP - Government to lead bounce from weak Q4, Core PCE prices stronger

April 21, 2026 5:31 PM UTC

We expect a 2.6% annualized increase in Q1 GDP, improved from a weak 0.5% in Q4 largely due to a rebound in government from Q4 data that was depressed by a shutdown. Excluding government we expect a second straight quarter close to 1.5%. We expect a significant acceleration in core PCE prices, to 4.

April 17, 2026

Equities: Still a Rocky Road in 2026

April 17, 2026 12:49 PM UTC

· Any deal between the U.S. and Iran would still be seen as a positive win in equities, as it would raise hopes that it could be followed by a multi-year settlement that could include more Iran oil and gas into the global energy markets and lower energy prices. No deal is also feasible,

April 15, 2026

DM Central Bank Signals Awaited

April 15, 2026 12:12 PM UTC

· Fed/ECB and BOE meetings will likely see concern over the potential 2nd round inflation effects from the Iran war, but forecasts seeing inflation coming down in 2027 and no imminent signals of tightening from the ECB/BOE – our baseline remains for easing later in the year, as energy

April 10, 2026

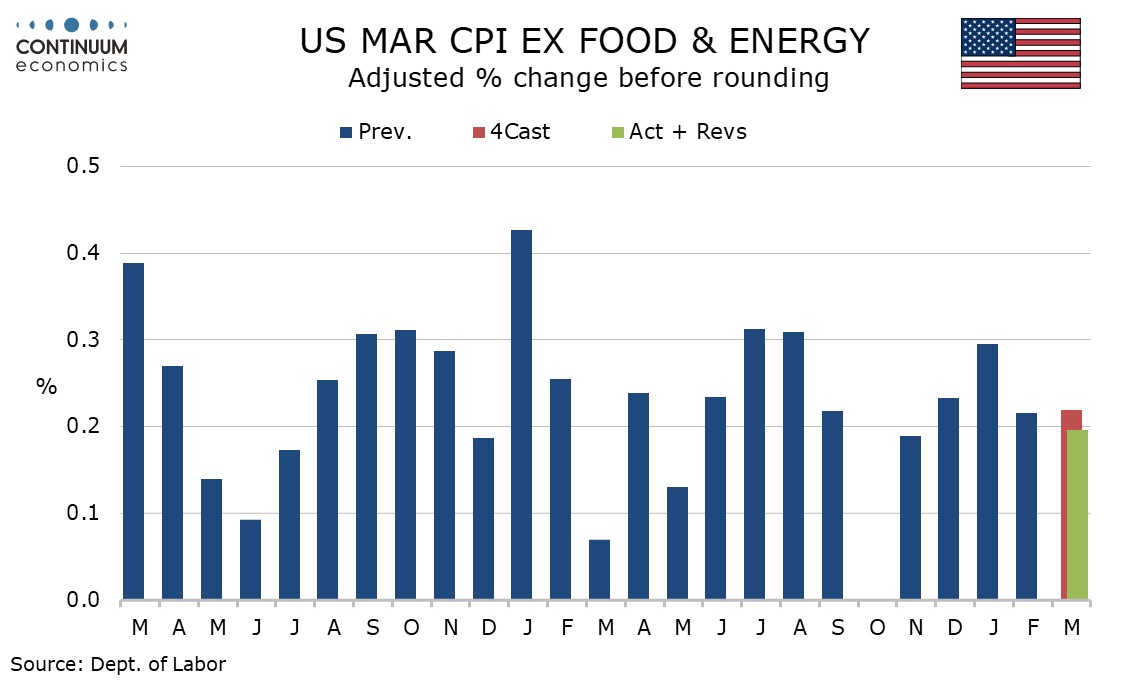

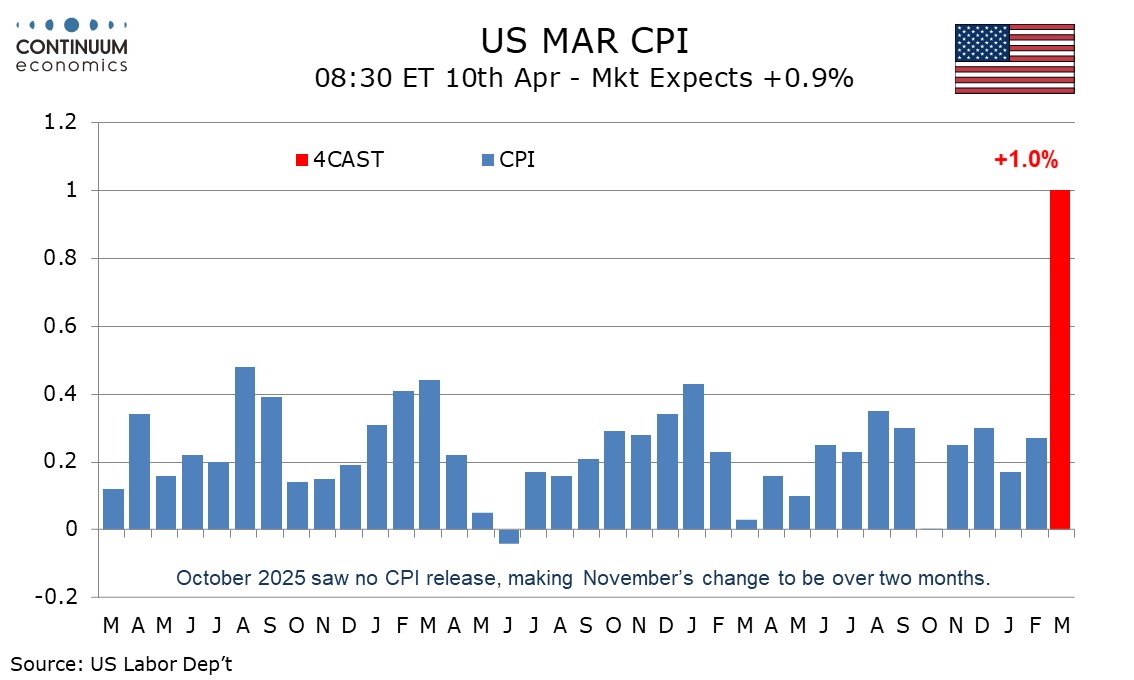

U.S. March CPI - Subdued core rate provides relief

April 10, 2026 12:55 PM UTC

March CPI is as the market expected with a 0.9% increase (0.865% before rounding) led by a surge in energy, but the core rate ex food and energy shows little sign of feed through, rising by a lower than expected 0.2%, with the gain before rounding at 0.196%, the slowest since November’s subdued tw

April 09, 2026

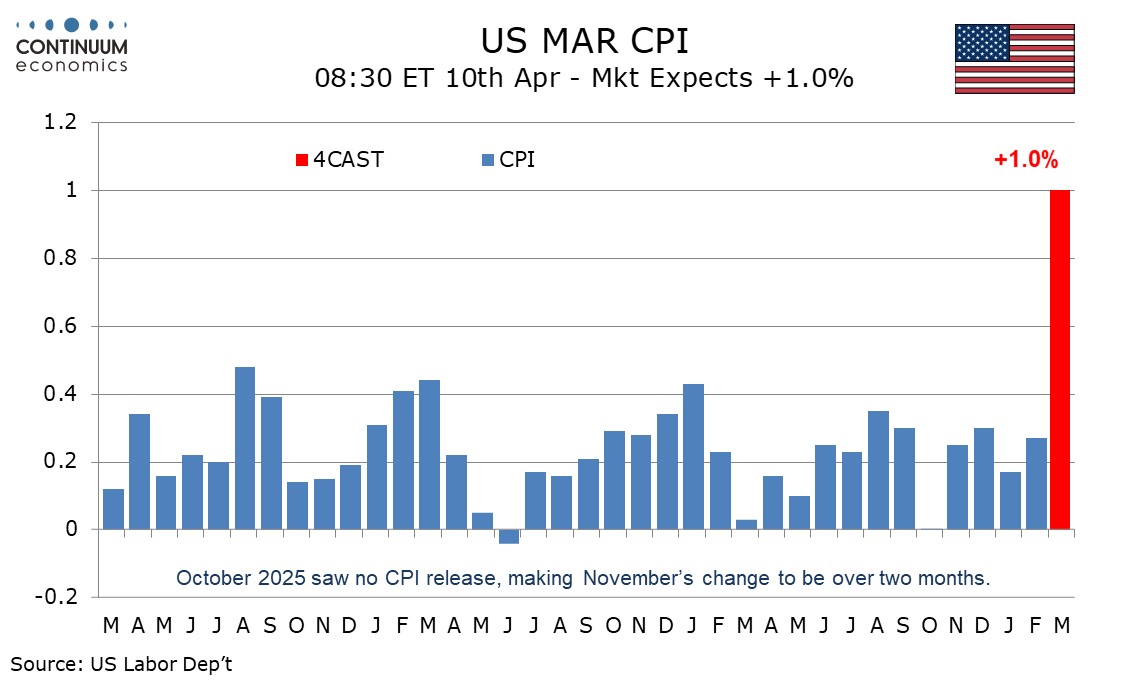

Preview: Due April 10 - U.S. March CPI - Energy to surge, but core rate seen similar to February

April 9, 2026 1:39 PM UTC

We expect March CPI to surge by 1.0% overall, which would be the strongest rise since June 2022, seen in the aftermath of the Russian invasion of Ukraine. However we expect only a moderate increase ex food and energy, of 0.22% before rounding, which would match that seen in February.

April 08, 2026

2-Week Ceasefire, Then?

April 8, 2026 10:09 AM UTC

· The ceasefire will likely involve a new normal of shipping companies paying Iran a toll. While this is adding a cost to Gulf crude oil/products and LNG, the premium will be a lot lower than the cost of an ongoing war. The U.S. and Iran will now likely be reluctant to restart the w

April 03, 2026

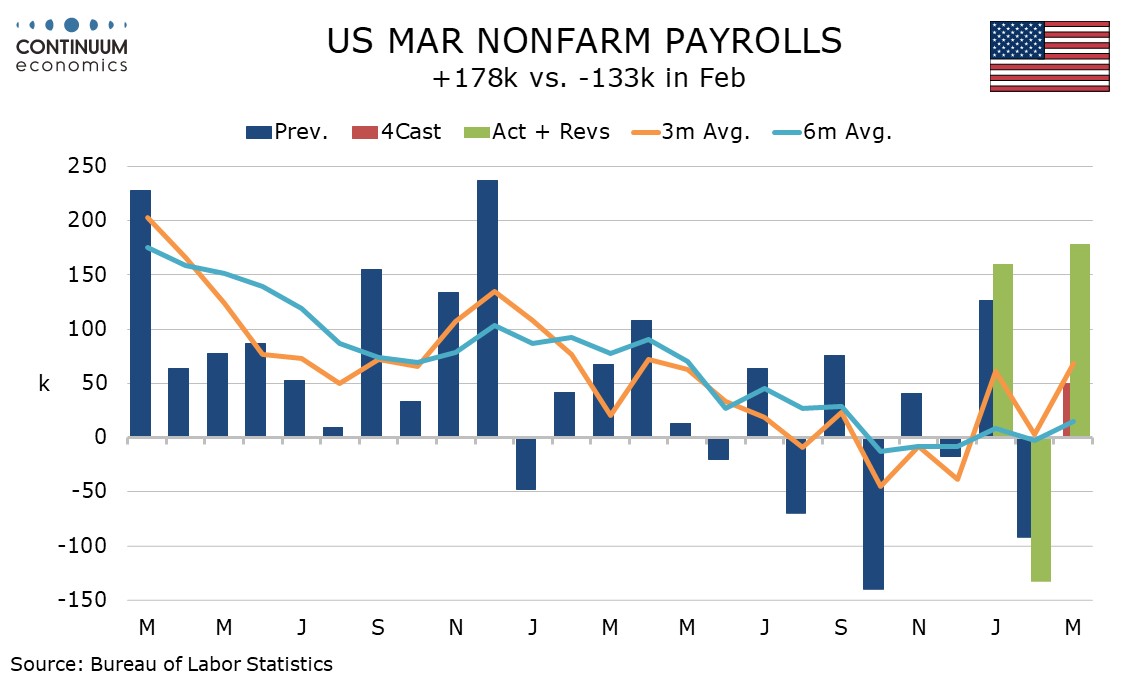

U.S. March Employment - Strong report suggests risks clearly higher on the inflation side

April 3, 2026 1:27 PM UTC

March’s non-farm payrolls is clearly on the strong side of expectations, up by 178k and an even stronger 186k in the private sector, with minimal net downward revisions of 7k. Unemployment unexpectedly fell to 4.3% from 4.4%. Less positive are a lower than expected 0.2% rise in average hourly earn

April 02, 2026

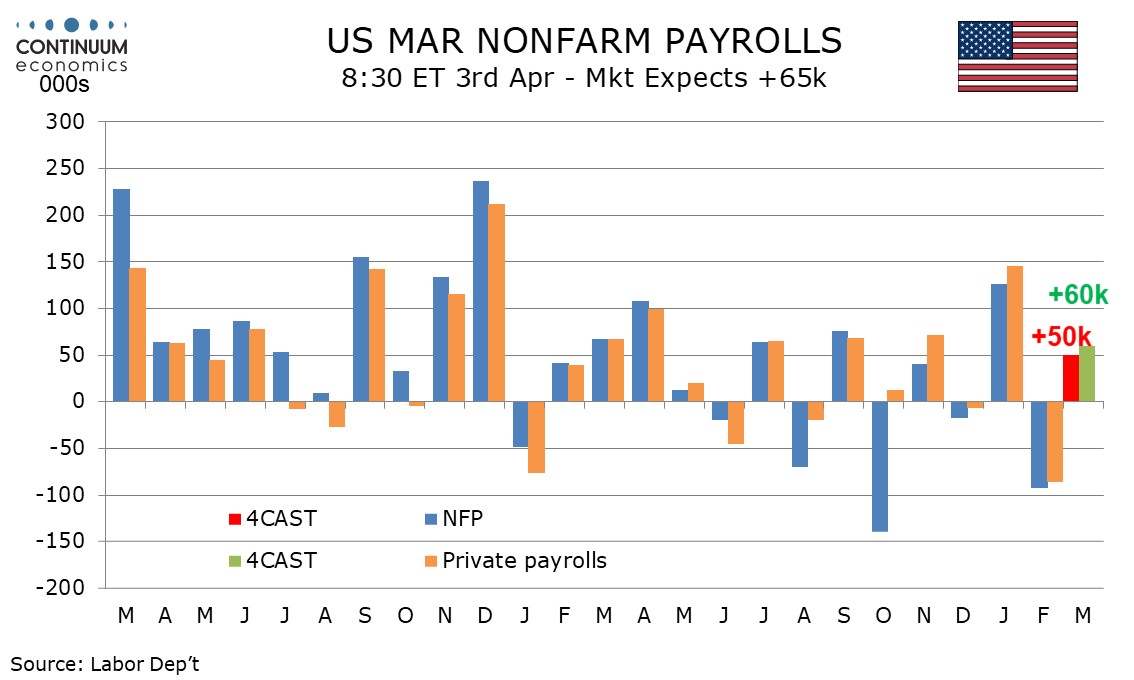

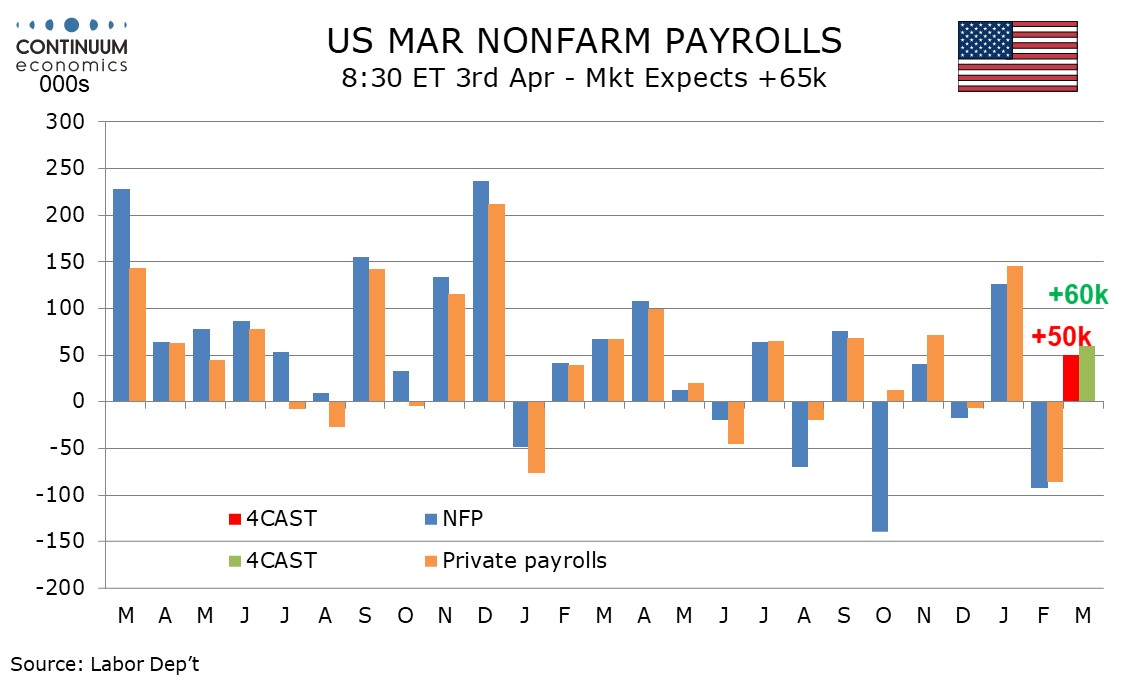

Preview: Due April 3 - U.S. March Employment (Non-Farm Payrolls) - A boost from returning strikers, but trend subdued

April 2, 2026 1:57 PM UTC

We now expect March’s non-farm payroll to rise by 50k overall and by 60k in the private sector, both revised up by 30k due to the ending of strikes, largely in health, as shown in Friday’s strike report. This is still consistent with a subdued labor market picture, which a rise in unemployment

April 01, 2026

Preview: Due April 10 - U.S. March CPI - Energy to surge, but core rate seen similar to February

April 1, 2026 7:26 PM UTC

We expect March CPI to surge by 1.0% overall, which would be the strongest rise since June 2022, seen in the aftermath of the Russian invasion of Ukraine. However we expect only a moderate increase ex food and energy, of 0.22% before rounding, which would match that seen in February.

March 31, 2026

Preview: Due April 3 - U.S. March Employment (Non-Farm Payrolls) - Forecast revised up on returning strikers, but still implying a subdued trend

March 31, 2026 5:56 PM UTC

We now expect March’s non-farm payroll to rise by 50k overall and by 60k in the private sector, both revised up by 30k due to the ending of strikes, largely in health, as shown in Friday’s strike report. This is still consistent with a subdued labor market picture, which a rise in unemployment

March 30, 2026

Markets: Short vs Long Iran War

March 30, 2026 8:00 AM UTC

· For a 4-8 week war and 3-4 quarters of energy price normalisation, we see a 10% U.S. equity market correction in H1 2026 driven by the current Iran war and/or consumption slowing due to lower (real) wage growth, alongside still stretched valuations in equity and equity-bond terms. T