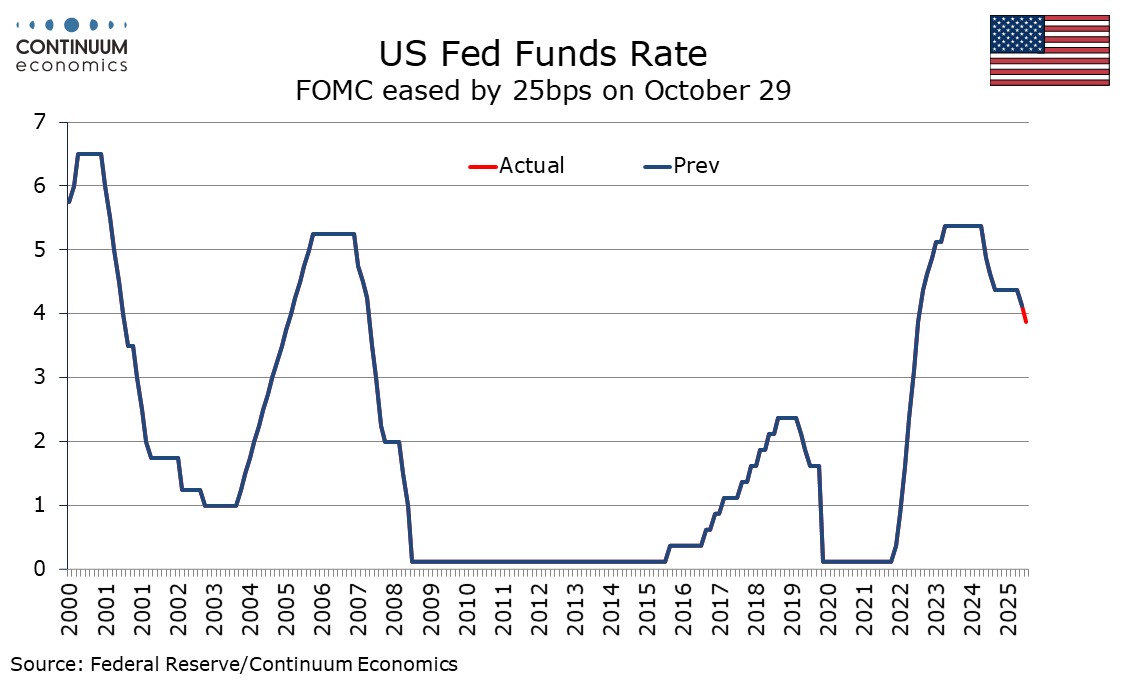

FOMC - Strong Differences of Opinion Leave December Decision Dependent on Incoming Information

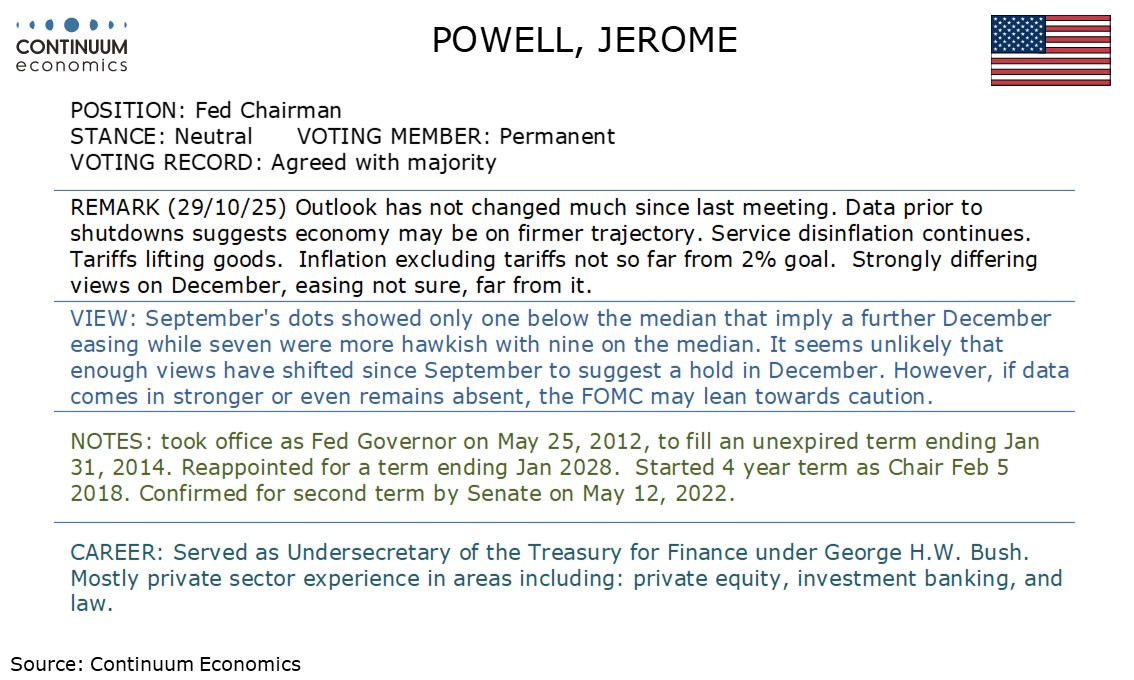

After a statement that contained no major surprises, the highlight of FOMC Chairman Jerome Powell’s press conference was his comment that there were strong differences on policy going forward, and that a December ease was far from assured. While we still feel that on balance easing in December is more likely than not, it will be dependent on incoming information sustaining the case for easing. Even a continued lack of data could keep the Fed on hold.

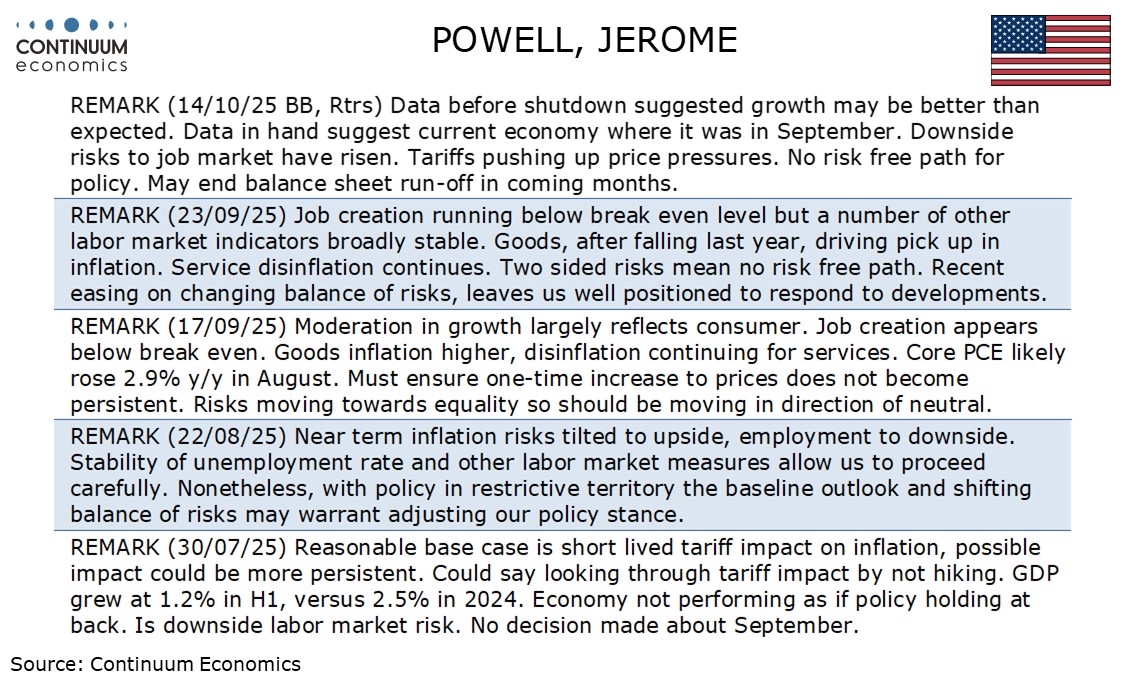

The 25bps easing to 3.75%-4.0% was as expected, and there were only two dissents, dovish Governor Stephen Miran backing a 50-bps move while Kansas City Fed President Jeffrey Schmid wanted no change. The adjustments to the statement appeared marginally more hawkish, stating that available indicators suggest the economy has been expanding at a moderate pace, consistent with forecasts from most economists that Q3 GDP is likely to be stronger than the 1.6% annualized average of Q1 and Q2. Powell added that data prior to the shutdown suggested the economy may be on a firmer trajectory. He also noted that state initial jobless claims data has not seen much change since the government shutdown which has prevented the Federal Labor Department aggregating the state data.

The statement added the words “since earlier in the year” in repeating that inflation has moved up and remains somewhat elevated, which notes recent gains. However Powell in his press conference however did not sound overly anxious about recent inflation data, noting continued disinflation in services despite tariff-induced gains in goods, and adding that excluding tariffs inflation was not too far from target. He also forecast gains of 2.8% for both overall and core PCE prices in September, and that is consistent with subdued monthly gains of 0.2% and 0.1% respectively.

It should not be a surprise that there are differences on policy going forward. September’s dots showed nine respondents on the median which implied one more easing in December, with only one below the median and seven above. It is normal to state that the decision for the next meeting is not a done deal, but Powell’s follow up to that, saying far from it, was unusually emphatic. We doubt that enough voters have had a clear change of opinion to mean that a hold is now more likely than an ease in December, particularly with inflationary risks not appearing to have significantly increased since September. However, even the recently dovish Governor Christopher Waller has noted the contrast between signals of labor market slowing but probable GDP resilience, and wants to see whether the contrast persists and if not, how it is resolved before committing to further easing. It is not even certain whether the Fed will have received the Q3 GDP and employment reports for September, October and November that are due to be released before the FOMC next meets on December 10. Powell compared conducting monetary policy in the absence of data to driving in fog, which calls for slowing down, but stressed that a continued absence of data would not automatically mean a policy hold.

On balance we still expect a 25bps easing in December, but our central view is that data will resume in mid-November and will not show a clear increase in inflationary risks or a fresh acceleration in the labor market. Our Q3 GDP estimate of 2.3% is also lower than several, if stronger than the first half. Still, the caution towards December suggests that a pause in Q1 2026 would be likely to follow a December move. The comments on December’s meeting ensured that the decision to end Quantitative Tightening on December 1 was not given excessive attention. Powell had signaled that this was likely in comments on October 14.