United Kingdom

View:

June 30, 2026

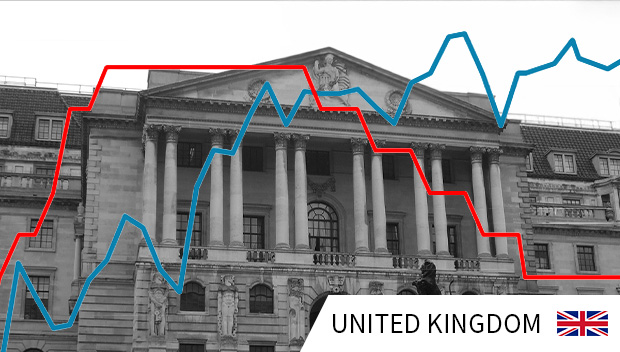

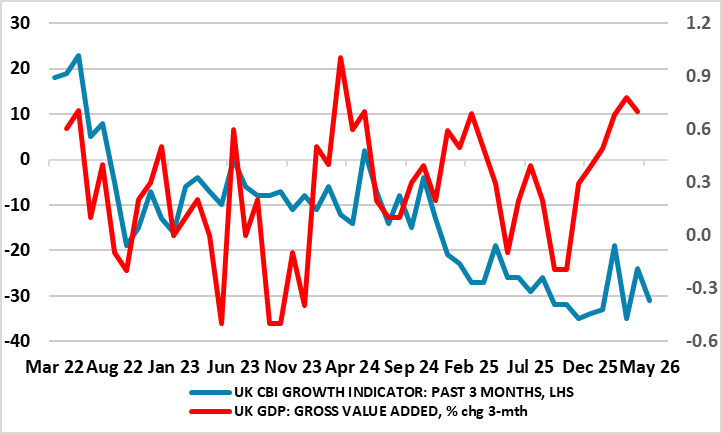

UK GDP Outlook Update – Still Fragile With Surveys Negative

June 30, 2026 4:13 PM UTC

It is the relative norm for an economy to be offering disparate signals at any one juncture, if not actual conflicting ones. This is certainly the case in the UK currently, where upbeat Q1 GDP data of 0.6% q/q have been, confirmed and notably by a perkier consumer. Such shots of real growth ar

June 26, 2026

Economic Data and Events Week Ahead Jun 29 - Jul 3

June 26, 2026 2:45 PM UTC

The week ahead has plenty of notable events, spanning Eurozone inflation on one side, to US payrolls on the other, and with central bank speakers all round - the ECB Sintra conference at the start of the week hears from Lagarde and then a panel that includes Warsh and Bailey.

June 25, 2026

June 24, 2026

Outlook Overview: Cyclical and Structural Forces

June 24, 2026 7:00 AM UTC

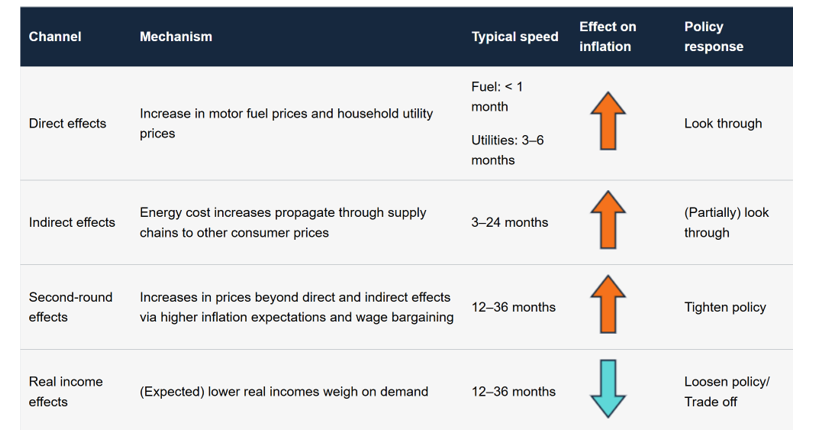

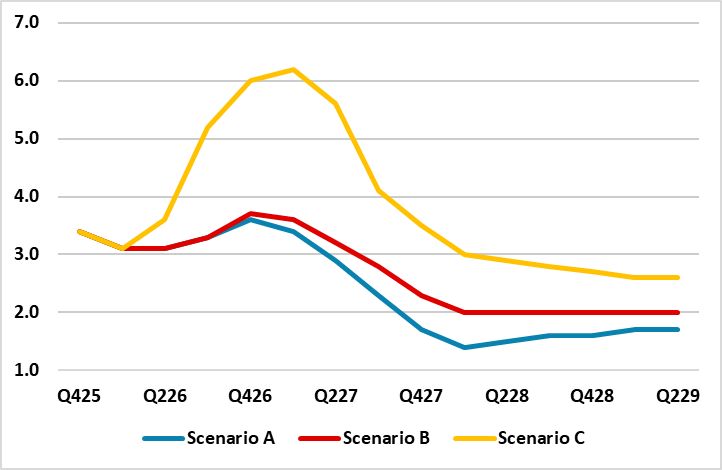

· The difference between 2nd round inflation effects from higher energy prices and 1st round effects that central banks can look through swings on whether the Straits of Hormuz will remain open in the coming months after the U.S./Iran interim agreement (here). Despite some tensions, we

June 23, 2026

DM Rates Outlook: Tightening or Easing?

June 23, 2026 8:15 AM UTC

· With the U.S./Iran interim agreement likely to hold and energy prices softening, our projected consumer slowdown will likely tilt the Fed not to hike in H2 2026 and to actually ease by 50bps in 2027, with 25bps moves in both Q2 and Q3. With 2yr yields consistent with a hike, the tra

DM and EM FX Outlook: Cross-Currents for H2 and 2027

June 23, 2026 8:00 AM UTC

· Our baseline for the coming quarters is that global FX is moving through a period of dollar bounce and cross-current positioning adjustment, rather than a clean return to the dollar downtrend. The near-term driver is the market's (over) hawkish reading of the June FOMC/Summary of Econ

DM ex U.S. EZ Outlook (Japan and Western Europe): Navigating the Post Iran War Period?

June 23, 2026 7:43 AM UTC

· We have revised 2026 Japan GDP only slightly lower to 0.8% as wage growth is solidly above 3%, which will support consumption for the rest of 2026/27. The extension of energy stimulus will cap headline inflation for Q2/Q3 2026. For the BOJ, despite hawkish forward guidance, the 1% r

June 22, 2026

Equities Outlook: AI Optimism, But Caution Elsewhere in DM economies

June 22, 2026 7:05 AM UTC

· In terms of the S&P500, we remain less concerned about high valuations in the tech sector provided AI labs growth remains fast. 12mth fwd information technology are mid-range in the 2020-26 experience rather than at the highs. Even so, heavy equity issuance by tech companies and a s

June 18, 2026

BOE: Gang of 6 and Steady 2026 Rates

June 18, 2026 11:27 AM UTC

Though Megan Greene joined Huw Pill in calling for a one off 25bps risk management hike, 6 MPC members feel that disinflation is showing through and a soft economy and labor market warrants waiting to see energy prices and potential 2nd round effects. This gang of 6 also feels that markets have ti

June 17, 2026

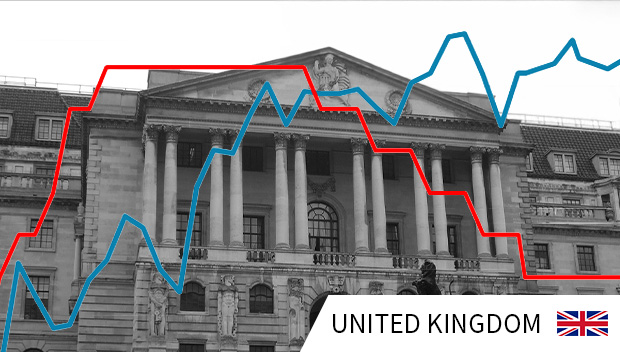

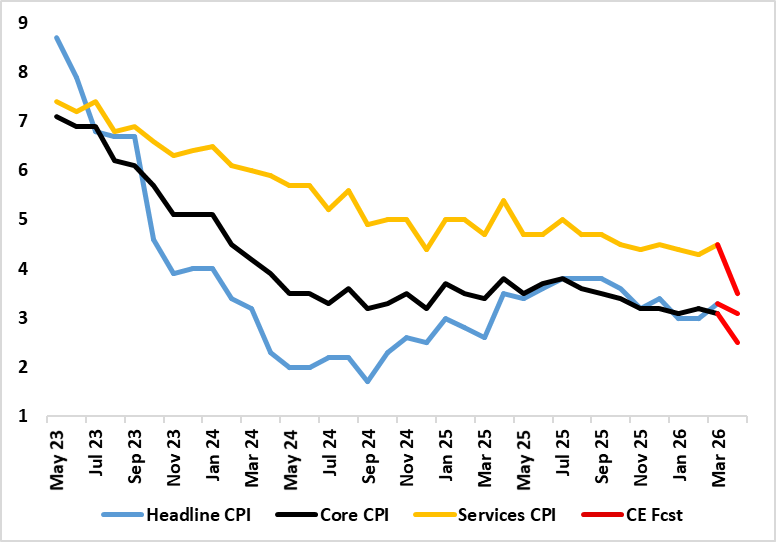

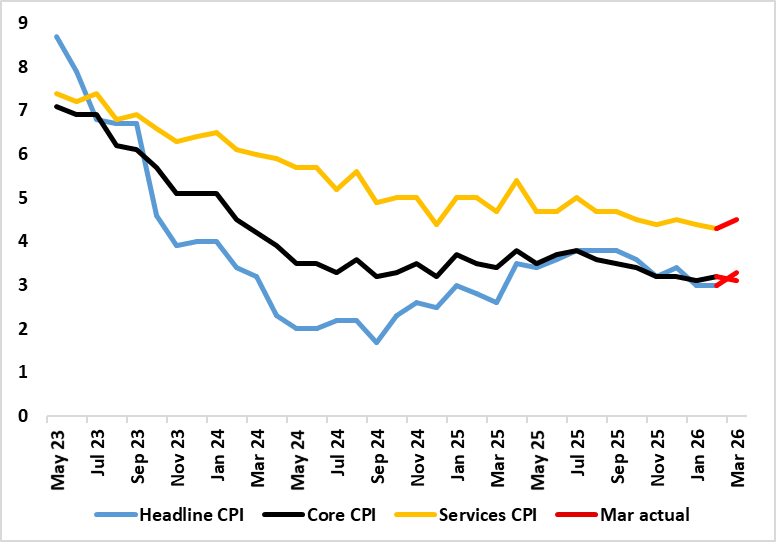

UK CPI Review: Inflation Peaking?

June 17, 2026 7:40 AM UTC

What have been energy induced price rises are starting to ease and may do so further In June before the OFGEM induced price rise hits July numbers. But a less worrying picture emerges in the latest (ie May) CPI and even PPI data. Indeed, once again, actual CPI have offered a more benign picture

June 15, 2026

U.S./Iran Interim Deal and Reopening Strait of Hormuz

June 15, 2026 12:32 PM UTC

· Our baseline (80%) is that the Strait of Hormuz will reopen in H2 2026 and remains open through 2027. However, logistics dislocation plus a switch from commercial inventory rundown to rebuilding will likely slow the decline in oil prices back towards normal levels (Figure 1). O

June 12, 2026

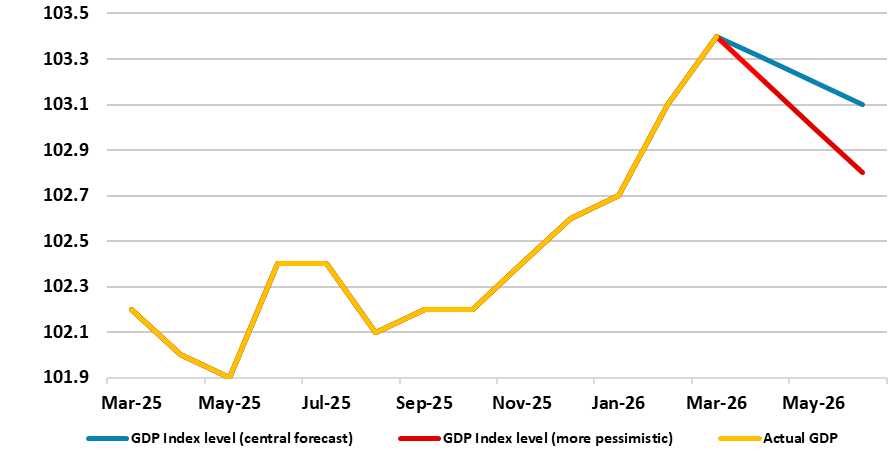

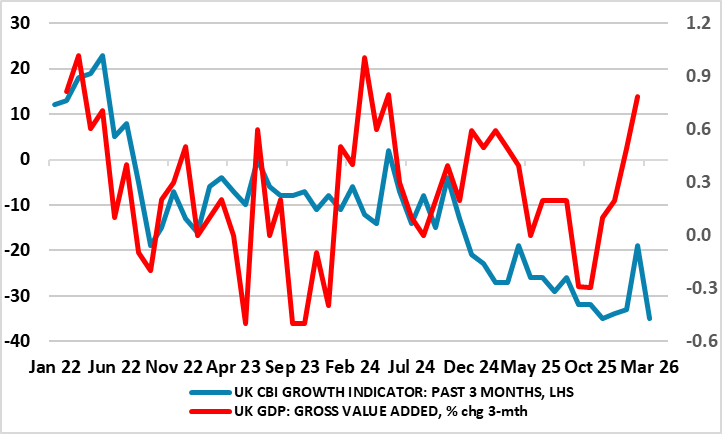

UK GDP Review: GDP Upside Surprises Persist?

June 12, 2026 6:56 AM UTC

Perhaps it is a supreme irony that just as business surveys suggest clear weakness, if not fresh contraction, the actual real economy has surprised on the upside, even now into the second month after the Middle East conflict started. Indeed, and in perspective, official GDP data suggest that since

June 11, 2026

BoE Preview (Jun 18): Splits to Widen, But Stable Policy Outlook Intact

June 11, 2026 10:26 AM UTC

Not only this month, but we see the BoE being on hold for the rest of the year with rate cuts then resuming through 2027. Although markets are pricing just over two hikes from the current 3.75% with a 50%-plus probability of the first being delivered at the July 30 MPC meeting, our view is hardly

June 10, 2026

Financial Markets/Policymakers and the Strait of Hormuz Question

June 10, 2026 8:05 AM UTC

· Though the U.S. and Iran have attacked each other June 10, talks to reopen the straits of hormuz still continue. An Iran/U.S. agreement to reopen the Straits of Hormuz could cure the risk of a demand/supply oil market imbalance and produce some psychological relief that could knock USD

June 09, 2026

UK CPI Preview (Jun 17): Inflation Peaking?

June 9, 2026 9:37 AM UTC

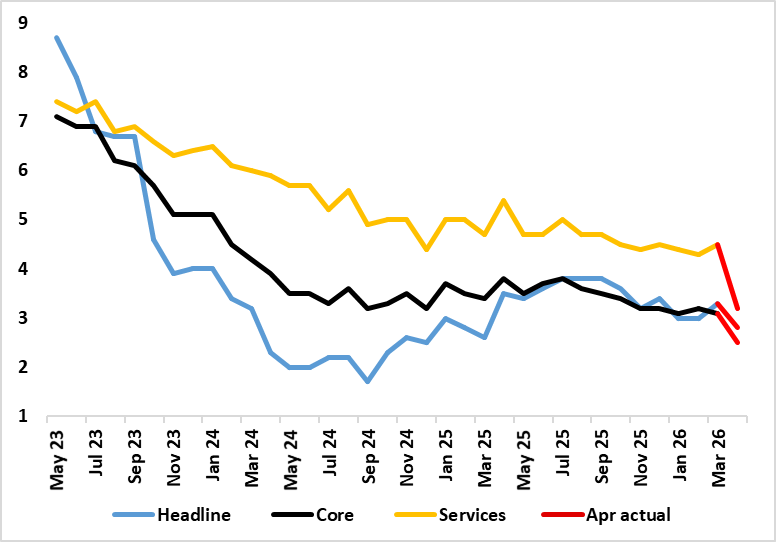

What have been energy induced price rises are now very evident, even more so in some aspects of the latest PPI data. Regardless, actual CPI have offered a more benign picture both in terms fo headline and underlying trends. Indeed, having seen headline CPI jump to 3.3% in March and where service

June 08, 2026

DM Government Bonds: Risks of Higher Long End Premia?

June 8, 2026 2:10 PM UTC

· Our baseline is for DM government bond yields ex Japan to remain elevated, but controlled. Japan extra risk premium is driven by BOJ QT at 6% of GDP, more than long-term debt fears. Major catalysts could drive a regime change to higher risk premia and steeper yield curves, but non

June 04, 2026

UK GDP Preview (Jun 12): GDP Upside Surprises To Reverse?

June 4, 2026 9:49 AM UTC

Perhaps it is a supreme irony that just as business surveys suggest clear weakness, if not fresh contraction, the actual real economy has surprised on the upside, even in the first month after the Middle East conflict. Indeed, and in perspective, official GDP data suggest that since Labour took of

May 29, 2026

Taiwan: Low Invasion Risk Post Trump Visit

May 29, 2026 11:05 AM UTC

· The most likely option for China is to continue the air and naval grey zone warfare around Taiwan, combined with support for pro-China factions in Taiwan’s parliament to build pressure for reunification at some stage. This stick and carrot approach is our baseline (Figure 1). Wi

May 27, 2026

DM Government Bond Markets in Limbo

May 27, 2026 12:22 PM UTC

· DM central bank meetings in June will be crucial, with a high risk of a 25bps ECB hike to warn against 2nd round effects from higher oil prices and a BOJ 25bps hike as part of the ongoing normalisation. However, the tone that the Fed’s Warsh will set will also be key. The bigges

May 22, 2026

Europe: Anti-Immigration Vs More Negative Demographics

May 22, 2026 8:12 AM UTC

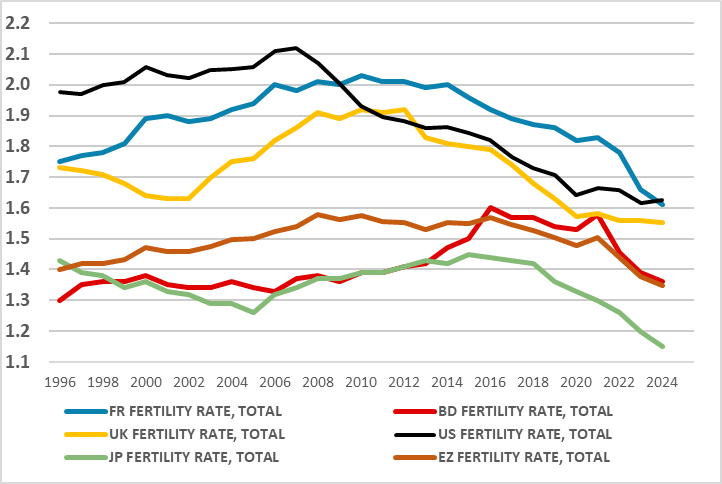

A significant demographic tremor is gaining speed and breadth - globally. Just as politics – certainly in the west - is framed around ending or at least reducing and controlling immigration, it seems that the populists at the helm of such thinking are not considering the ramifications of such a

May 20, 2026

UK CPI Review: Inflation Falls Broadly But A Calm Before the Storm?

May 20, 2026 6:42 AM UTC

What are energy induced price rises are now very evident, even more so in the latest PPI data very much contrasting with the more benign picture in April’s more closely watched CPI figures. Thus, having seen headline CPI jump to 3.3% in March and where services rose to 4.5% on the back if what may

May 19, 2026

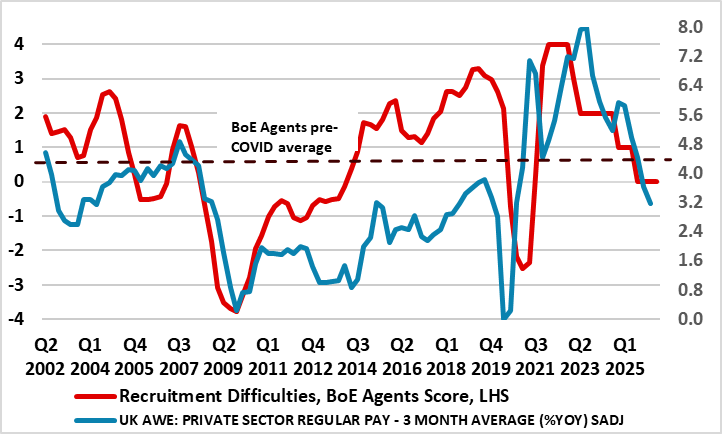

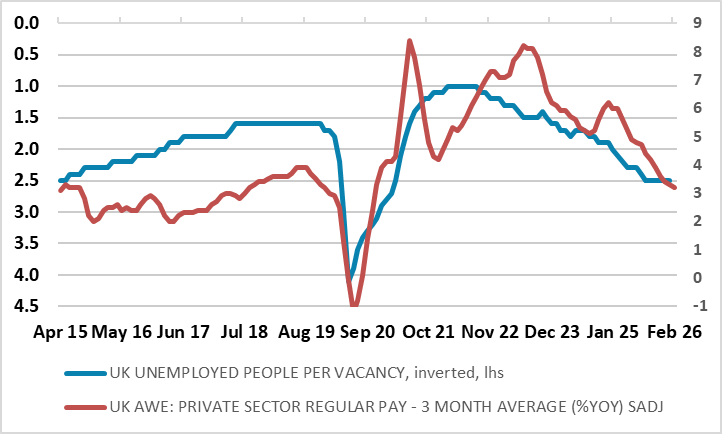

UK Labor Market: Core Wage Pressures hit New Cycle -Low as Jobs Growth into Sharp Reverse

May 19, 2026 6:56 AM UTC

Even more clearly, there are further signs that the labor market is haemorrhaging jobs both clearly and broadly with fresh falls in the more authoritative measure of jobs covering payrolls. Indeed, private sector payrolls are still falling, down over 0.8 ppt in y/y terms with the m/m drop the larg

May 15, 2026

Middle East Conflict: U.S. Helping Chinese Whispers?

May 15, 2026 11:26 AM UTC

In hosting President Trump this week, China feels it is vying, if not achieving, parity with the U.S. as the world’s superpowers; from China’s perspective, it regards Russia similarly. It does seem as if China’s goal at this summit was to get more effective flexibility in shaping Taiwan’

May 14, 2026

UK Politics – A Laboured Labour Election Ahead?

May 14, 2026 12:55 PM UTC

It is somewhat ironic that as markets (particularly gilts) fret over a shift to the left causing less fiscal prudency, it is actually the centre of the Labour party that is fermenting the most uncertainty. (Now Ex) Secretary Streeting has yet to make a formal bid to challenge PM Starmer for the le

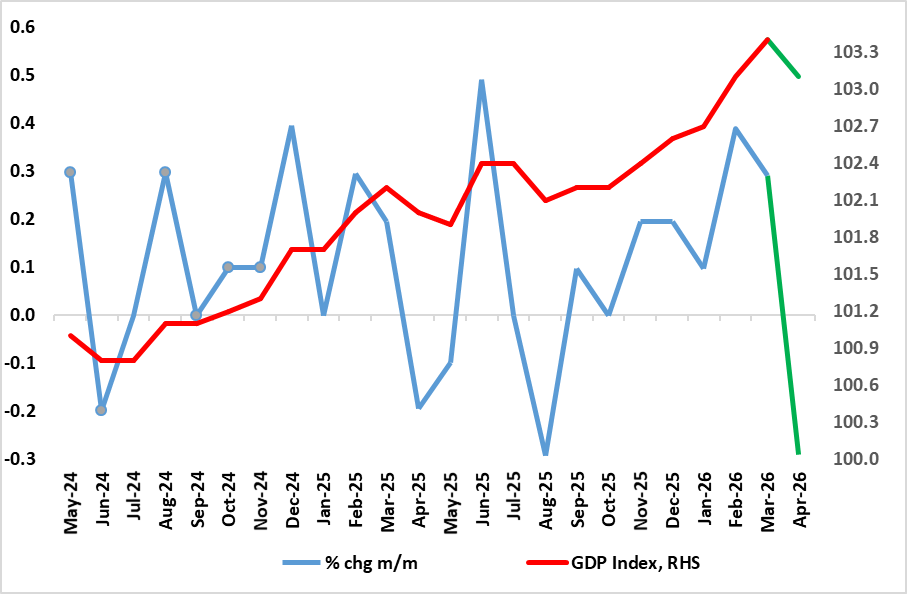

UK GDP Review: GDP Upside Surprises Continue, Correction Due or Fresh Trend?

May 14, 2026 6:59 AM UTC

Perhaps it is a supreme irony that just as the Labour government tears itself apart after disastrous election results last week, the actual real economy continues to surprise on the upside. Notably, since taking office in July 2024, the economy has grown a cumulative 2%-plus, ie over 1% per year.?

May 12, 2026

UK CPI Preview (May 20): Inflation Sedate For Now But Wages Still on the Wane?

May 12, 2026 12:05 PM UTC

What are energy induced price rises are now very evident, most notably in PPI data as well as the more closely watched CPI figures. Thus after a stable 3.0% (a 10-mth low) February’s headline – matching the consensus, headline CPI jumped to 3.3% in March. Services, however, rose from 4.3% a fo

May 07, 2026

Straits of Hormuz Scenarios

May 7, 2026 6:25 AM UTC

· Our new baseline (70% probability) is for the Straits of Hormuz to start to partially reopen by June/July based on a framework deal between Iran and the U.S. This means more elevated oil prices in Q2, but then a gradual reduction in WTI to USD85 end-2026 and USD75 end 2027. The al

May 05, 2026

UK GDP Preview (May 14): March GDP Drop Expected, Correction or Fresh Trend?

May 5, 2026 10:16 AM UTC

Before the outbreak of the Iran War there was already a split within the MPC about the policy outlook and that such divisions may have been accentuated by the much stronger than expected February GDP update which showed a m/m rise of 0.5%, the strongest in 14 months. This is likely to have been ab

April 30, 2026

BoE Review: MPC Playing Its Cards Safely (For Now)?

April 30, 2026 12:29 PM UTC

Very clearly, the BoE kept rates on hold with the MPC last month and the same decision was both expected and delivered this time around but with only token fresh dissent, with Chief Economist Pill wanting an immediate hike from the current 3.75%. But splits were more evident in the individual MPC

April 29, 2026

UK Political Risk – Bad Things Come in Threes?

April 29, 2026 12:12 PM UTC

The biggest set of elections since the 2024 general election takes place on 7 May in the UK. Already, UK markets are fretting about the possible outcome, in particular that serious electoral damage to the Labour Party currently running the government could make it swing more to left and dilute fis

April 27, 2026

Straits of Hormuz Standoff and Mixed Markets

April 27, 2026 9:02 AM UTC

• Equities longer time horizon means that they are hoping for a reopening of the Straits of Hormuz (though also being helped by renewed AI optimism), whereas government bond markets actually want to see tangible progress and an associated tempering of DM central banks posturing. This dive

April 24, 2026

BoE Preview (Apr 30) Divided Again But Unmoved (For Now)?

April 24, 2026 9:34 AM UTC

Very clearly, the BoE kept rates on hold with the MPC unanimous last month and the same decision is expected this time around but with probable fresh dissent, with up to 2-3 members opting for an immediate hike. These splits will be even more evident in the individual MPC member statements (as exp

April 22, 2026

Iran Conflict – Who Has the ‘Trump’ Card

April 22, 2026 9:17 AM UTC

When Trump aspires to reaching a deal, he thinks in either black or white. But whether it be political, economic or military the reality is that the world is always various shades of grey. This is very much evident in the way the Iran conflict was planned by the U.S. – the expected clear and r

UK CPI Review: Inflation Being Fuelled But Wages Still on the Wane?

April 22, 2026 6:35 AM UTC

What are energy induced price rises are now very evident, most notably in PPI data as well as the more closely watched CPI figures. Thus after a stable 3.0% (a 10-mth low) February’s headline – matching the consensus, headline CPI jumped to 3.3% in March. Services, however, rose from 4.3% a fo

April 21, 2026

UK Labor Market: Lower Jobless Rates Misleading, as Wage Pressures hit New Cycle -Low

April 21, 2026 6:54 AM UTC

There are further signs that the labor market is haemorrhaging jobs both clearly and broadly with fresh falls in the more authoritative measure of jobs covering payrolls. Indeed, private sector payrolls are still falling, down over 0.5 ppt in y/y terms. Admittedly, headlines may be formed around

April 17, 2026

Equities: Still a Rocky Road in 2026

April 17, 2026 12:49 PM UTC

· Any deal between the U.S. and Iran would still be seen as a positive win in equities, as it would raise hopes that it could be followed by a multi-year settlement that could include more Iran oil and gas into the global energy markets and lower energy prices. No deal is also feasible,

April 16, 2026

UK GDP Review (Apr 16): Fresh But Fleeting Momentum Before the War

April 16, 2026 7:10 AM UTC

Without the outbreak of the Iran War there was already a split within the MPC about the policy outlook and that such divisions may have been accentuated by this latest GDP update which showed a very much above consensus m/m rise of 0.5%, the strongest in 14 months. But of course, the conflict has ch

April 15, 2026

DM Central Bank Signals Awaited

April 15, 2026 12:12 PM UTC

· Fed/ECB and BOE meetings will likely see concern over the potential 2nd round inflation effects from the Iran war, but forecasts seeing inflation coming down in 2027 and no imminent signals of tightening from the ECB/BOE – our baseline remains for easing later in the year, as energy

April 13, 2026

UK CPI Preview (Apr 22): Inflation Being Fuelled But Watch Financial Conditions?

April 13, 2026 2:39 PM UTC

The stormy weather inflation wise is now very evident, most notably in UK fuel prices surging. Thus after a stable 3.0% (a 10-mth low) February’s headline – matching both consensus and BoE projections we see it jumping to 3.5% in March. Services, however, may stay at 4.3% which was a four-year

Iran Blockade and What Next?

April 13, 2026 9:58 AM UTC

· Though the U.S. is introducing a blockade on Iran oil exports, we think the U.S. and Iran remain reluctant to restart the war. How Iran responds to the U.S. blockade is important. It could choose to respond by attacking Gulf energy installations before or after the 2-week ceasefir

April 09, 2026

UK GDP Preview (Apr 16): Moving Sideways Even Before Conflict?

April 9, 2026 8:01 AM UTC

Fresh downside surprises were the story from the January GDP numbers and we expect a similarly muted outcome for the looming February numbers. There were expectations that the economy would enjoy a further successive rise in January, thereby providing the best three-month showing in two years were

April 08, 2026

2-Week Ceasefire, Then?

April 8, 2026 10:09 AM UTC

· The ceasefire will likely involve a new normal of shipping companies paying Iran a toll. While this is adding a cost to Gulf crude oil/products and LNG, the premium will be a lot lower than the cost of an ongoing war. The U.S. and Iran will now likely be reluctant to restart the w

April 07, 2026

2yr and The Iran War

April 7, 2026 8:00 AM UTC

· 2yr yields can edge lower from current less elevated levels, as DM central banks continue to try to calm fears of near-term rate hikes outside of the BOJ/RBA. However, the key swing factor remains the length of the Iran war, as that will determine the trajectory of energy prices in

March 31, 2026

Iran War: Invasion Risks

March 31, 2026 10:55 AM UTC

· Any ground-based invasion would likely result in a long war and Iran would likely counter with attacks on energy or other key facilities around the Gulf. Sea and air based invasions are also difficult, while any victory would likely be followed by occupation. WTI oil prices would

March 30, 2026

Markets: Short vs Long Iran War

March 30, 2026 8:00 AM UTC

· For a 4-8 week war and 3-4 quarters of energy price normalisation, we see a 10% U.S. equity market correction in H1 2026 driven by the current Iran war and/or consumption slowing due to lower (real) wage growth, alongside still stretched valuations in equity and equity-bond terms. T