Germany

View:

July 01, 2026

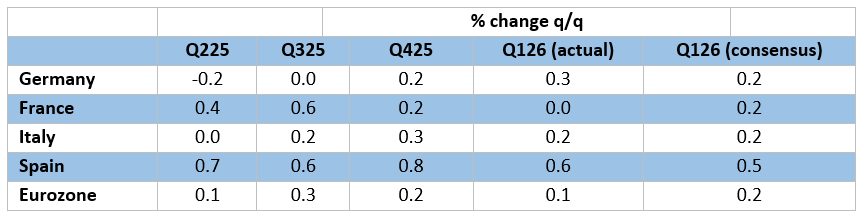

EZ HICP Review: Absence Second-Round Effects Continues

July 1, 2026 1:42 PM UTC

Contrary to some thinking, EZ HICP inflation continues to behave, both absolutely and relatively – ie to what looks ever excessive ECB price thinking. The question must be if and when the ECB chooses to note friendlier price and costs signals, rather than pander to the upside prices risks that o

EZ HICP Review: Absence Second-Round Effects Continues

July 1, 2026 10:41 AM UTC

Contrary to some thinking, EZ HICP inflation continues to behave, both absolutely and relatively – ie to what looks ever excessive ECB price thinking. The question must be if and when the ECB chooses to note friendlier price and costs signals, rather than pander to the upside prices risks that o

June 30, 2026

June 26, 2026

Economic Data and Events Week Ahead Jun 29 - Jul 3

June 26, 2026 2:45 PM UTC

The week ahead has plenty of notable events, spanning Eurozone inflation on one side, to US payrolls on the other, and with central bank speakers all round - the ECB Sintra conference at the start of the week hears from Lagarde and then a panel that includes Warsh and Bailey.

ECB Sin(a)tra Preview: Should the ECB Only Consider My Way?

June 26, 2026 1:29 PM UTC

The speed and manner in which the ECB adopted a hawkish stance is response to the Middle East conflict was no surprise; it has many precedents, some of which have led to policy errors which we think may be being repeated at this juncture. Indeed, despite friendlier price and costs signals, the ECB

June 25, 2026

June 24, 2026

Outlook Overview: Cyclical and Structural Forces

June 24, 2026 7:00 AM UTC

· The difference between 2nd round inflation effects from higher energy prices and 1st round effects that central banks can look through swings on whether the Straits of Hormuz will remain open in the coming months after the U.S./Iran interim agreement (here). Despite some tensions, we

June 23, 2026

DM Rates Outlook: Tightening or Easing?

June 23, 2026 8:15 AM UTC

· With the U.S./Iran interim agreement likely to hold and energy prices softening, our projected consumer slowdown will likely tilt the Fed not to hike in H2 2026 and to actually ease by 50bps in 2027, with 25bps moves in both Q2 and Q3. With 2yr yields consistent with a hike, the tra

DM and EM FX Outlook: Cross-Currents for H2 and 2027

June 23, 2026 8:00 AM UTC

· Our baseline for the coming quarters is that global FX is moving through a period of dollar bounce and cross-current positioning adjustment, rather than a clean return to the dollar downtrend. The near-term driver is the market's (over) hawkish reading of the June FOMC/Summary of Econ

June 22, 2026

Eurozone Outlook: Has Inflation Peaked Already?

June 22, 2026 11:35 AM UTC

· Under our only slightly updated view of no further fighting in the Middle East, we see oil and gas prices largely consolidating recent falls before falling afresh from mid-2027.The current situation is very different from that of 2022 and the Ukraine War in which the EZ lost access to

Germany/France/Italy and Spain: Growth and Inflation Outlooks

June 22, 2026 10:25 AM UTC

· We have retained our 2026 GDP picture of 0.3% (Our Forecasts below) and actually pared back that for next year, with more and more signs that China is continuing to ship cheap products to Germany (lower energy prices post Iran war still help 2027). For France, we have made a 0.3% do

Equities Outlook: AI Optimism, But Caution Elsewhere in DM economies

June 22, 2026 7:05 AM UTC

· In terms of the S&P500, we remain less concerned about high valuations in the tech sector provided AI labs growth remains fast. 12mth fwd information technology are mid-range in the 2020-26 experience rather than at the highs. Even so, heavy equity issuance by tech companies and a s

June 15, 2026

U.S./Iran Interim Deal and Reopening Strait of Hormuz

June 15, 2026 12:32 PM UTC

· Our baseline (80%) is that the Strait of Hormuz will reopen in H2 2026 and remains open through 2027. However, logistics dislocation plus a switch from commercial inventory rundown to rebuilding will likely slow the decline in oil prices back towards normal levels (Figure 1). O

June 11, 2026

ECB Review: If Not Insurance, Why the Hike?

June 11, 2026 2:27 PM UTC

The 25 bp official rate hike unveiled today was so well-flagged it is hard to suggest that it is consistent with a decision process on a meeting-by-meeting basis. Similarly, the dominance of inflation upside risks, alongside another dose of optimistic real economy projections, is hardly proper dat

June 10, 2026

Financial Markets/Policymakers and the Strait of Hormuz Question

June 10, 2026 8:05 AM UTC

· Though the U.S. and Iran have attacked each other June 10, talks to reopen the straits of hormuz still continue. An Iran/U.S. agreement to reopen the Straits of Hormuz could cure the risk of a demand/supply oil market imbalance and produce some psychological relief that could knock USD

June 08, 2026

DM Government Bonds: Risks of Higher Long End Premia?

June 8, 2026 2:10 PM UTC

· Our baseline is for DM government bond yields ex Japan to remain elevated, but controlled. Japan extra risk premium is driven by BOJ QT at 6% of GDP, more than long-term debt fears. Major catalysts could drive a regime change to higher risk premia and steeper yield curves, but non

June 03, 2026

ECB Preview (Jun 11): Words Not Deeds the Focus

June 3, 2026 10:23 AM UTC

Aware of repeating ourselves (again), it is the case that the next ECB Council meeting will be more important for what is said than what is done. In fact, a 25 bp official rate hike is virtually nailed on irrespective of how events in the Middle East may fare in coming days. But the ECB comments

June 02, 2026

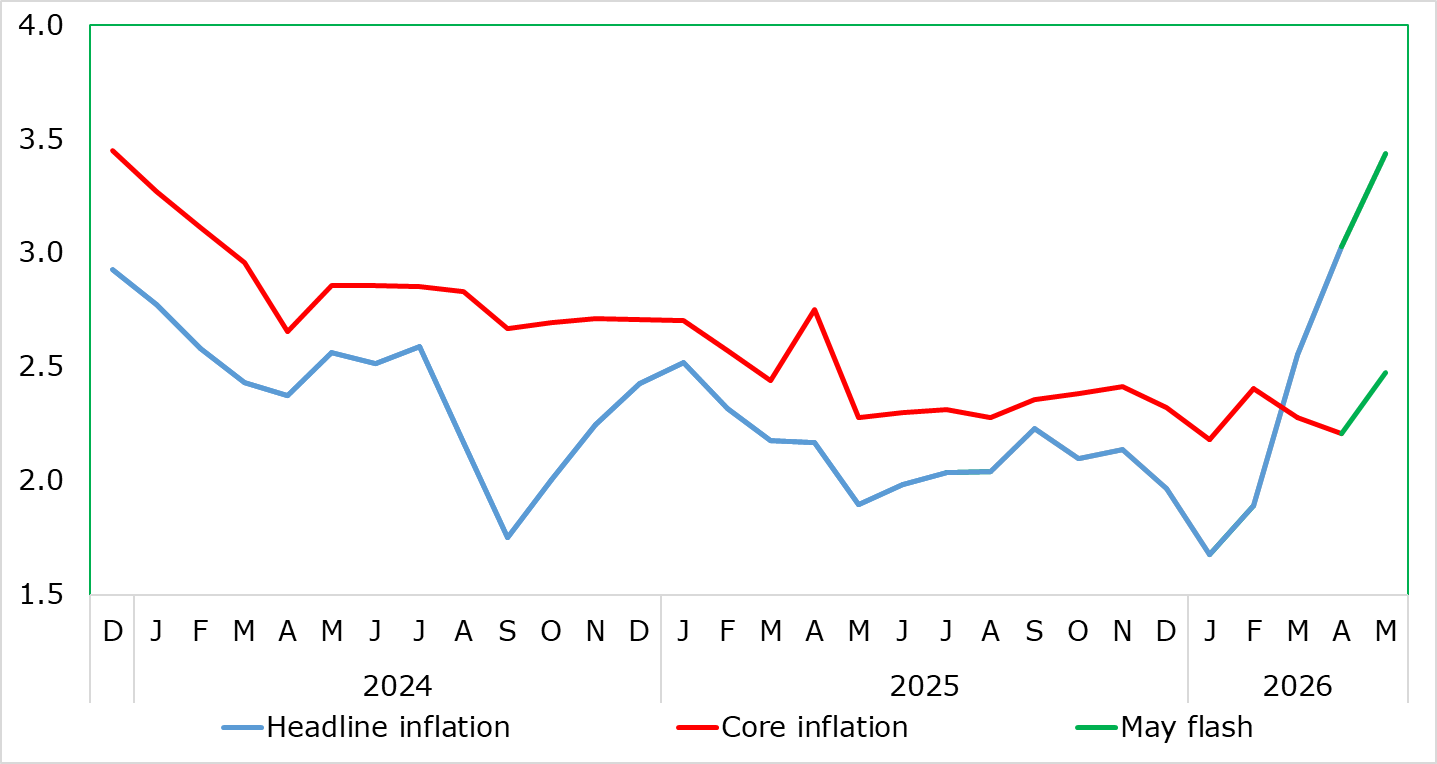

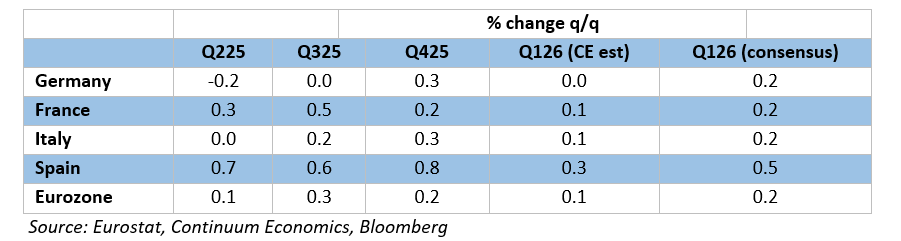

EZ HICP Review: Headline Rise Capped by Food & Energy, Services Jump Seasonal?

June 2, 2026 9:50 AM UTC

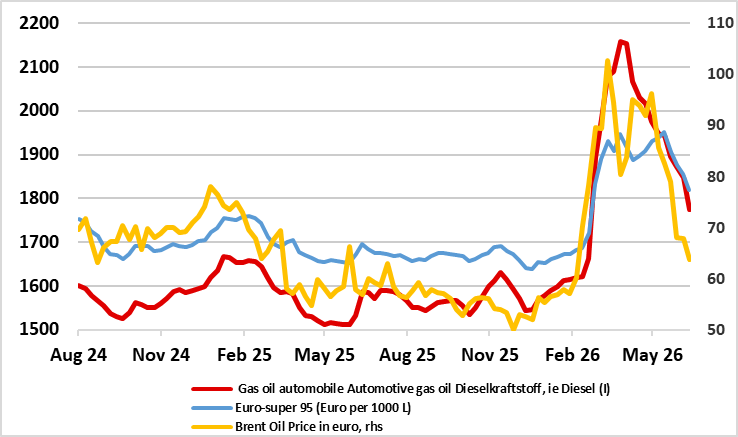

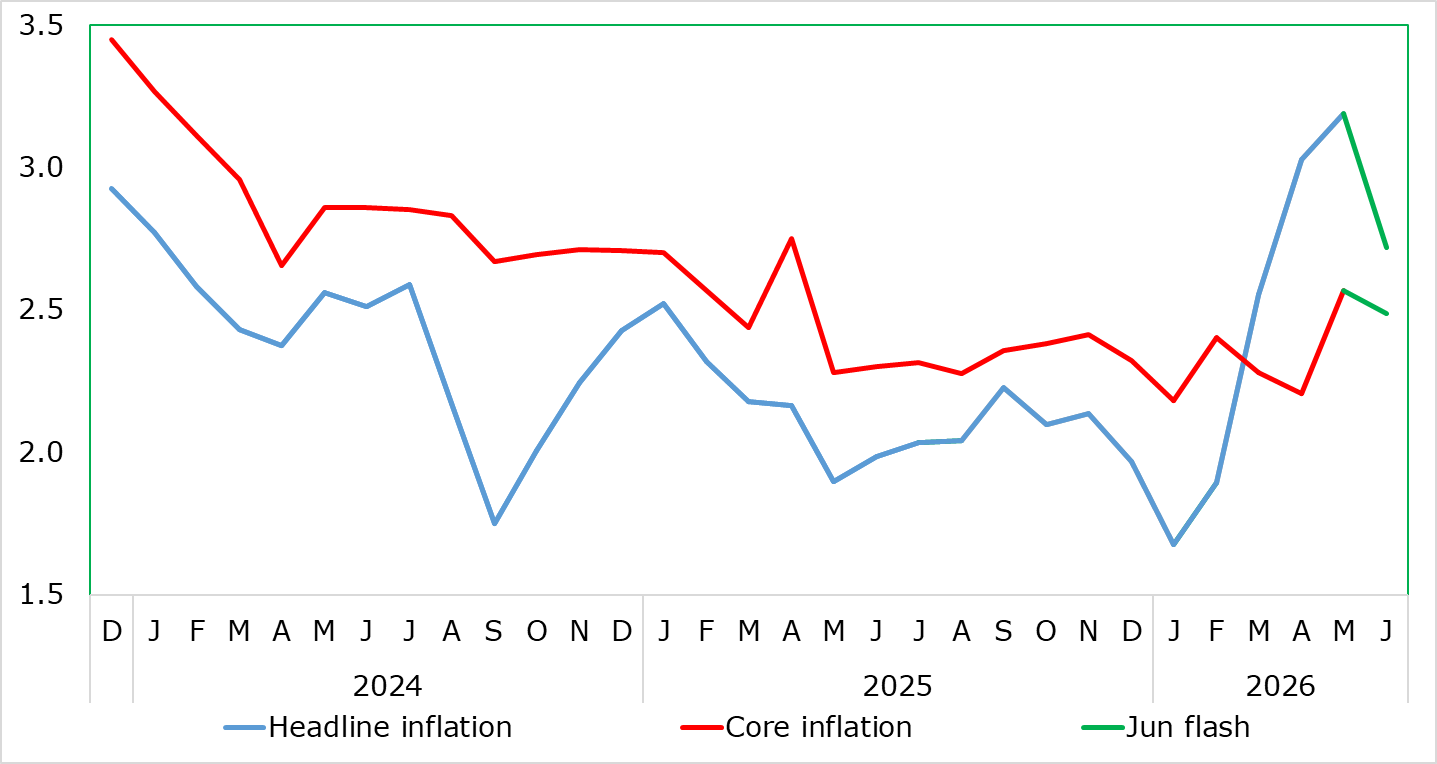

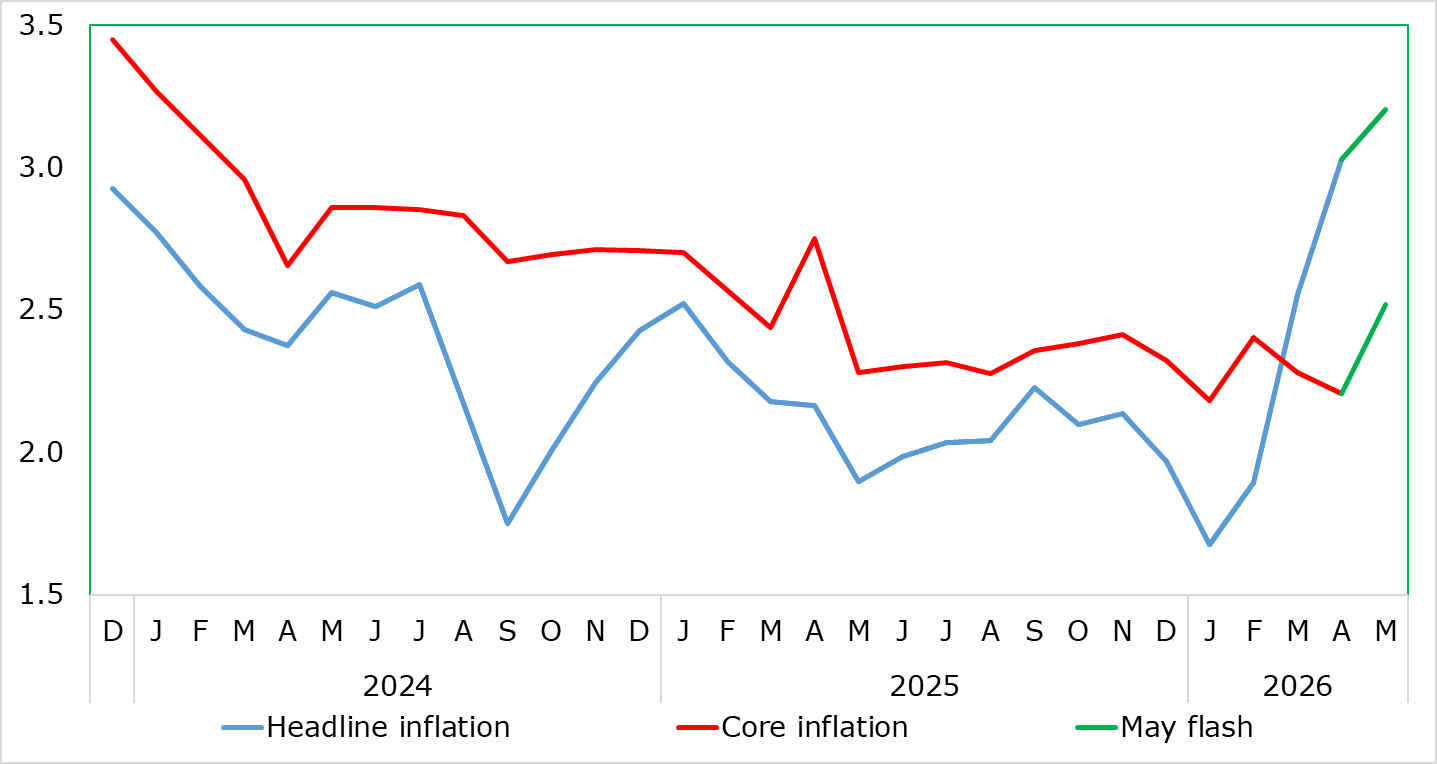

Even given what seem to be a series of reassuring aspects, the May flash HICP data is unlikely to have a material impact on ECB thinking. As expected, and helped by German fuel subsides which kept the energy rise to around zero, headline HICP rose just 0.2 ppt to 3.2%, still a 32-mth high, but whe

May 28, 2026

ECB April 30 Account: Not Willing to Look Through Energy Shock?

May 28, 2026 12:40 PM UTC

The Account of the April 30 ECB meeting offers few added clues with comments from Council member since more directly suggesting a precautionary if not pre-emptive 25 bp rate hike on June 11. As was case back then, markets are seeing two such moves by September and a strong probability of a third b

May 27, 2026

DM Government Bond Markets in Limbo

May 27, 2026 12:22 PM UTC

· DM central bank meetings in June will be crucial, with a high risk of a 25bps ECB hike to warn against 2nd round effects from higher oil prices and a BOJ 25bps hike as part of the ongoing normalisation. However, the tone that the Fed’s Warsh will set will also be key. The bigges

EZ HICP Preview (Jun 2): Headline To Surge Again as Core Starts To Rise?

May 27, 2026 9:23 AM UTC

While somewhat important, the May flash HICP data is unlikely to have a material impact on ECB thinking, irrespective of whichever way it may surprise. Most likely the data will show a further and still largely energy driven rise of 0.4 ppt, matching the April gain, but now to a 32-mth high of 3.4

May 22, 2026

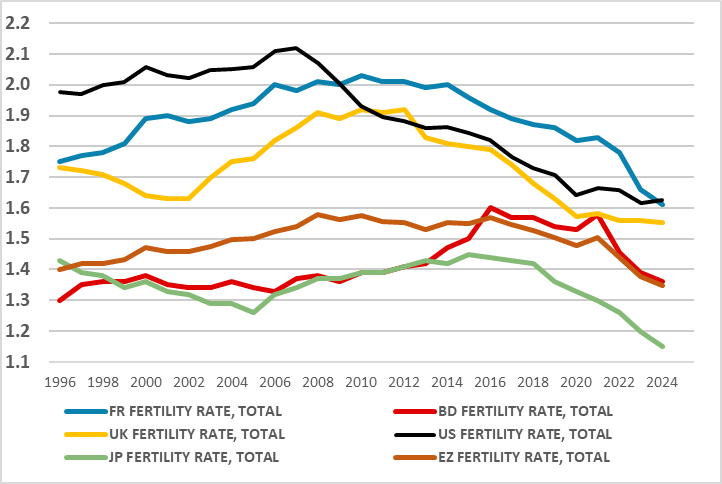

Europe: Anti-Immigration Vs More Negative Demographics

May 22, 2026 8:12 AM UTC

A significant demographic tremor is gaining speed and breadth - globally. Just as politics – certainly in the west - is framed around ending or at least reducing and controlling immigration, it seems that the populists at the helm of such thinking are not considering the ramifications of such a

May 21, 2026

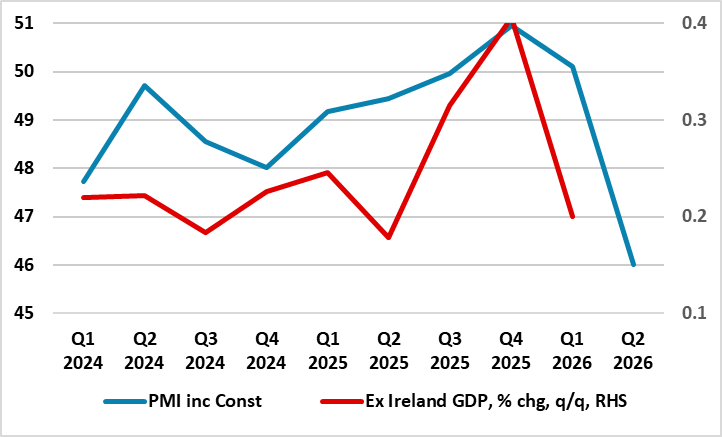

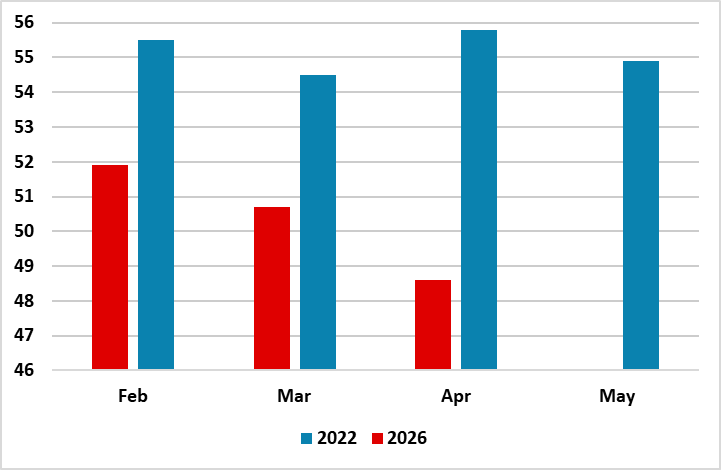

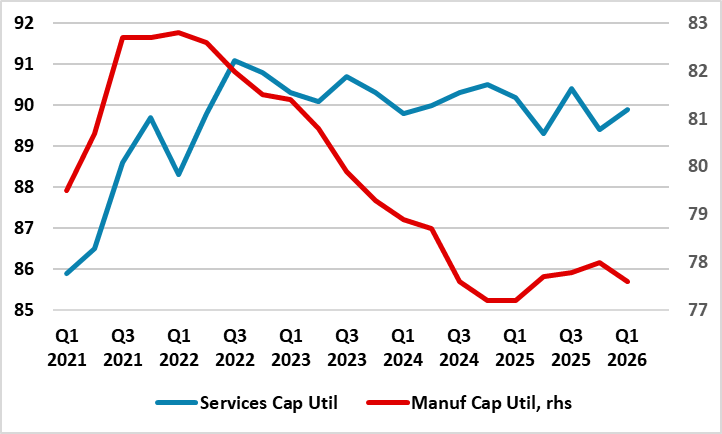

Eurozone: PMI Slump Shows Energy Surge Constraining Activity, Not Just Hitting Costs

May 21, 2026 8:36 AM UTC

Once again surprising on the downside flash Eurozone Composite PMI fell to 47.5 in May from 48.8 in April and below the 50.0 no-change mark for the second successive month. The latest reading thereby signalled a further and steeper m/m reduction in business activity, was the sharpest since October 2

May 19, 2026

ECB: Not the Only Game in Town – But A Time for Hair Shirts?

May 19, 2026 11:22 AM UTC

When hearing ECB Council policy thinking one can get the impression that it sees only a direct link from changes in its policy rate to inflation rather than the latter succumbing to a range of factors, this being the transmission mechanism. Most important of course is the economic damage that chan

May 15, 2026

Middle East Conflict: U.S. Helping Chinese Whispers?

May 15, 2026 11:26 AM UTC

In hosting President Trump this week, China feels it is vying, if not achieving, parity with the U.S. as the world’s superpowers; from China’s perspective, it regards Russia similarly. It does seem as if China’s goal at this summit was to get more effective flexibility in shaping Taiwan’

May 08, 2026

Eurozone: In Dire Straits?

May 8, 2026 10:55 AM UTC

Amid all the concern about the energy-induced surge in inflation resulting from the Middle East conflict, the impact on EZ real economy looks to be sizeable and growing. High profile PMI numbers are flashing alarmingly, but the message from the April composite (at a 17-mth low) may actually be not

April 30, 2026

ECB Review: ECB Mixed Communications

April 30, 2026 2:01 PM UTC

· Overall, the June and July meetings have live risks that the ECB could undertake a modest 25bps hike. If a partial reopening of the Straits of Hormuz occurs then the ECB will likely keep hawkish, but not actually hike. We feel that the ECB is overestimating natural gas prices, whi

Eurozone GDP & HICP Review: Fragile Resilience?

April 30, 2026 9:30 AM UTC

We continue to be critical of the ECB assertion (at least before the Iran War) that the EZ economy was in a ‘good place’. This to us was too backward looking and amid some signs in both hard, soft and monetary data, that the economy going into the last quarter was soft and fragile. Indeed, f

April 29, 2026

April 28, 2026

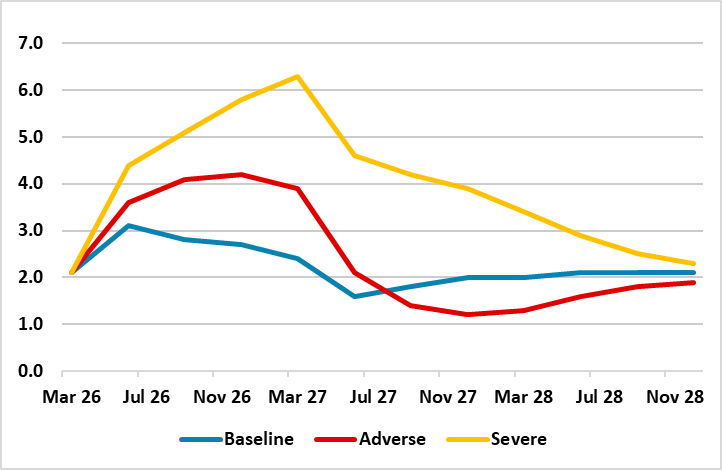

Eurozone: Even Tighter Corporate Credit Standards Continues and More Loans Applications Rejected

April 28, 2026 8:51 AM UTC

Given the ever clearer fall-out from the conflict in the Gulf, it was hardly a surprise of even tighter credit standards (Figure 1), thereby merely accentuating trends in the four previous Bank Lending Surveys (BLS). At least as far as firms and especially consumers seeking credit are concerned, t

April 27, 2026

Straits of Hormuz Standoff and Mixed Markets

April 27, 2026 9:02 AM UTC

• Equities longer time horizon means that they are hoping for a reopening of the Straits of Hormuz (though also being helped by renewed AI optimism), whereas government bond markets actually want to see tangible progress and an associated tempering of DM central banks posturing. This dive

April 23, 2026

ECB Preview (Apr 30): Real Economy Buckling Already!

April 23, 2026 12:21 PM UTC

We again expect no change from the ECB on Apr 30, but President Lagarde will probably have to admit in the Q&A that unlike last time the decision was not unanimous. Overall, the communication will again suggest upside risks for inflation and downside risks for economic growth the extent and durati

April 22, 2026

Iran Conflict – Who Has the ‘Trump’ Card

April 22, 2026 9:17 AM UTC

When Trump aspires to reaching a deal, he thinks in either black or white. But whether it be political, economic or military the reality is that the world is always various shades of grey. This is very much evident in the way the Iran conflict was planned by the U.S. – the expected clear and r

April 21, 2026

EZ HICP Preview (Apr 30): Headline Surges Again as Core Stabilises?

April 21, 2026 9:29 AM UTC

The first of the Iran War induced rise in prices arrived with the final March HICP data in line with expectations, as the headline rate spiked higher to 2.6% from February’s 1.9%, but with the core rate falling back (Figure 1) underscoring that this March surge was purely energy-led. Indeed, thi

April 20, 2026

Eurozone Flash GDP Preview (Apr 30): Softer Even Before Iran Conflict?

April 20, 2026 1:20 PM UTC

We have been critical of the ECB assertion (at least before the Iran War) that the EZ economy was in a ‘good place’. This to us was too backward looking and amid some signs in both hard, soft and monetary data, that the economy going into the last quarter was slowing. Indeed, part of a broad

April 17, 2026

Equities: Still a Rocky Road in 2026

April 17, 2026 12:49 PM UTC

· Any deal between the U.S. and Iran would still be seen as a positive win in equities, as it would raise hopes that it could be followed by a multi-year settlement that could include more Iran oil and gas into the global energy markets and lower energy prices. No deal is also feasible,

April 16, 2026

Eurozone; ECB Tone More Neutral Than Suggested by March Meeting Market Reaction?

April 16, 2026 12:18 PM UTC

Little new can be taken from the minutes to the March ECB Council 19 meeting, save that at least to us the ECB was too optimistic about growth and too pessimistic about inflation. In regard to the latter, while acknowledging tighter financial conditions, the ECB still seemed to be downplaying what a

April 15, 2026

DM Central Bank Signals Awaited

April 15, 2026 12:12 PM UTC

· Fed/ECB and BOE meetings will likely see concern over the potential 2nd round inflation effects from the Iran war, but forecasts seeing inflation coming down in 2027 and no imminent signals of tightening from the ECB/BOE – our baseline remains for easing later in the year, as energy

April 14, 2026

Eurozone: ECB Downplaying Supply of Credit as it Focuses on its Cost

April 14, 2026 1:35 PM UTC

Even amid increasing suggestions that the Middle East conflict will reap marked real economy damage that should limit the length and extent of any inflation surge, markets are still pricing in almost three 25 bp ECB hikes in the coming year. We think this is still very excessive and reflects an ou

April 08, 2026

Eurozone: Manufacturing Seeing Excess Supply Not Excess Demand

April 8, 2026 11:13 AM UTC

In Europe generally, but especially in the EZ, it will be manufacturing that will bear the brunt of the recent jump in energy prices, where industrial electricity prices even before the conflict started were among the highest globally. While high energy costs affect all sectors, manufacturing’s re

2-Week Ceasefire, Then?

April 8, 2026 10:09 AM UTC

· The ceasefire will likely involve a new normal of shipping companies paying Iran a toll. While this is adding a cost to Gulf crude oil/products and LNG, the premium will be a lot lower than the cost of an ongoing war. The U.S. and Iran will now likely be reluctant to restart the w

April 01, 2026

Eurozone Labor Market: A Structural and Disinflationary Shift?

April 1, 2026 10:00 AM UTC

That we think the ECB is being optimistic about the real economy and labor market outlook is almost an understatement made all the more so since the outbreak of the Iran War. In the ECB’s latest baseline scenario, recession is clearly avoided and the jobless rate, while revised a little higher (

March 31, 2026

EZ HICP Review: Headline Surges as Core Slips Back?

March 31, 2026 9:44 AM UTC

The first of the Iran War induced rise in prices has arrived but with the flash March HICP data a little below expectations, both the consensus and that of the ECB. Instead, the headline rate spiked higher to 2.5% from February’s 1.9%, but with the core rate falling back (Figure 1) underscoring

March 30, 2026

Markets: Short vs Long Iran War

March 30, 2026 8:00 AM UTC

· For a 4-8 week war and 3-4 quarters of energy price normalisation, we see a 10% U.S. equity market correction in H1 2026 driven by the current Iran war and/or consumption slowing due to lower (real) wage growth, alongside still stretched valuations in equity and equity-bond terms. T

March 27, 2026

March 26, 2026

EZ HICP Preview (Mar 31): Headline to Surge but Core to Slip Back?

March 26, 2026 1:54 PM UTC

The first of the Iran War induced rise in prices arrive in the coming week with flash March HICP data. We see the headline rate spiking higher to 2.6%-2.7 from February’s 1.9%, the former largely chiming with that implied ECB thinking from the latter’s recent updated projections. But both it

March 25, 2026

DM FX Outlook: The Rest of 2026

March 25, 2026 7:55 AM UTC

Our baseline is for a 4-8 week Iran war, with WTI down to USD80-85 by June; USD65-70 end 2026 and USD60 by Q3 2027. This should see the USD return to a weaker profile later in the year. In our December Outlook, our favorites were the AUD and NOK based on yield spreads, but it is also worth noting th

March 24, 2026

Eurozone Outlook: Conflicts of Interest

March 24, 2026 9:55 AM UTC

· Under our more likely view of limited further fighting in the Middle East, we see oil and gas prices largely falling back to the pre-war levels within a year, with the current situation very different from that of 2022 and the Ukraine War in which the EZ lost access to Russian gas as