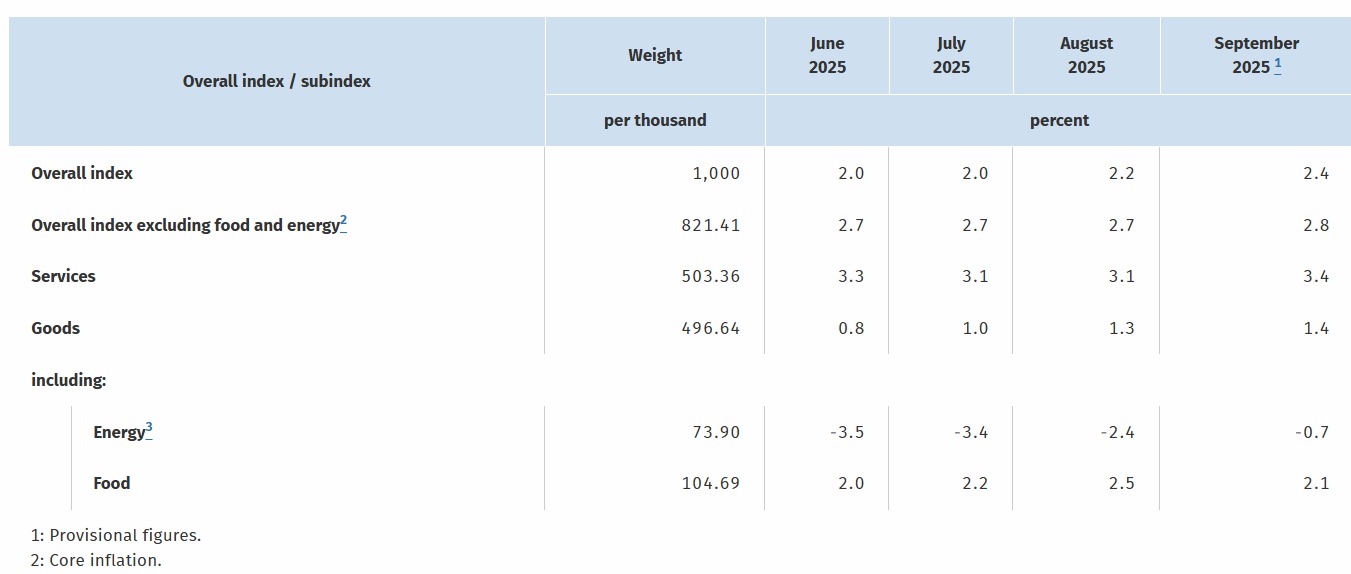

German HICP Review: Headline Higher And Core Rises Due to Fresh Services Push?

Germany’s disinflation process hit a further more-than-expected hurdle in September, as the HICP measure rose 0.3 ppt for a second successive month, thereby even more clearly up from July’s 1.8% y/y, that having been a 10-mth low (Figure 1). This (again) occurred largely due to energy base effects but with service prices also contributing slightly – breaking a softening trend for the latter. The result was that the CPI core edged up a notch to 2.8% (The HICP core probably rose similarly). Regardless core adjusted data are telling a more reassuring tale (Figure 2). But with clear (also largely energy but some service pressure) gains seen in France and other countries, the EZ HICP data (due Oct 1) is now likely to show steeper gain than previously thought, ie 0.2-0.3 ppt!

Figure 1: German HICP Inflation Moves Further Above Target?

Source: German Federal Stats Office, % chg y/y

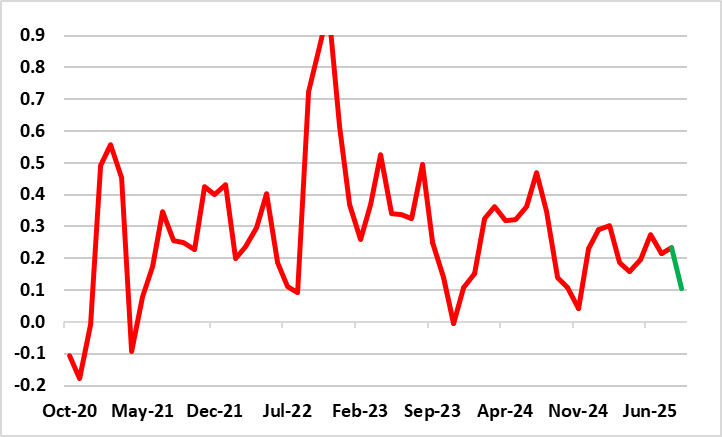

The German August and now September data were again bolstered by energy prices – mainly due to fuel prices having dipped more this time last year than this year. Indeed, such base effects should now start to unwind and a fresh fall resumes in Q4! The question is how aberrant id the seemingly vacation induced rise in services inflation – this all the more puzzling given survey and wage data suggesting a still weakening trend

Regardless, perhaps continued disinflation news is evident in adjusted m/m data which have shown some fresh downtick in core rates even though this does not seem to have proceeded discernibly further in the August numbers. But, we think the September HICP details will verify this with a core reading just above zero in adjusted m/m terms (Figure 2).

Figure 2: German Adjusted HICP Core Rate Drop to Resume?

Source: German Federal Stats Office, CE, % chg m/m seasonally adjusted and smoothed

We still see German HICP inflation moving back below 2% by year end with the October numbers likely to unwind this September rise.

I,Andrew Wroblewski, the Senior Economist Western Europe declare that the views expressed herein are mine and are clear, fair and not misleading at the time of publication. They have not been influenced by any relationship, either a personal relationship of mine or a relationship of the firm, to any entity described or referred to herein nor to any client of Continuum Economics nor has any inducement been received in relation to those views. I further declare that in the preparation and publication of this report I have at all times followed all relevant Continuum Economics compliance protocols including those reasonably seeking to prevent the receipt or misuse of material non-public information.