EZ HICP Review: Headline Inflation Moves Higher as Services Ticks Up From Cycle-low

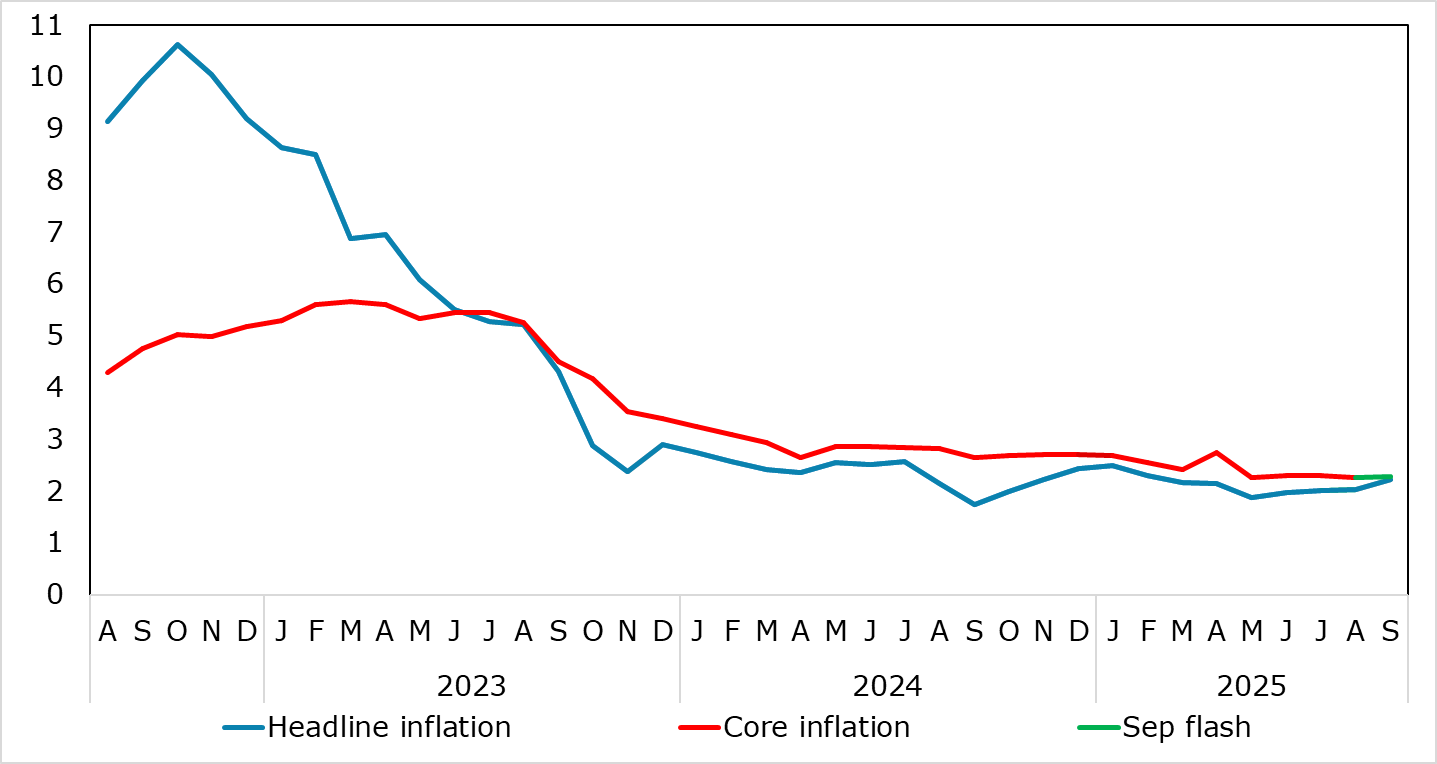

A second successive upside surprise is unlikely to make inflation any more of an issue for the ECB at present. Instead, moderate concerns whether the apparent resilience of the real economy may yet falter should remain the order of the day, this possibly a result of a still somewhat unresponsive transmission mechanism (effective borrowing rates have failed to match the drop in the ECB policy rate). This mindset will not be altered by the flash HICP data for September even given the further but largely as-expected 0.2 ppt rise in the headline to 2.2% (Figure 1), not least as this still implies that the ECB’s Q3 projection for both the overall and core figures in Q3 were met. This rise in the headline was again food and (largely) energy base effect driven but also with services, almost solely due to travel related base effects. But highlighting still soft core inflation, adjusted m/m data (Figure 2) still show reassuring signs while supply pressures still seem abated also offering signs that underlying inflation is no worse than in line with target, if not lower (Figure 3).

Figure 1: Headline Moves Further Above Target as Core and Services Edge Up

Source: Eurostat, CE

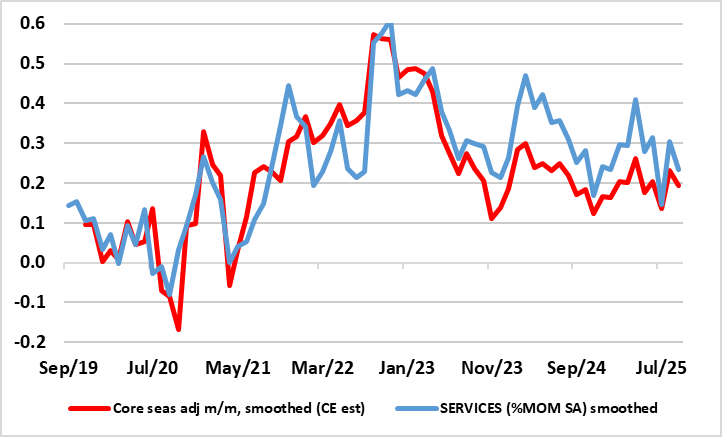

In contrast to food inflation in neighbouring economies, that for the EZ seems under control, actually slipping back despite some adverse weather of late. Admittedly, services inflation, at 3.2% in September, moved up a bare 0.1 ppt from what was the lowest since March 2022 but despite this rise, it not only matches ECB thinking for the last quarter but still seems to be belatedly following in the footsteps of lower wage pressures and where survey data for the sector also shows weaker price pressures. As a result, this trend and noise could bring the headline and core rate could both dip below 2% in Q4 with base effects pulling the headline down toward 1.7% in Q1, especially if demand weakness starts to accentuate what have largely been supply factors driving the disinflation process hitherto (see below). Notably, as recent calendar distortions unwind, what has looked like fresh price pressures in seasonally adjusted short-term m/m movements for core and services have reversed and are consistent with on-target inflation (Figure 2)!

Figure 2: Core and Services Inflation Around Target in Shorter-Term Dynamics?

Source: Eurostat, ECB, CE, smoothed = 3-mth mov avg

Supply or Demand?

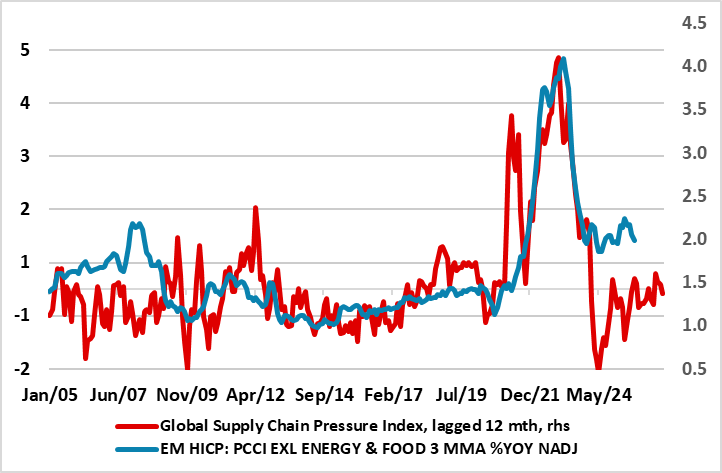

The relevance of demand vs supply in inflation dynamics is resurfacing and was mentioned in a speech in Jackson Hole by President Lagarde and again in a speech yesterday when she discussed shocks This is still a topic of big debate and disagreement, partly depending upon what part of the global economy one is more guided by. Indeed, economists at the IMF influenced more by matters-USA seem to think that inflation has been demand driven while an ECB paper suggests the opposite - as does Lagarde. Indeed, the ECB paper notes that ‘shocks linked to global supply chains and to gas prices have exhibited a much larger influence than in the past. Overall, supply shocks can explain the bulk of the post-pandemic inflation surge, also for core inflation’. This is backed up by measures of supply side pressures such as that compiled by the NY Fed. Its monthly aggregate (its so-called Global Supply Chain Pressure Index) has stopped falling but has done so only back to levels that were seen prior to the pandemic and which also suggest supply factors may yet have a further impact on EZ underlying Inflation (Figure 3).

Figure 3: Reduced Supply Pressures Largely Responsible for Softer Inflation So Far?

Source: ECB, Federal Reserve Bank of New York, Global Supply Chain Pressure Index, CE

This latter view is one with which we agree and can provide evidence to substantiate. Notably ECB Chief Economist Lane has very much underscored that the Persistent and Common Component of Inflation (PCCI) is the best predictor of inflation one and two years ahead and this is all the more notable as this measures have eased back to 2% of late. Given that it perhaps the best measure of price persistence, it is adding to arguments that lingering worries about price resilience are overdone, albeit at the same time suggesting that clear disinflation may have largely run its course.