Continuum Daily

View:

July 03, 2026

EM Government Debt Sinners and Saints

July 3, 2026 1:05 PM UTC

· Overall, the clearest EM fiscal sinner is Brazil, given its tax revenue/GDP ratio is already very high and requires politically sensitive expenditure cuts after the October election to increase the primary surplus to stabilize the government debt/GDP trajectory and get real bond yield

July 02, 2026

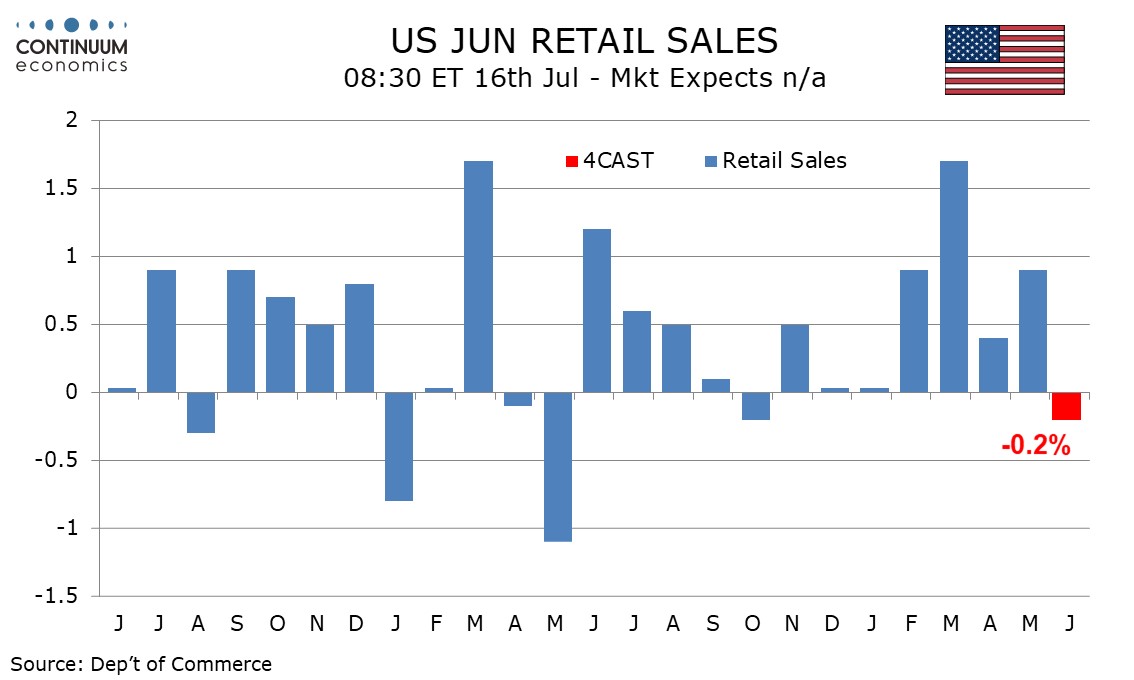

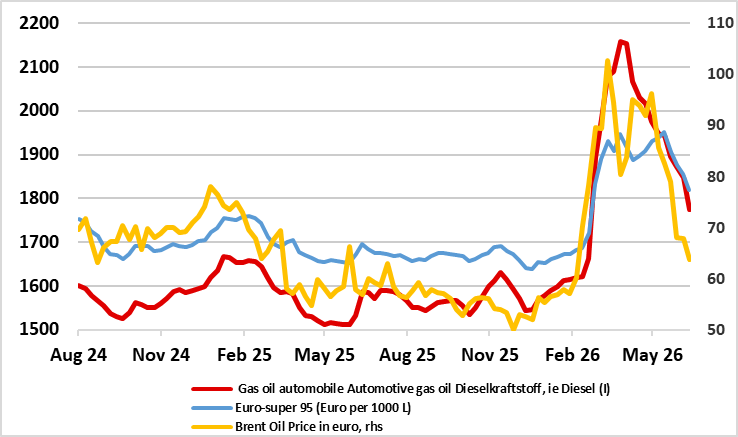

Preview: Due July 16 - U.S. June Retail Sales - Softer on gasoline, only modest underlying slowing

July 2, 2026 5:33 PM UTC

We expect June retail sales to fall by 0.2% overall and 0.4% ex autos, though with a 0.2% rise ex auto and gasoline. Even the latter would be the slowest gain since a flat December 2025.

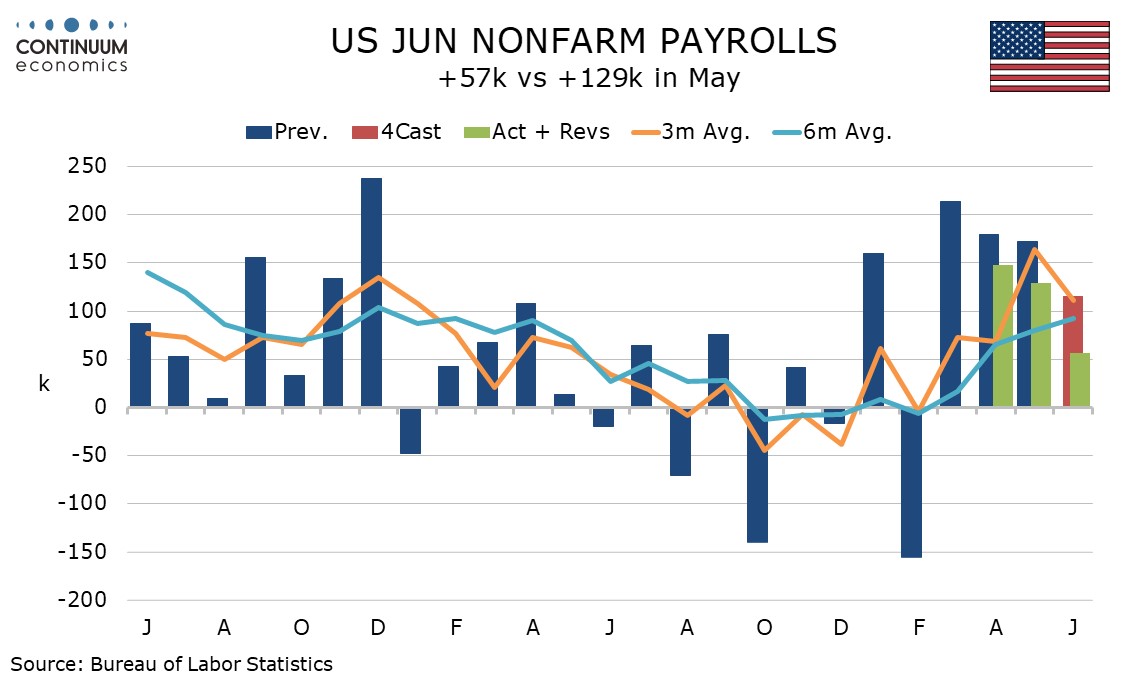

U.S. June Employment - Upside May surprise offset, but unemployment falls on lower labor force

July 2, 2026 1:20 PM UTC

June’s non-farm payroll is weaker than expected with a 57k increase, 49k private, with downward revisions to April and May. The slowing is consistent with an upturn in the initial and continued claims trends, though both were almost unchanged (-1k to 215k and +2k to 1.814m respectively) in the l

U.S. June Employment - Upside May surprise offset, but unemployment falls on lower labor force

July 2, 2026 1:12 PM UTC

June’s non-farm payroll is weaker than expected with a 57k increase, 49k private, with downward revisions to April and May. The slowing is consistent with an upturn in the initial and continued claims trends, though both were almost unchanged (-1k to 215k and +2k to 1.814m respectively) in the l

July 01, 2026

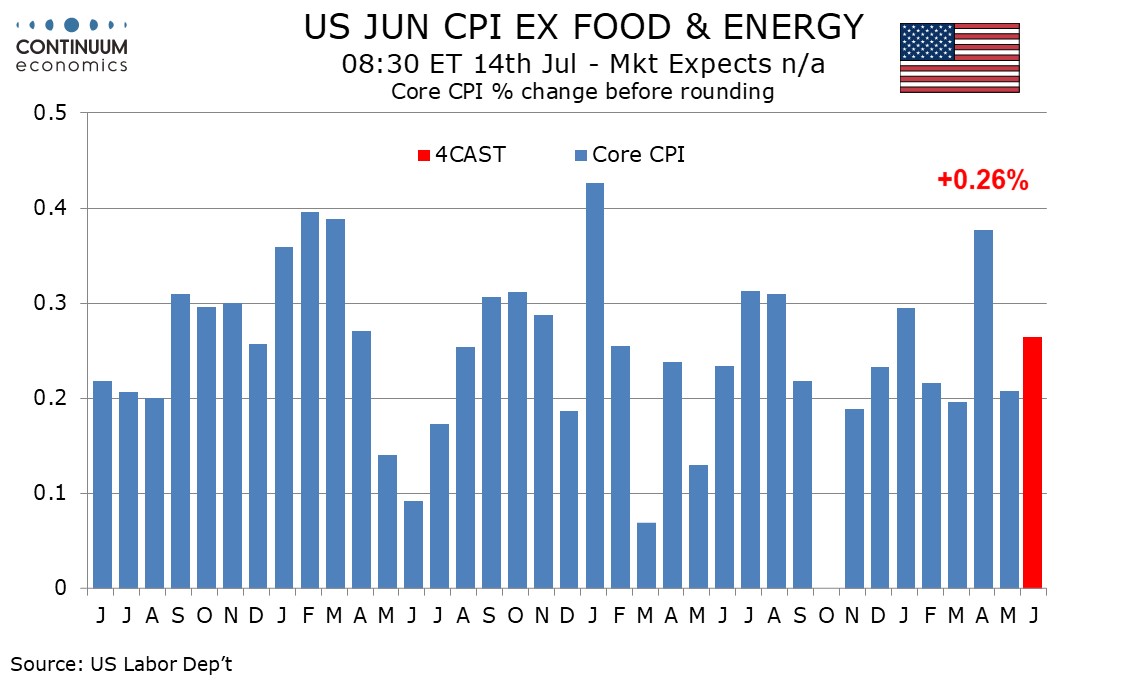

Preview: Due July 14 - U.S. June CPI - Energy to correct lower, World Cup to support core

July 1, 2026 3:18 PM UTC

We expect June CPI to be unchanged overall as energy corrects from three straight strong gains while the core rate ex food and energy sees a slightly firmer 0.3% increase. Before rounding we expect respective outcomes of -0.02% and up 0.26%, with the World Cup having just enough impact to nudge the

EZ HICP Review: Absence Second-Round Effects Continues

July 1, 2026 1:42 PM UTC

Contrary to some thinking, EZ HICP inflation continues to behave, both absolutely and relatively – ie to what looks ever excessive ECB price thinking. The question must be if and when the ECB chooses to note friendlier price and costs signals, rather than pander to the upside prices risks that o

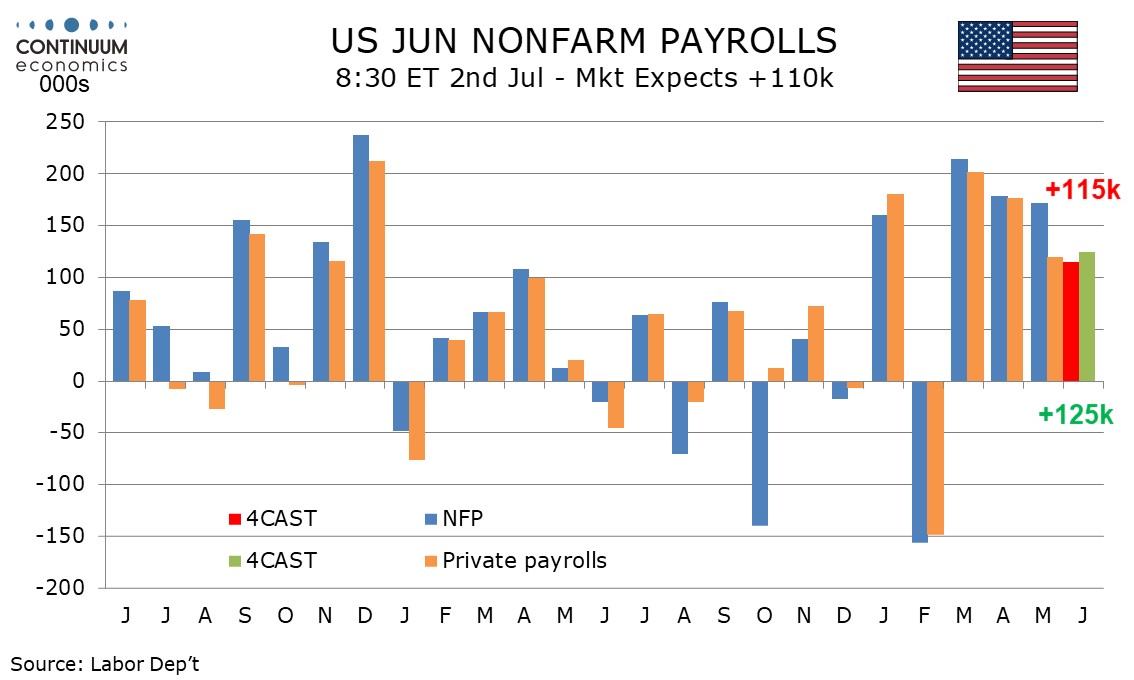

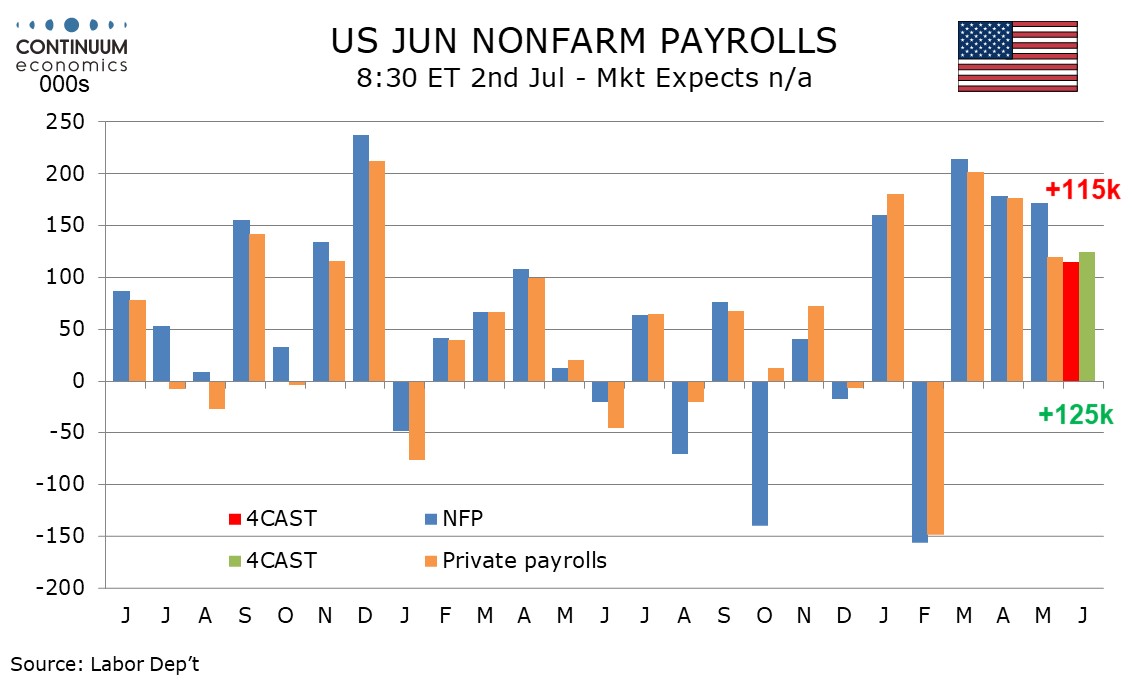

Preview: Due July 2 - U.S. June Employment (Non-Farm Payrolls) - World Cup boost versus underlying slowing

July 1, 2026 12:47 PM UTC

We expect June’s non-farm payroll to rise by 115k overall and by 125k in the private sector, the former a slowing from 172k in May but the latter marginally stronger than May’s 120k increase. We expect the unemployment rate to remain at 4.3% for a fourth straight month and an in line with trend

EZ HICP Review: Absence Second-Round Effects Continues

July 1, 2026 10:41 AM UTC

Contrary to some thinking, EZ HICP inflation continues to behave, both absolutely and relatively – ie to what looks ever excessive ECB price thinking. The question must be if and when the ECB chooses to note friendlier price and costs signals, rather than pander to the upside prices risks that o

Macro and Market Implications of 'Super' El Nino Risks

July 1, 2026 8:08 AM UTC

El Nino, and a potentially severe one, is increasingly looking like a central scenario rather than a tail risk for 2026-27.

2026-27 El Nino is shaping up to be strong enough to matter, at least for scenario planning.

The key facts are broadly: Australia, New Zealand, Indonesia and South Africa are l

June 30, 2026

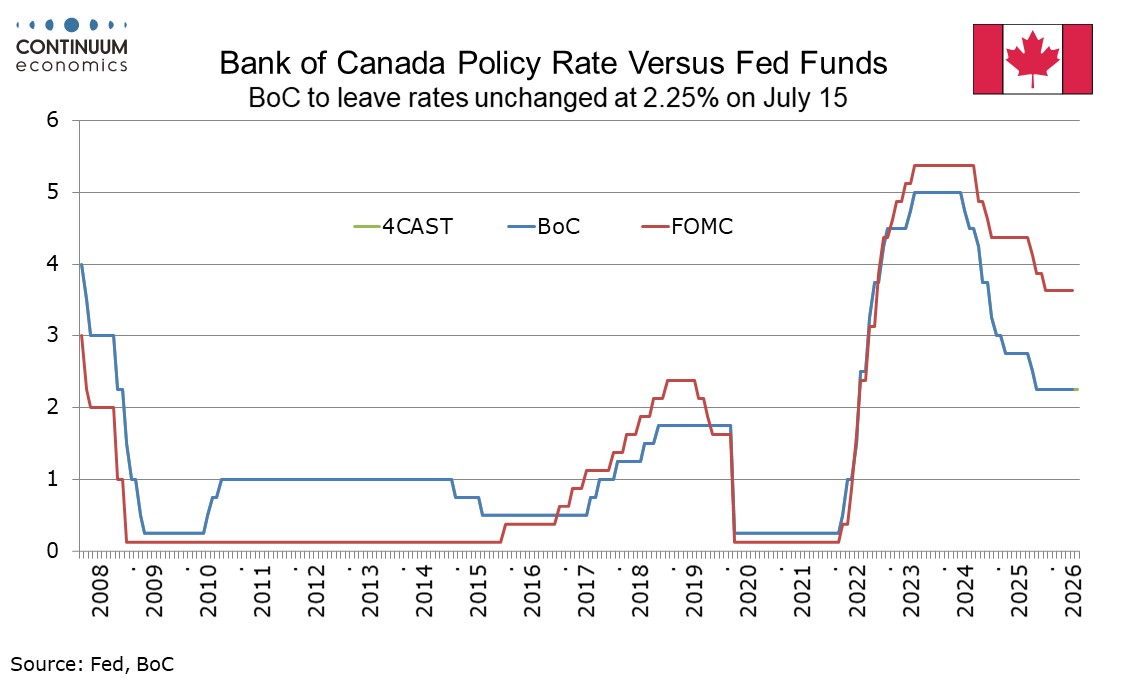

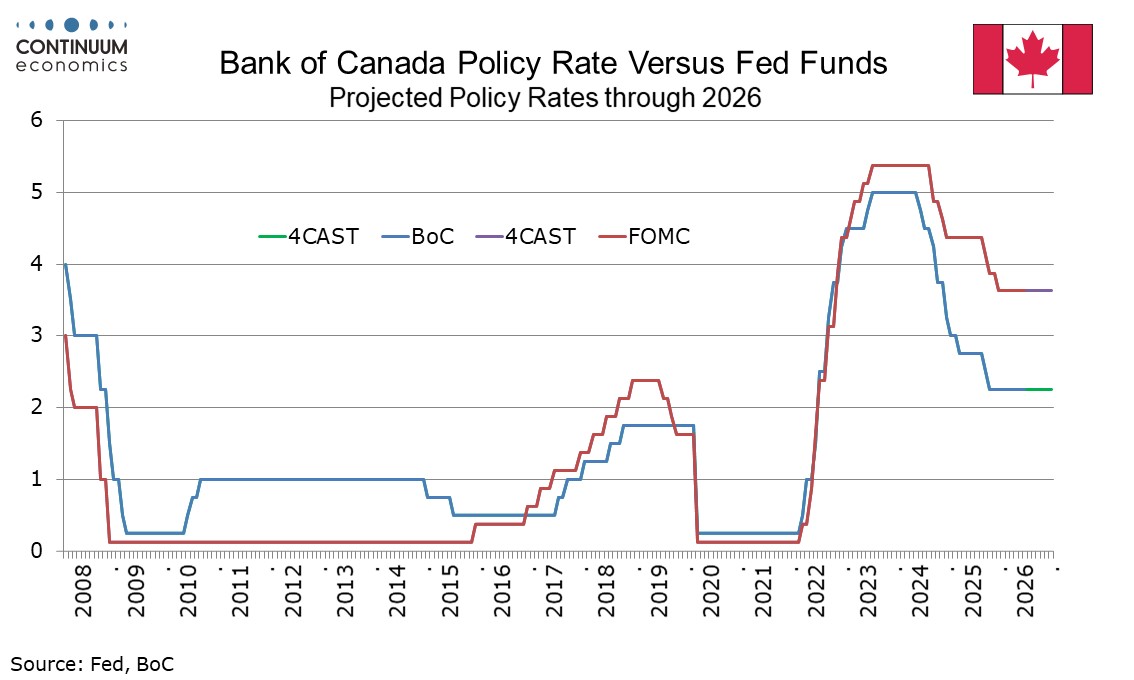

Bank of Canada Preview for July 15: Reduced energy risk may see more attention on trade

June 30, 2026 5:35 PM UTC

The Bank of Canada meets on July 15 and looks set to leave rates unchanged at 2.25%. The meeting will take place with inflationary risks coming from the Middle East having faded somewhat and escalation of trade tensions with the US a significant risk. This could lead to a dovish lean to the statemen

UK GDP Outlook Update – Still Fragile With Surveys Negative

June 30, 2026 4:13 PM UTC

It is the relative norm for an economy to be offering disparate signals at any one juncture, if not actual conflicting ones. This is certainly the case in the UK currently, where upbeat Q1 GDP data of 0.6% q/q have been, confirmed and notably by a perkier consumer. Such shots of real growth ar

AI Boom and Bust?

June 30, 2026 10:45 AM UTC

• While some are becoming wary that AI bust could arrive in coming quarters, AI labs revenue growth has been explosive and this sustains the vertical chain of datacenter demand and commitments for the hyperscalers and also buoyant semiconductor demand. For 2027 and 2028 capital markets re

June 29, 2026

China Yuan to 6.65 Then 6.50?

June 29, 2026 7:10 AM UTC

· We feel that the authorities will pause appreciation at times via FX intervention, but then allow appreciation to restart. We now see further Yuan appreciation to 6.65 by end 2026, though the authorities will be reluctant to see much more. For end 2027 we forecast USDCNY at 6.50

June 26, 2026

ECB Sin(a)tra Preview: Should the ECB Only Consider My Way?

June 26, 2026 1:29 PM UTC

The speed and manner in which the ECB adopted a hawkish stance is response to the Middle East conflict was no surprise; it has many precedents, some of which have led to policy errors which we think may be being repeated at this juncture. Indeed, despite friendlier price and costs signals, the ECB

Turkiye Inflation Preview: CPI is Expected to Slightly Increase in June

June 26, 2026 12:37 PM UTC

Bottom line: After standing at 32.6% annually in May, we expect consumer price index (CPI) will slightly surge to around 32.8%-33.0% y/y in June due to secondary impacts of the energy price shocks stemming from Middle East tensions. June print will be announced by Turkish Statistical Institute (TU

Mexico: Banxico Pause, But MXN and USMCA Renegotiations

June 26, 2026 7:04 AM UTC

· As expected Banxico left the policy rate unchanged at 6.50%, with the focus now on the lagged benefit of easing and also what will happen with the USMCA negotiations. Banxico will likely keep the current policy rate through end 2026, given concerns that the Fed could tighten – eve

June 25, 2026

Preview: Due July 2 - U.S. June Employment (Non-Farm Payrolls) - World Cup boost versus underlying slowing

June 25, 2026 7:12 AM UTC

We expect June’s non-farm payroll to rise by 115k overall and by 125k in the private sector, the former a slowing from 172k in May but the latter marginally stronger than May’s 120k increase. We expect the unemployment rate to remain at 4.3% for a fourth straight month and an in line with trend

June 24, 2026

Bank of Canada Minutes from June 10 - Balanced tone, and energy risks have fallen since the meeting

June 24, 2026 7:24 PM UTC

Minutes from the Bank of Canada meeting from June 10 do not provide many surprises, but confirm a fairly balanced tone that was evident after the meeting. The balanced tone does not however mean that policy will remain on hold, with high uncertainty meaning that risks could shift and the BoC agree

June 23, 2026

Preview: Due July 2 - U.S. June Employment (Non-Farm Payrolls) - World Cup boost versus underlying slowing

June 23, 2026 6:31 PM UTC

We expect June’s non-farm payroll to rise by 115k overall and by 125k in the private sector, the former a slowing from 172k in May but the latter marginally stronger than May’s 120k increase. We expect the unemployment rate to remain at 4.3% for a fourth straight month and an in line with trend

June 22, 2026

Eurozone Outlook: Has Inflation Peaked Already?

June 22, 2026 11:35 AM UTC

· Under our only slightly updated view of no further fighting in the Middle East, we see oil and gas prices largely consolidating recent falls before falling afresh from mid-2027.The current situation is very different from that of 2022 and the Ukraine War in which the EZ lost access to

Germany/France/Italy and Spain: Growth and Inflation Outlooks

June 22, 2026 10:25 AM UTC

· We have retained our 2026 GDP picture of 0.3% (Our Forecasts below) and actually pared back that for next year, with more and more signs that China is continuing to ship cheap products to Germany (lower energy prices post Iran war still help 2027). For France, we have made a 0.3% do

Equities Outlook: AI Optimism, But Caution Elsewhere in DM economies

June 22, 2026 7:05 AM UTC

· In terms of the S&P500, we remain less concerned about high valuations in the tech sector provided AI labs growth remains fast. 12mth fwd information technology are mid-range in the 2020-26 experience rather than at the highs. Even so, heavy equity issuance by tech companies and a s

June 19, 2026

CBR Extends Easing Cycle but Slows Pace Amid Global Inflation Risks

June 19, 2026 6:23 PM UTC

Bottom Line: Following 50 bps rate cut on April 24—driven by the disinflationary trend in H1— the Central Bank of Russia (CBR) extended its easing cycle on June 19. However, the bank opted for a smaller 25-basis-point reduction, lowering the key rate from 14.5% to 14.25% citing mounting global i

Brazil: Slowing Pace of Cuts and BRL Strength

June 19, 2026 6:55 AM UTC

· Brazil cut the SELIC by 25bps to 14.25%, but received critiques from the market by raising end 2027 CPI inflation from 3.5% to 3.7% and talking about Q1 2028 in the relevant policy horizon. We feel that BCB still wants to leave the door open to further cuts in 2026, given how restrict

June 18, 2026

BOE: Gang of 6 and Steady 2026 Rates

June 18, 2026 11:27 AM UTC

Though Megan Greene joined Huw Pill in calling for a one off 25bps risk management hike, 6 MPC members feel that disinflation is showing through and a soft economy and labor market warrants waiting to see energy prices and potential 2nd round effects. This gang of 6 also feels that markets have ti

Fuel and Transportation Costs Pushed South African Inflation to 4.5% in May

June 18, 2026 10:25 AM UTC

Bottom Line: South Africa’s annual inflation climbed to 4.5% in May driven by surging fuel and transport costs, according to StatsSA's announcement. The core inflation surged to 3.8% y/y in May from 3.6% in the previous month, marking the highest reading since October 2024. While we anticipate tha

Norges Bank Review (Jun 18): Higher Rates Then Down?

June 18, 2026 8:23 AM UTC

The June Norges bank statement had a hawkish bias with a higher policy rate profile than in March MPR (Figure 1) and concerns voiced again over persistent domestic inflation pressures. The Norges bank appear ready to move in September or November. However, the Iran/U.S. deal impact on energy pri

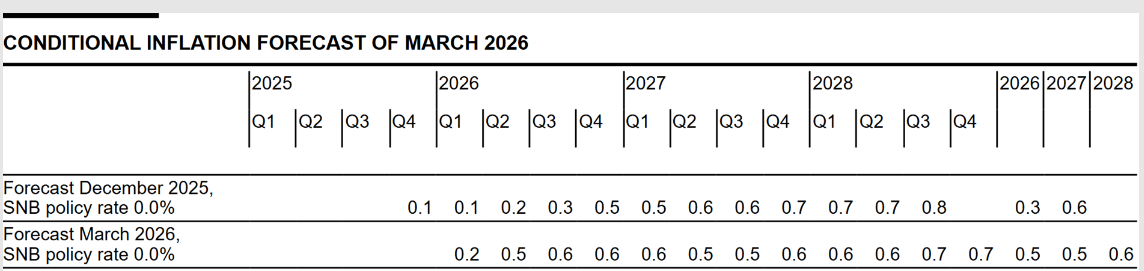

SNB: Holding Steady on Rates

June 18, 2026 7:54 AM UTC

The June quarterly assessment saw little shift in the forecasts for either growth or inflation (Figure 1), with the tone of the economic outlook remained guarded due to concerns over the Iran war on the global economy (forecasts though look to have been completed before the U.S. Iran deal). With

June 17, 2026

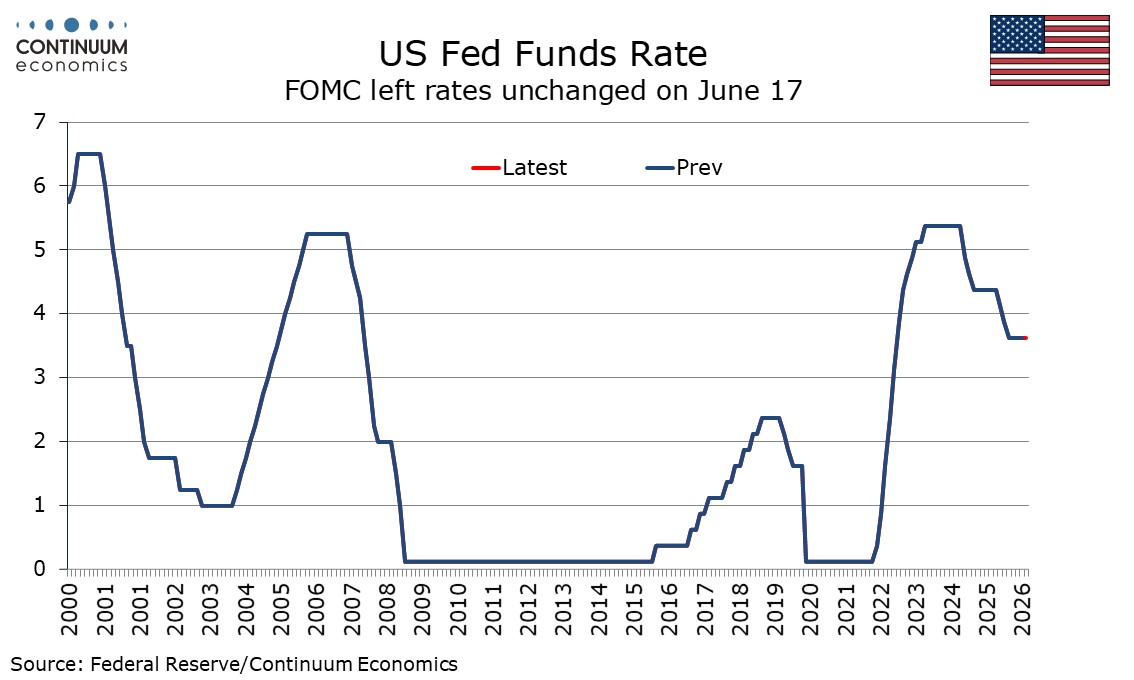

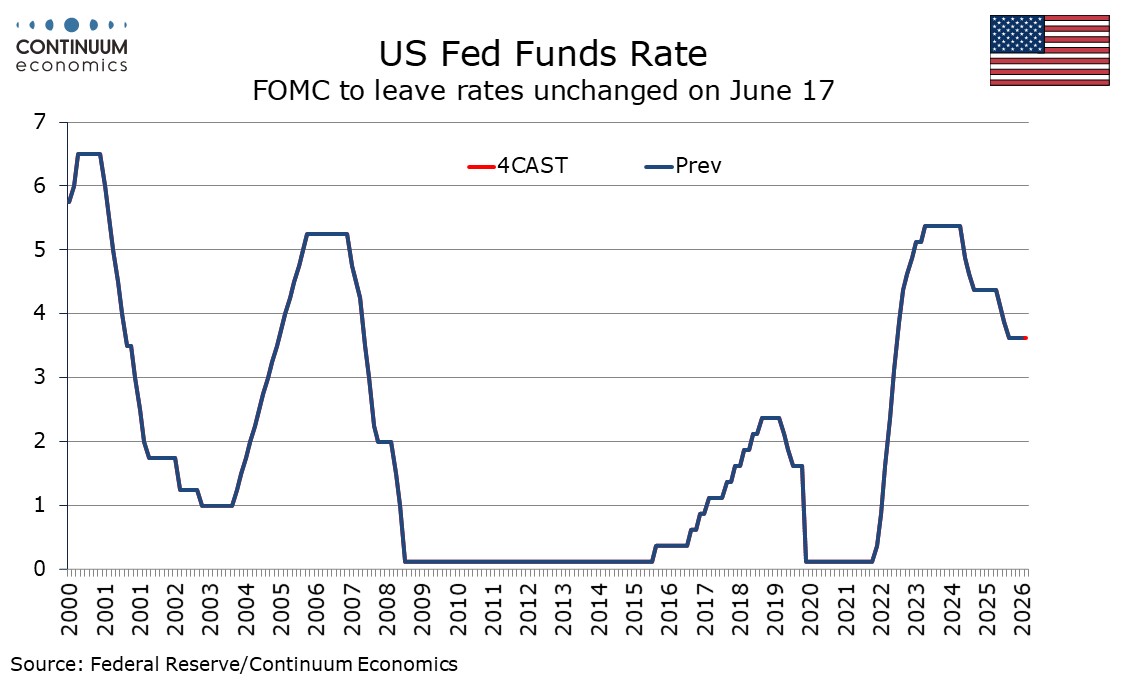

FOMC - Policy may prove less hawkish than the dots, assuming slowing in data

June 17, 2026 8:08 PM UTC

The Fed dots show a clearly divided Fed with only a minority on the median rates view for 2026, for a 25bps hike, 2027, which sees a 25bps reversal, and 2027, which sees a further 25bps easing. There are several respondents on either side of the median but we believe the voters lean towards the dovi

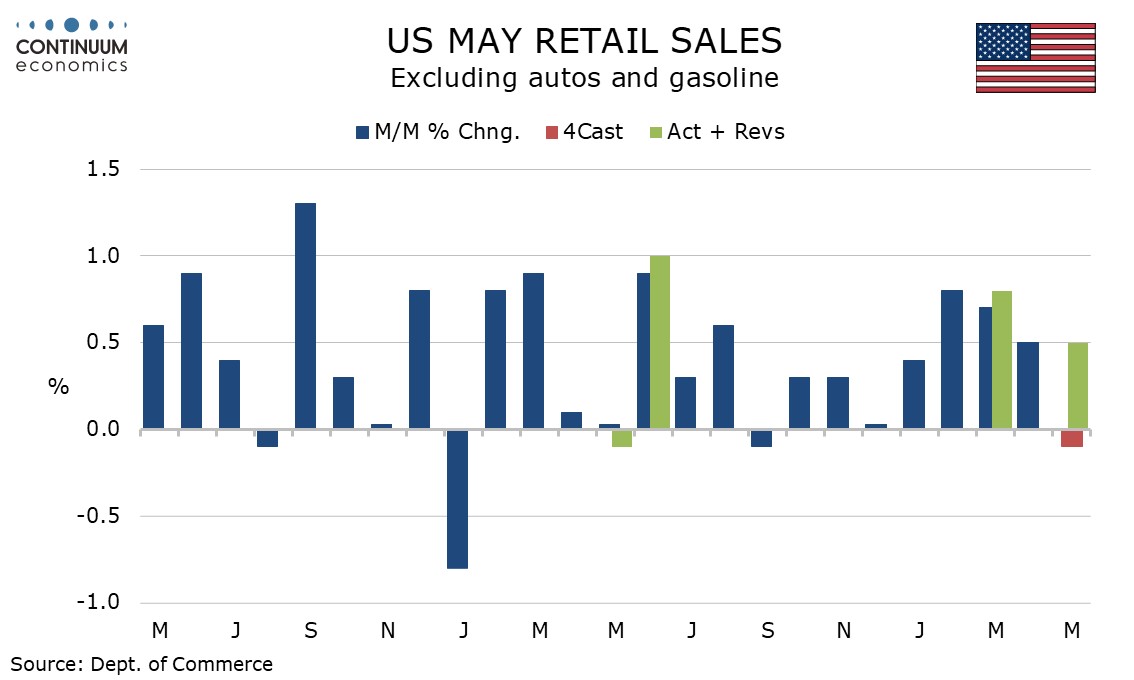

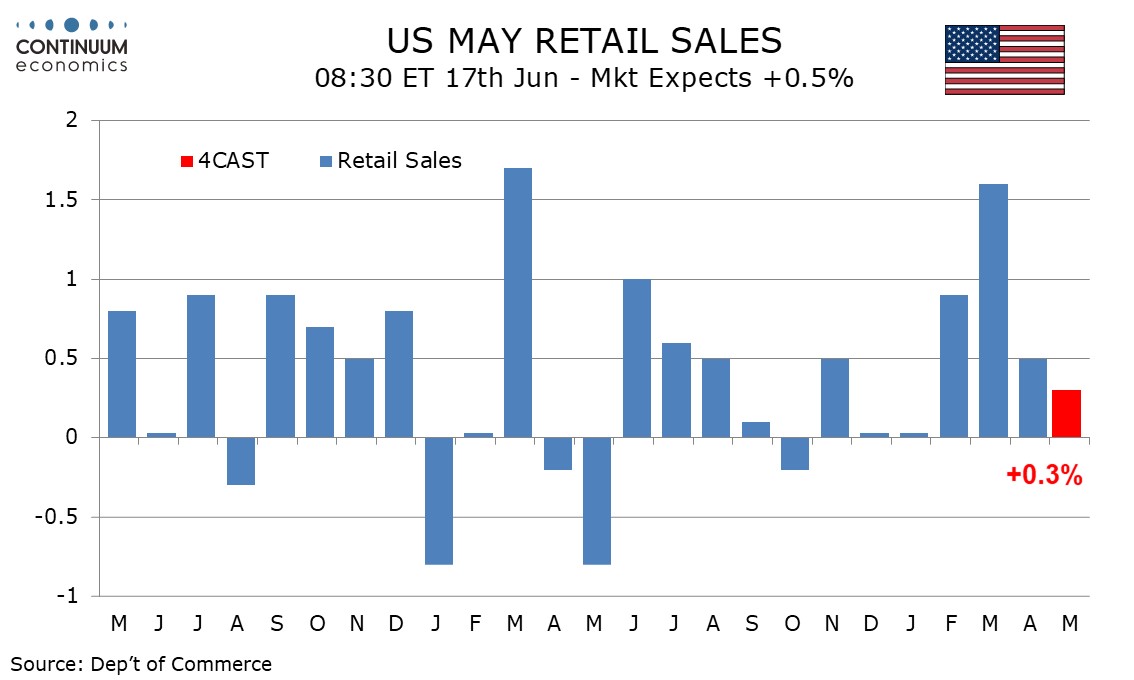

U.S. May Retail Sales - Impressive resilience

June 17, 2026 1:01 PM UTC

May retail sales continue to show impressive resilience to downward pressure on real disposable income from rising gasoline prices, with equity strength and lower taxes offsetting to the headwinds, as well as recent resilience in employment, Overall sales rose by 0.9%, with gains of 0.8% ex auto and

Sweden Riksbank Review: Mild Tightening Bias Persist but We Don’t See it Exercised?

June 17, 2026 8:08 AM UTC

Not only at the meeting this, we still see stable policy though to end-2027 rather than the small hikes markets and the Board are now pricing for late 2026. A similar profile has been offered by the Riksbank since last autumn (Figure 1) and it did bring forward its first hike hint a touch when it pr

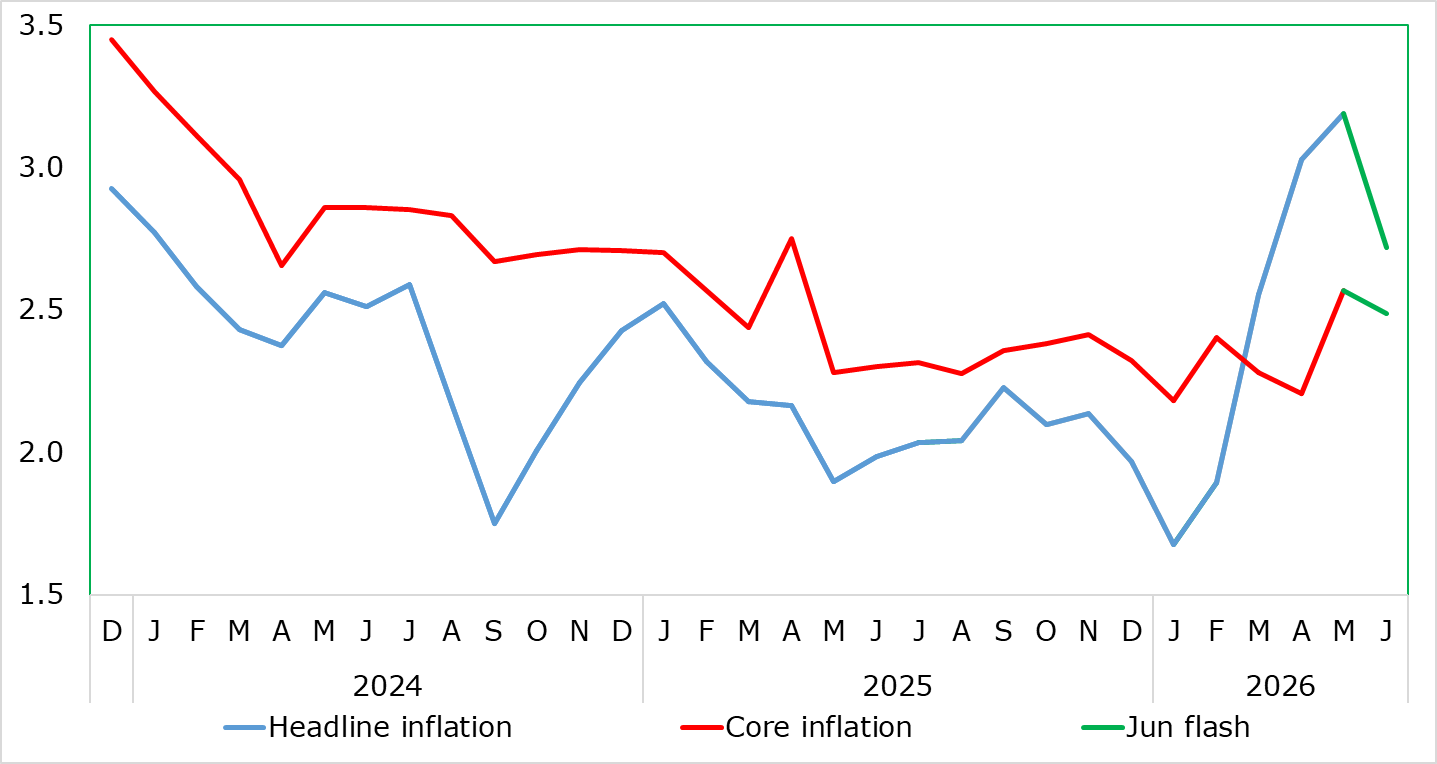

UK CPI Review: Inflation Peaking?

June 17, 2026 7:40 AM UTC

What have been energy induced price rises are starting to ease and may do so further In June before the OFGEM induced price rise hits July numbers. But a less worrying picture emerges in the latest (ie May) CPI and even PPI data. Indeed, once again, actual CPI have offered a more benign picture

BOJ: QT still 5-6% of GDP until 2030 at least!

June 17, 2026 6:25 AM UTC

· Though the BOJ will maintain bond buying at Yen2trn pm from April 2027, huge redemptions means that net QT will be Yen45trn April 27-March 28 i.e. around 6.5% of GDP after QT at 6% of GDP in 2026. Then JGB net reduction of Yen40trn (6% of GDP) FY 29 and Yen35trn (5.5% of GDP). Wit

June 16, 2026

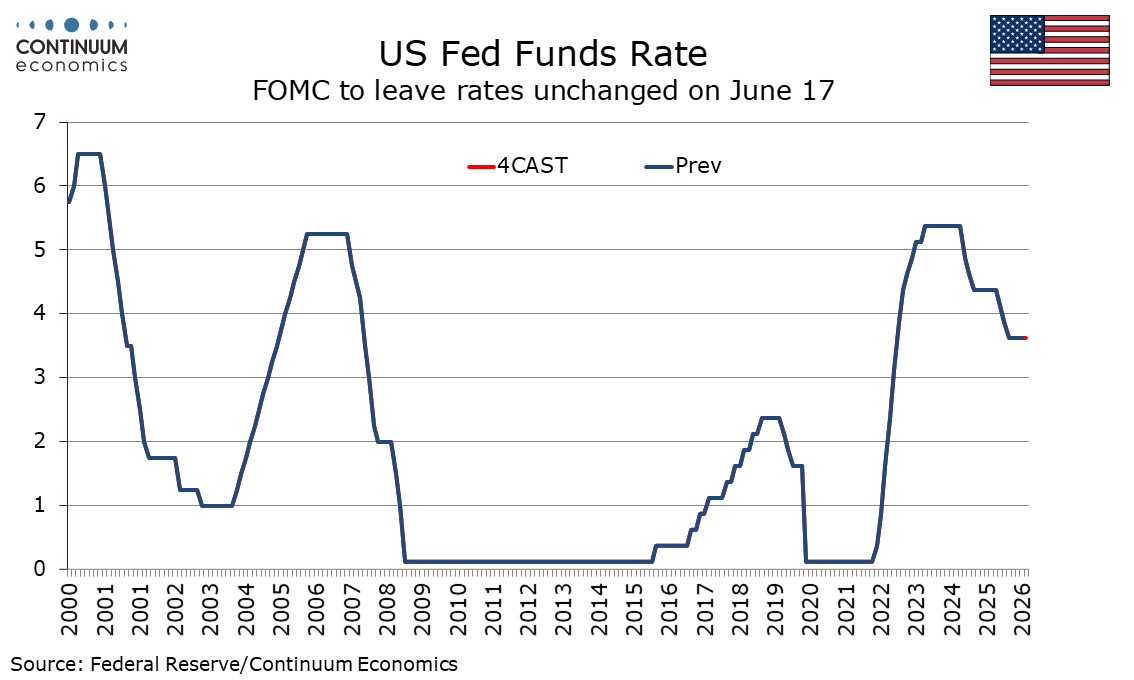

FOMC Preview for June 17: Dropping the easing bias (update)

June 16, 2026 2:58 PM UTC

The FOMC meets on June 17 and while a change in the Fed Funds target range from the current 3.5-3.75% is unlikely, the statement is likely to drop the easing bias. The median dots are likely to get a little more hawkish with a hawkish skew in the detail, with inflation forecasts, including those for

Preview: Due June 17 - U.S. May Retail Sales - Consumers vulnerable to a pull back

June 16, 2026 12:02 PM UTC

We expect May retail sales to increase by 0.3% both overall and ex autos, but with a 0.1% decline ex autos and gasoline, which would suggest that consumers are starting to pull back as elevated gasoline prices increasingly weigh on real disposable income.

China: Divided Economy

June 16, 2026 7:22 AM UTC

· Overall, growth remains unbalanced. Momentum in AI/automation leads economic growth, with support from net exports still. However, consumption is not consistent with a 5% growth pace, as adverse wealth effects and a soft labor market mean only modest consumption. While the stimu

June 15, 2026

June 12, 2026

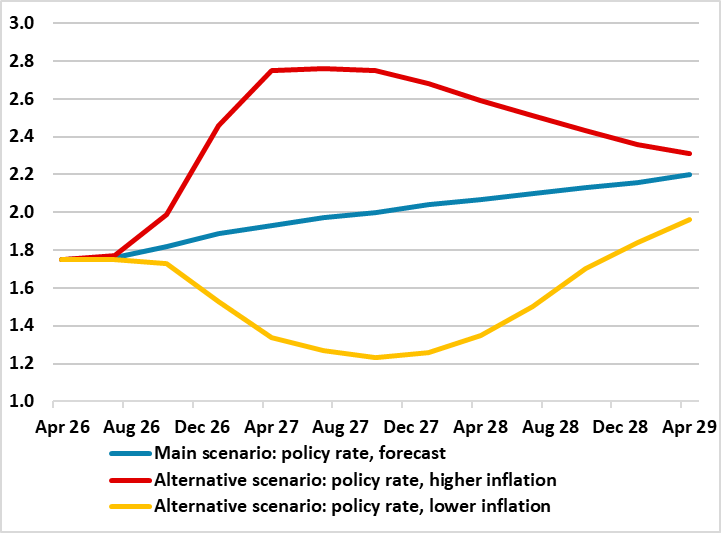

Fed Tightening and U.S. Treasury Yields: 1994, 1999 and 2022 Redux

June 12, 2026 7:05 AM UTC

Our baseline involves no Fed hike, but 50-75bps is feasible in a plausible adverse scenario. In this alternative scenario of 50-75bps of Fed tightening it is easy to build the case for 2yr yields going to 4.30-4.40% area, before thoughts turn to H2 2027/28 involving modest Fed rate cuts. 10yr

UK GDP Review: GDP Upside Surprises Persist?

June 12, 2026 6:56 AM UTC

Perhaps it is a supreme irony that just as business surveys suggest clear weakness, if not fresh contraction, the actual real economy has surprised on the upside, even now into the second month after the Middle East conflict started. Indeed, and in perspective, official GDP data suggest that since

June 11, 2026

CBRT Kept Key Rate Constant at 37% Despite Inflationary Risks

June 11, 2026 3:44 PM UTC

Bottom Line: Central Bank of Turkiye (CBRT) held the policy rate constant at 37% during the MPC meeting on June 11 despite inflationary risks as economy remains under pressure from Iran war, which sparked a surge in energy, transportation and agricultural input costs. CBRT stated in its written stat

ECB Review: If Not Insurance, Why the Hike?

June 11, 2026 2:27 PM UTC

The 25 bp official rate hike unveiled today was so well-flagged it is hard to suggest that it is consistent with a decision process on a meeting-by-meeting basis. Similarly, the dominance of inflation upside risks, alongside another dose of optimistic real economy projections, is hardly proper dat

BoE Preview (Jun 18): Splits to Widen, But Stable Policy Outlook Intact

June 11, 2026 10:26 AM UTC

Not only this month, but we see the BoE being on hold for the rest of the year with rate cuts then resuming through 2027. Although markets are pricing just over two hikes from the current 3.75% with a 50%-plus probability of the first being delivered at the July 30 MPC meeting, our view is hardly

Swiss SNB Preview (Jun 18): Still Keeping a Low Profile

June 11, 2026 6:33 AM UTC

Once again and in line with consensus thinking we see SNB policy being unchanged (ie the policy rate remaining at zero) when it gives its next quarterly assessment this month with little shift in the forecasts for either growth or inflation. Admittedly, the tone of the economic outlook will remain

June 10, 2026

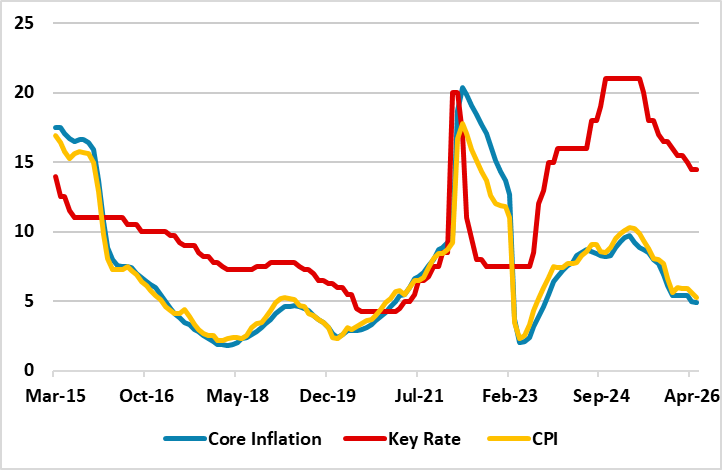

Russian Inflation Drops to 5.3% in May, Hitting Lowest Level Since August 2023

June 10, 2026 5:41 PM UTC

Bottom Line: Russia’s annual inflation continued its decreasing pattern moderately in May and slowed to 5.3% y/y. This deceleration was driven by the lagged effects of previous aggressive monetary tightening, a relatively resilient ruble, and softening core inflation. Marking the lowest level sinc

FOMC Preview for June 17: Dropping the easing bias

June 10, 2026 4:55 PM UTC

The FOMC meets on June 17 and while a change in the Fed Funds target range from the current 3.5-3.75% is unlikely, the statement is likely to drop the easing bias. The median dots are likely to get a little more hawkish with a hawkish skew in the detail, with inflation forecasts, even ex food and en