Norges Bank Preview (Dec 18): Still Far Too Cautious

No change in policy and little shift in rhetoric was the message from the Norges Bank’s latest verdict. After what was to some a surprise (and seemingly far from a formality) move in September, in which the Norges Bank cut is policy rate by a further 25 bp to 4.0%, we see no change at the looming Dec 18 verdict, this being consistent with the Board’s repeated assertion that ‘the policy rate will be reduced further in the course of the coming year’. This December meeting will have both new forecasts and data for the Board to peruse, not least inflation and lending numbers, the latter possibly becoming a worry given the fresh slowing in corporate credit growth and weaker GDP backdrop. But with underlying inflation dynamics being friendly (Figure 2), we still think that the Norges Bank is being far too cautious as it plans to keep policy very restrictive through the projected timeframe out to 2028; we wonder why the Board therefore only see inflation only just approaching the 2% target by the end of that period.

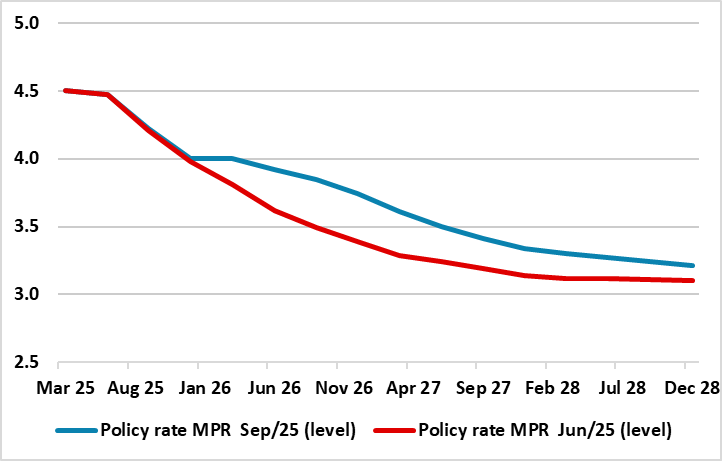

Figure 1: Norges Bank Policy Outlook

Source: Norges Bank Monetary Policy Report

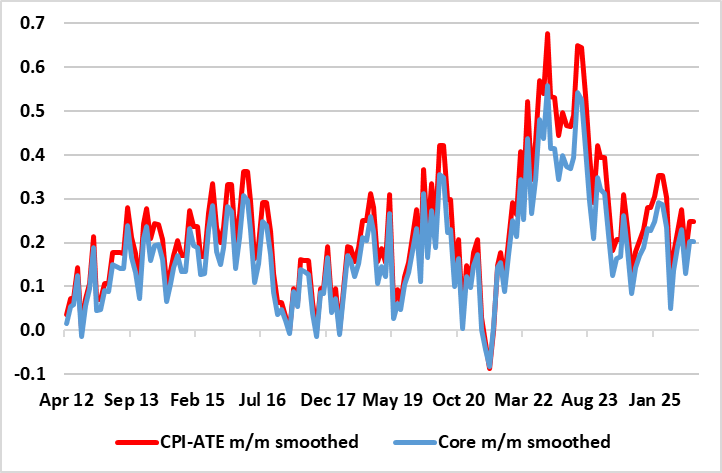

We remain a little less confident about the extent of easing into 2026 but envisage further 25 bp cuts every quarter through next year and then similarly into H1 2027. At 2.5%, that would still leave the policy rate still within the neutral rate range estimated by the Norges Bank. In other words, the Norges Bank will be merely taking its foot of the brake, rather than pressing on the accelerator. But inflation worries continue to dominate Norges Bank thinking. Admittedly, running at a circa-3% rate, thereby still a full ppt above target, targeted (CPI-ATE) inflation is being boosted by stubborn services inflation. This is partly offsetting ever softer goods and imported inflation, the latter coming in spite of the weak Krona backdrop that continues to influence Board thinking excessively – albeit the latter having failed to appreciate in line with the Board’s hawkish caution. Regardless, taking food out of the CPI-ATE, thus mirroring a core rate measure used by other central banks, actually shows inflation running just above the 2% target (Figure 2).

This being similar to the core inflation backdrop seen in EZ, where the ECB has responded with 200 bp of rate cuts, this surely in an indictment of the Norges Bank’s excessive caution and focus on the exchange rate despite the latter lack of correlation with imported inflation. But real economy issues are also adding to the arguments for rate cutting. GDP hardly rose in Q3, this undershooting Board expectations and where m/m falls in the last two months of Q3 hardly provide much momentum for the current quarter, let alone the Board’s 0.4% q/q projection. This is occurring as company credit growth is slowing g, actually falling in apparent real terms and where the Norges Bank’s recent bank lending survey note that banks report a slight decline in non-financial corporate credit demand in the last quarter.

Figure 2: CPI Dynamics More Friendly in Adjusted and Ex Food Perspective

Source: Stats Norway, CE, smoothed is 3 mth mov avg. Core is CPI-ATE ex food

Thus, as for inflation, we think that the Norges Bank is still being too cautious, and that the Board may have to pare back its recently upgraded 2.0% 2025 GDP projection more in line with its more reasonable 2026 1.5% mainland GDP projections. In fact, we would contend that an emerging and earlier output gap is partly responsible for the fall in inflation seen of late – admittedly unwinding the overshoot of the early part of 2025.

I,Andrew Wroblewski, the Senior Economist Western Europe declare that the views expressed herein are mine and are clear, fair and not misleading at the time of publication. They have not been influenced by any relationship, either a personal relationship of mine or a relationship of the firm, to any entity described or referred to herein nor to any client of Continuum Economics nor has any inducement been received in relation to those views. I further declare that in the preparation and publication of this report I have at all times followed all relevant Continuum Economics compliance protocols including those reasonably seeking to prevent the receipt or misuse of material non-public information.