Editor's Choice

View:

July 06, 2026

July 03, 2026

EM Government Debt Sinners and Saints

July 3, 2026 1:05 PM UTC

· Overall, the clearest EM fiscal sinner is Brazil, given its tax revenue/GDP ratio is already very high and requires politically sensitive expenditure cuts after the October election to increase the primary surplus to stabilize the government debt/GDP trajectory and get real bond yield

July 02, 2026

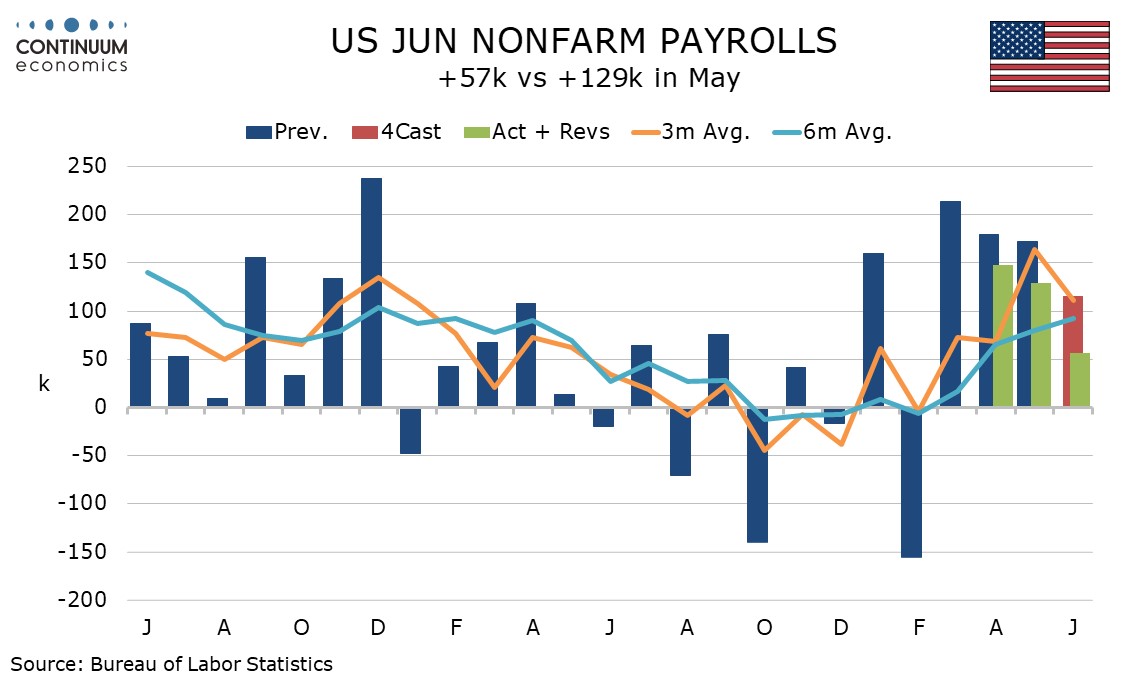

U.S. June Employment - Upside May surprise offset, but unemployment falls on lower labor force

July 2, 2026 1:20 PM UTC

June’s non-farm payroll is weaker than expected with a 57k increase, 49k private, with downward revisions to April and May. The slowing is consistent with an upturn in the initial and continued claims trends, though both were almost unchanged (-1k to 215k and +2k to 1.814m respectively) in the l

U.S. June Employment - Upside May surprise offset, but unemployment falls on lower labor force

July 2, 2026 1:12 PM UTC

June’s non-farm payroll is weaker than expected with a 57k increase, 49k private, with downward revisions to April and May. The slowing is consistent with an upturn in the initial and continued claims trends, though both were almost unchanged (-1k to 215k and +2k to 1.814m respectively) in the l

July 01, 2026

EZ HICP Review: Absence Second-Round Effects Continues

July 1, 2026 1:42 PM UTC

Contrary to some thinking, EZ HICP inflation continues to behave, both absolutely and relatively – ie to what looks ever excessive ECB price thinking. The question must be if and when the ECB chooses to note friendlier price and costs signals, rather than pander to the upside prices risks that o

EZ HICP Review: Absence Second-Round Effects Continues

July 1, 2026 10:41 AM UTC

Contrary to some thinking, EZ HICP inflation continues to behave, both absolutely and relatively – ie to what looks ever excessive ECB price thinking. The question must be if and when the ECB chooses to note friendlier price and costs signals, rather than pander to the upside prices risks that o

June 30, 2026

AI Boom and Bust?

June 30, 2026 10:45 AM UTC

• While some are becoming wary that AI bust could arrive in coming quarters, AI labs revenue growth has been explosive and this sustains the vertical chain of datacenter demand and commitments for the hyperscalers and also buoyant semiconductor demand. For 2027 and 2028 capital markets re

June 29, 2026

China Yuan to 6.65 Then 6.50?

June 29, 2026 7:10 AM UTC

· We feel that the authorities will pause appreciation at times via FX intervention, but then allow appreciation to restart. We now see further Yuan appreciation to 6.65 by end 2026, though the authorities will be reluctant to see much more. For end 2027 we forecast USDCNY at 6.50

June 26, 2026

ECB Sin(a)tra Preview: Should the ECB Only Consider My Way?

June 26, 2026 1:29 PM UTC

The speed and manner in which the ECB adopted a hawkish stance is response to the Middle East conflict was no surprise; it has many precedents, some of which have led to policy errors which we think may be being repeated at this juncture. Indeed, despite friendlier price and costs signals, the ECB

Mexico: Banxico Pause, But MXN and USMCA Renegotiations

June 26, 2026 7:04 AM UTC

· As expected Banxico left the policy rate unchanged at 6.50%, with the focus now on the lagged benefit of easing and also what will happen with the USMCA negotiations. Banxico will likely keep the current policy rate through end 2026, given concerns that the Fed could tighten – eve

June 25, 2026

U.S. Personal Income and Spending, GDP, Durable Goods Orders, and Initial Claims - Mostly firm but consumer spending revised lower

June 25, 2026 1:40 PM UTC

The latest US data is mostly strong, with an upward revision to Q1 GDP, stronger than expected May personal income and spending, still firm core PCE prices, lower initial claims and strength in May durable goods orders outside a fall in transport. However the Q1 GDP revision was mixed, with a signif

June 24, 2026

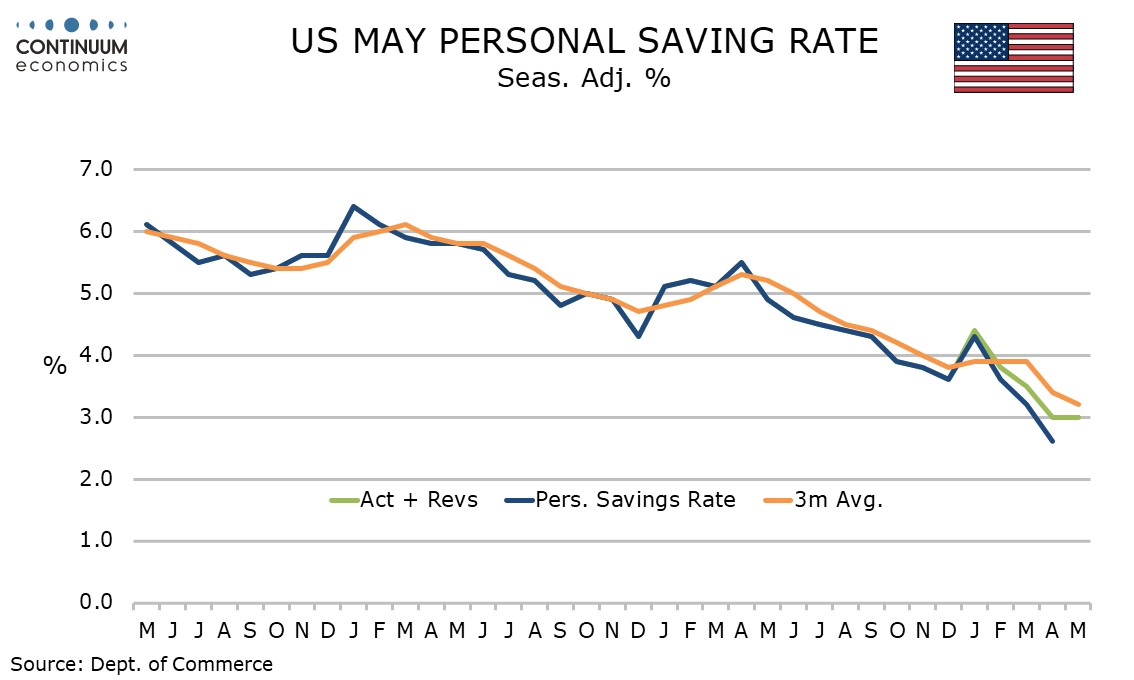

Preview: Due June 25 - U.S. May Personal Income and Spending - Core PCE Prices to outperform CPI, Savings to fall further

June 24, 2026 1:24 PM UTC

We expect May’s core PCE price index to rise by 0.3%, though probably on the low side of 0.3% before rounding, with overall PCE prices up by 0.4%. We expect a 0.6% increase in personal spending to outperform a 0.3% rise in personal income, extending a recent sharp decline in savings.

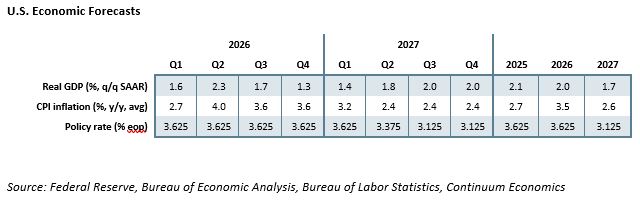

Outlook Overview: Cyclical and Structural Forces

June 24, 2026 7:00 AM UTC

· The difference between 2nd round inflation effects from higher energy prices and 1st round effects that central banks can look through swings on whether the Straits of Hormuz will remain open in the coming months after the U.S./Iran interim agreement (here). Despite some tensions, we

China and EM Asia Outlook: Divergent Trends

June 24, 2026 6:22 AM UTC

· China’s growth momentum is being sustained by AI/tech and green energy production and investment. However, growth is imbalanced with modest consumption growth, due to adverse housing wealth effects and slow wage/job growth. Overall, we forecast 4.4% for 2026 and 4.2% for 2027. Chi

June 23, 2026

DM Rates Outlook: Tightening or Easing?

June 23, 2026 8:15 AM UTC

· With the U.S./Iran interim agreement likely to hold and energy prices softening, our projected consumer slowdown will likely tilt the Fed not to hike in H2 2026 and to actually ease by 50bps in 2027, with 25bps moves in both Q2 and Q3. With 2yr yields consistent with a hike, the tra

DM and EM FX Outlook: Cross-Currents for H2 and 2027

June 23, 2026 8:00 AM UTC

· Our baseline for the coming quarters is that global FX is moving through a period of dollar bounce and cross-current positioning adjustment, rather than a clean return to the dollar downtrend. The near-term driver is the market's (over) hawkish reading of the June FOMC/Summary of Econ

June 22, 2026

U.S. Outlook: Consumers Looking Vulnerable

June 22, 2026 2:17 PM UTC

• The US economy is showing resilience with strength in investment offsetting a gradual slowing in consumption, though consumer spending, which is running well ahead of real disposable income, looks set to slow further. This is likely to see the economy slow in the second half of 2026 even

Equities Outlook: AI Optimism, But Caution Elsewhere in DM economies

June 22, 2026 7:05 AM UTC

· In terms of the S&P500, we remain less concerned about high valuations in the tech sector provided AI labs growth remains fast. 12mth fwd information technology are mid-range in the 2020-26 experience rather than at the highs. Even so, heavy equity issuance by tech companies and a s

June 19, 2026

Brazil: Slowing Pace of Cuts and BRL Strength

June 19, 2026 6:55 AM UTC

· Brazil cut the SELIC by 25bps to 14.25%, but received critiques from the market by raising end 2027 CPI inflation from 3.5% to 3.7% and talking about Q1 2028 in the relevant policy horizon. We feel that BCB still wants to leave the door open to further cuts in 2026, given how restrict

June 18, 2026

BOE: Gang of 6 and Steady 2026 Rates

June 18, 2026 11:27 AM UTC

Though Megan Greene joined Huw Pill in calling for a one off 25bps risk management hike, 6 MPC members feel that disinflation is showing through and a soft economy and labor market warrants waiting to see energy prices and potential 2nd round effects. This gang of 6 also feels that markets have ti

June 17, 2026

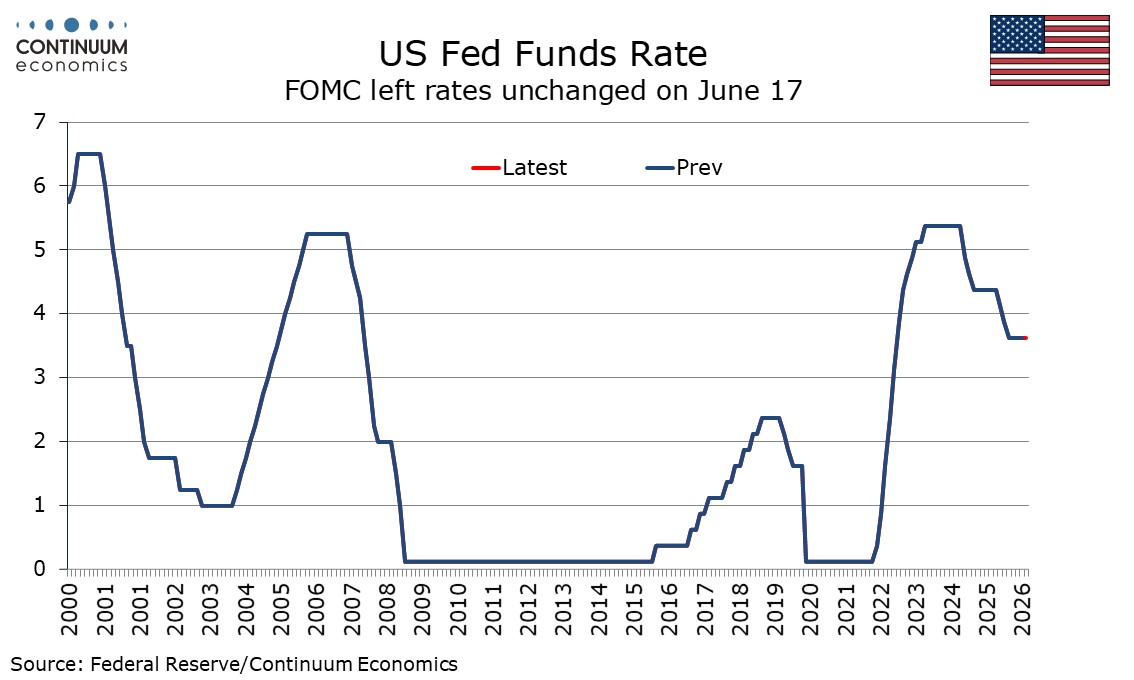

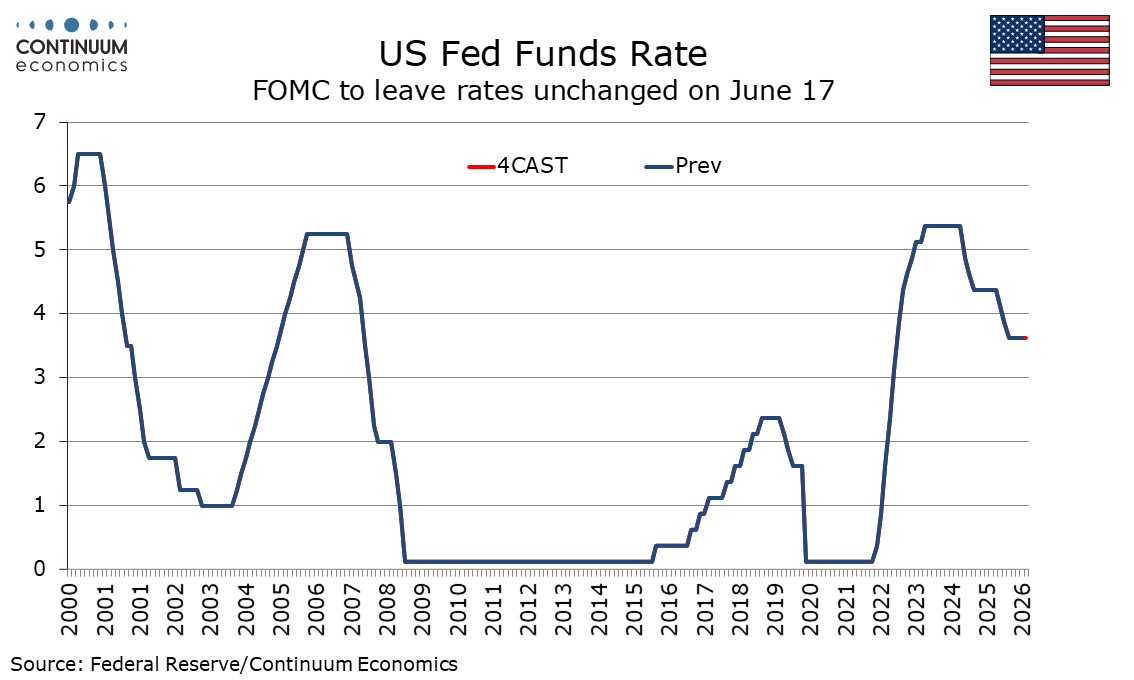

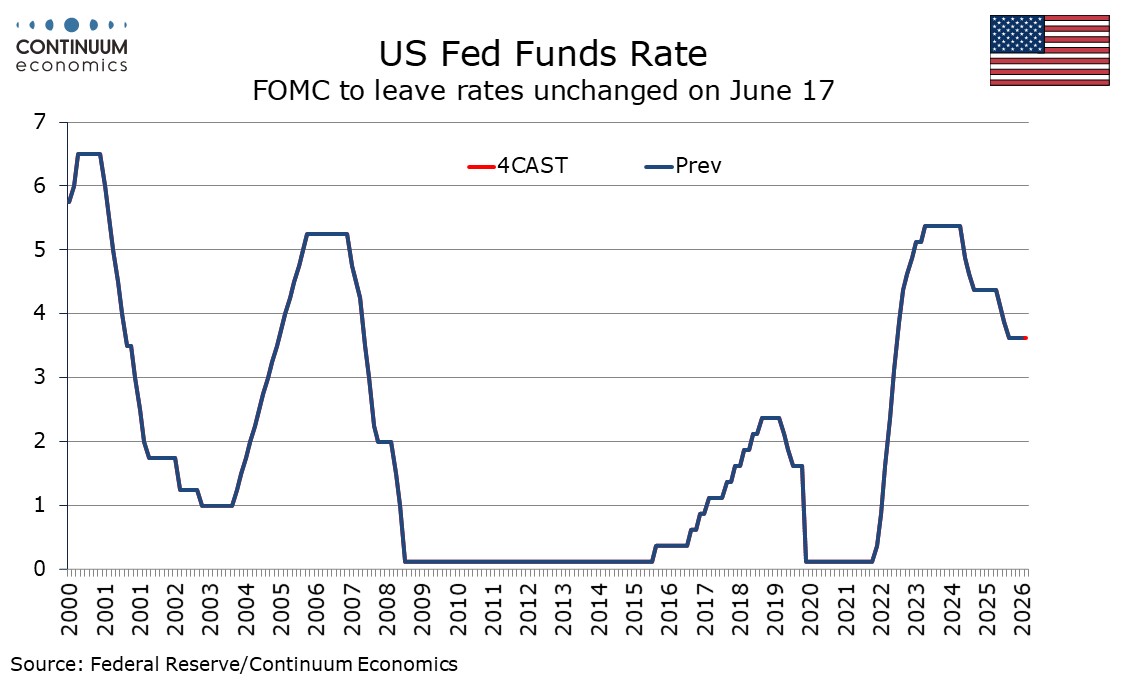

FOMC - Policy may prove less hawkish than the dots, assuming slowing in data

June 17, 2026 8:08 PM UTC

The Fed dots show a clearly divided Fed with only a minority on the median rates view for 2026, for a 25bps hike, 2027, which sees a 25bps reversal, and 2027, which sees a further 25bps easing. There are several respondents on either side of the median but we believe the voters lean towards the dovi

Preview: Due June 25 - U.S. May Personal Income and Spending - Core PCE Prices to outperform CPI, Savings to fall further

June 17, 2026 2:30 PM UTC

We expect May’s core PCE price index to rise by 0.3%, though probably on the low side of 0.3% before rounding, with overall PCE prices up by 0.4%. We expect a 0.6% increase in personal spending to outperform a 0.3% rise in personal income, extending a recent sharp decline in savings.

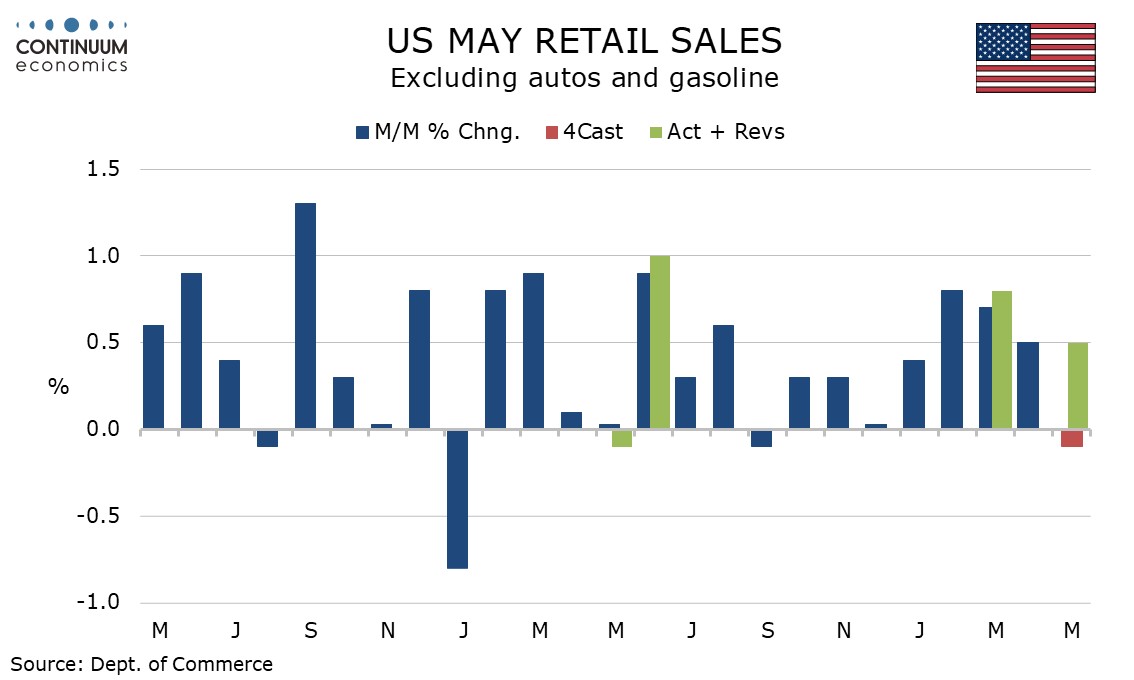

U.S. May Retail Sales - Impressive resilience

June 17, 2026 1:01 PM UTC

May retail sales continue to show impressive resilience to downward pressure on real disposable income from rising gasoline prices, with equity strength and lower taxes offsetting to the headwinds, as well as recent resilience in employment, Overall sales rose by 0.9%, with gains of 0.8% ex auto and

BOJ: QT still 5-6% of GDP until 2030 at least!

June 17, 2026 6:25 AM UTC

· Though the BOJ will maintain bond buying at Yen2trn pm from April 2027, huge redemptions means that net QT will be Yen45trn April 27-March 28 i.e. around 6.5% of GDP after QT at 6% of GDP in 2026. Then JGB net reduction of Yen40trn (6% of GDP) FY 29 and Yen35trn (5.5% of GDP). Wit

June 16, 2026

FOMC Preview for June 17: Dropping the easing bias (update)

June 16, 2026 2:58 PM UTC

The FOMC meets on June 17 and while a change in the Fed Funds target range from the current 3.5-3.75% is unlikely, the statement is likely to drop the easing bias. The median dots are likely to get a little more hawkish with a hawkish skew in the detail, with inflation forecasts, including those for

China: Divided Economy

June 16, 2026 7:22 AM UTC

· Overall, growth remains unbalanced. Momentum in AI/automation leads economic growth, with support from net exports still. However, consumption is not consistent with a 5% growth pace, as adverse wealth effects and a soft labor market mean only modest consumption. While the stimu

June 15, 2026

U.S./Iran Interim Deal and Reopening Strait of Hormuz

June 15, 2026 12:32 PM UTC

· Our baseline (80%) is that the Strait of Hormuz will reopen in H2 2026 and remains open through 2027. However, logistics dislocation plus a switch from commercial inventory rundown to rebuilding will likely slow the decline in oil prices back towards normal levels (Figure 1). O

June 12, 2026

Fed Tightening and U.S. Treasury Yields: 1994, 1999 and 2022 Redux

June 12, 2026 7:05 AM UTC

Our baseline involves no Fed hike, but 50-75bps is feasible in a plausible adverse scenario. In this alternative scenario of 50-75bps of Fed tightening it is easy to build the case for 2yr yields going to 4.30-4.40% area, before thoughts turn to H2 2027/28 involving modest Fed rate cuts. 10yr

June 11, 2026

ECB Review: If Not Insurance, Why the Hike?

June 11, 2026 2:27 PM UTC

The 25 bp official rate hike unveiled today was so well-flagged it is hard to suggest that it is consistent with a decision process on a meeting-by-meeting basis. Similarly, the dominance of inflation upside risks, alongside another dose of optimistic real economy projections, is hardly proper dat

June 10, 2026

FOMC Preview for June 17: Dropping the easing bias

June 10, 2026 4:55 PM UTC

The FOMC meets on June 17 and while a change in the Fed Funds target range from the current 3.5-3.75% is unlikely, the statement is likely to drop the easing bias. The median dots are likely to get a little more hawkish with a hawkish skew in the detail, with inflation forecasts, even ex food and en

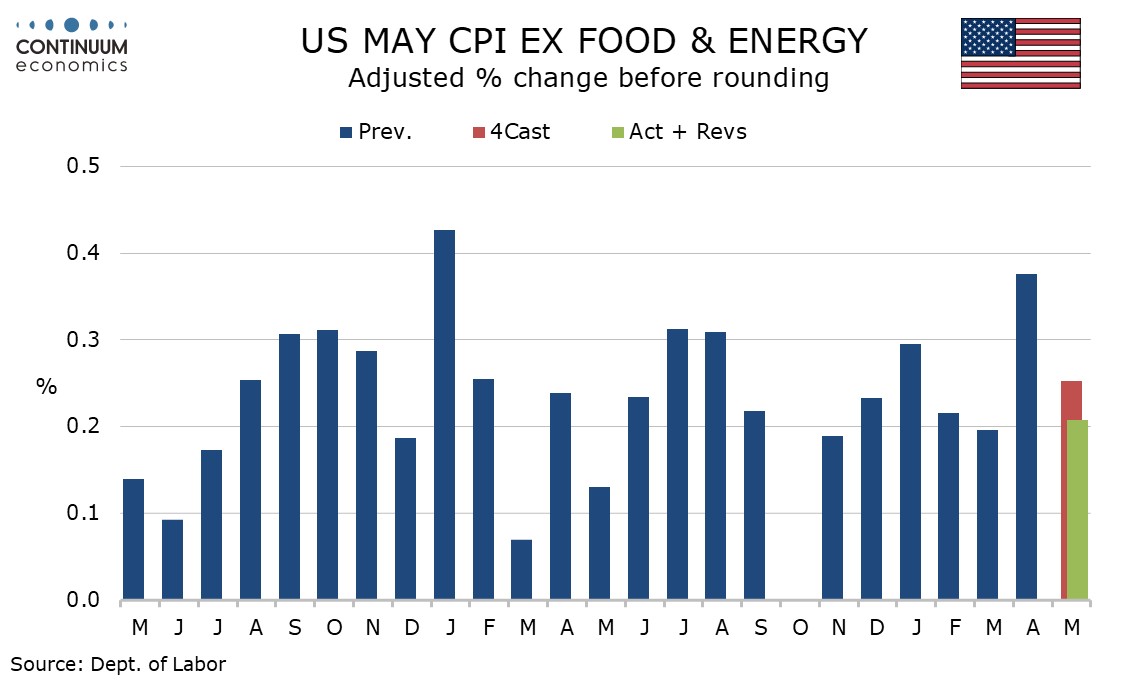

U.S. May CPI - Surprising fall in transport services despite continued gains in air fares

June 10, 2026 1:08 PM UTC

May CPI is in line with expectations at 0.5% overall but the core rate ex food and energy was softer than expected at 0.2%, with the rise before rousing being 0.208%. The most surprising restraint on the data was a 0.6% fall in transportation services, despite continued gains in air fares.

Financial Markets/Policymakers and the Strait of Hormuz Question

June 10, 2026 8:05 AM UTC

· Though the U.S. and Iran have attacked each other June 10, talks to reopen the straits of hormuz still continue. An Iran/U.S. agreement to reopen the Straits of Hormuz could cure the risk of a demand/supply oil market imbalance and produce some psychological relief that could knock USD

June 08, 2026

DM Government Bonds: Risks of Higher Long End Premia?

June 8, 2026 2:10 PM UTC

· Our baseline is for DM government bond yields ex Japan to remain elevated, but controlled. Japan extra risk premium is driven by BOJ QT at 6% of GDP, more than long-term debt fears. Major catalysts could drive a regime change to higher risk premia and steeper yield curves, but non

June 05, 2026

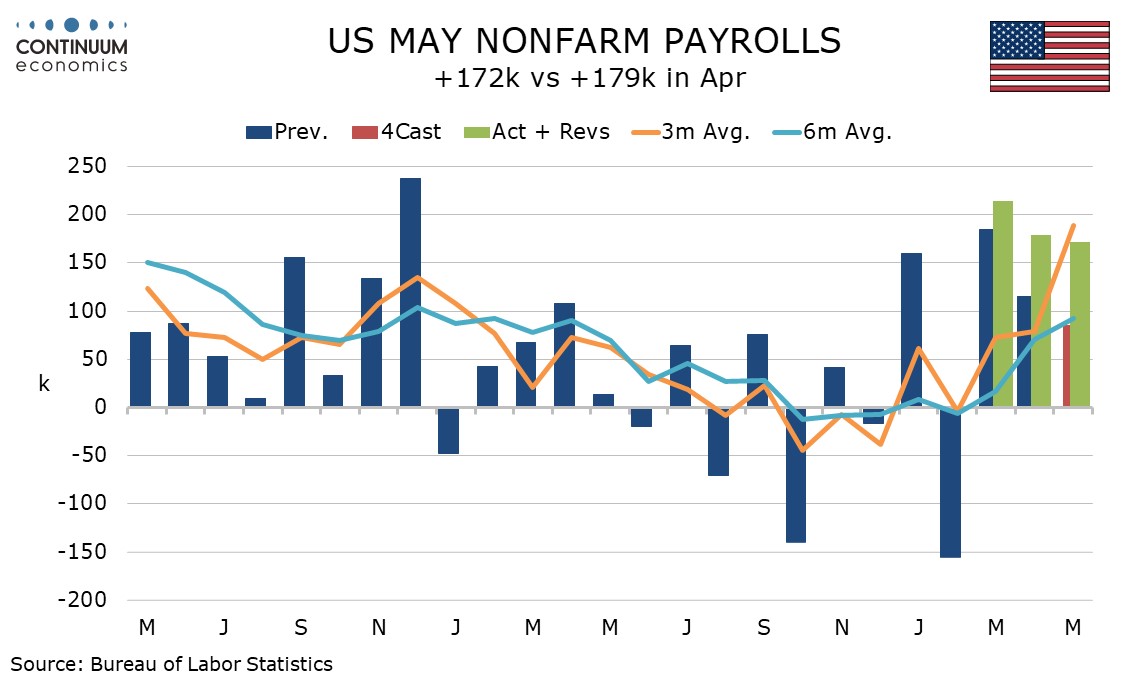

U.S. May Employment - Surprise came from local government and leisure and hospitality

June 5, 2026 1:19 PM UTC

May’s non-farm payroll is significantly stronger than expected with a rise of 172k though the private sector was less impressive at 120k, if still healthy. Upward revisions to March and April add to the positive message. In addition to government, leisure and hospitality with a 70k increase was

June 04, 2026

More Yuan Appreciation, but Controlled

June 4, 2026 9:55 AM UTC

• The Yuan has been appreciating driven by a large trade surplus; the ongoing trade truce with the U.S. after Trump May visit and official acceptance of Yuan gains. Even so, we feel that China’s authorities will pause appreciation at times via FX intervention to stop the move becoming too

June 03, 2026

ECB Preview (Jun 11): Words Not Deeds the Focus

June 3, 2026 10:23 AM UTC

Aware of repeating ourselves (again), it is the case that the next ECB Council meeting will be more important for what is said than what is done. In fact, a 25 bp official rate hike is virtually nailed on irrespective of how events in the Middle East may fare in coming days. But the ECB comments

June 02, 2026

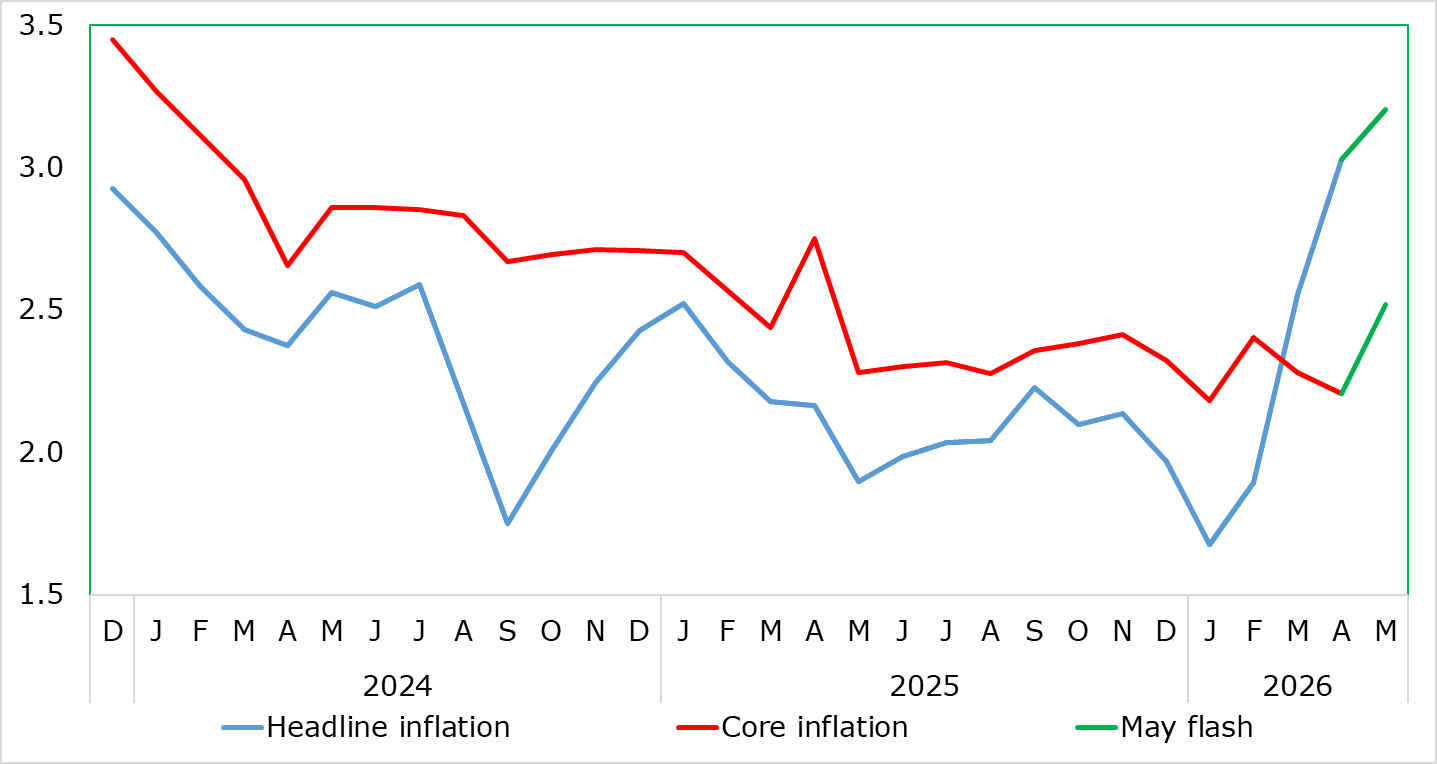

EZ HICP Review: Headline Rise Capped by Food & Energy, Services Jump Seasonal?

June 2, 2026 9:50 AM UTC

Even given what seem to be a series of reassuring aspects, the May flash HICP data is unlikely to have a material impact on ECB thinking. As expected, and helped by German fuel subsides which kept the energy rise to around zero, headline HICP rose just 0.2 ppt to 3.2%, still a 32-mth high, but whe

June 01, 2026

AI Labs IPO Fever

June 1, 2026 12:58 PM UTC

· Space X could get an initial good reception, but then go flat waiting for the Open AI and Anthropic IPO’s. Space X is an AI enterprise play rather than space and xAI is lagging. This could mean a modest correction in the U.S. equity market at some stage in the summer, but then the

May 29, 2026

2026 Q1 Country Insights Scores to Download in Excel

May 29, 2026 11:52 AM UTC

The Country Insights (CI) Model is a comprehensive quantitative tool for assessing country and sovereign risk, measuring a country’s exposure to external and domestic financial shocks and its capacity to grow. Our full range of scores across 174 countries for the first quarter of 2026 is now avail

Taiwan: Low Invasion Risk Post Trump Visit

May 29, 2026 11:05 AM UTC

· The most likely option for China is to continue the air and naval grey zone warfare around Taiwan, combined with support for pro-China factions in Taiwan’s parliament to build pressure for reunification at some stage. This stick and carrot approach is our baseline (Figure 1). Wi