United States

View:

August 22, 2025

Fed Powell: Signals September Cut

August 22, 2025 2:35 PM UTC

Fed Chair Powell spent the first 10 minutes at Jackson hole reviewing current data and discussing the policy stance. Powell clearly signaled a September cut, given downside risks to employment after the July employment report revisions. However, Powell did not signal whether the move will be 25b

August 20, 2025

U.S./China Trade Deal: Slow Progress

August 20, 2025 10:25 AM UTC

· Overall, we would attach a 50% probability to a trade framework deal being announced in Q4, though this is unlikely to be comprehensive and could merely be a collection of measures. Even so, the risk also exists of trade negotiations dragging onto 2026 and then reaching a deal or fa

August 19, 2025

China Slow Diversification: Gold And Others

August 19, 2025 8:05 AM UTC

China’s diversification from U.S. Treasuries appears to be at a slow pace. Gold is the obvious alternative if geopolitical tensions were to rise or skyrocket in the scenario of a China invasion of Taiwan. However, Gold holdings are merely creeping higher and suggesting no urgency from China

August 18, 2025

U.S. Strategic Fiscal Comparisons

August 18, 2025 9:05 AM UTC

The U.S. short average term to maturity is a structural fiscal weakness if higher rates lift U.S. government interest costs close to the nominal GDP trend. Hence, Trump’s pressure for fiscal dominance of the Fed to deliver lower policy rates and reduce U.S. government interest rate costs. Howeve

August 15, 2025

Preview: Due August 29 - U.S. July Personal Income and Spending - Core PCE Prices to match Core CPI

August 15, 2025 2:34 PM UTC

We expect PCE price data to match the July CPI, with a 0.3% rise in the core rate and a 0.2% increase overall. We expect both personal income and spending to rise by 0.5%, ahead of prices.

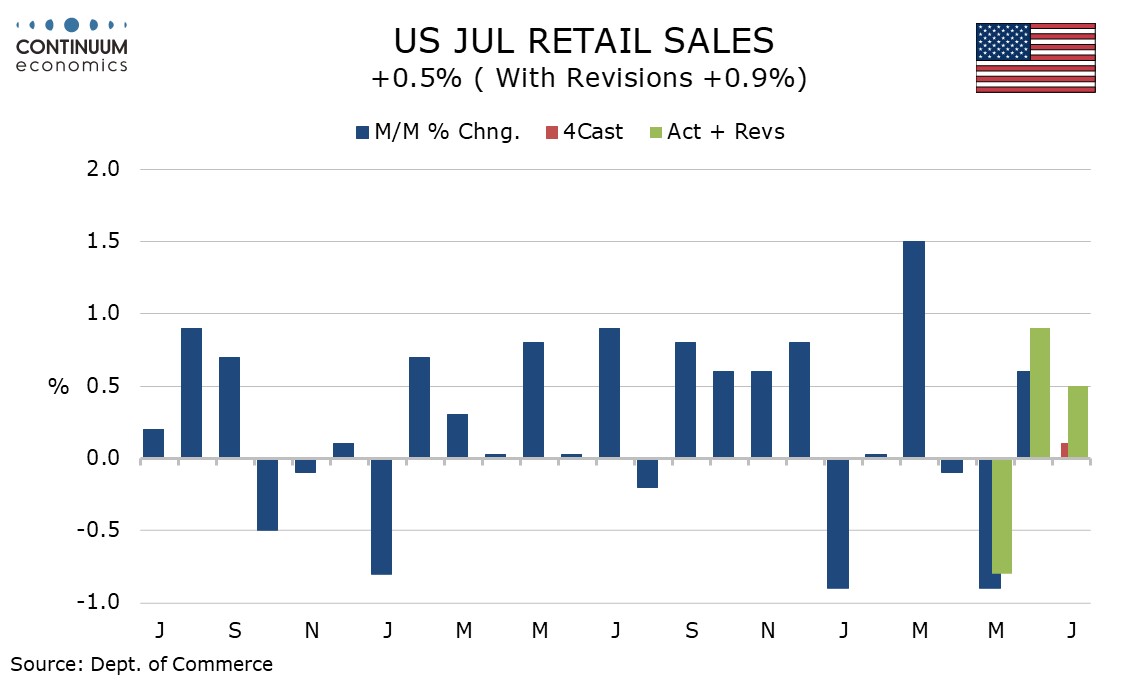

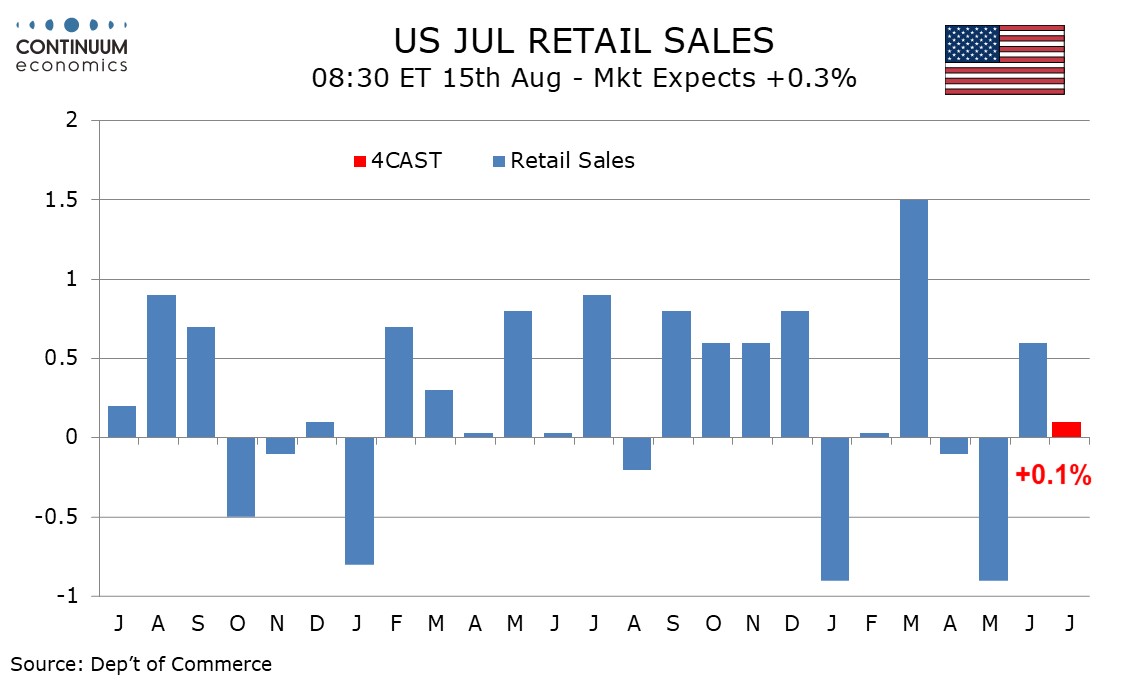

U.S. July Retail Sales - Resilient entering Q3

August 15, 2025 12:51 PM UTC

July retail sales with a 0.5% increase are in line with expectations, with net upward revisions totaling 0.4%. Ex auto sales rose by 0.3% also with 0.4% in upward revisions while ex auto and gasoline sales rose by 0.2%, here with revisions of only 0.2%. The data suggest consumer spending is holdin

August 14, 2025

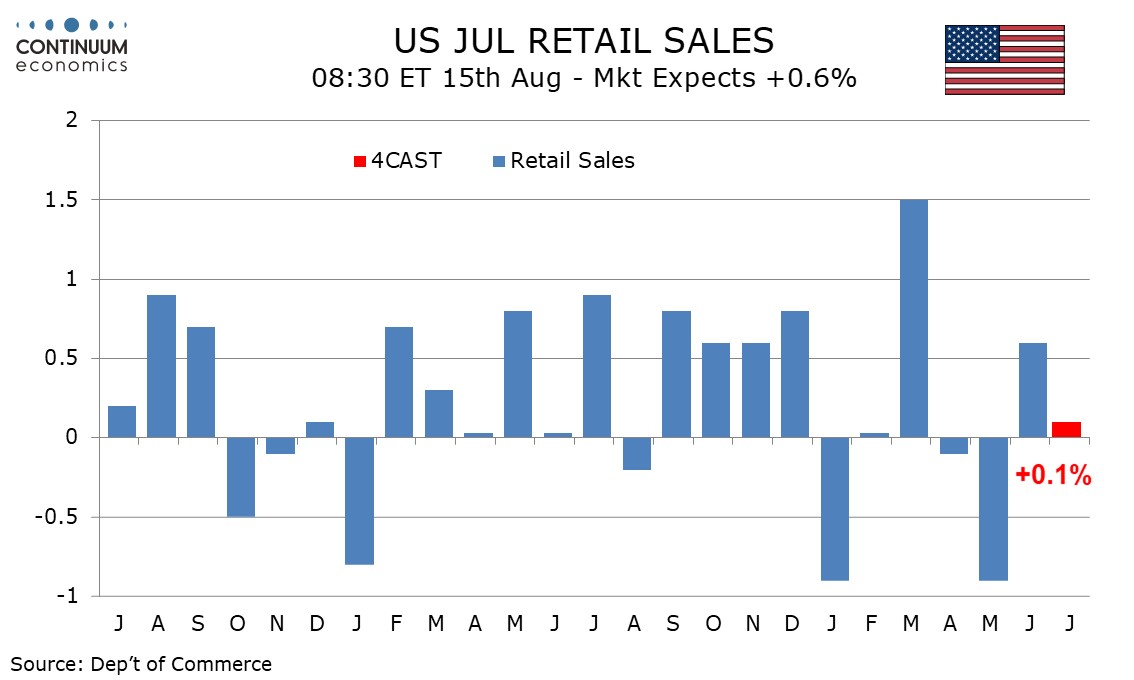

Preview: Due August 15 - U.S. July Retail Sales - Trend losing momentum

August 14, 2025 1:31 PM UTC

We expect a 0.1% increase in July retail sales to follow two straight declines, with 0.1% decline ex autos and an unchanged outcome ex autos and gasoline. This would restore a slowing trend after June saw a correction from declines in April and May.

U.S. Markets: Soft Versus Hard Landing

August 14, 2025 1:02 PM UTC

A mild recession would likely trigger the Fed to ease quickly to 2.0-2.5%, which would produce yield curve steepening but would likely drag 10yr yields down to 3.50-3.75%. The S&P500 would likely fall to 5000 in this scenario, as corporate earnings are axed; buybacks slow and the price/ea

August 13, 2025

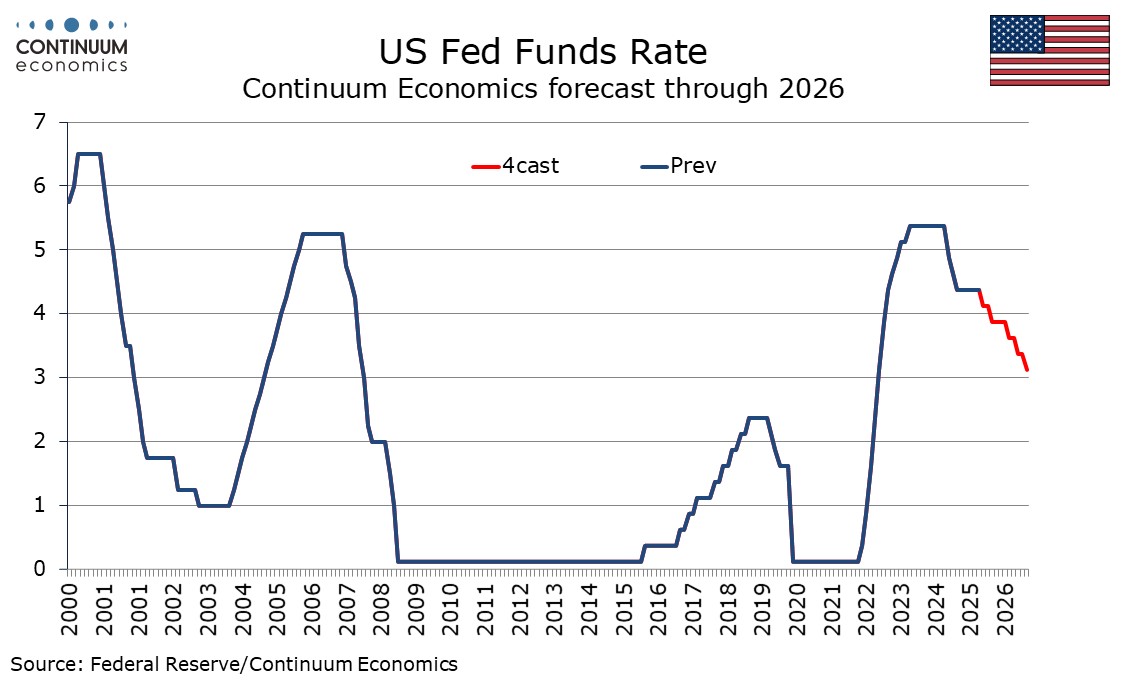

September Fed ease now more likely than not, but far from assured

August 13, 2025 3:29 PM UTC

A September FOMC easing now looks more likely than not, but remains far from a done deal. We are however revising our call to two 25bps FOMC easings this year, in September and December, from just one, in December. 2026 is harder still to call given threats to Fed independence, but we continue to ex

August 12, 2025

U.S. Budget moves back into deficit in July

August 12, 2025 6:27 PM UTC

Contrasting June’s $27.0bn budget surplus, July has recorded a deficit of $291.1bn, which is up from $243.7bn a year ago. Outlays bounced by 9.7% yr/yr after a 7.0% decline in June while receipts rose by only 2.5% yr/yr w3hixch is the weakest since October 2024, and down from a 12.9% rise in June.

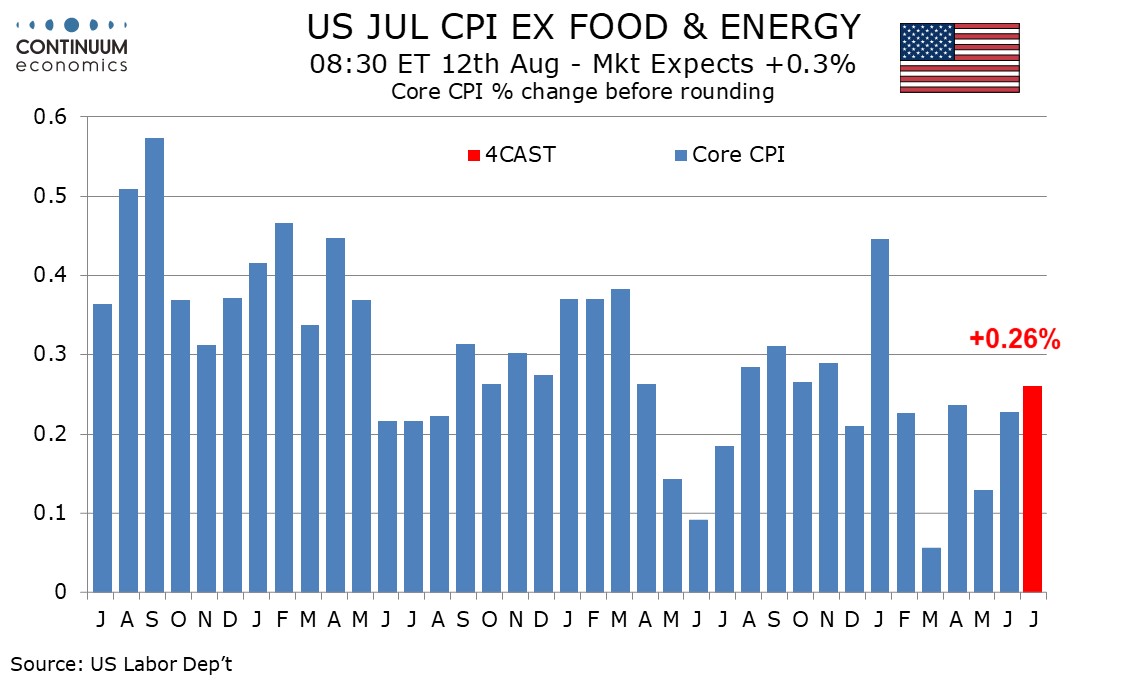

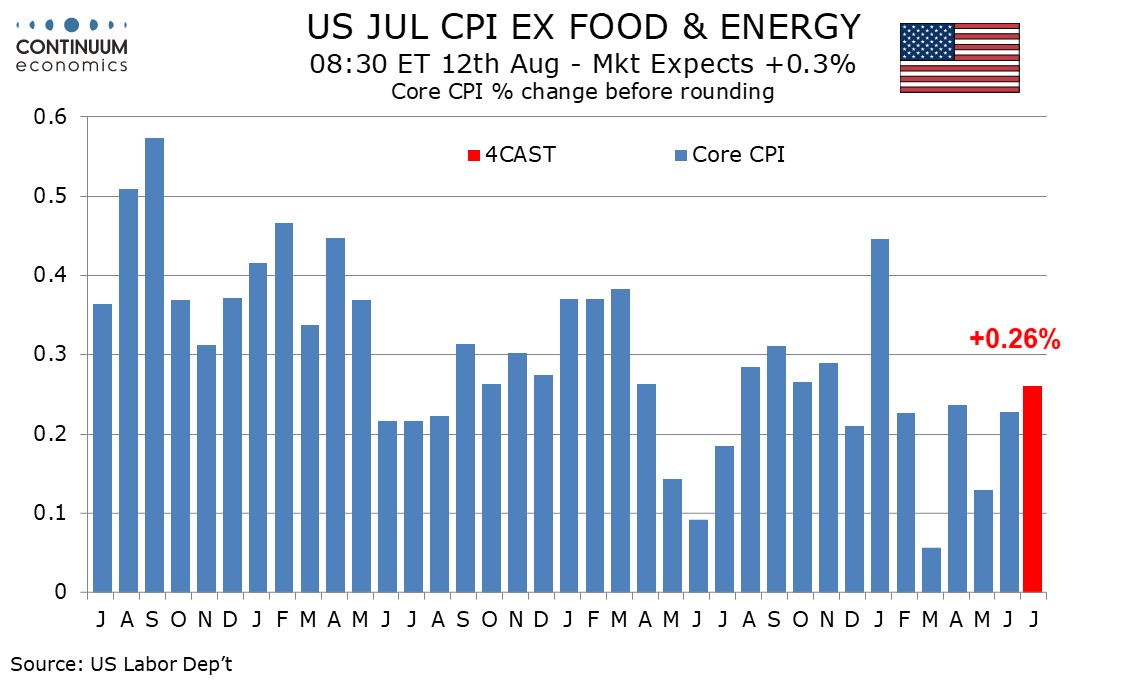

U.S. July CPI - Core rate, particularly services, a marginal disappointment

August 12, 2025 1:02 PM UTC

July’s CPI is in line with consensus at 0.2% overall, 0.3% ex food and energy, but the core rate of 0.322% before rounding is a little high for comfort. The detail shows the acceleration from June was more in services than goods, so the story is not a simple one of tariffs.

August 11, 2025

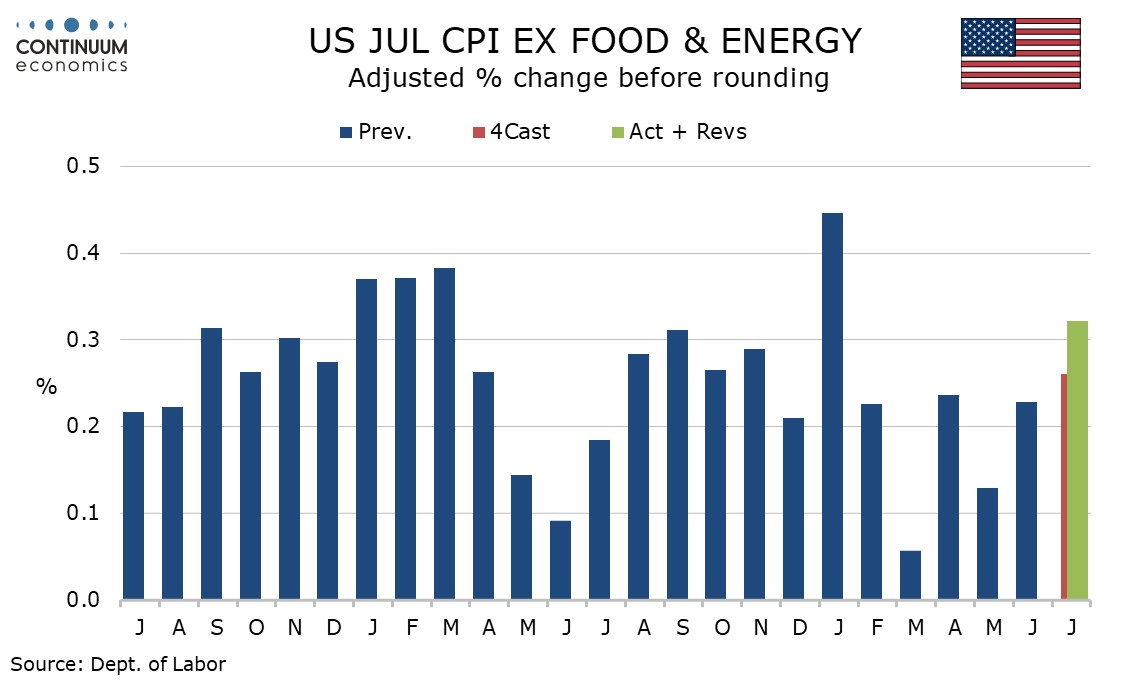

Preview: Due August 12 - U.S. July CPI - Tariff impact slowly building

August 11, 2025 1:10 PM UTC

We expect July CPI to increase by 0.2% overall and by 0.3% ex food and energy, with the overall pace close to 0.2% even before rounding but the core rate rounded up from 0.26%. This would still be the strongest core rate since January and reflect a further feed through of tariffs, something that is

August 08, 2025

August 07, 2025

EM Rates: Domestic Fundamentals Dominate

August 7, 2025 9:30 AM UTC

Once trade is agreed with the U.S., the good fundamentals actually argue for a 10yr Mexico-U.S. spread close to 400bps and this is our favored strategic risk reward for big EM government bonds. In Brazil a case can be made for a 12.75% policy rate end 2026 and 10% in 2027, but this could only mean 1

August 06, 2025

U.S. Immigration Slowdown and the Labor Market

August 6, 2025 7:58 AM UTC

Overall, slower illegal and legal immigration will likely slow employment growth and curtail the rise in the unemployment rate from the U.S. economic slowdown. More older workers or an increase in the percentage of female workers would help, but are not a priority for the Trump administration and

August 05, 2025

Preview: Due August 15 - U.S. July Retail Sales - Trend losing momentum

August 5, 2025 3:55 PM UTC

We expect a 0.1% increase in July retail sales to follow two straight declines, with 0.1% decline ex autos and an unchanged outcome ex autos and gasoline. This would restore a slowing trend after June saw a correction from declines in April and May.

June US trade deficit falls on weak imports, Canada trade deficit increases on one-time imports bounce

August 5, 2025 1:02 PM UTC

June’s US trade deficit of $60.2bn is even lower than expected, down from $71.7bn in May and in slipping marginally below April’s $60.3bn has reached its lowest level since September 2023. Exports fell by 0.5%, a second straight decline, but imports fell by 3.7%, a third straight fall as strong

DM Rates: Slowdown Debate Trump’s Independence Question for Now

August 5, 2025 9:50 AM UTC

U.S. Treasury spreads versus other DM government bond markets or 10-2yr U.S. Treasuries are not yet showing a risk premium from the Trump administration attacks on the Fed and economic data. Debate over whether the U.S. is seeing a soft or hard landing are reemerging and this will dominate the outlo

August 04, 2025

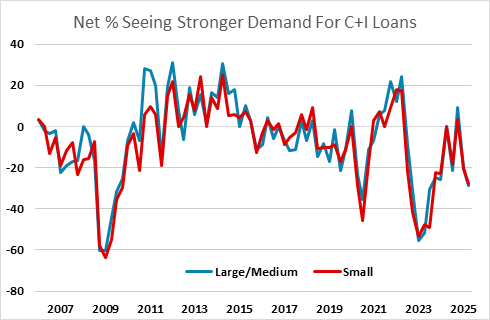

Fed Senior Loan Officer Opinion Survey Suggests Weaker Demand For Business Investment

August 4, 2025 6:44 PM UTC

The Fed’s July Senior Loan Officer Opinion Survey of bank lending practices suggests uncertainty is restraining investment demand, with supply signals on balance fairly neutral but demand signals weaker.

Preview: Due August 12 - U.S. July CPI - Tariff impact slowly building

August 4, 2025 12:47 PM UTC

We expect July CPI to increase by 0.2% overall and by 0.3% ex food and energy, with the overall pace close to 0.2% even before rounding but the core rate rounded up from 0.26%. This would still be the strongest core rate since January and reflect a further feed through of tariffs, something that is

Trump Tougher Posture with Russia

August 4, 2025 8:31 AM UTC

We suspect that Trump will not follow-through with an across the board secondary sanction on importers of Russia oil, as it would freeze U.S./China trade again and could boost U.S. gasoline prices – high inflation is one main reason for Trump’s softer approval rating. Trump could agre

August 01, 2025

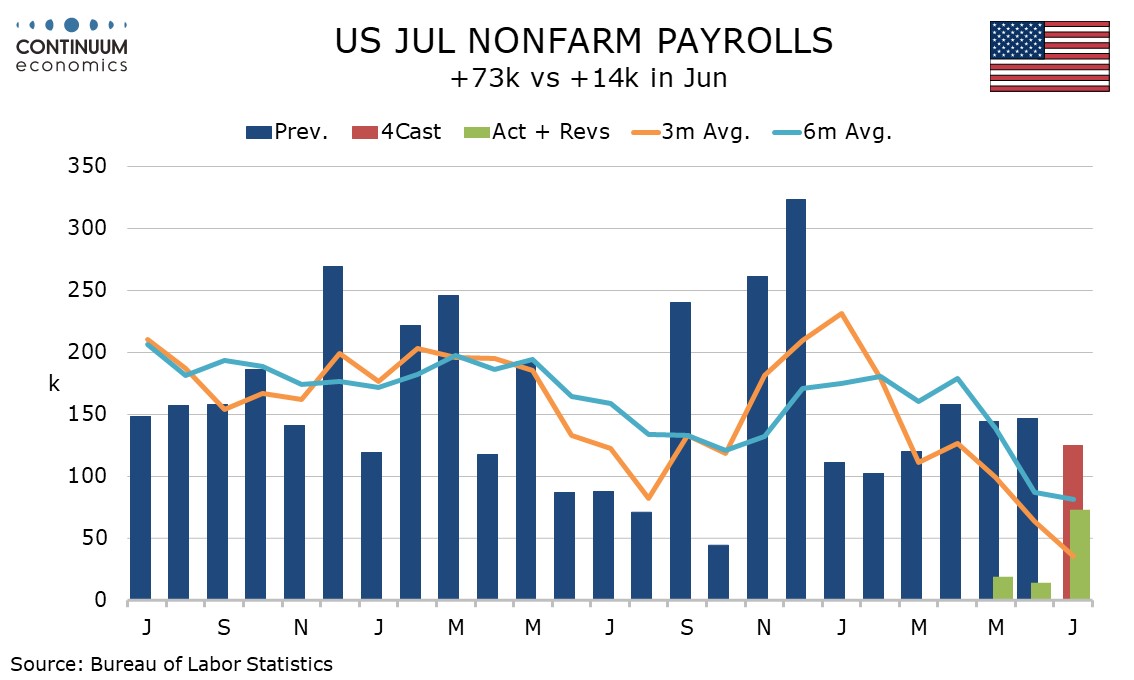

U.S. July Employment - Revisions to May and June mean trend has slowed significantly

August 1, 2025 1:06 PM UTC

July’s non-farm payroll is weaker than expected not only with the 73k headline and 83k rise in the private sector, but also with large downward revisions totaling 258k for May and June. Unemployment remains low but edged up to 4.2% from 4.1% while average hourly earnings were on consensus at 0.3%,

Reciprocal Tariffs: Some Hikes, Deals and Delays

August 1, 2025 8:40 AM UTC

Though high reciprocal tariffs with some countries catches the headline, five of the top 10 countries with large bilateral deficits have reached framework trade deals, two have delays and three have higher tariffs imposed. With exemptions on some USMCA Canada/Mexico goods, plus phones/ semicondu

July 31, 2025

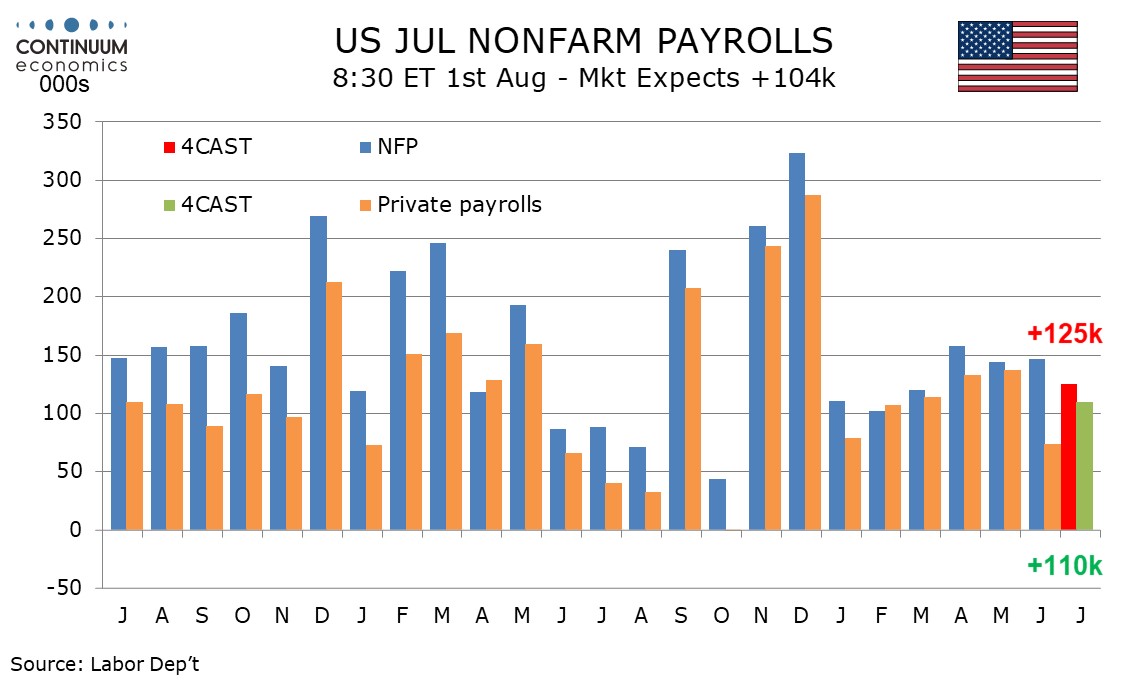

Preview: Due August 1 - U.S. July Employment (Non-Farm Payrolls) - Slower overall, but stronger in the private sector

July 31, 2025 1:26 PM UTC

We expect a 125k increase in July’s non-farm payroll, slightly slower than in each month of Q2 but slightly stronger than in each month of Q1. We expect a 110k rise in private sector payrolls, up from 74k in June but slower than in April and May. An unchanged unemployment rate of 4.1% and a 0.3% r

July 30, 2025

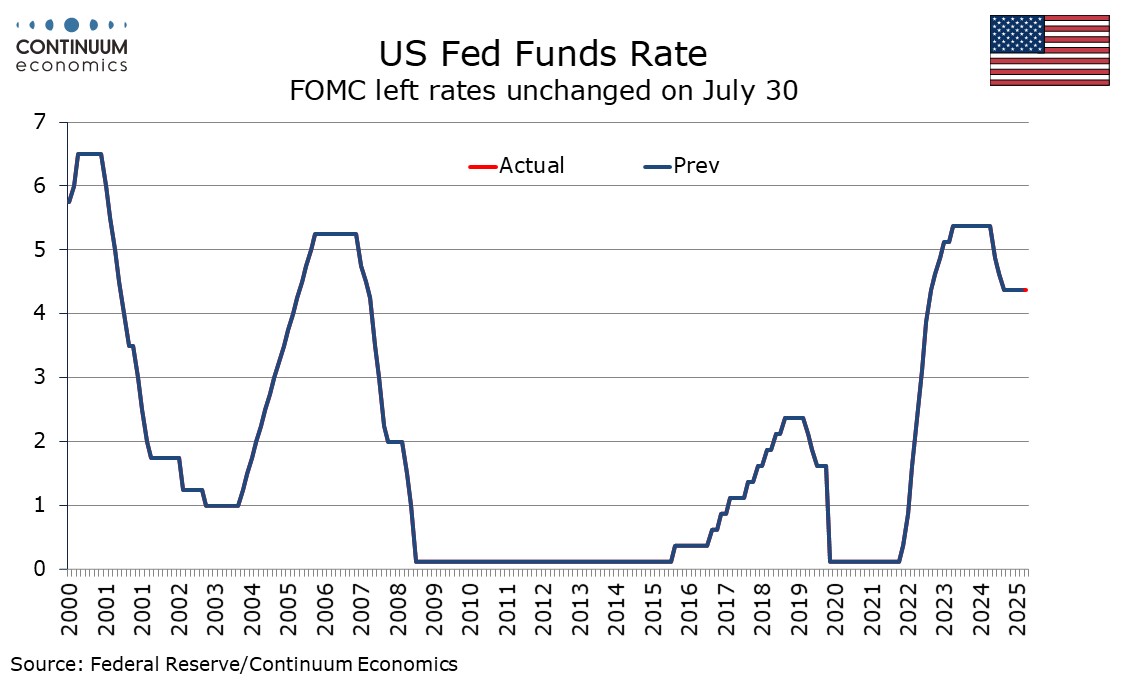

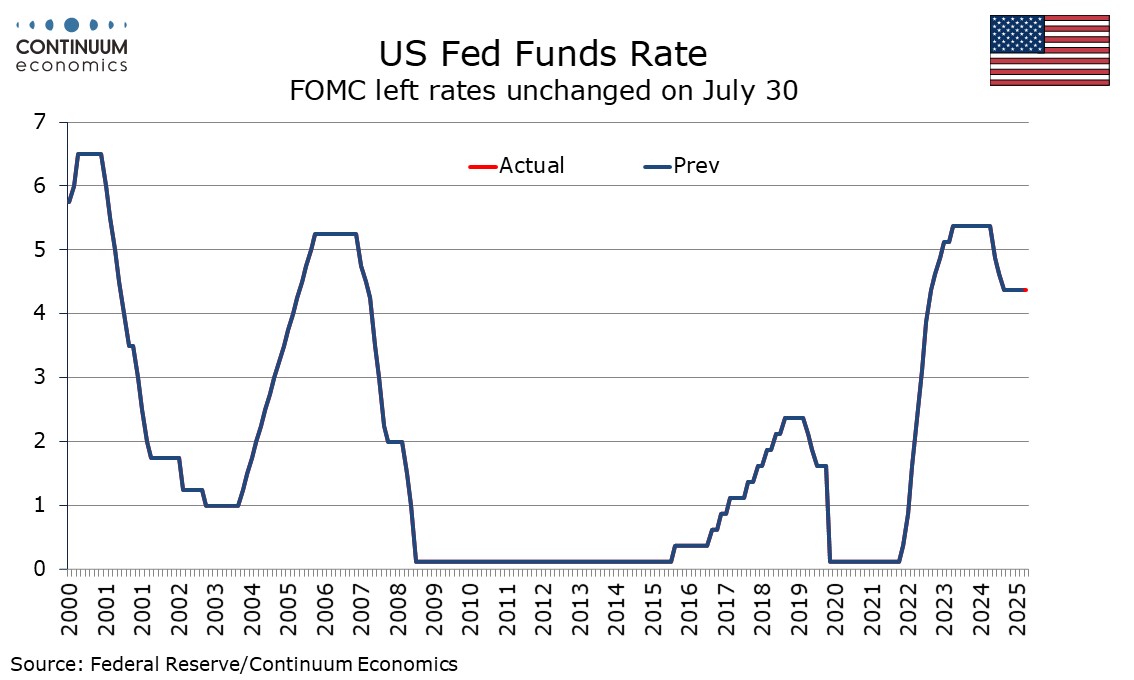

Fed's Powell Remains Cautious Over Tariff Risk

July 30, 2025 7:34 PM UTC

The FOMC left rates unchanged at 4.25-4.5% as expected, though there were two dissenting votes for easing, from Governors Waller and Bowman, who had already given signals in that direction. The statement made a concession to the doves stating that growth moderated in the first half of the year, but

FOMC leaves rates unchanged, two dissents for easing, language more dovish on growth

July 30, 2025 6:16 PM UTC

The FOMC left rates unchanged at 4.25-4.5% as expected, though there were two dissenting votes for easing, from Governors Waller and Bowman, who had already given signals in that direction. The wording of the statement also contains a dovish shift, stating that growth moderated in the first half of

Preview: Due July 31 - U.S. June Personal Income and Spending - Core PCE Prices to outpace Core CPI

July 30, 2025 1:41 PM UTC

June’s personal income and spending report will be largely old news, with Q2 totals seen in the GDP report. Ahead of the GDP report we expected a stronger 0.3% increase in core PCE prices, with a weak 0.2% rise in personal income but a solid 0.5% rise in personal spending. If these forecasts prove

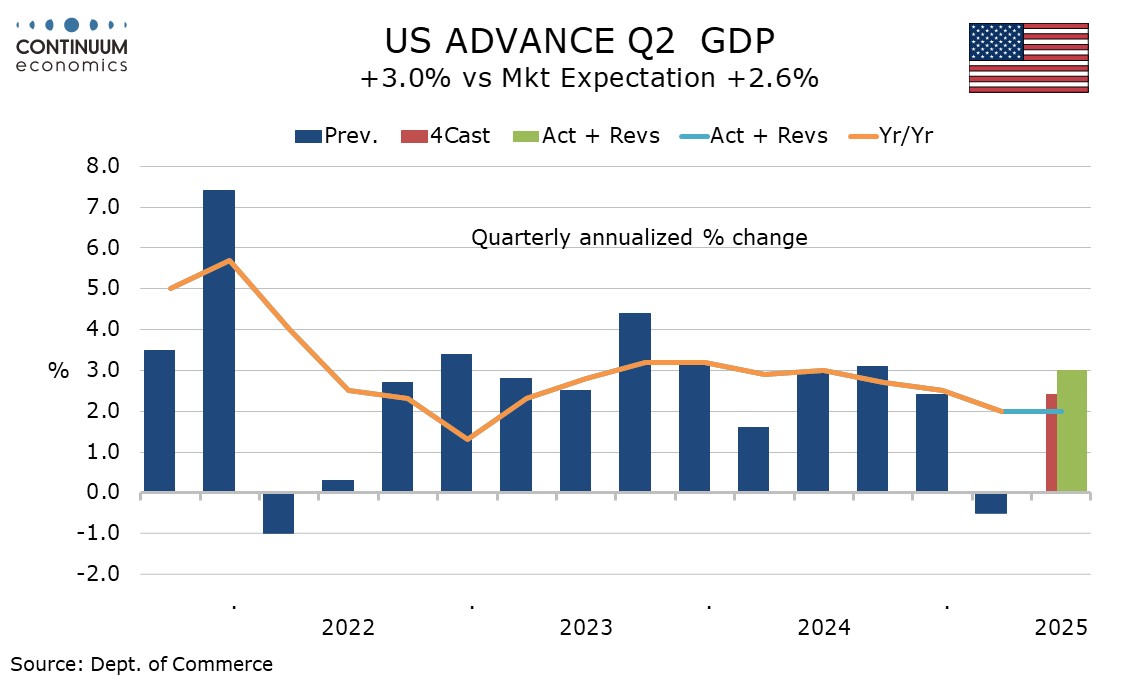

U.S. Q2 GDP - Subdued underlying growth, but with persistent price pressures

July 30, 2025 1:12 PM UTC

The advance estimate of Q2 GDP at 3.0% is stronger than expected though an above consensus outcome had looked likely after yesterday’s decline in June’s trade deficit. Given extreme volatility in net exports the Q2 data should be seen alongside Q1’s 0.5% decline, giving an average of an unimpr

Preview: Due July 31 - U.S. Q2 Employment Cost Index - Returning to pre-pandemic pace

July 30, 2025 11:42 AM UTC

We look for the Q2 employment cost index (ECI) to increase by 0.7%, after two straight gains of 0.9% and the slowest since Q2 2021. A 0.7% rise would be consistent with trend returning to where it was before the pandemic.

DM Household Sluggish Borrowing

July 30, 2025 10:45 AM UTC

· Overall, restrained credit supply from banks; abundant employment/income or wealth for most households but restrained financial conditions for low income households could have restrained household lending growth to GDP. However, the surge in government debt and ensuing fear of fut

July 29, 2025

China/U.S. Trade Talks Into the Autumn

July 29, 2025 8:20 AM UTC

· Our baseline (Figure 1) remains that a U.S./China deal will be reached (most likely in Q4), but a moderate probability exists of no deal being done this year and China being stuck with 30% tariffs – the worst-case scenario of still higher tariffs is now less likely with Trump in a

July 28, 2025

Food Glorious Food

July 28, 2025 10:15 AM UTC

· Global food prices should see small increases in the future, as production continues to rise broadly in line with increasing demand driven by population and a rising consumption per person in EM countries. However, China will remain dependent on food imports given it has limited roo

July 24, 2025

EM Currencies with a USD Downtrend

July 24, 2025 10:15 AM UTC

· BRL, ZAR and MXN have been helped by FX carry trades and bond inflows on still wide interest rate differentials. However, actual reciprocal tariff risks are high for all three countries and a wave of profit-taking could be seen. Elsewhere, though we see a U.S./China trade deal by

July 23, 2025

Trump Deals: Japan, Philippines and Indonesia

July 23, 2025 8:26 AM UTC

• Other countries cannot be guaranteed to get a Japan style deal, both as Japan is the key geopolitical ally in the Asia pivot against China and as Trump is keen to agree deals by August 1. India and Taiwan are trying to finalize deals, but the EU is more difficult. China 90 day deadlin

July 18, 2025

Trump’s and Fed Easing

July 18, 2025 9:34 AM UTC

• Trump goal of substantially lower short-term rates could be achieved with a recession, but otherwise is unlikely even when Fed chair Powell is replaced. The majority of voting FOMC members will make decisions based on economics not politics. However, Trump fixation with lower rates an

July 17, 2025

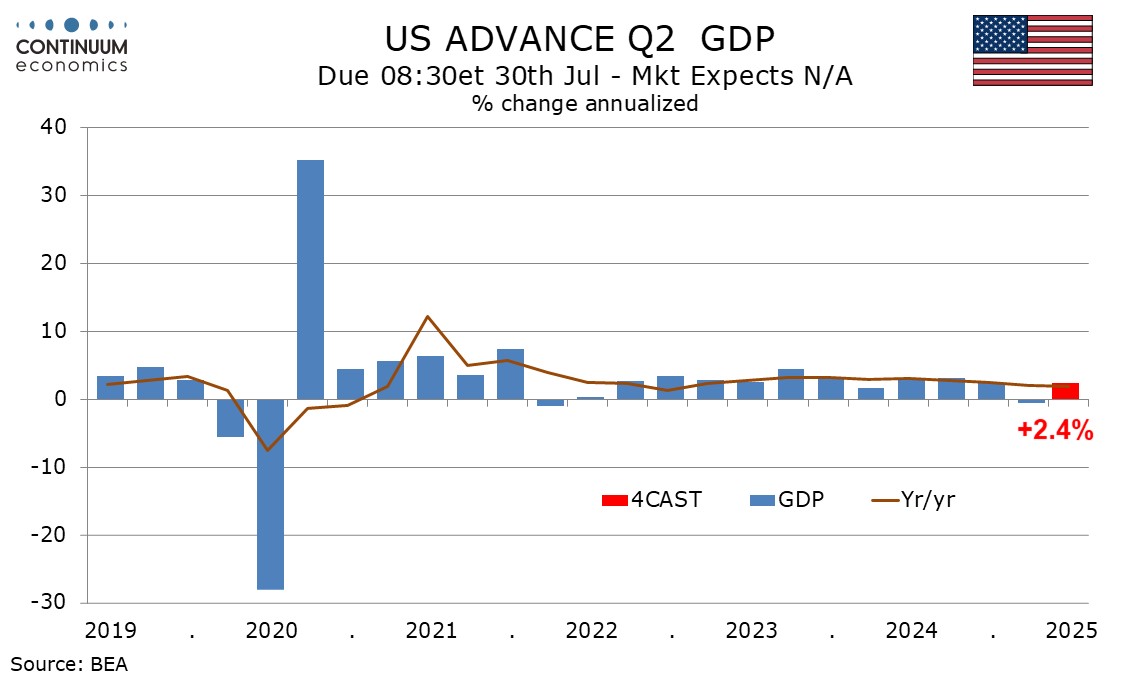

Preview: Due July 30 - U.S. Q2 GDP - Rebounding from a negative Q1, but a subdued first half of the year

July 17, 2025 5:54 PM UTC

We expect a 2.4% annualized increase in Q2 GDP, which after a 0.5% decline in Q1 would leave the first half of the year rising at a pace close to 1.0%. A similar pace may be seen in the second half of the year if tariffs persist. Our Q2 forecast has been lifted from 1.4% on a generally improved tone