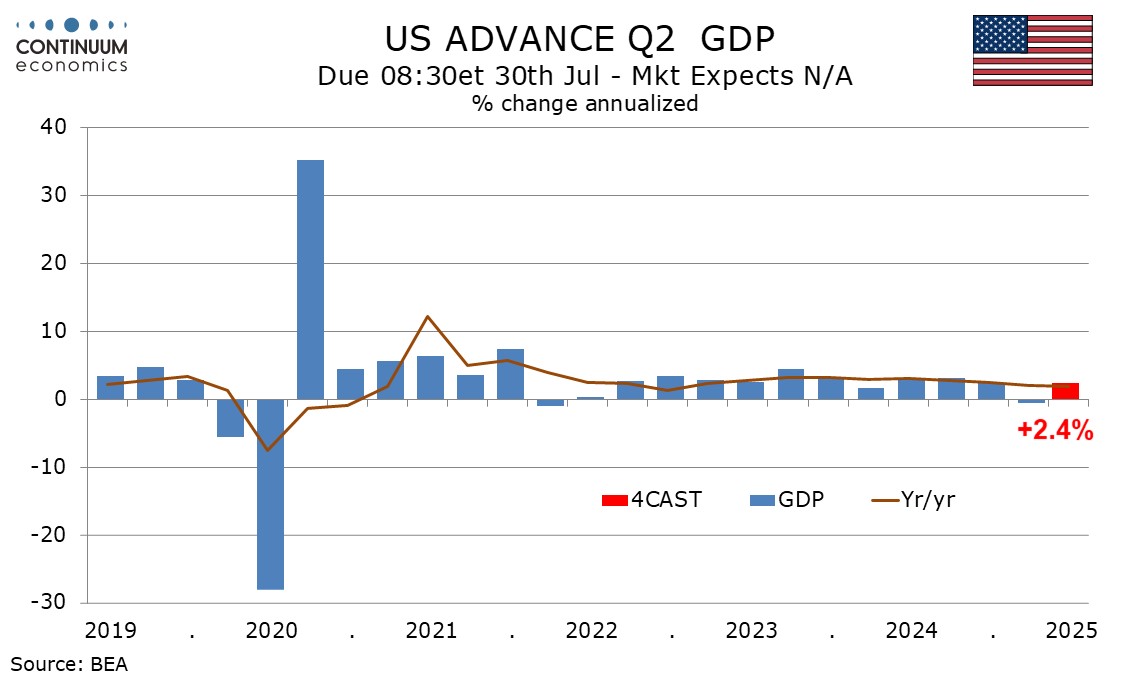

Preview: Due July 30 - U.S. Q2 GDP - Rebounding from a negative Q1, but a subdued first half of the year

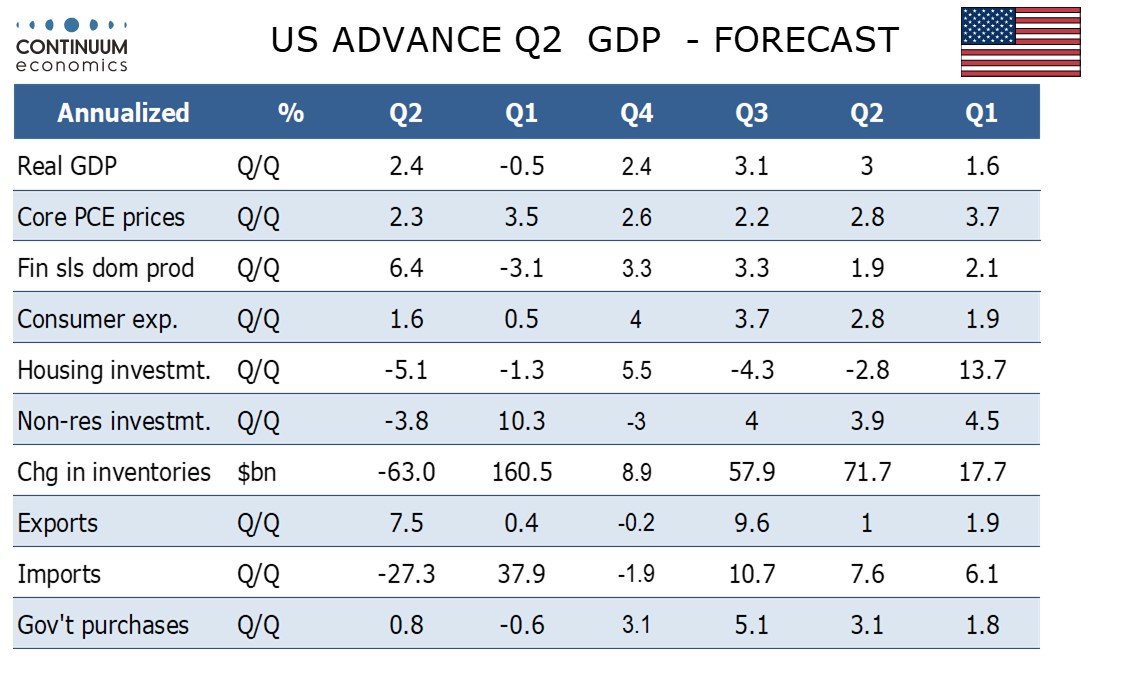

We expect a 2.4% annualized increase in Q2 GDP, which after a 0.5% decline in Q1 would leave the first half of the year rising at a pace close to 1.0%. A similar pace may be seen in the second half of the year if tariffs persist. Our Q2 forecast has been lifted from 1.4% on a generally improved tone to June data to date.

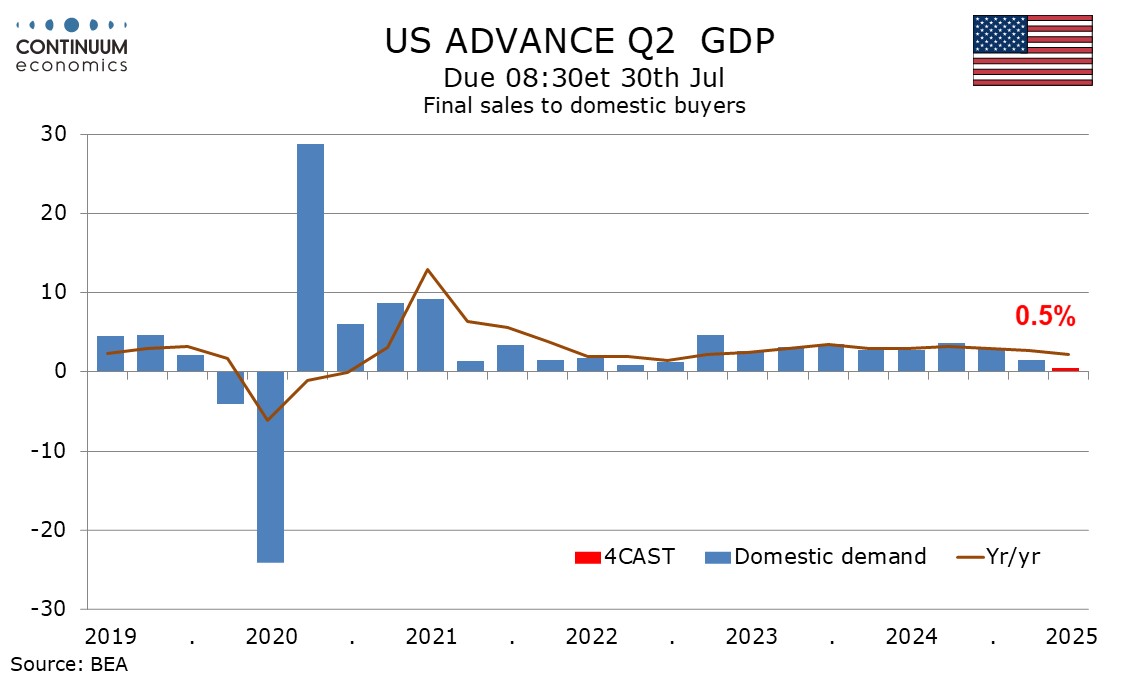

We expect final sales to domestic buyers (GDP less inventories and net exports) to rise by only 0.5% after a 1.5% increase in Q1, also averaging near 1.0%.

We expect consumer spending to rise by 1.6% after a 0.5% increase in Q1, with April and May having produced subdued data but retail sales picking up in June. We also expect firmer services data in June, but this will leave services up by only 1.1% in Q2, matching the pace we expect from non-durables. We expect a 5.1% rise in durables, correcting from a Q1 decline. We expect consumer spending to underperform real disposable income, where we expect a rise of 2.7% after a 2.5% increase in Q1. Anxiety over the impact of tariffs may have encouraged consumers to save more.

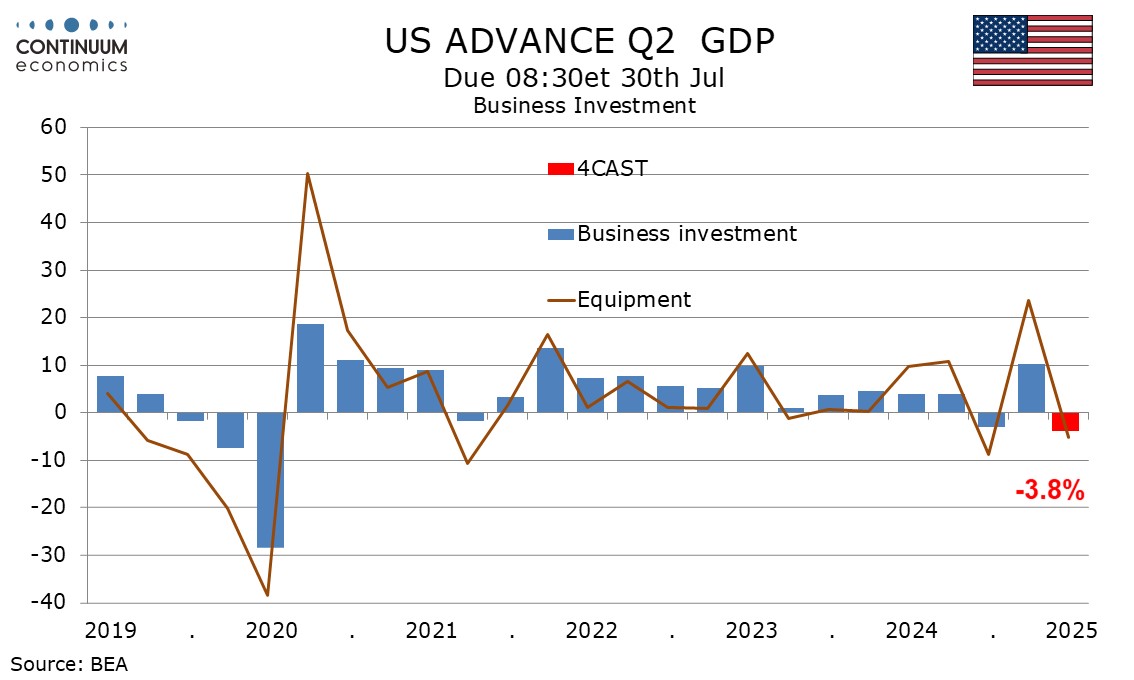

Business investment was very strong in Q1 with a 10.3% rise which appears to reflect pre-tariff front loading. We expect a 3.8% decline in Q2. Non-residential structures are likely to extend a 2.4% dip seen in Q1, we expect by 6.0%, but corrections in equipment, falling by 5.1%, and intellectual property, by 2.4%, are likely to be moderate compared to respective Q1 gains of 23.7% and 6.0%.

Private sector construction appears to be slowing generally, and this is likely to see increased weakness in residential investment, falling by 5.1% after a 1.3% Q1 decline. However there has been resilience in public construction. We expect government to rise by 0.8% after a 0.6% decline in Q1, led by state and local. We expect a second straight negative from Federal government, though defense is likely to be less negative than in Q1.

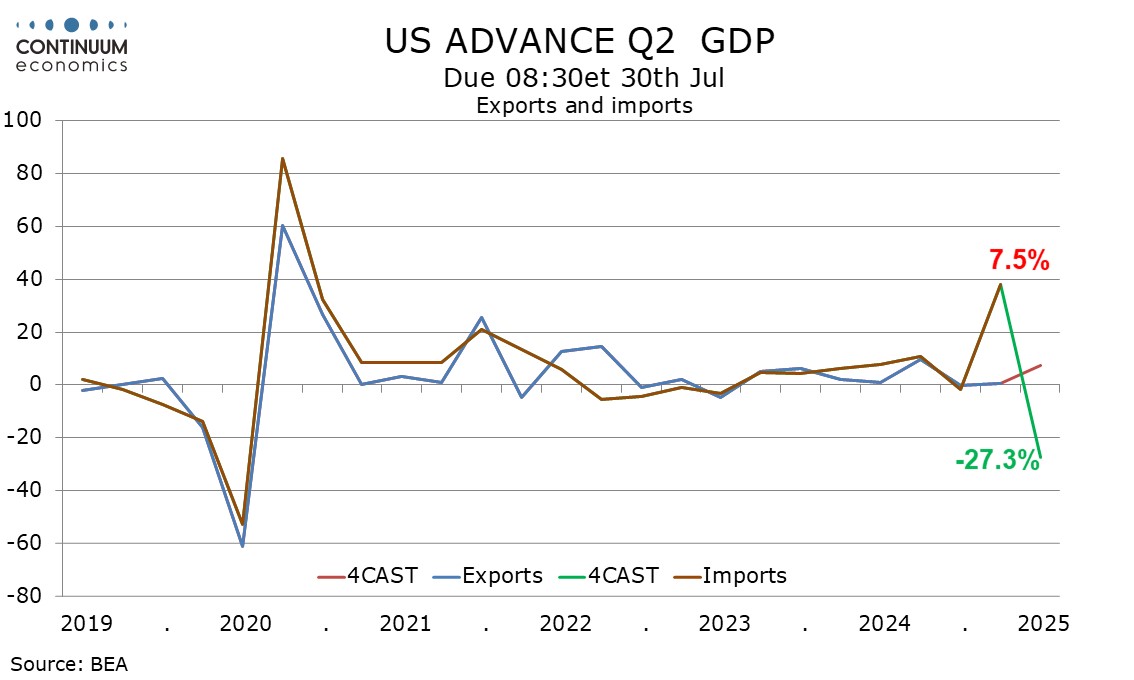

We expect net exports to add a huge 5.9% to Q2 GDP, more than fully reversing a negative of 4.6% in Q1. We expect a strong 7.5% rise in exports after a gain of only 0.4% in Q1, the acceleration assisted by a rebound in services from a weak Q1. We expect imports to plunge by 27.3%, with the level almost fully reversing Q1’s pre-tariff surge of 37.9%, even if the annualized decline from a sharply higher level will not be as steep as Q1’s annualized increase.

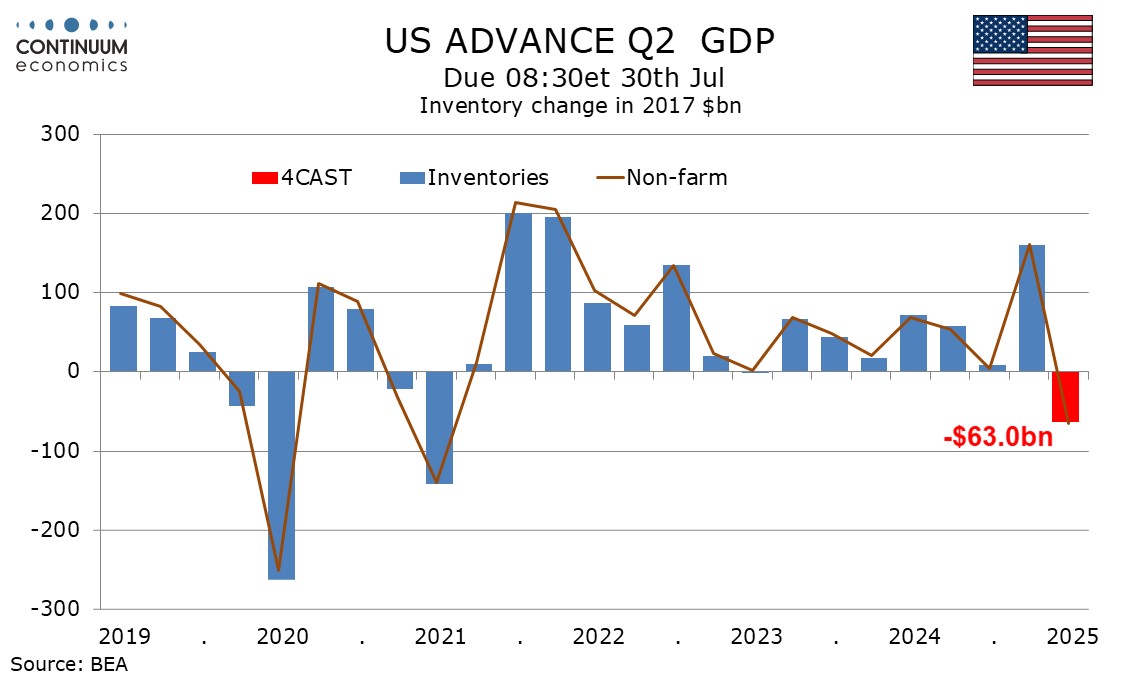

We expect final sales (GDP less inventories) to rise by 6.4% after a 3.1% decline in Q1 as inventories take off 4.0% from GDP after a 2.6% positive contribution in Q1. The Q1 surge in imports went mostly into business investment and inventories, which will correct lower as imports do, offsetting some of the boost to GDP coming from net exports.

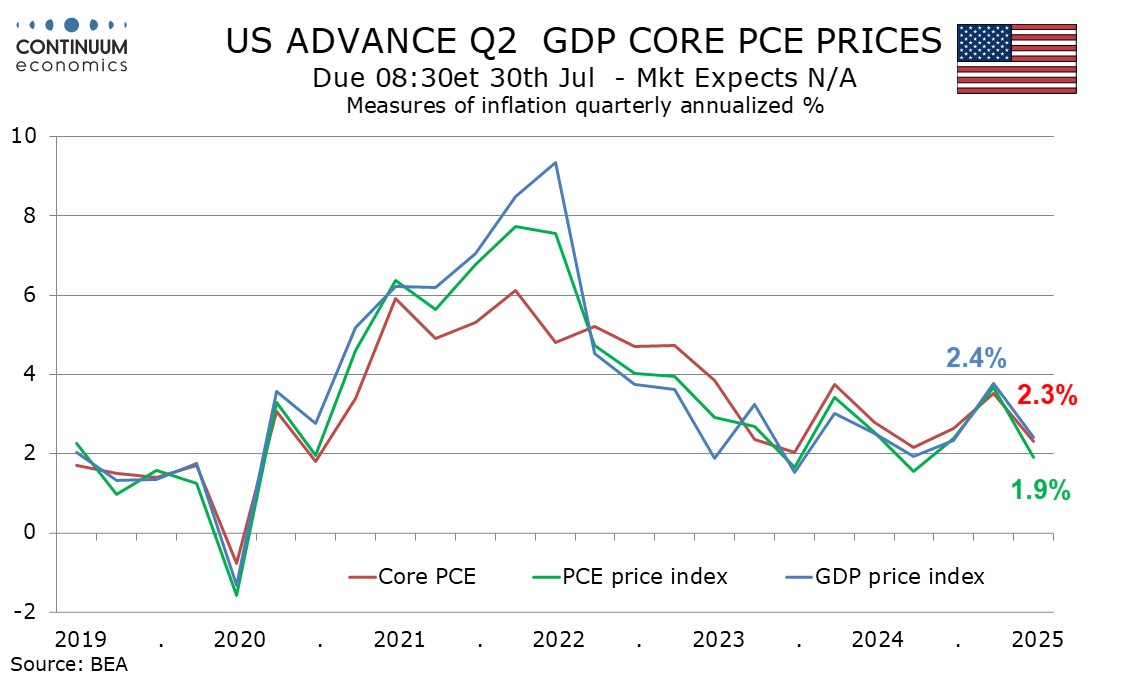

We assume a 0.3% increase in June PCE prices both overall and core, with tariffs beginning to feed through. This would leave annualized gains of 1.9% for overall PCE prices and 2.3% for the core rate in Q2, close to the 2.0% target but with the core rate not quite there. We expect Q3 data to be stronger as tariff-feed through picks up. We expect a 2.4% increase in the overall GDP price index in Q2.