Trump and Dollar Policies

The Trump administration could decide to more broadly talk the USD down or less likely try to reach a cooperative Mar A Lago accord with big DM and EM countries. A more cohesive alternative is a forced currency deal for countries to appreciate their currencies to avoid more tariffs and withdrawal of U.S. military security guarantees. Worst case alternative would force foreign central banks to swap short-dated U.S. Treasuries into 100yr bonds i.e. a debt reprofiling that is a partial debt default with toxic consequences. The most likely approach is more complaints that certain currencies are too weak and some USD jawboning. Trump hates multilateral approaches and loves a bilateral focus.

President Donald Trump has started complaining about the weak Japanese Yen (JPY) and Chinese Yuan (CNY). What next for Trump’s USD policy?

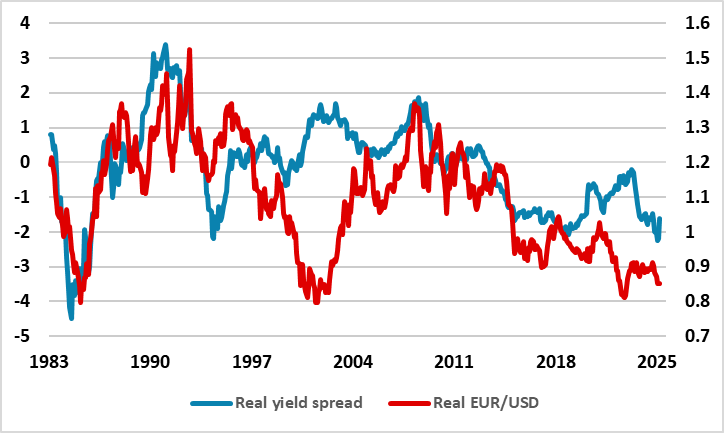

Figure 1: Real EUR/USD (RHS) and Real 10yr U.S.-Germany Government Bond Spread (LHS)

Source: Continuum Economics

Speculation is growing that the Trump administration will try to engineer a lower USD to help improve the U.S. trade position alongside tariffs and other policies. Key points to note

· Your currency is too weak. Trump this week has said of Japan and China that you cannot continue to reduce and break down your currency and that it is unfair to the U.S. Trump then noted that the U.S. response will be higher tariffs. This is targeted bilateral pressure that Trump loves and is designed to get other countries to raise the value of their currencies against the USD. The JPY is seeing a recovery and we actually see a move to 135 this year on further BOJ hikes; Fed easing; rate spreads and the U.S. losing the perception of exceptionalism. For USDCNY, we see a move to 7.45 given already large interest rate differentials (here), but unlike 2018 China is not undertaking noticeable depreciation despite 20% extra tariffs from the U.S. – China will not be keen on a Yuan appreciation however. The Euro (EUR) could get similar verbal intervention from Trump at some stage.

· Talking the USD down and more Fed rate cuts. A broader approach is to say that the value of the USD is currently too high (true) but that the U.S. still believes in stable inflation for a “strong” USD. The U.S. has done this in the past, with the most well known being the 1985 Plaza accord (Trump later bought and sold the hotel). In 2003, U.S. Treasury secretary Snow jawboning led to a USD decline (here), when the USD was overvalued compared to interest rate differentials – see Figure 1 for EUR/USD. The USD currently looks overvalued relative to real interest rate differentials of select DM currencies (JPY and EUR). Trump or Bessant jawboning the USD would have some impact in hurting the USD initially. However, in general, FX policy is hard to enact effectively independent of monetary policy. The Plaza and Louvre accords which affected the value of the USD in 1985 and 1987 respectively saw the USD decline and then stabilize because monetary policy was in part focused on FX policy. In a world of inflation targeting by central banks it will be hard to get FX policy to work in this way. However, when FX values are deviating from fundamental relationships with value and yield spreads, intervention (verbal or actual) can have an impact in bringing currencies back into line. In 2025, much depends on what the Fed is doing relative to other central banks, which at the moment is only really narrowing rate differentials versus Japan. A U.S. hard landing would see aggressive Fed easing and associated USD decline, but that depends on economic data. One associated issue to watch for is Trump pressuring the Fed to cut rates if the equity market says see a 10% peak to trough decline like 2018. This would hurt the USD initially, though the Fed would be reluctant to become politicised.

· Cooperative Mar A Lago accord. Steve Miran the president’s CEA advisor has pushed this idea (here) in various forms. One form is a cooperative Mar A Lago accord like the Plaza accord. The problem is that as well as FX intervention this could require reducing interest rate differentials e.g. Fed cutting and ECB hiking! Additionally, big EM currencies are also now important unlike 1985. It is unlikely that India, China and South Africa push to appreciate their currencies versus the USD or hike rates to help lower the value of the USD. Countries outside the U.S. are also not in a cooperative spirit with actual tariffs against Canada/Mexico/China, steel and aluminium from March 12 and more product and reciprocal tariffs from April. Finally, Trump hates multilateral approaches and loves a bilateral focus.

· Forced Mar A Lago deal. One other idea floating around the Trump administration is that the U.S. forces a deal with threats. Appreciate your currency or else face more tariffs and withdrawal of U.S. security guarantees. Do as the U.S. wants and you face less tariff threat and continued U.S. military protection. Japan/S Korea and Taiwan would be very fearful of losing the U.S. military security guarantee and feel pressured. However, European countries have already decided that the Trump administration cannot be trusted with Europe defence and hence the huge effort to boost Europe defence spending in the last few weeks. How this cohesive approach would work with big EM countries is unclear e.g. India/S Africa/Brazil. It would led private investors to fear more toxic solutions (see below) and this could backfire on U.S. financial markets.

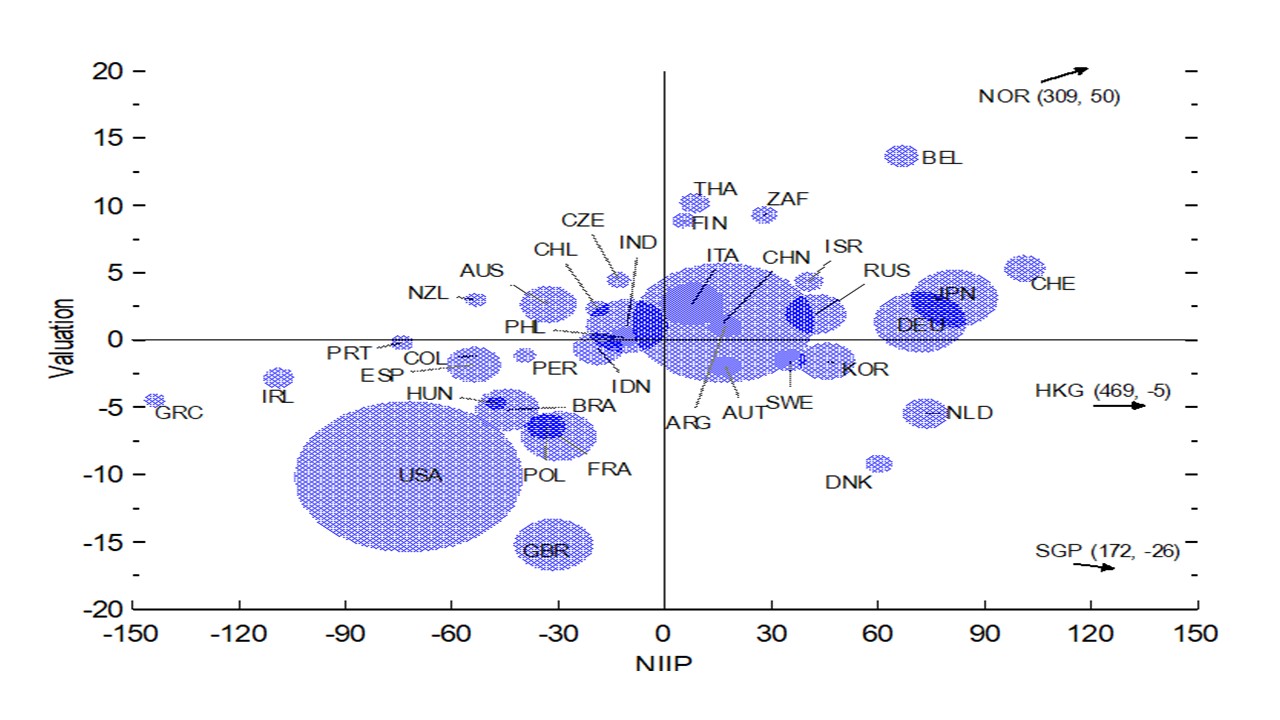

· Swapping your U.S. Treasuries into 100yr bonds or charging a withdrawal fee. Two other ideas floated by Miran are swapping foreign central bank holdings into 100yr Treasuries or perpetual bonds or charging a withdrawal fee (e.g. for coupon payments). The former if forced would a debt reprofiling, which the UK effectively did in 1932 after World War 1 or Greece did after the 2010 crisis. This is technically a partial debt default, which would see private holders around the world dump U.S. Treasuries; surge U.S. nominal and real yields and cause a U.S. equity market crash/U.S. recession. If voluntary it would led to dumping of Treasuries and a surge in U.S. bond yields! The 2 idea of charging a withdrawal fee to foreign holders is also toxic to overseas holders and would led to sharp reduction in overseas holdings of U.S. Treasuries. These ideas are a disaster for a large debtor country that depends on foreign holders. The U.S. net international investment position is estimated by the IMF ESR to be 70% of GDP in 2023 – a high level already (Figure 2). You do not want to upset your creditors.

Figure 2: Net International Investment Position (NIIP) and Valuation Changes for NIIP 2023 (% of GDP)

Source: IMF ESR 2024