Trump Product and Reciprocal Tariffs

It appears that we will get bad news from April 2 on extra tariffs before any good news. Firstly, the announcement effect of tariffs for many countries and extra products will hurt U.S. business and consumer sentiment. Secondly, part of the reason for tariffs is extra tax revenue and to try to shift production back to the U.S., as well as negotiating trade deals. This means some tariffs are permanent, while trade deal negotiations are at an early stage. H2 will likely be adverse for the U.S. economy and could cause renewed caution and selloff in the U.S. equity market.

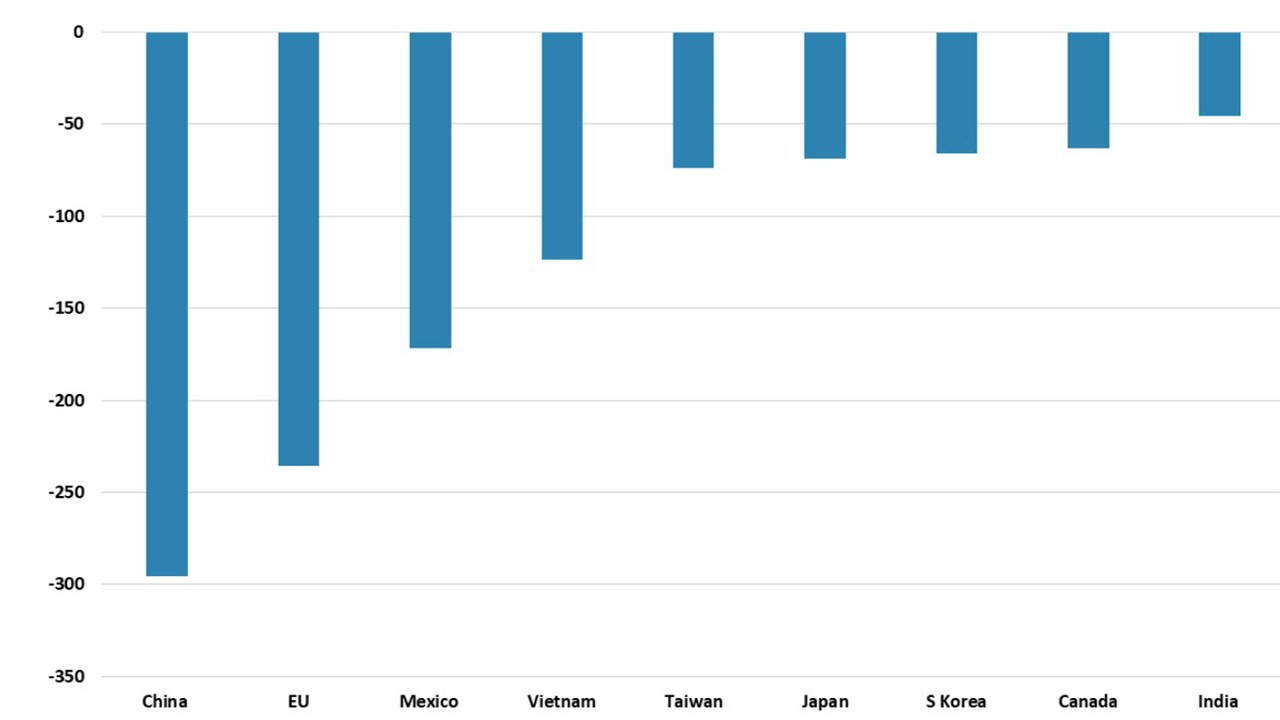

Figure 1: U.S. Bilateral Trade Deficit 2024 (USD Blns)

Source: BEA/Continuum Economics

The days are counting down to the April 2 announcement on product specific and reciprocal tariffs, with much uncertainty on the latter. Key points include.

· Cars/Pharma/Semiconductors and Lumber at 25%? President Donald Trump has signaled that he is likely to impose 25% tariffs on cars/pharma/semiconductors and lumber and confirm this on April 2. How long the delay is before implementation is a key question. The gap for steel and aluminum at 25% was quite short and no exemptions were made for countries or sub products showing a hard line stance. It will be interesting to see whether these product categories are weeks or months, as the latter could allow scope for negotiations. Additionally, it is also unclear whether these will apply to USMCA covered goods with Canada and Mexico such as cars, where production is so integrated into U.S. supply changes. Part of this uncertainty is whether Trump wants trade deals or tax revenue and a shift of production into the U.S. – we feel both given Peter Navarro guidance and this means some tariffs are permanent. Uncertainty also reflects the on-off nature of the 25% overall tariffs with Canada/Mexico.

· Reciprocal tariffs. Last week key administration officials were reported to be looking at low, medium and high level of tariffs for countries to simplify the reciprocal tariff process according to the WSJ. However, this has currently been dismissed to be replaced by a plan for individual tariffs for each country. If this was a percentage that only reflected tariffs, then this would only have small to modest impact on individual countries – though cumulative it would impact the U.S. more, as the U.S. would be imposing on all trading patterns. However, Peter Navarro has been reported as being very keen for these reciprocal tariffs to include VAT, which could add 10-20% to the tariffs and make them heavy for Mexico/EU (Canada VAT is 5%). Additionally, uncertainty exists whether country/product and reciprocal tariffs would be cumulative, which for Mexican cars with reciprocal tariffs based on VAT would be penal! Finally, it remains unclear whether implementation will be weeks or months, with U.S. Treasury secretary Bessant indicating that the U.S. will negotiate with countries for them to reduce tariffs to get lower reciprocal tariffs and the main focus was on a dirty 15 countries – likely the largest bilateral deficits (Figure 1). India has already cut some tariffs for this reason.

We will watch for developments before and on April 2. It appears that we will get bad news before any good news. Firstly, the announcement effect of tariffs for many countries and extra products will hurt U.S. business and consumer sentiment. Spending will also be hit when they are implemented, as price rise suppresses demand and production take time to switch to the U.S. We are also uncertain whether U.S. and overseas businesses will scale up production at the pace that the Trump administration expects. Secondly, part of the reason for tariffs is extra tax revenue and to try to shift production back to the U.S., as well as negotiating trade deals. Negotiations on revising the USMCA with Canada and Mexico is only starting, while U.S./China negotiations on a revised trade deal are reported to be stuck at a low level. Meanwhile, Trump appears to want a trade war with the EU, who he hates.

We do feel that trade deals negotiations will start with Canada/Mexico and China by the summer and so the news flow will start to get less bad, but H2 will likely be adverse for the U.S. economy as tariffs feedthrough and could cause renewed caution and selloff in the U.S. equity market (here).