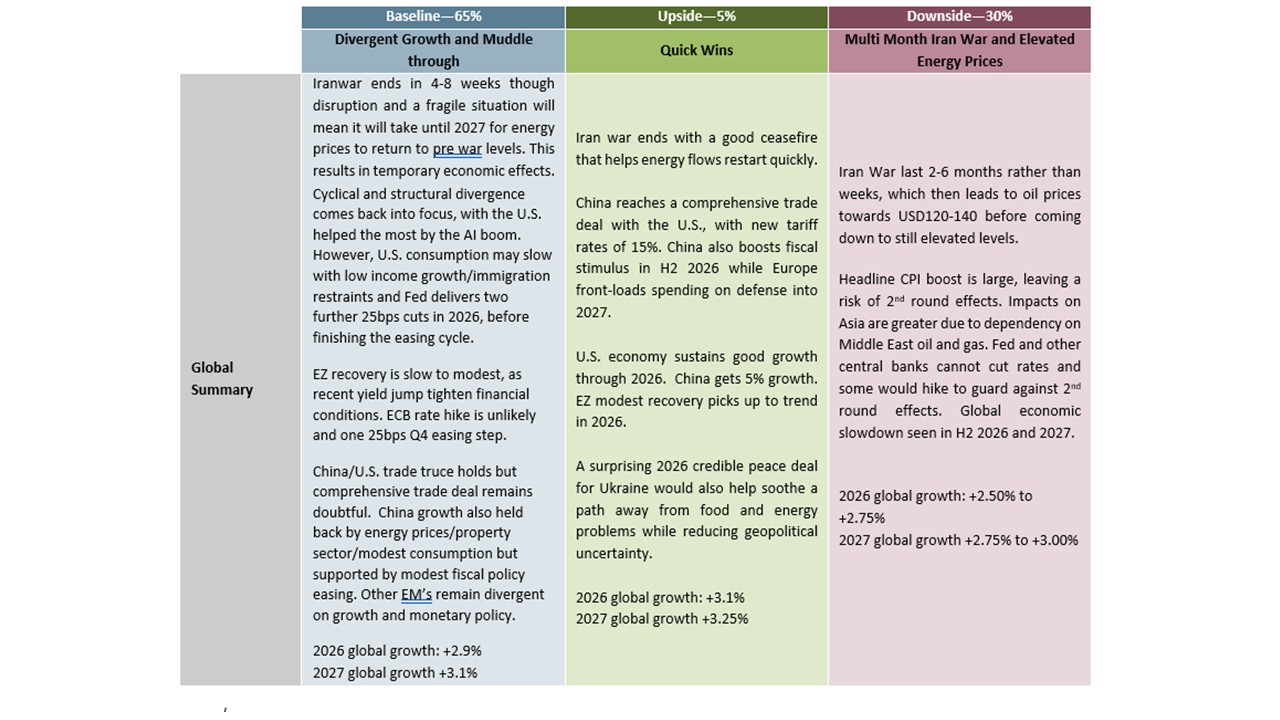

Outlook Overview: Iran War and AI Challenges

· The Iran war macro impact depends on length of the conflict and impact on energy flows. Our baseline is for a 4-8 week Iran war, with WTI down to USD80-85 by June; USD65-70 end December and USD60 by Q3 2027 (here). The jump in oil and gas prices mean at least a temporary increase in inflation to this supply shock. This certainly pauses plans for rate cuts for the spring in some DM countries. However, DM domestic demand is weaker than it was in 2022, monetary policy is less accommodative and labor markets are slacker. This suggests that 2nd round effects should be small and some disinflation could appear into 2027 from increasing spare capacity. For the Fed this delays two 25bps cut until September and December, as lower effective tariffs also help temper core inflation. Meanwhile, EZ and UK financial conditions are tightening quickly without policy rate hikes and given a 4-8 week war we feel that actual tightening will not be seen. European gas prices are high but nowhere near the super spike seen in 2022-23. As energy prices ease in H2, disinflation can be enough to deliver a 25bps cut from the ECB and BOE in Q4 2026. In contrast we see one further 25bps hike from the BOJ, before a prolonged hold as inflation slows below 2% in 2027.

· EM countries focus is also on the energy price shock. However, the experience during the Ukraine war suggests that EM central banks should be able to avoid 2nd round effects, especially as some labor market slack now exists in most major EM economies. EM central banks will likely want to avoid rate hikes. China’s inflation forecast is revised up, but at 1.4% is controlled and we still see a 10bps seven-day reverse repo rate cut in 2026. GDP growth is forecast at 4.2%, supported by high-tech manufacturing but consumption will be modest. India is somewhat more vulnerable to temporary increase in energy prices in terms of higher inflation and a headwind to growth for 2026, which should see a dovish RBI reluctant to react. Elsewhere, the temporary effects of the Iran war will likely slow the pace of easing in Brazil and South Africa.

· The structural story from AI should also not be ignored, with a boost to U.S. growth via the semiconductor/data center boom. Cyclical productivity has improved in the U.S. but it is difficult to attribute this to AI alone, as tech usage has accelerated during and after the COVID pandemic. Policymaking will also face a question of whether some disinflation benefits arrive soon or occur in the coming years. Most critically, will labor shedding be modest in aggregate (our baseline) or more rapid that has adverse income/consumption impacts. Our view at this juncture is that the pace is somewhat quicker than the internet revolution that should bring some disinflation benefits in the next 1-2 years. However, benefits will be skewed toward the U.S. where the quickest and broadest adoption is occurring.

· Outside of Iran, geopolitics will look at Taiwan. Though President Xi will likely ask Trump not to get involved in Taiwan reunification, Trump administration officials will likely ensure that Trump does not drop the strategic ambiguity policy when they eventually meet. Odds of a China attack on Taiwan remain at 5-10% for 2026-27, given the very high risks involved. Meanwhile, we believe that a Russia-friendly peace deal in Ukraine could eventually arrive by H1 2027 due to exhaustion, with only a 30% chance of occurring this year. Elsewhere, the Donroe doctrine should also be watched closely, as Trump adventurism is likely to still leave him inclined to pressure Cuba and Greenland later this year – though more military action is unlikely following the Iran war problems. We would still suspect that U.S./Europe could find a negotiated solution for Greenland (here), while Trump will also be preoccupied with the mid-term elections in November.

· For financial markets, a 4-8 week Iran war will likely see inflation fears reduced and allowing 2yr yields to undiscount tightening. In H2 start to speculate on rate cuts again in the U.S. and to a degree in EZ/UK. U.S. 10yr yields can see a slight reduction but are unlikely to fall below 4%, while German fiscal spending means that 10yr Bund yields will remain sticky around 3%. 10yr JGB yields will keep rising however, as the BOJ QT reaches close to 6% of GDP but this will likely force a BOJ QT U turn by mid-year. U.S. equities may have less fears over Iran by the spring, but are overvalued still and vulnerable to consumption slowing down to the weaker pace of income growth. However, by the end of 2026 we forecast a rebound in the S&P500 to 7200. In terms of 2027, U.S. job losses from AI could be more noticeable and cause a fear factor among consumers that dents consumption and growth. The economic cycle will also be more mature. This risks a new deeper correction in the overvalued U.S. equity market. We see the S&P500 to 7000 by end 2027. Other DM equity markets and China will find it difficult to outperform the U.S. in 2026, as markets are no longer cheap. India equities could start to see some recovery in H2 2026, with fwd P/E ratio less overvalued. In FX, the USD can see a slow decline resuming versus most DM currencies, with the AUD and NOK remains our favorite on valuation; structural fundamentals and policy rate grounds. JPY is also extremely undervalued and could snap higher.

· Risks to our views: A 2-to-6 months Iran war can spike WTI to USD 120-180 (depends on duration of the war and further damage) and remain elevated for the remainder of 2026. This would prompt a stagflation hit to the global economy; cancel interest rate cuts and in some cases prompt modest rate hikes to lean against 2nd round effects. It would likely stop the Fed from easing further initially. However, if the shock caused a U.S. recession, then the Fed would cut policy rates to 2% or lower, which would see 2yr yields drop but sharp yield curve steepening and a U.S. equity bear market. Fiscal policy would provide less of a buffer due to limited fiscal space in most major countries, except balance sheet strong DM countries.

Figure 1: Economic Scenarios

Source: Continuum Economics

Market Implications

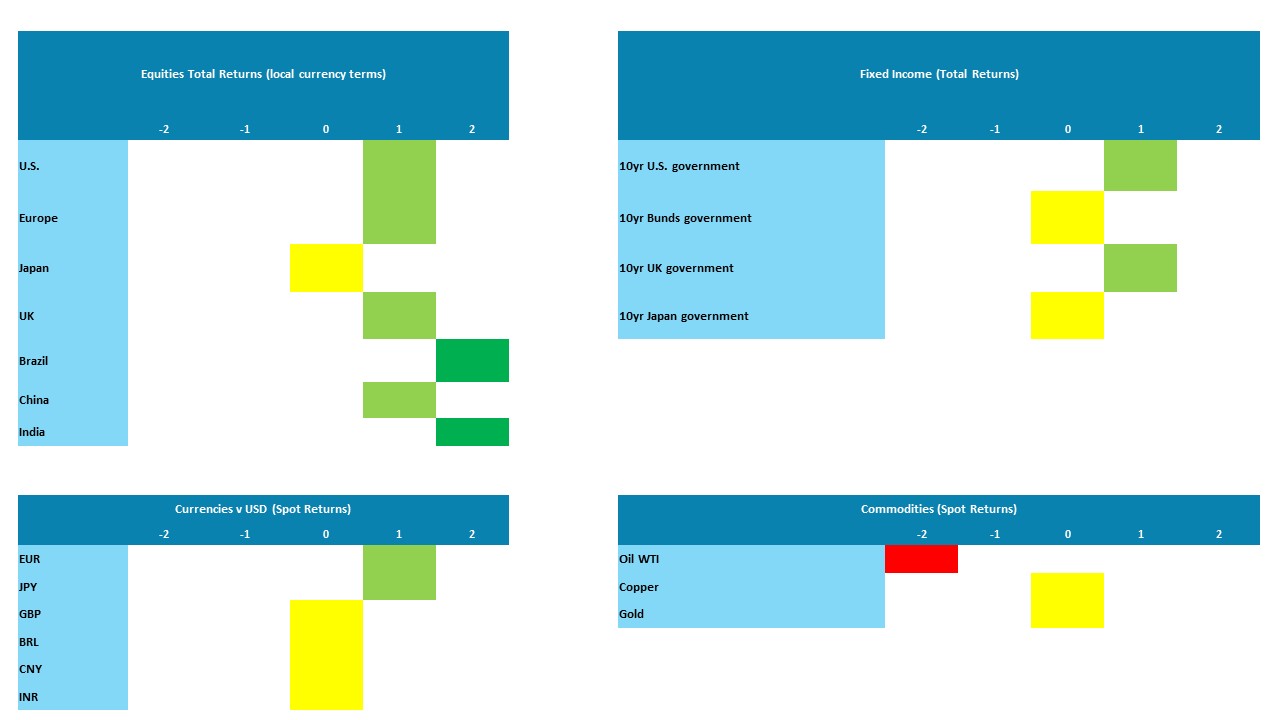

Figure 2: Asset Allocation for the Next 9 Months

Source: Continuum Economics Note: Asset views in absolute total returns from levels on March 23 2026 (e.g., 0 = -5 to +5%, +1 = 5-10%, +2 = 10% plus).

· Government Bonds. A 4-to-8 week war will likely reduce inflation fears and allowing 2yr yields to undiscount tightening and in H2 start to speculate on rate cuts again in the U.S. and to a degree in EZ/UK. U.S. 10yr yields may see a slight reduction but are unlikely to fall below 4%, while German fiscal spending means that 10yr Bund yields remain sticky around 3%.

· Equities. U.S. equities may have less fears over Iran by the spring, but are overvalued still and vulnerable to consumption slowing down to the weaker pace of income growth. 6000 should be the bottom. However, by the end of 2026, we forecast a rebound in the S&P500 to 7200. In terms of 2027, U.S. job losses from AI could be more noticeable and cause a fear factor among consumers that dents consumption and growth. We see the S&P500 to 7000 by the end of 2027. Other DM equity markets and China will find it difficult to outperform the U.S. in 2026, as markets are no longer cheap.

· FX. The USD can see a slow decline resuming versus most DM currencies, with the AUD and NOK remaining our favourite of valuation; structural fundamentals and policy rate grounds. JPY is also extremely undervalued and could snap higher. In EM, the Brazilian Real remains attractive on a total return basis in 2026, helped by wide nominal and real interest rate differentials.

· Commodities. Our baseline (here) is for a 4-8 week war, with WTI down to USD80-85 by June; USD65-70 end 2026 and USD60 by Q3 2027. A 2-to-6-month war would require oil prices to trigger demand destruction as strategic stockpile release would be insufficient. WTI to USD 120-180 (depending on duration and damage) and remain elevated for the remainder of 2026.

Figure 3: Key Events

| May 2026 | Powell Replaced as Fed Chair | Powell is set to be replaced as Fed Chair in May, though his replacement by former Fed Governor Kevin Warsh could be delayed, with a key Republican Senator (North Carolina’s Thom Tillis, who is not seeking re-election) threatening to delay confirmation as long as a legal investigation into Powell continues. Warsh will advocate a more dovish stance, on the grounds that rising productivity will reduce inflation, but may struggle to receive majority support for this in FOMC voting. He also wants to reduce the size of the balance sheet, but others on the FOMC oppose this idea. |

| July 2026 | USMCA Renegotiations | President Trump has made clear that he wants to renegotiate USMCA and new threats will be used as a negotiating tool by summer. However, a deal will likely be reached by end 2026/early 2027, with USTR Greer indicating that an addendum could be added to the existing agreement with bilateral sub deals for Canada and Mexico. Odds of the U.S. not renewing USMCA are low, but if it did occur then the agreement would technically run until 2036. |

| September 13, 2026 | Sweden General Election | The current right-wing coalition still has a very slim effective majority in parliament even with the far-right Sweden Democrats offering support. This is all the result of the 2022 election, which brought a fragmented result but locking out the Social Democrats even though they are the largest party. This fragmentation was a result of a more polarized parliament, and polls suggest more of the same, but with a general drip more to the left. But even if left-leaning parties return to power, it is unlikely to change much given the current focus on defence but where an election issue may be a speedier defence build-up. |

| By September 20, 2026 | Russia Parliamentary Elections | Russia is set to hold its next parliamentary elections by September 20, 2026 to determine the State Duma, the lower house of the Federal Assembly. All 450 seats are up for grabs, with 226 needed for a majority. As of current polling trends, United Russia (YeR) leads with around 35%-40% support; Communist Party (KPRF) trails with 10%; and Liberal Democratic Party (LDPR) also holds 8%-10%. We expect United Russia, led by Dmitry Medvedev, will likely remain dominant after its 2021 victory. |

| October 4 and 25, 2026 | Brazil General Election | In 2026, Brazil will hold general elections to elect the next President, renew all the Chamber of Deputies seats, and two-thirds of the Senate, while also electing the governors of all Brazilian states. Lula will seek re-election, while opinion polls suggest Lula could face Flavio Bolsonaro who has overtaken Tarcísio de Freitas (an ex-Bolsonaro minister), with the race being too close to call at this stage. Pre-election fiscal easing will likely be seen. |

| November 3, 2026 | U.S. Mid Term Elections | All seats in the House and a third of the seats in the Senate will be up for election. With the current Republican majority in the House being marginal even a modest level of disappointment in the Trump administration, which seems likely, would be enough to see the Democrats gain control of the House. It will harder for the Democrats to make the necessary gain of 4 seats in the Senate, though they look likely to make gains in Maine and North Carolina, and Trump’s increasing unpopularity now makes the Senate a close call. States to watch are Alaska, Ohio and Texas. |

| May 2027 | French Presidential Election | Opinion polls and this month’s local elections suggest that if/when a fresh legislative election occurs, this will not change parliament materially meaning insufficient fiscal consolidation. President Macron has ruled out fresh parliamentary elections and they are not due until 2029. The 2027 presidential election will likely see all other main parties supporting a candidate to prevent the National Rally getting the presidency. However, it is not yet clear who this will be, but it is unlikely to resolve the slow progress in reducing the budget deficit. We feel France will face fiscal pressure and could face a fiscal crisis. |

| Aug 2027 | Spain General Election | The election is scheduled to occur by Aug 22, although one could occur much earlier if the current Socialist administration’s run of scandals deepens enough and/or the diplomatic friction with Trump persuades PM Sanchez to get electoral support. He has tried to rule out such a snap vote out and insisted he will stand for office again. Either way it does look as if there would be a change in who runs the country, given the right of centre People’s Party lead in the polls, the question being how much of a swing to the right would occur depending upon who the PP go into coalition with. |

| Sep-Oct 2027 | Italian General Election | The election has to occur by late December, but is more likely to occur earlier, probably in September. As for the possible result, important wins for Italy's opposition in southern regional elections recently show cracks in the ruling conservative bloc's dominance, raising doubts over PM Meloni's ability to secure a second term. However, at this juncture, Meloni’s coalition (her Brothers of Italy party, Forza Italia and the far-right League) are ahead in national polls while the opposition needs to unify more after years of mutual hostility. |

| Oct/Nov 2027 | Turkiye Presidential Election | Parliamentary elections in Turkiye are scheduled to occur no later than May 14, 2028, alongside presidential elections. We expect the elections to be held in October/November 2027, earlier than the scheduled time. This timing is critical, as an early election called by Parliament is the only constitutional path for President Erdoğan to seek another term. The presidential race will be between AKP’s candidate and an opposition candidate supported by CHP. Taking into account that CHP’s official presidential candidate Ekrem Imamoglu is still in jail, he will likely be replaced by someone else (such as Ankara Mayor Mansur Yavaş or CHP Chairman Ozgur Ozel) if Imamoglu won’t be released before 2027. We expect a close race between AKP/MHP block (People's Alliance) and the CHP for the parliamentary elections. |

| Oct-Nov 2027 | Argentina General Election | President Javier Milei’s administration has been boosted by October 2025 election results that saw his party (La Libertad Avanza LLA) doing better than expected in mid-term elections. USD2bln of U.S. Treasury FX purchases and a USD20bln credit line from Milei’s friend, U.S. President Trump, helped to reduce financial market volatility and boost Milei support. Trump has rewarded Milei with a trade deal in 2026. The continued slowing in inflation and fear of returning to economic instability should also support Milei and LLA in the 2027 general election. However, 2025 had shown how fluid voter behaviour is and the situation needs to be monitored near the 2027 elections. |