Federal Reserve

View:

July 02, 2026

U.S. June Employment - Upside May surprise offset, but unemployment falls on lower labor force

July 2, 2026 1:20 PM UTC

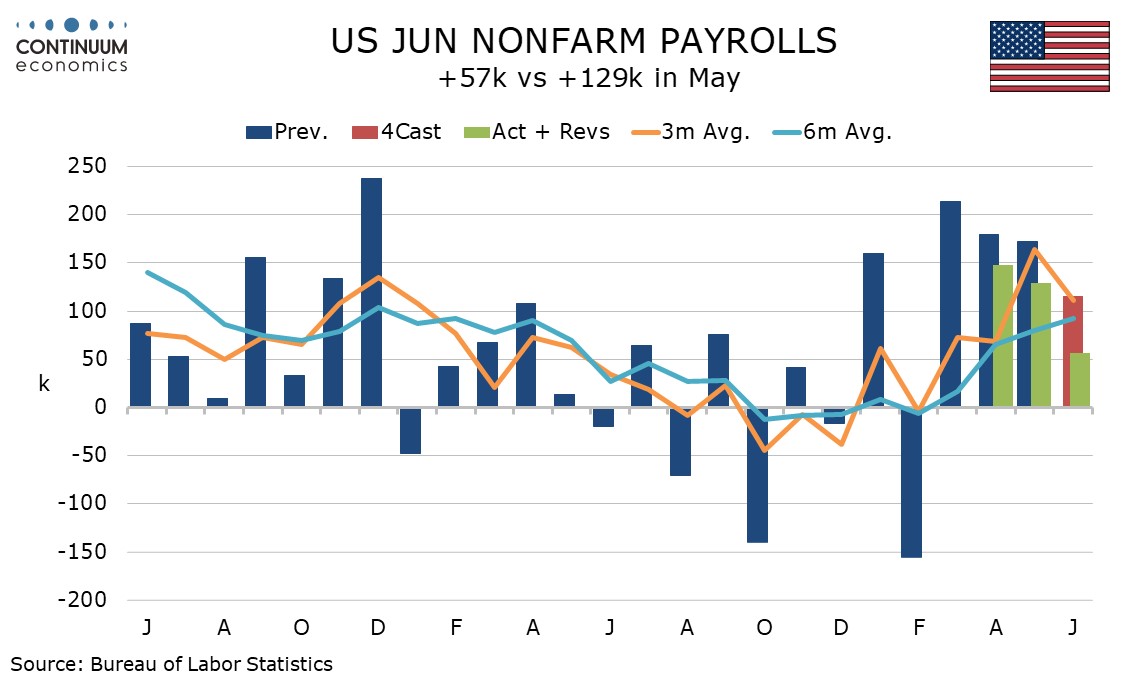

June’s non-farm payroll is weaker than expected with a 57k increase, 49k private, with downward revisions to April and May. The slowing is consistent with an upturn in the initial and continued claims trends, though both were almost unchanged (-1k to 215k and +2k to 1.814m respectively) in the l

U.S. June Employment - Upside May surprise offset, but unemployment falls on lower labor force

July 2, 2026 1:12 PM UTC

June’s non-farm payroll is weaker than expected with a 57k increase, 49k private, with downward revisions to April and May. The slowing is consistent with an upturn in the initial and continued claims trends, though both were almost unchanged (-1k to 215k and +2k to 1.814m respectively) in the l

July 01, 2026

June 26, 2026

U.S. Trimmed Mean and Median PCE Price Indices not as strong as Core PCE

June 26, 2026 7:05 AM UTC

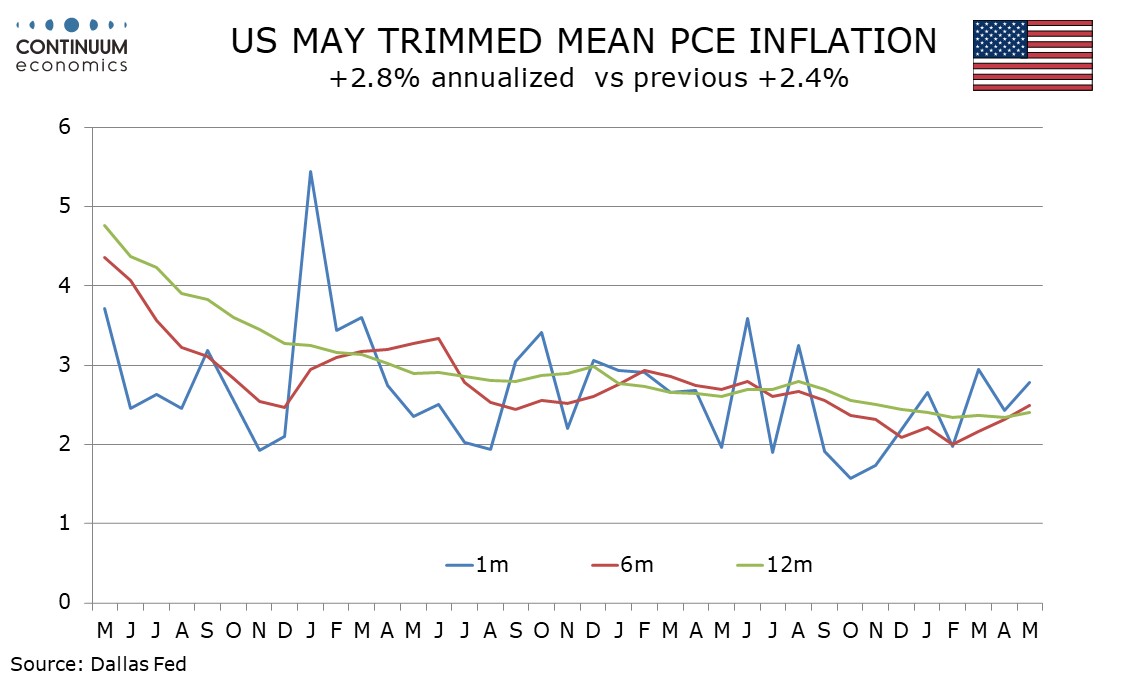

The Dallas Fed’s Trimmed Mean PCE inflation index, which is reported to be a series favored by Fed Chair Kevin Warsh, as well as the Cleveland Fed’s Median PCE price index, look a little less alarming than the Fed’s officially targeted Core PCE price index. This could be used as an argument ag

June 25, 2026

U.S. Trimmed Mean and Median PCE Price Indices not as strong as Core PCE

June 25, 2026 6:19 PM UTC

The Dallas Fed’s Trimmed Mean PCE inflation index, which is reported to be a series favored by Fed Chair Kevin Warsh, as well as the Cleveland Fed’s Median PCE price index, look a little less alarming than the Fed’s officially targeted Core PCE price index. This could be used as an argument ag

June 23, 2026

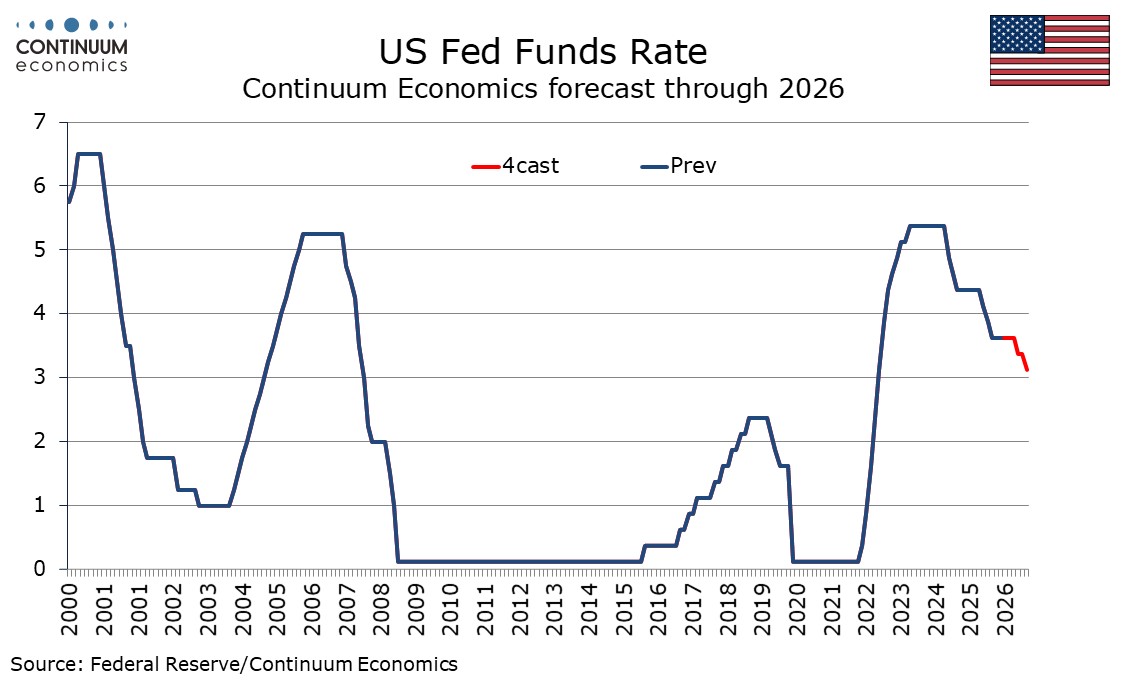

DM Rates Outlook: Tightening or Easing?

June 23, 2026 8:15 AM UTC

· With the U.S./Iran interim agreement likely to hold and energy prices softening, our projected consumer slowdown will likely tilt the Fed not to hike in H2 2026 and to actually ease by 50bps in 2027, with 25bps moves in both Q2 and Q3. With 2yr yields consistent with a hike, the tra

June 22, 2026

U.S. Outlook: Consumers Looking Vulnerable

June 22, 2026 2:17 PM UTC

• The US economy is showing resilience with strength in investment offsetting a gradual slowing in consumption, though consumer spending, which is running well ahead of real disposable income, looks set to slow further. This is likely to see the economy slow in the second half of 2026 even

June 17, 2026

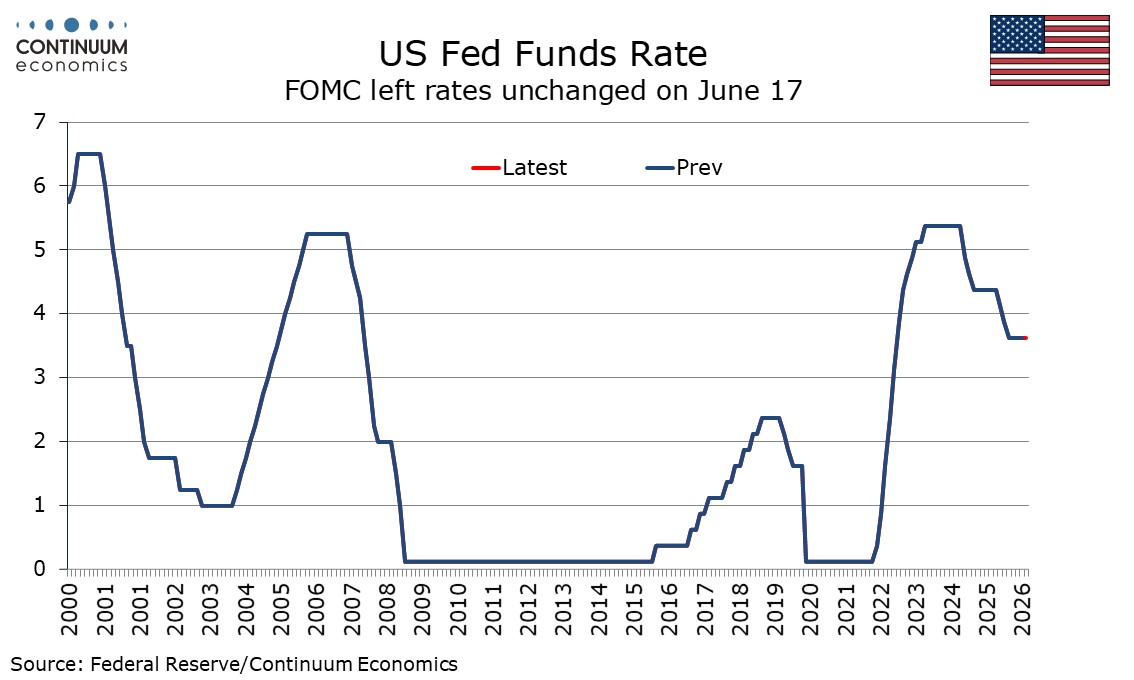

FOMC - Policy may prove less hawkish than the dots, assuming slowing in data

June 17, 2026 8:08 PM UTC

The Fed dots show a clearly divided Fed with only a minority on the median rates view for 2026, for a 25bps hike, 2027, which sees a 25bps reversal, and 2027, which sees a further 25bps easing. There are several respondents on either side of the median but we believe the voters lean towards the dovi

June 16, 2026

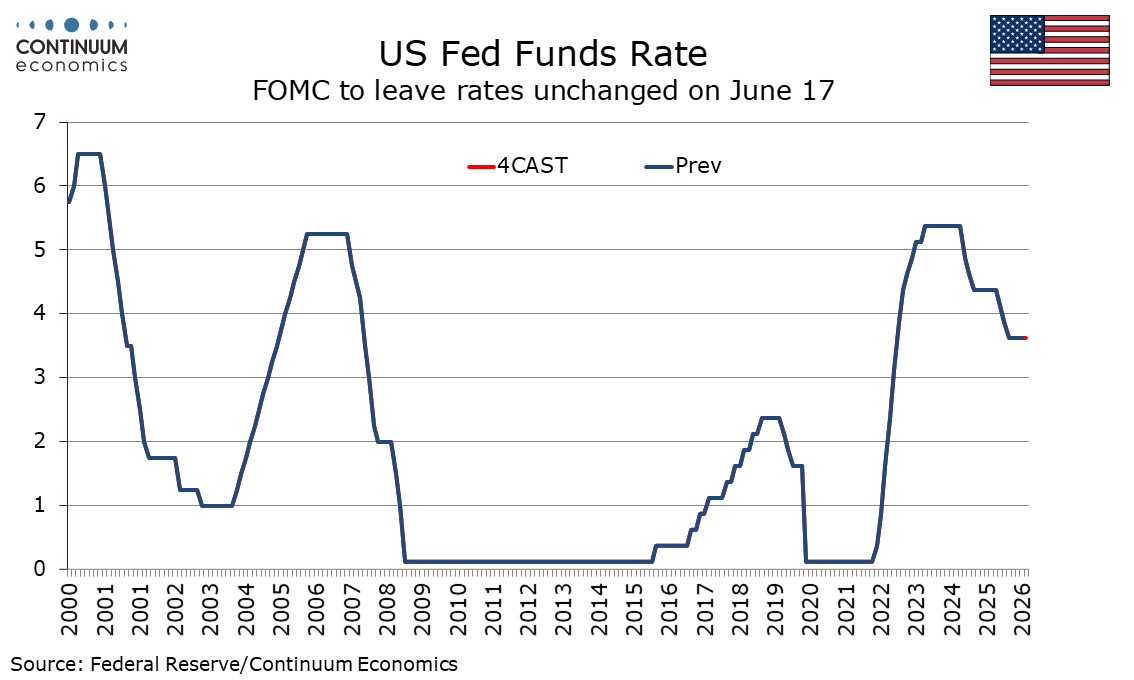

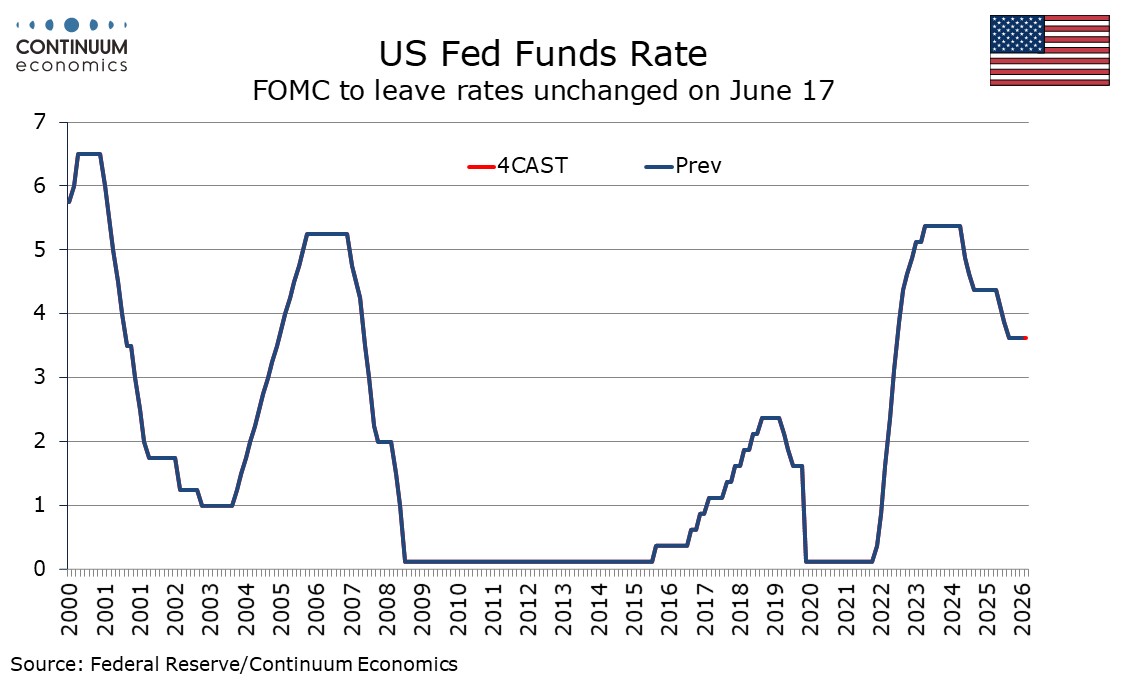

FOMC Preview for June 17: Dropping the easing bias (update)

June 16, 2026 2:58 PM UTC

The FOMC meets on June 17 and while a change in the Fed Funds target range from the current 3.5-3.75% is unlikely, the statement is likely to drop the easing bias. The median dots are likely to get a little more hawkish with a hawkish skew in the detail, with inflation forecasts, including those for

June 15, 2026

U.S./Iran Interim Deal and Reopening Strait of Hormuz

June 15, 2026 12:32 PM UTC

· Our baseline (80%) is that the Strait of Hormuz will reopen in H2 2026 and remains open through 2027. However, logistics dislocation plus a switch from commercial inventory rundown to rebuilding will likely slow the decline in oil prices back towards normal levels (Figure 1). O

June 12, 2026

Fed Tightening and U.S. Treasury Yields: 1994, 1999 and 2022 Redux

June 12, 2026 7:05 AM UTC

Our baseline involves no Fed hike, but 50-75bps is feasible in a plausible adverse scenario. In this alternative scenario of 50-75bps of Fed tightening it is easy to build the case for 2yr yields going to 4.30-4.40% area, before thoughts turn to H2 2027/28 involving modest Fed rate cuts. 10yr

June 10, 2026

FOMC Preview for June 17: Dropping the easing bias

June 10, 2026 4:55 PM UTC

The FOMC meets on June 17 and while a change in the Fed Funds target range from the current 3.5-3.75% is unlikely, the statement is likely to drop the easing bias. The median dots are likely to get a little more hawkish with a hawkish skew in the detail, with inflation forecasts, even ex food and en

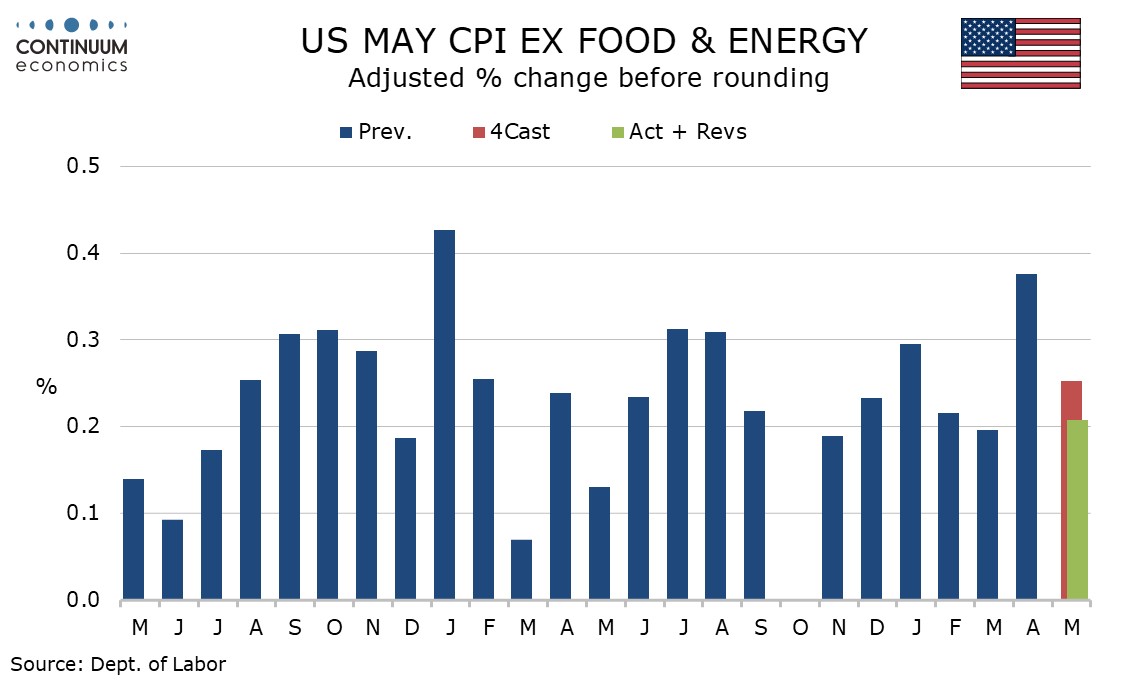

U.S. May CPI - Surprising fall in transport services despite continued gains in air fares

June 10, 2026 1:08 PM UTC

May CPI is in line with expectations at 0.5% overall but the core rate ex food and energy was softer than expected at 0.2%, with the rise before rousing being 0.208%. The most surprising restraint on the data was a 0.6% fall in transportation services, despite continued gains in air fares.

Financial Markets/Policymakers and the Strait of Hormuz Question

June 10, 2026 8:05 AM UTC

· Though the U.S. and Iran have attacked each other June 10, talks to reopen the straits of hormuz still continue. An Iran/U.S. agreement to reopen the Straits of Hormuz could cure the risk of a demand/supply oil market imbalance and produce some psychological relief that could knock USD

June 08, 2026

DM Government Bonds: Risks of Higher Long End Premia?

June 8, 2026 2:10 PM UTC

· Our baseline is for DM government bond yields ex Japan to remain elevated, but controlled. Japan extra risk premium is driven by BOJ QT at 6% of GDP, more than long-term debt fears. Major catalysts could drive a regime change to higher risk premia and steeper yield curves, but non

June 05, 2026

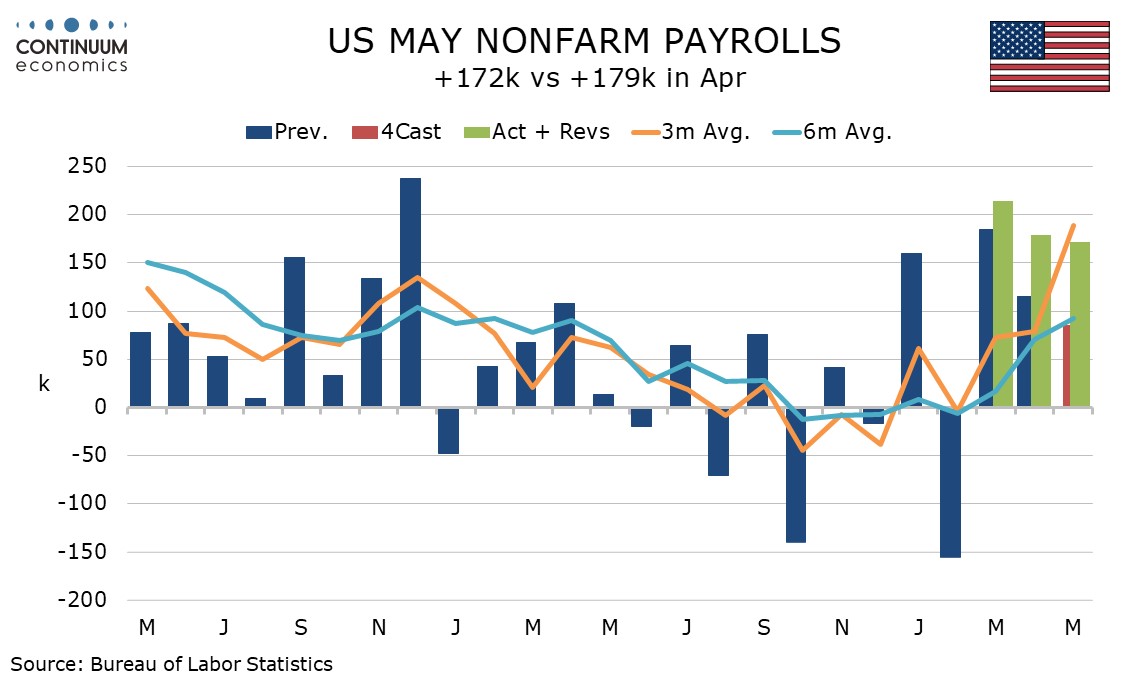

U.S. May Employment - Surprise came from local government and leisure and hospitality

June 5, 2026 1:19 PM UTC

May’s non-farm payroll is significantly stronger than expected with a rise of 172k though the private sector was less impressive at 120k, if still healthy. Upward revisions to March and April add to the positive message. In addition to government, leisure and hospitality with a 70k increase was

June 03, 2026

June 02, 2026

May 29, 2026

May 28, 2026

May 22, 2026

May 20, 2026

FOMC Minutes from April 29: Hawkish concerns appear broadly felt

May 20, 2026 6:54 PM UTC

FOMC minutes from April 29 show a hawkish leaning, confirming market perceptions that there was more interest in removing an easing bias from the language than revealed by the three hawkish dissents at the meeting. Should inflation remain persistent, tightening could come onto the agenda, though sho

May 13, 2026

May 12, 2026

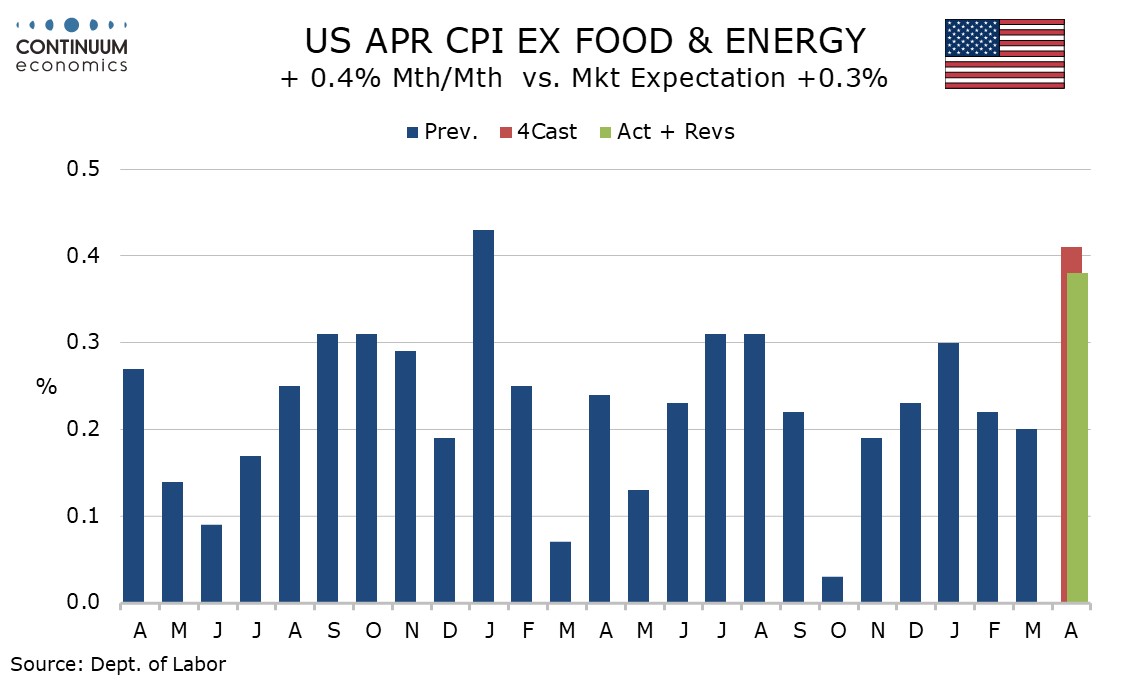

U.S. April CPI - Subdued ex food, energy and what looks like one-time strength in shelter

May 12, 2026 1:08 PM UTC

April CPI is only marginally stronger than expected on the core rate, up by 0.4%, 0.376% before rounding, and the data not alarming outside of a one-time distortion in housing. The headline gain of 0.6% was as expected, and here the rise was a little firmer at 0.64% before rounding.

May 08, 2026

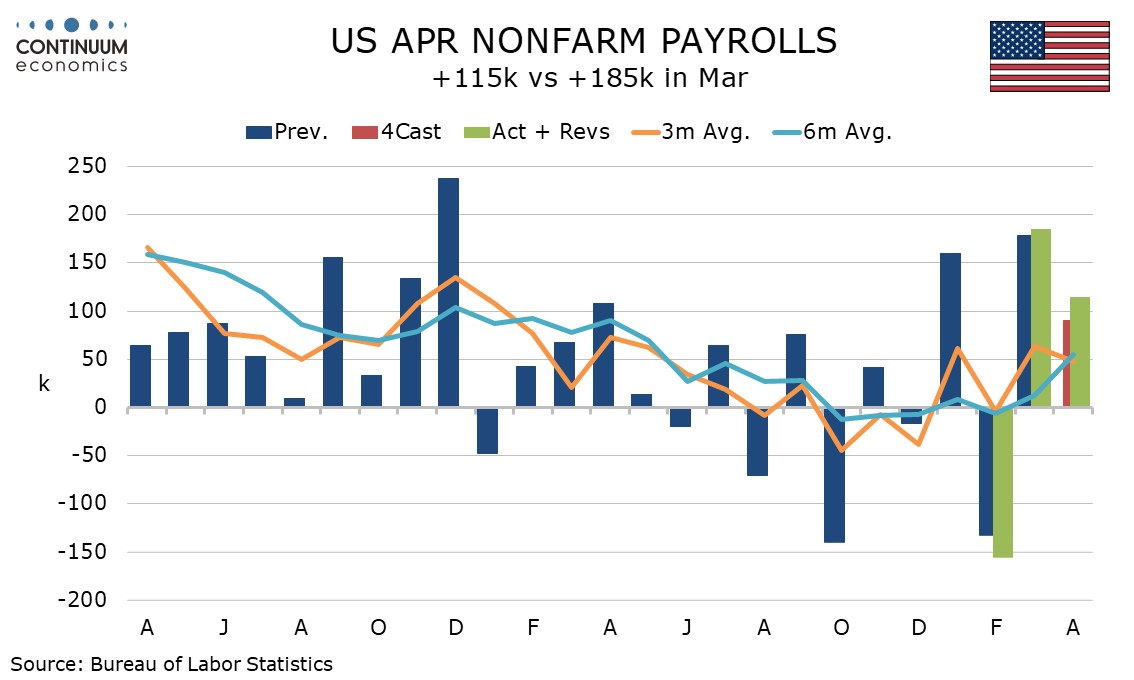

U.S. April Employment - Resilience should keep easing off the near term agenda

May 8, 2026 1:04 PM UTC

April’s non-farm payroll suggests the US economy continues to grow at a respectable pace in early Q2 with no signs of a hit from the oil shock yet. Payrolls increased by a stronger than expected 115k, with unemployment stable at 4.3% and the workweek stronger at 34.3 hours from 34.2. Average hourl

May 07, 2026

May 05, 2026

U.S. Labour: In Praise of Older Workers

May 5, 2026 8:32 AM UTC

· While financial pressures are prompting U.S. workers to delay retirement and work longer, this is not being realized due to deteriorating health/labour market skills mismatches and other issues. More work from older workers is unlikely to be the solution to shrinking net immigration.

May 04, 2026

May 01, 2026

U.S. Fed's Kashkari, Hammack and Logan explain their hawkish dissents

May 1, 2026 2:42 PM UTC

The three hawkish dissents at the latest meeting were against an easing bias. Kashkari seems the most hawkish, with a leaning to tightening. Hammack and Logan both noted resilence in activity data as well as infltionary risk. There was a dovish dissent from Miran, but he will leave the Fed once Wars

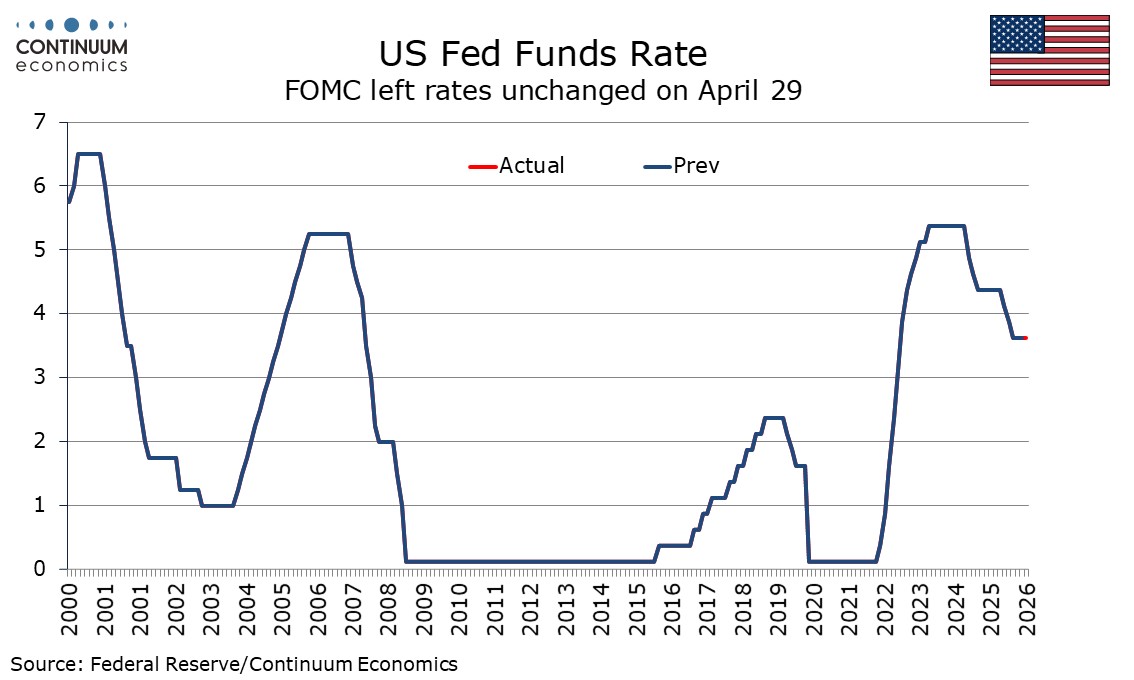

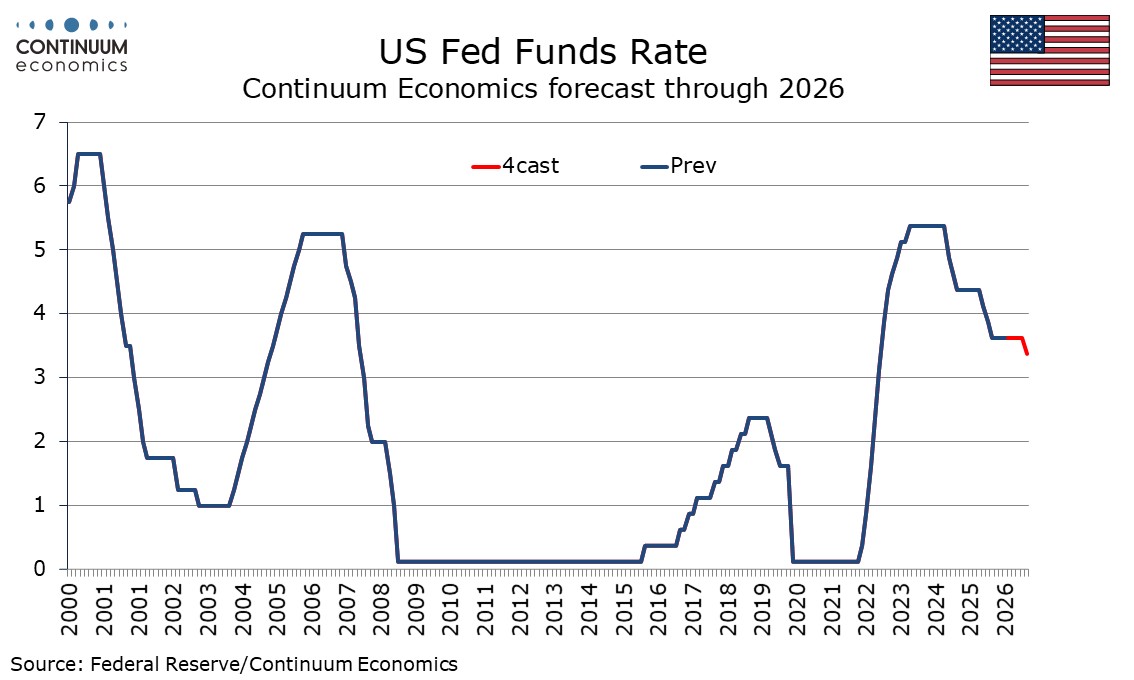

April 29, 2026

FOMC - Easing call moved to December from September

April 29, 2026 7:58 PM UTC

The Fed is now entering a transition from Chairman Powell to Chairman Warsh, who looks set to be in place at the next meeting on June 17. The final meeting of Powell’s term saw three hawkish dissents on the language and Powell announce he will continue as Governor after his term as Chair ends. We

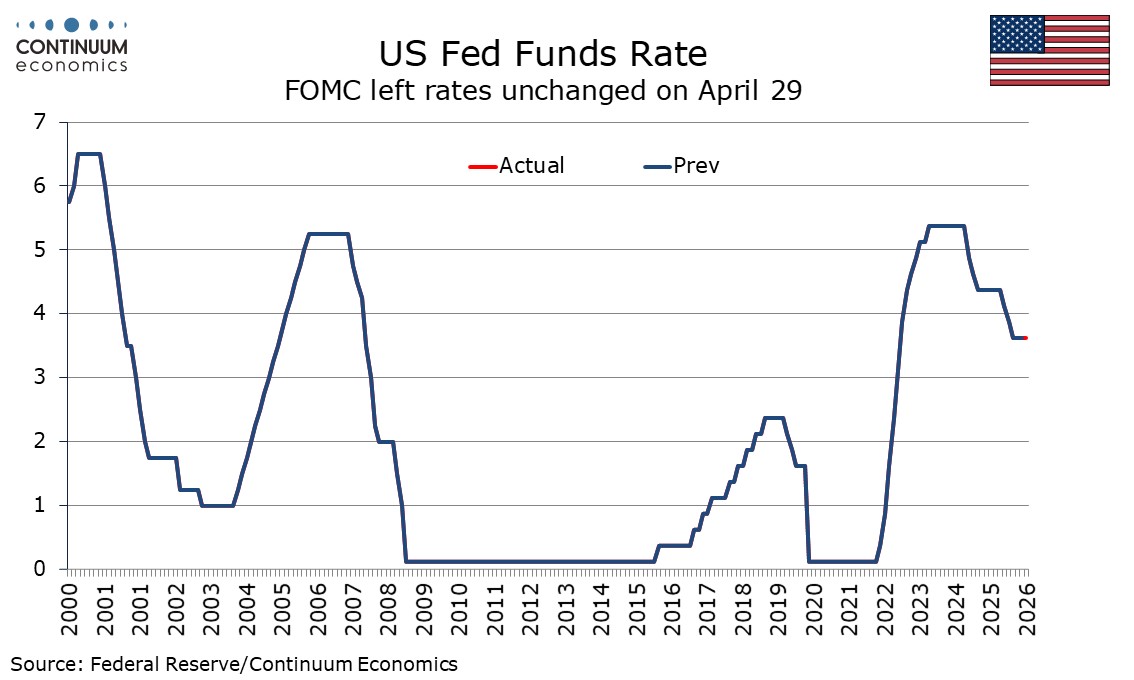

FOMC keeps rates on hold but three of four dissents are hawkish

April 29, 2026 6:23 PM UTC

The main surprise in the FOMC statement was the number of dissents, one dovish, Miran continuing to call for a 25bps easing, and three hawkish, with Hammack, Kashkari and Logan in agreement with the decision to leave rates unchanged but objecting to the inclusion of an easing bias.

April 22, 2026

FOMC Preview for April 29: Uncertainty keeping the Fed on hold

April 22, 2026 2:29 PM UTC

The FOMC meets on April 29 and there is little risk of a change in rates from the current target range of 3.5-3.75%. High uncertainty, both on the geopolitical situation and the future of the Fed, suggests there will be little forward guidance, and the dots will not be updated until the next meeting

April 16, 2026

April 15, 2026

April 10, 2026

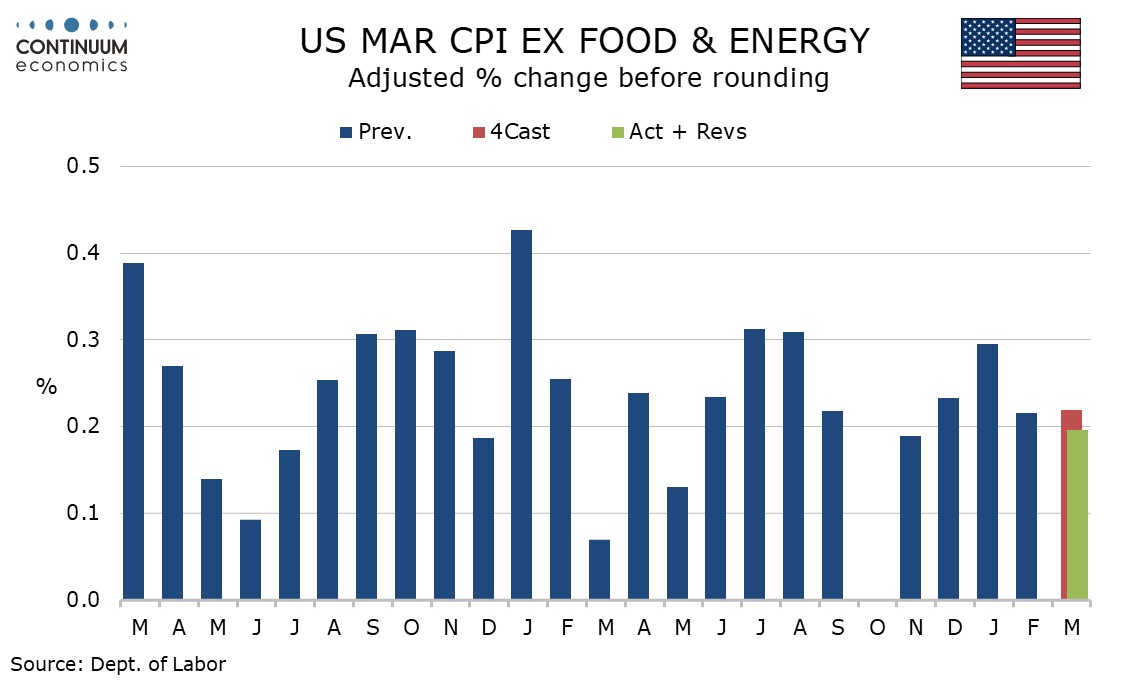

U.S. March CPI - Subdued core rate provides relief

April 10, 2026 12:55 PM UTC

March CPI is as the market expected with a 0.9% increase (0.865% before rounding) led by a surge in energy, but the core rate ex food and energy shows little sign of feed through, rising by a lower than expected 0.2%, with the gain before rounding at 0.196%, the slowest since November’s subdued tw

April 08, 2026

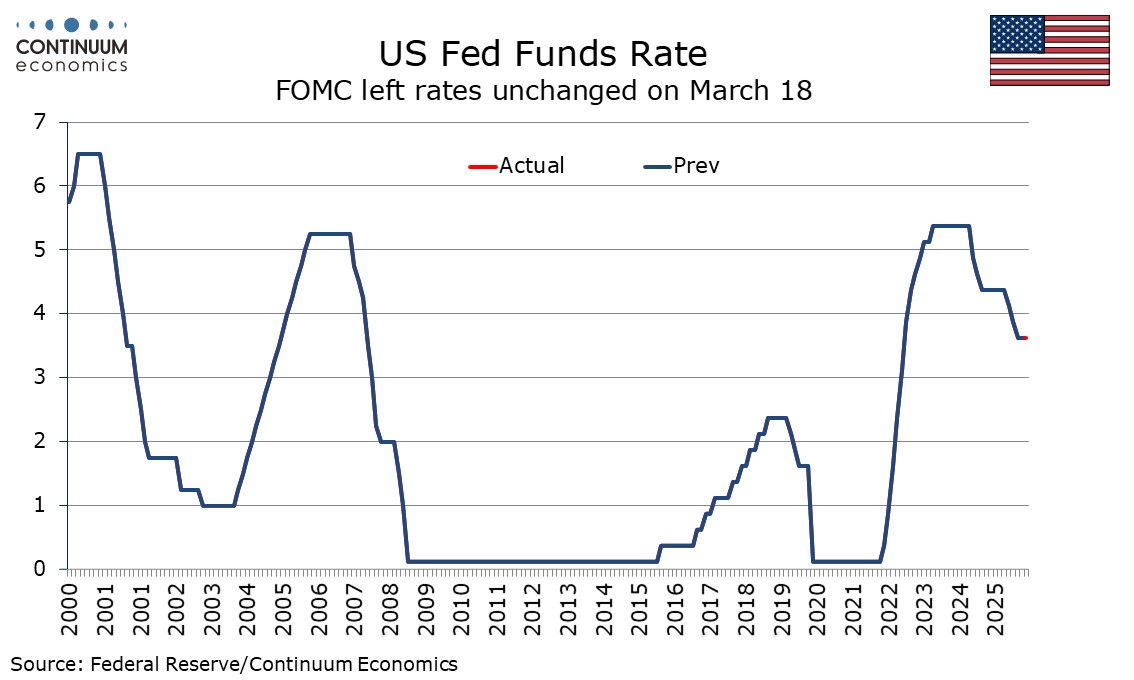

FOMC Minutes from March 18: Increased risks, but still a dovish leaning

April 8, 2026 6:58 PM UTC

FOMC minutes from March 18 show greater concern over inflationary risks but with concerns also seen on risks to employment, do not appear to be hawkish. It still appears that the next move is more likely to be an ease than a hike, even if the timing for rate cuts may have been pushed back somewhat.

April 07, 2026

April 03, 2026

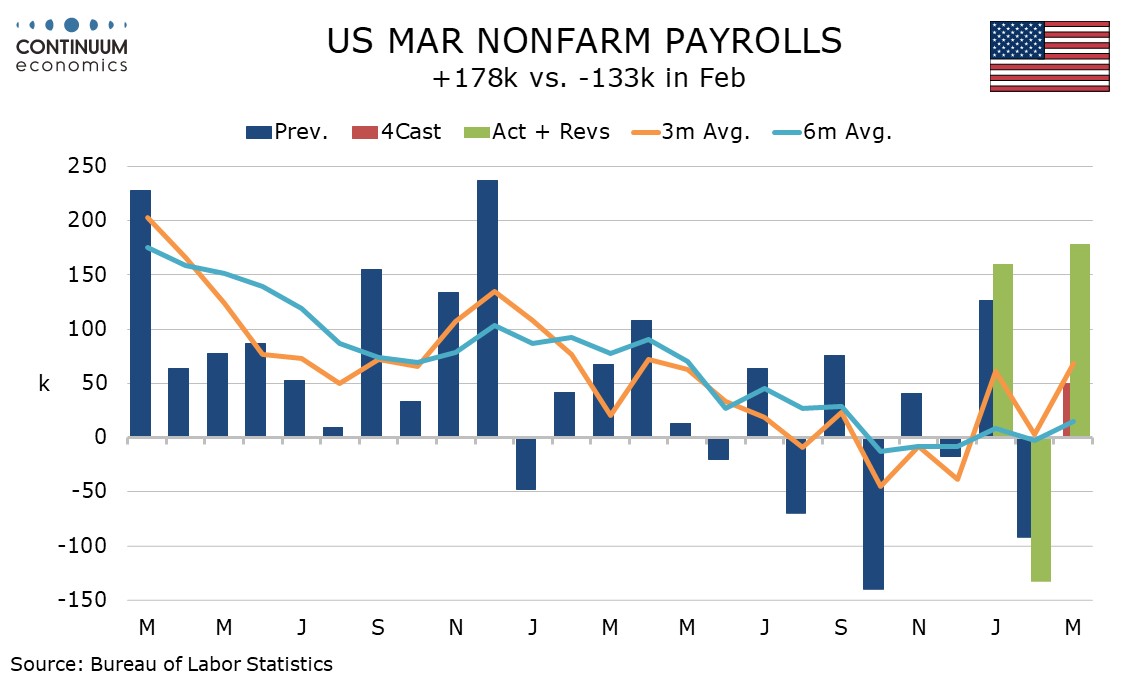

U.S. March Employment - Strong report suggests risks clearly higher on the inflation side

April 3, 2026 1:27 PM UTC

March’s non-farm payrolls is clearly on the strong side of expectations, up by 178k and an even stronger 186k in the private sector, with minimal net downward revisions of 7k. Unemployment unexpectedly fell to 4.3% from 4.4%. Less positive are a lower than expected 0.2% rise in average hourly earn