Straits of Hormuz Standoff and Mixed Markets

• Equities longer time horizon means that they are hoping for a reopening of the Straits of Hormuz (though also being helped by renewed AI optimism), whereas government bond markets actually want to see tangible progress and an associated tempering of DM central banks posturing. This divergence can continue into May, but it does need new progress on trying to actual reopening the Straits of Hormuz – which is our baseline given economic pressures on the U.S. and Iran.

While Equities have found new optimism, government bond markets remain worried about energy prices and the risk that some DM central banks could hike rates.

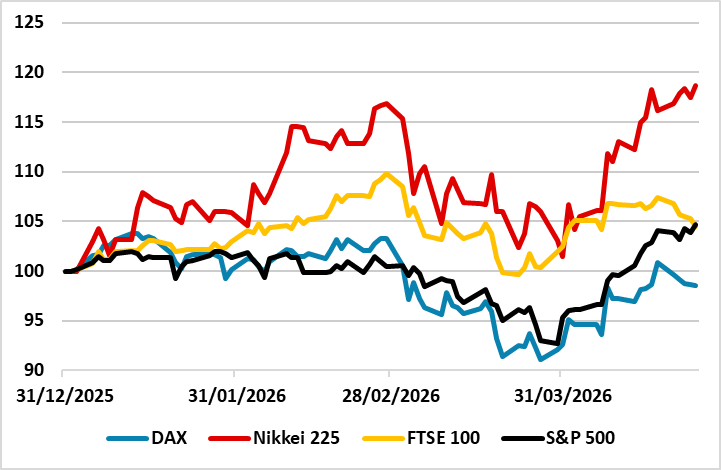

Figure 1: DM Equity Markets (31/12/25 =100)  Source: Datastream/Continuum Economics.

Source: Datastream/Continuum Economics.

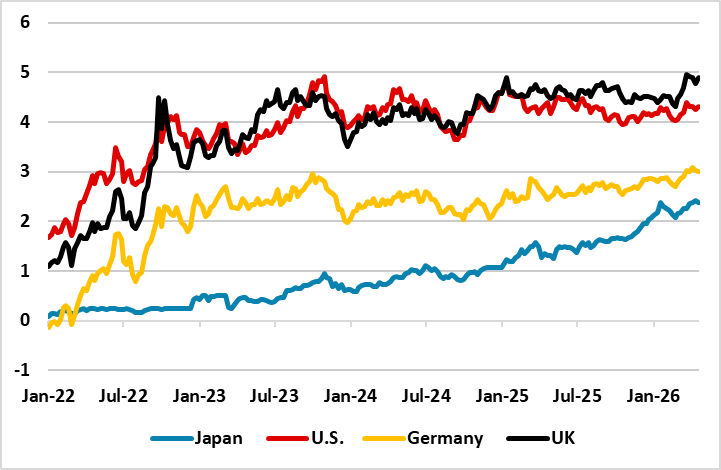

A divergence exists in major financial markets with equities extending their early April rebound (Figure 1), but government bond yields remain elevated compared to pre Iran war levels (Figure 2). Equities remain underpinned by the view that the Trump administration will be very reluctant to restart the war and will eventually compromise further to get the Straits of Hormuz reopened. Government bond markets with a shorter time horizon than equities are concerned that it is taking so long to get the Straits reopened with a standoff currently. Government bond markets are also worried that some DM central banks could tightening with 25bps BOJ & 50bps of ECB and BOE hikes discounted this year, but a flat profile from the Fed. Is this divergence a concern?

Figure 2: DM 10yr Government Bond Yields (%)  Source: Datastream/ Continuum Economics

Source: Datastream/ Continuum Economics

Central bank meetings this week will likely see the Fed signaling stable policy (here) and the ECB (here) and BOE (here) leaving the door open to tightening but also signaling no rush and that an easing of energy prices could mean no hikes! For government bond markets this likely reduces fear of higher policy rates and could help sentiment, but geopolitics on the Straits of Hormuz are more important. Reports of a three stage Iran proposal (ceasefire, then Straits of Hormuz reopen, then negotiations on nuclear) are one attempt to break the deadlock. Iran is also under pressure financially from the U.S. blockade, but also from the risk that oil wells could have to stop production in the coming weeks. Meanwhile, parts of the Trump administration will also be aware that oil prices could see renewed upward pressure into the summer, as the strategic oil reserve release finishes and a repeat is difficult. Our baseline remains towards a compromise and at least a partial reopening of the Straits of Hormuz as soon as May, which would provide some sentiment relief to global markets.

Equities have already taken this view, but are also benefitting from renewed AI optimism. Major tech companies reached relatively attractive valuations by their standards, which has prompted renewed investor interest. Additionally, the rollout of more powerful Blackwell chips from Nvidia comes where the focus is also advancing from large language models to more powerful world models that advance beyond text predictions to more real world reality. AI application revenue is also reported to be booming, which keeps the AI optimism. However, we still worry that the U.S. consumer could slow and hurt non tech U.S. stocks (here). Equities are also dependent on some progress eventually being made on actually reopening the Straits of Hormuz.

However, if the Straits of Hormuz is closed for say 6 months, then oil prices would have to adjust for demand destruction and this could be USD150 oil prices. This would prompt concerns that some DM central banks would actually hike and also likely prompt a correction in equities.