ECB Preview (Apr 30): Real Economy Buckling Already!

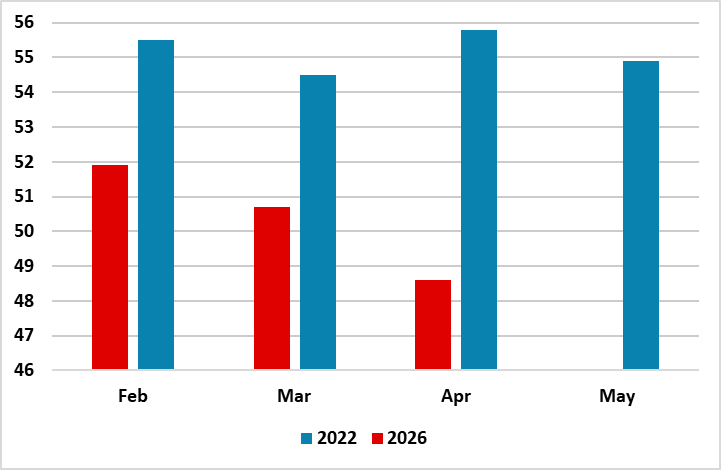

We again expect no change from the ECB on Apr 30, but President Lagarde will probably have to admit in the Q&A that unlike last time the decision was not unanimous. Overall, the communication will again suggest upside risks for inflation and downside risks for economic growth the extent and duration of both depend both on the intensity, length and likely resolution of the conflict. We still think the ECB is too pessimistic about inflation and too optimistic about growth as PMI data have started to show (Figure 1). And a series of data updates in the coming week may highlight this further, not least a bank lending survey showing probably increasing, signs of banks wariness about lending (Figure 2). In coming months, and given the manner in which the ECB may feel it cannot afford a repeat of what some call the policy mistake of four years ago, a rate hike by mid–year cannot be ruled out. But, this would be a mistake, ignoring how the policy and economic backdrop is vastly and increasingly different to then. As a result, we still see the next move being a cut to address adverse monetary condition albeit very late in the year!

Figure 1: Real Economy Hit Clear(er) This Time Around

Source: Markit, CE – Composite PMI balances this year and in 2022

Luckily from a presentational point of view the ECB will not be offering any updated projection which could limit a certain amount of degrees of freedom regarding the policy outlook. At this stage, it will probably continue to think that the outlook presented last time is still valid, albeit now skewed somewhat to the more adverse scenario. If this is a pretext to press for early hiking, it is misplaced as both gas prices have fallen and are averaging below the baseline assumptions while the adverse inflation picture actually sees a persistent undershoot of target from mid-2027 onward even on stable policy. And taking the cue from the IMF which last week warned that central banks should resist the urge to tighten as this could damage economic output, we note just how much more modest the current demand backdrop is relative the energy shock of four years ago, especially for the consume

Indeed, while it may be the case that the ECB is still reverberating from the 2022 energy shock and criticism it faced of hiking too slowly. If so, the ECB is getting confused. What is notable is that this energy shock and he ECB’s positioning is very much different to that of 2022, occurring at a point when the EZ economy is operating with a margin of spare capacity as opposed to one reviving from a pandemic induced demand shock. This is evident in survey data, where PMI numbers are now just showing a clear(er) hit to activity already, but also that the demand backdrop four years was so different (Figure 1). Indeed, this time around, increases in household fuel and utility costs, and other prices, are more likely to squeeze real incomes and damage already fragile household and business confidence, further weighing on demand. These factors could widen the output gap somewhat, more than potentially constraining second-round effects as should be fact that the current main official rate is currently 2.5 ppt higher than four years ago while HICP inflation is much lower so that ‘real’ rates are very much higher!

And this assumes that changes in policy rates have been fully passed on by banks to borrowers, something that does not seem to have been the case during the most recent easing cycle. Indeed, while the ECB discount rate (now down to 2%) is some 2 ppt below the peak last seen in mid-2024, the effective cost of borrowing for firms has fallen by only 1.5 ppt while that for household by a puny 40 bp!

This is all the more notable because assessing the policy stance and the monetary transmission mechanism includes not just the cost of credit buts its availability or supply. Sure, measures such as financial conditions indices are aggregates of various costs of borrowing and thus partly reflect credit supply but not to the full and direct extent that a credit market such as that of the EZ. Indeed, in the EZ, banks provide some 70% of credit demanded – unlike the likes of the U.S. where banks provide less than half that.

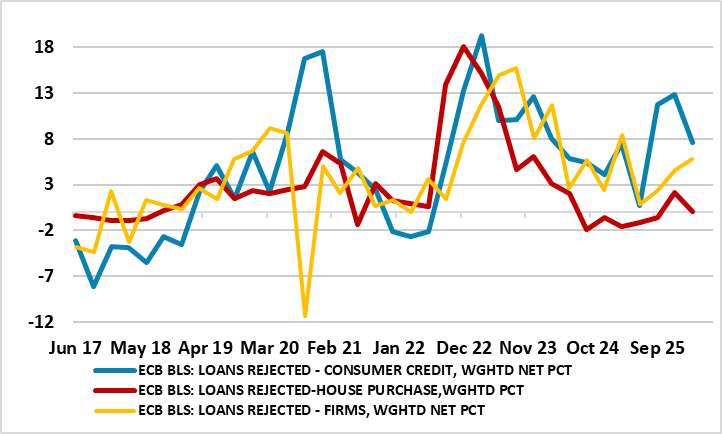

Figure 2: Loan Rejection Rates Rising and Above Long-Term Averages

Source: ECB

Moreover, there are clearer signs from various surveys and official monetary data that suggest a clearer wariness from banks have about the recent, current and projected economic outlook even before the latest conflict broke out. Indeed, the (last) ECB Bank Lending Survey (BLS) published three months ago, saw EZ banks report a clear net tightening of credit standards (banks’ internal guidelines for loan approval criteria) for loans or credit lines to enterprises in last quarter. Moreover, credit standards for consumer credit and other lending to households tightened further. Notably, for firms, this additional credit tightening surpassed the expectations reported by banks in the previous survey round and, according to the BLS, reflected ‘ongoing and perhaps deeper concerns about the outlook for firms and the broader economy, as well as banks’ lower risk tolerance’ the former probably accentuated by tariff-induced trade concerns given that export orientated companies were the focus of bank’s worries. But more troubling still, banks reported a further net increase in the share of rejected loan applications across all loan categories, particularly for firms and consumer credit. Furthermore, the extent of rejected loans was well above recent and pre-pandemic averages (Figure 2).

With this mind among the various important data updates due before the next ECB verdict, such as Thursday’s HICP and GDP numbers, it is the next BLS (Tue) that may be the most telling updates, it’s likely message of bank wariness about lending partly being flagged by the ECB’s survey on the access to finance of enterprises (SAFE) due on Monday which also provides information on developments in the financial situation of enterprises and availability of external financing.

These are just the added considerations that the ECB will have to assess but recent Council member comments suggest it is in no hurry to make sudden conclusions. Indeed, speaking from either side of the hawk-dove divide, Council member Schnabel suggested last week of no need to rush into a decision to raise rates while BoF Governor Villeroy de Galhau stressed that ‘a focus on April would be premature’.