FOMC Preview for April 29: Uncertainty keeping the Fed on hold

The FOMC meets on April 29 and there is little risk of a change in rates from the current target range of 3.5-3.75%. High uncertainty, both on the geopolitical situation and the future of the Fed, suggests there will be little forward guidance, and the dots will not be updated until the next meeting on June 17. If there is a shift in tone it is more likely to be in a hawkish direction, but few appear to be considering a near term tightening, and we still expect the next move is more likely to be an ease.

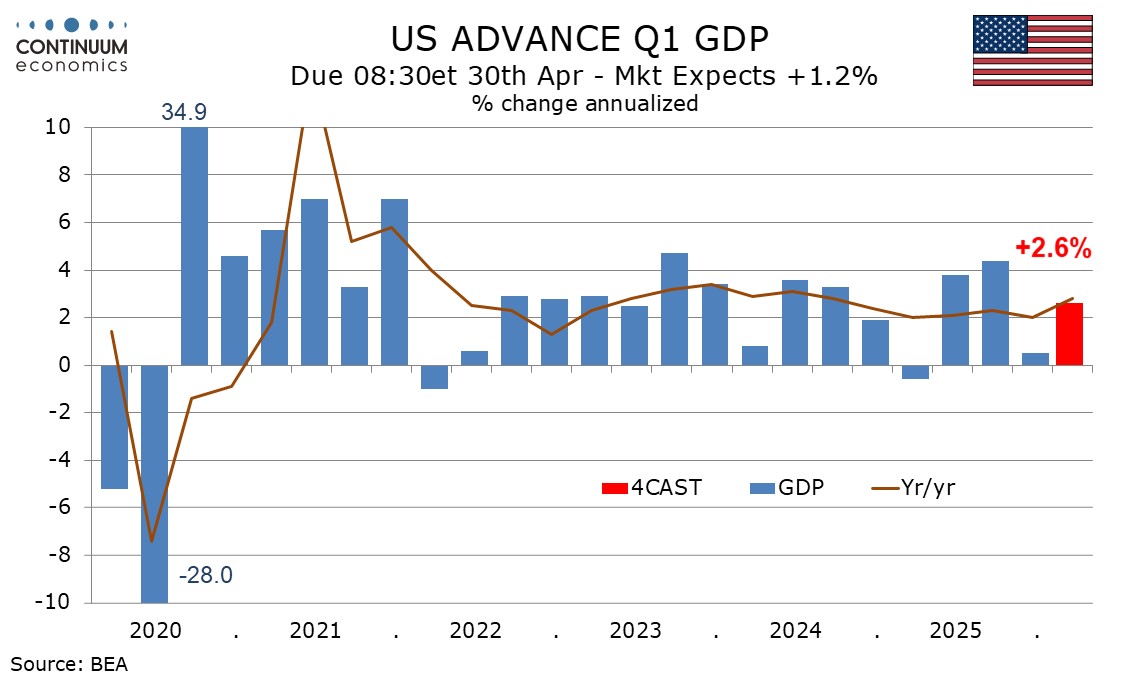

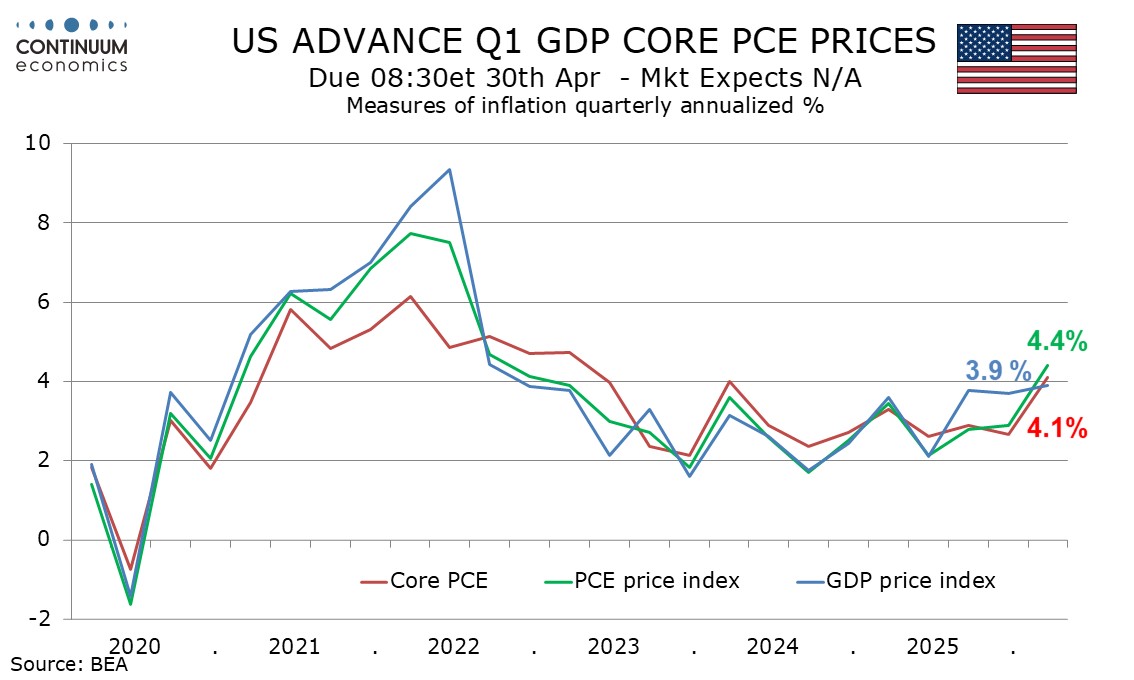

There does not appear to be any pressing need for the FOMC to alter its statement from the last one on March 16, which saw the economy expanding at a solid pace. Q1 GDP data due on April 30 is likely to confirm this (we expect a 2.6% annualized increase). The statement went on to say that job gains have remained low and the unemployment rate has been little changed in recent months. That also remains the case, but a stronger March non-farm payroll suggests any fine tuning to the view will be positive. Inflation was described as somewhat elevated. With core PCE prices looking firm in Q1 (we expect a 4.1% annualized increase) and energy prices having surged, the Fed may say a little more on inflation this time.

On March 18 the FOMC stated that uncertainty remains elevated, the implications of the Middle East conflict are uncertain, and that the Committee was attentive to risks on both sides of its mandate. That will remain the case, but downside risks on growth have probably eased marginally on recent data, while risks on inflation have on balance picked up, though the risks from tariffs are fading as those from energy increase. The Fed may stress the importance of keeping inflation expectations stable and recognize the risk that energy prices may remain elevated for some time. Governor Christopher Waller, recently a dove, has stated that markets are underestimating this risk.

March 18 saw only one dissent, a dovish one from Governor Stephen Miran, and this is likely to be repeated, though even Miran may recognize that the case for easing is not urgent. There are unlikely to be any hawkish dissents. Even the hawkish Cleveland Fed President Beth Hammack, a voter this year, has simply suggested that rates are likely to be on hold for some time. The most likely consequence of a protracted energy shock will be delays to easing rather than tightening.

In his press conference Chair Jerome Powell is likely to see rates as in the right place, and restrictive enough to weigh against inflationary risk, with the potential to move in either direction. He will be reluctant to give forward guidance given the uncertainty, not only on the geopolitical situation but also over the future of the Fed. Powell’s term as Chair ends in May but he may continue beyond that given potential delays in the confirmation of his nominated successor Kevin Warsh, which outgoing Republican Senator Thom Tillis has pledged to block until legal action against Powell is resolved.

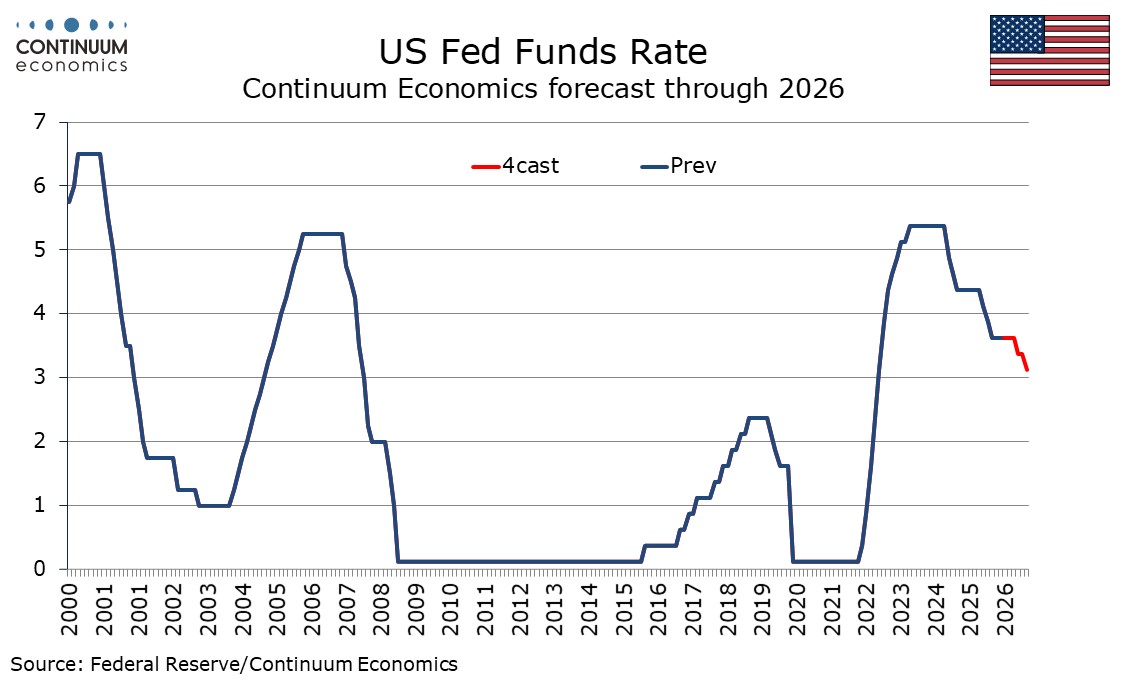

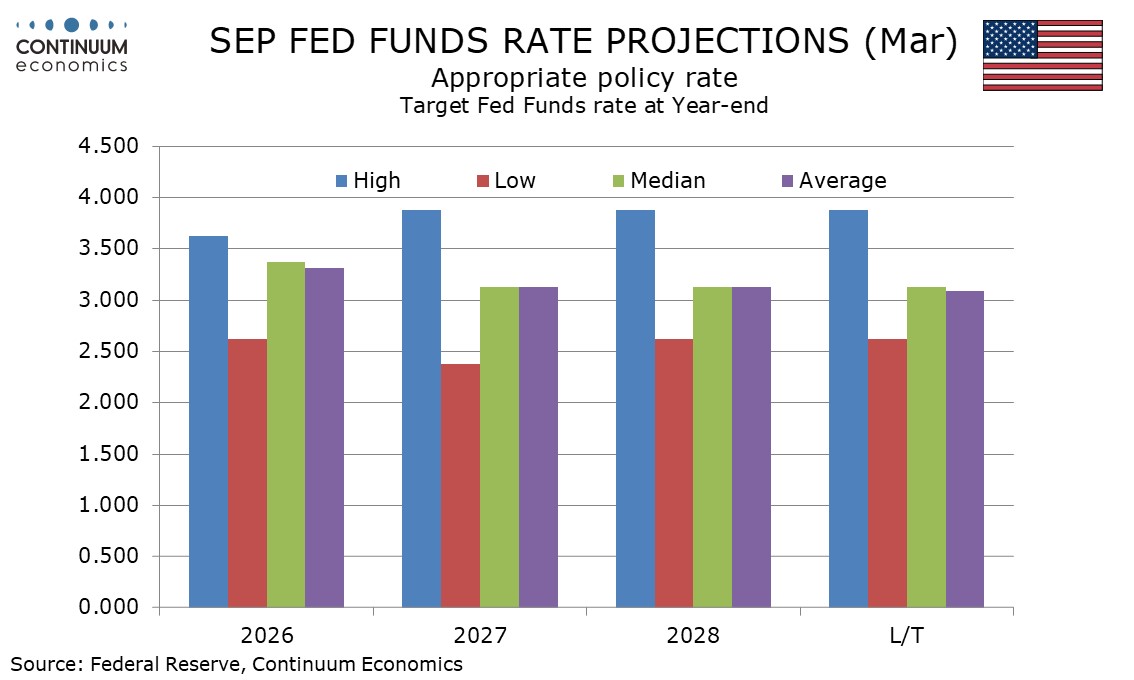

Warsh’s conformation still appears a question of when rather than if, and in his Senate hearings signaled a willingness to significantly change how the Fed operates, notably wanting less commentary on rates from Fed speakers, a sign that he is eager to assert his authority once appointed. He is clearly leaning dovish, on a view that rising productivity led by AI will increase the potential for noninflationary growth, but may have trouble getting the FOMC to vote his way. Risks to our rates forecast, of 25bps easings in September and December are later rather than sooner, but we are reluctant to change our view given that a lack of resolution of the situation in the Middle East by September is a pessimistic, if plausible, view. Uncertainty at the Fed is likely to be resolved before September. Two 25bps easings would take the Fed Funds target to 3.0-3.25%, in line with our and the median Fed view of neutral. Warsh may view the neutral rate as lower than this, though current Fed dots show an upward skew.