Straits of Hormoz Scenarios

· Our new baseline (70% probability) is for the Straits of Hormuz to start to partially reopen by June/July based on a framework deal between Iran and the U.S. This means more elevated oil prices in Q2, but then a gradual reduction in WTI to USD85 end-2026 and USD75 end 2027. The alternative scenario (30%) is that negotiations fail to produce a deal to reopen the Straits of Hormuz and we assume the Straits remains effectively closed until end September. This leads to a super spike to USD160-190, as oil has to price for demand destruction.

Though the Iran war is effectively over, how will the stalemate over the Straits of Hormuz be resolved?

Figure 1: WTI Oil prices

Source: Continuum Economics

The U.S. and Iran are reluctant to restart the war, with President Trump’s threats having been followed by a ceasefire and Iran wishing to negotiate to avoid major infrastructure damages. Still, the ceasefire is fragile, and negotiations have not progressed on a number of occasions. We highlight two main scenarios re the Straits of Hormuz, which are shaped by the objectives of both sides.

The U.S. maximist demands have been laid out, with stopping Iran’s nuclear weapons push being a major goal. However, the Trump administration’s weakness is sky-high gasoline and diesel prices, which in turn has seriously hurt Trump approval rating and risk the Republicans losing the Senate as well as the House. Trump has also shown that he talks tough, but can quickly compromise to try and reach a deal. The fanfare of Project Freedom in the strait has been followed 3 days later by a freeze on operation Freedom to help peace negotiations with Iran! We still feel that the Trump administration wants to compromise, with the highest priority being getting energy prices down and thus reopening the Straits of Hormuz.

Iran has been playing tough, but we see this as a negotiating posture rather than a reluctance to do a deal. Iran wants to avoid a future war with Israel; prefers to leverage the U.S. to stop Israel from attacking Lebanon; and aims to restart oil and other exports. The desire for a nuclear bomb is likely to have increased, given it could act as a deterrent against any future Israel or U.S. attacks. – like the U.S. reluctant to really challenge North Korea. However, Iran is facing a financial challenge regarding export and government revenues and is also close to having to close down oil production, which would take time to restart and in the case of old wells could be difficult.

Maximalist negotiating positions on both sides have so far stopped a deal from being reached. However, we feel that the incentives outlined above will still lead to some form of agreement, which would include reopening the Straits of Hormuz. This may not involve an agreement on nuclear weapons initially, though could involve an interim agreement (e.g., a freeze on nuclear enrichment/weapons development) followed by further negotiations. Pessimists would argue that this is tough to achieve and the stalemate will drag on. We acknowledge that as our main alternative scenario (30%) is for the stalemate to continue until at least the end of September. However, our new baseline (70%) is that an agreement to reopen the Straits of Hormuz will be reached in June/July, which will initially take time for shipping to recover and still mean disruption to oil/petroleum products and fertilizer supplies through the Straits of Hormuz.

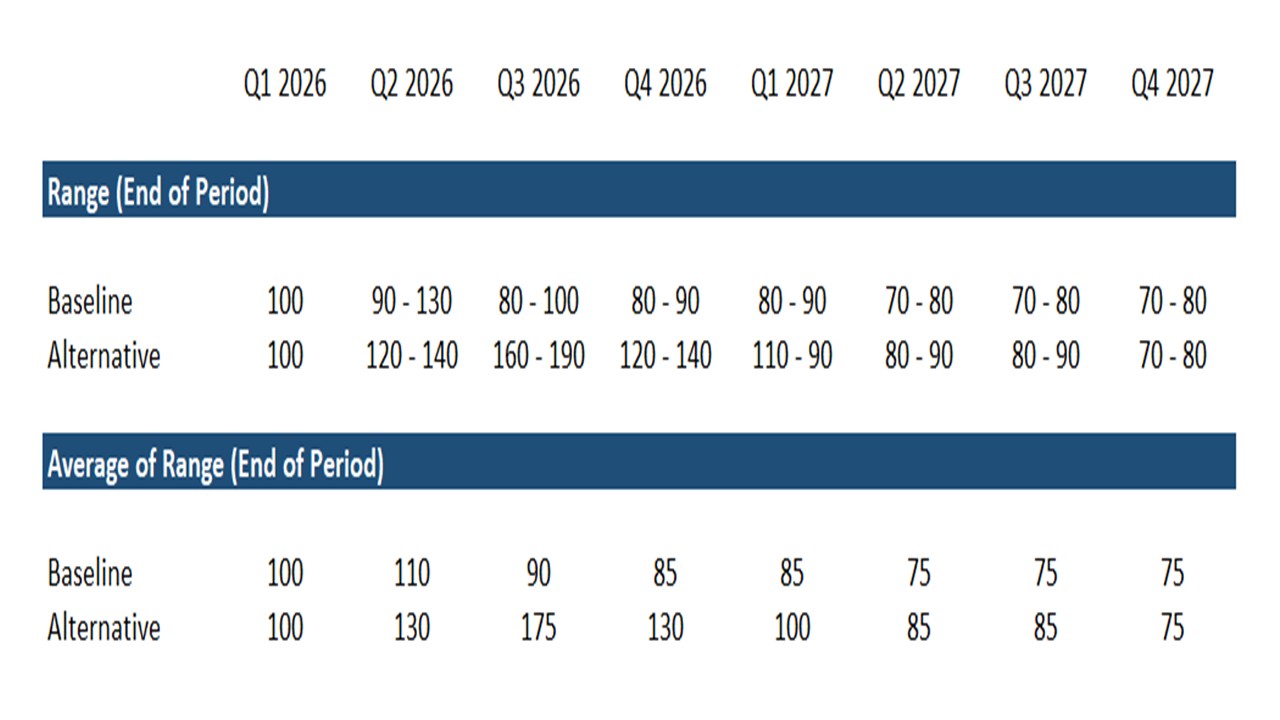

In Figure 1, we outline what we feel will happen to oil prices. The difference between our baseline and alternative scenarios comes down to a single factor: time. In the baseline scenario, we assume the Strait of Hormuz will partially reopen in June/July (70%); in the alternative scenario, we assume it will reopen in September/October (30%). Both scenarios imply that the Strait will remain closed for at least the next month, which not only constrains oil supply but also raises the probability of attacks on oil infrastructure across the Middle East. Even once the Strait reopens, the process is likely to be gradual and accompanied by elevated geopolitical risk, with significant uncertainty around how durable any deal proves to be and how secure the passage actually will be.

In our baseline scenario, WTI in Q2 2026 ranges from USD 90 to USD 130. The lower bound could be reached should the Strait of Hormuz partially reopen by the beginning of June following a possible successful negotiation and signing of a memorandum of understanding between the U.S. and Iran. However, if the Strait remains closed in June and into July, oil could hit USD 130 by the end of Q2, following two additional months of supply disruptions. In the alternative scenario, given the lack of progress and the failure to reopen the Strait, we anticipate prices would surge to the USD 120 – 140 range.

The scenarios continue diverging in the coming quarters. In the baseline scenario, prices ease in Q3 2026 averaging USD 80-100, whereas in the alternative scenario WTI sustains an average of USD 160-190. By Q4 2026, the baseline case is already two quarters into post-reopening convergence dynamics, while the alternative case is only entering its first, which supports the view of USD 80-90 by year-end in the baseline scenario and USD 120-140 in the alternative scenario.

The Q3 2026 divergence reflects differences in supply availability. In the baseline case, the Strait is partially open in June/July, allowing the market to price normalisation in progress rather than crisis ongoing. In the alternative case, the Strait remains closed through July and into September/October. The incremental damage to inventories under the alternative over baseline scenario explains part of the Q3 price premium, alongside risk premium expansion: each additional month of closure compounds market uncertainty around the timing of the reopening, infrastructure attack risk, and the durability of any eventual resolution, with reserve releases simultaneously approaching the limits of politically sustainable drawdown.

The draw rate from the March level of 6.6 mb/d moderates, however, because three mechanisms compress it. First, there is a price ceiling effect: higher prices destroy discretionary demand non-linearly through aviation cuts, industrial curtailment, and government rationing. Second, physical limits: by late Q3, some non-Gulf refineries approach minimum operating levels and cut runs, which itself reduces product demand. Third, political pressure: as high prices and economic damage drag on, governments on both sides face mounting pressure to negotiate a way out, which is why the alternative scenario assumes a September/October reopening.

Once the Strait reopens with reasonable normality, supply would likely run ahead of demand on several fronts. OPEC+ converts its approximately 600 kb/d of paper quota increases into physical barrels, backed by significant additional spare capacity in Saudi Arabia and the, now independent, UAE (now operating independently of OPEC; non-OPEC production continues expanding, notably in the U.S., Guyana, and Brazil; and the 120 mb of stranded Gulf inventory built up during the closure releases gradually into the market over 3-4 months post-reopening, adding 1-2 mb/d on top of resumed Gulf exports. Although both OPEC+ quotas and inventory build ups in the Gulf could expand in the coming months. On the demand side, the cyclical destruction caused by the conflict will reverse, but against a structurally weaker demand backdrop.

The net effect is a market with expanding supply meeting recovering but structurally weaker demand, pushing prices toward the USD 75 convergence. This level comes from three factors: the U.S. shale new-well breakeven (around USD 60-65 per barrel per the Q1 2026 Dallas Fed Energy Survey, with large producers at USD 59 and the average across all firms at USD 65), the 2025 average WTI of USD 65 (a useful reference for the pre-war equilibrium), and a residual geopolitical risk premium of USD 10-15 reflecting that markets will continue to price in some probability of recurring Hormuz disruption.

The same holds true for Urea Nitrogen fertilizers, though grain prices are up a lot less than during the Ukraine war, when both fertilizer and grain supply were impacted. Finally, natural gas prices have fallen back from the highs, as China has switched from LNG to coal-fired power stations. Additionally, though 20% of the global LNG pass through the Straits of Hormuz, it is only 2% of global gas consumption whereas over 15% of oil and oil products are being disrupted. Thus, we think natural gas prices are unlikely to spike by the same magnitude as oil prices under the alternative scenario.