View:

July 31, 2026

Preview: Due August 17 - Canada July CPI - Slightly firmer on energy but with stable core rates

July 31, 2026 7:03 PM UTC

We expect July Canadian CPI to correct higher to 2.9% yr/yr from June’s 2.8% which slipped significantly from May’s 3.2%, on a modest increase in gasoline prices after a sharp fall in June. However, we expect the Bank of Canada’s core rates to be unchanged from June, with CPI-Median at 1.9%, C

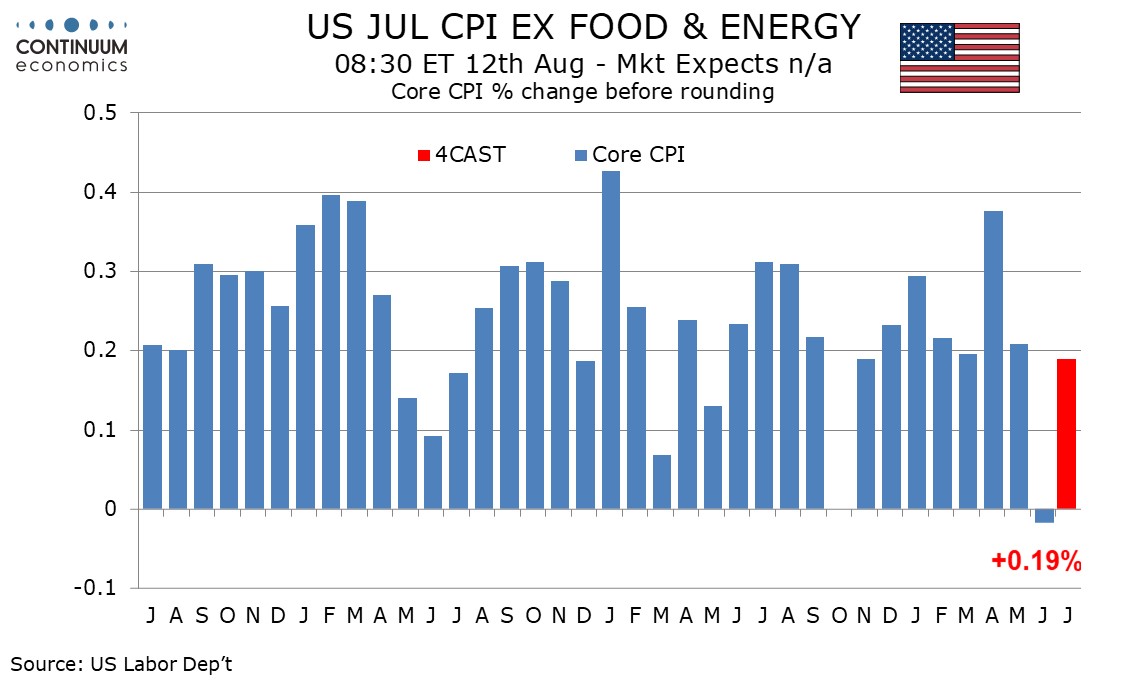

Preview: Due August 12 - U.S. July CPI - Another subdued month, if less so than June

July 31, 2026 3:52 PM UTC

We expect a subdued July CPI, up by 0.1% overall and 0.2% ex food and energy, with the respective gains before rounding being only 0.06% and 0.19%. This will however be less weak than June’s 0.4% decline overall, with the June core rate ex food and energy having been unchanged.

Preview: Due August 12 - U.S. July CPI - Another subdued month, if less so than June

July 31, 2026 3:51 PM UTC

We expect a subdued July CPI, up by 0.1% overall and 0.2% ex food and energy, with the respective gains before rounding being only 0.06% and 0.19%. This will however be less weak than June’s 0.4% decline overall, with the June core rate ex food and energy having been unchanged.

Canada May GDP - Set for a healthy Q2

July 31, 2026 1:07 PM UTC

May Canadian GDP data clearly shows an economy returning to growth in Q2. The 0.3% increase was stronger than a 0.2% consensus and a 0.1% preliminary estimate made with April’s data. April was revised higher to a 0.6% rise from 0.5% and the preliminary estimate for June is a respectable gain of 0.

EZ CPI: Boosted by Energy Prices

July 31, 2026 9:19 AM UTC

• The July provisional CPI provided no major surprise with the headline 2.9% Yr/Yr figure boosted by energy prices, but core at 2.5% and CPI ex energy unchanged at 2.2% Yr/Yr. Combined with the latest negotiated wage settlement data, we see no signs of 2nd round effects. For the ECB the dat

EZ CPI and ECB Rate Prospects

July 31, 2026 9:16 AM UTC

• The July provisional CPI provided no major surprise with the headline 2.9% Yr/Yr figure boosted by energy prices, but core at 2.5% and CPI ex energy unchanged at 2.2% Yr/Yr. Combined with the latest negotiated wage settlement data, we see no signs of 2nd round effects. For the ECB the dat