Gulf Countries U.S. Investment Deals Risks

· Lower budget revenue and a multi-year hit to tourism and the Gulf role as air transit hubs, could see delays and reduction in some parts of the Gulf states USD3.4 trillion deals with the Trump administration. The economic effects on the U.S. would likely be small and the geopolitics between Trump and the Gulf states is more important.

· However, U.S. portfolio holdings by key Gulf countries are moderate, with Europe dominating but TICS data are suggesting that European investors have continued net portfolio inflows despite the 2025 reciprocal tariff tensions. However, if Trump decided to send an armada to Greenland or actually invade in the next 1-2 years, then this would stretch NATO to the core (see here re internal European tensions) but could also impact European portfolio holdings in the U.S. We have increased this to a 20% probability from 10%, given Trump’s foreign adventurism.

Could Gulf countries slow investment deals and portfolio inflows into the U.S. after the Iran war and would it matter?

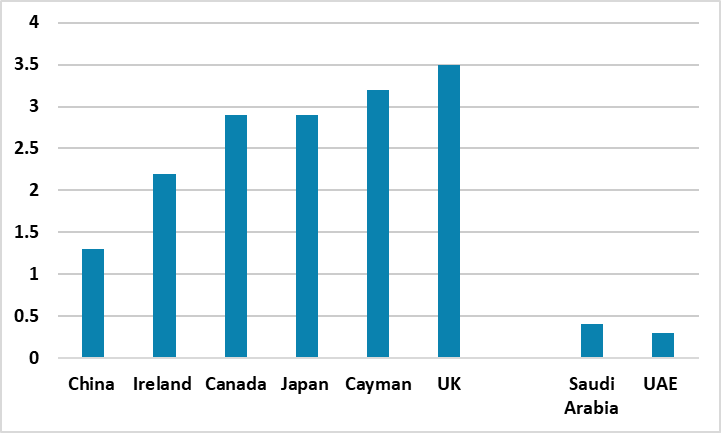

Figure 1: U.S. Portfolio Holdings by Key Countries (USD Trillions)

Source: U.S. Treasury/Continuum Economics

Iran closure of the strait of Hormuz and firing of missiles/drones at Gulf countries is a bad outcome for Gulf states. Could this slow investment/export orders from Gulf countries into the U.S. in the coming months and years?

· Collateral Damage in the Gulf. Though most analysts feel that the Iran war will be multi week rather than multi month, concerns exist within Gulf states that Iran tension could remain high after the war and a future attack on Iran by the U.S./Israel could return to hurt the region or that civil war could break out in Iran. At one level this could be financial and budgetary, as higher energy prices could be offset by lower import volumes. Secondly, it reflects current private sector concerns that Gulf tourism and air transport hubs could be impacted for years. Some reports have suggested that Gulf countries investment and export orders (e.g. aircraft) could be delayed or curtailed after the war. Finally, the Iran war derails Saudi Arabia vision that the Gulf could become a more cohesive economic region like the EU. It is also worth pointed out that the UAE is being disproportionately targeted by Iranian missiles and drones compared to Qatar and much more than Saudi Arabia.

· Trump mega Gulf deals. Trump secured USD2 trillion of deals in a May 2025 trip over the next 10 years. The USD600 billion deal including energy security, defense, AI technology, global infrastructure, aircraft and sport and critical minerals. The USD1.2 trillion Qatar deal includes defense sales, infrastructure investments, a massive aviation deal, projects in energy infrastructure, engineering and urban development and emerging technologies cooperation. It also included an extra USD200 billion from the UAE (on top of the existing USD1.4 trillion UAE deal) ranging across sectors including emerging AI technology, aerospace, energy infrastructure, and critical minerals. However, some estimates are that USD2 trillion could be USD700 billion of new deals (here), as a lot of existing deals are included in the headline figure. Trump would feel some pressure and anger, if these deals are diluted. However, Gulf diplomacy, plus Trump retaliation risks, could mean that concerns/delays are first voiced privately to the U.S. Additionally, most Gulf countries want to follow through on the bulk of plans and so it is only part that are at risk (e.g. airport hubs and tourism). It is also worth mentioning that Trump would be sensitive if the Trump organization’s plans for a Dubai tower are impact, while the UAE has also been an investor in the Trump family cryptocurrency ventures.

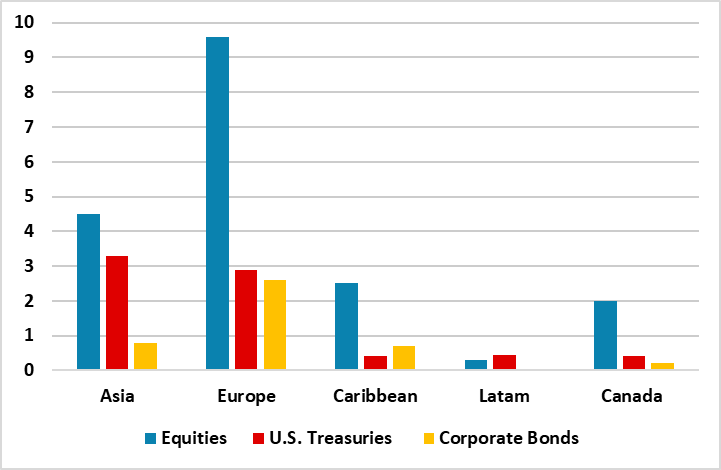

· Europe more important than Gulf for Portfolio Holdings. However, Gulf portfolio holdings are moderate and the deals are primarily focused on export orders and long-term investment. The U.S. Treasury data for direct country holdings shows only USD0.8 trillion of portfolio holdings from Saudi Arabia, the UAE (Figure 1) and Qatar. The actual holdings will likely be slightly larger, as the three countries sovereign wealth funds have USD3.6 trillion in assets and a fair portion will likely be invested in U.S. assets via European financial centers, but these sovereign wealth funds (SWFs) are also pivoting towards multi-year domestic non-oil investment. U.S. Treasury data shows that European countries are more important for overall holdings (Figure 1) and dominate for U.S. equities (Figure 2). We have noted in other articles that monthly TICS data suggests that European investors have continued net portfolio flows into the U.S., despite the reciprocal tariff debacle in 2025. However, if Trump decided to send an armada to Greenland or actually invade, then this would stretch NATO to the core (see here re internal European tensions) but could also impact European portfolio holdings in the U.S. We previously attached a 10% probability of the Trump administration invading Greenland by force, but given Trump zeal for using the U.S. military, we now raise this to a 20% probability risk.

Figure 2: Foreign Holders of Key U.S. Portfolio Assets (USD Trillions)

Source: U.S. Treasury/Continuum Economics