2yr and The Iran War

· 2yr yields can edge lower from current less elevated levels, as DM central banks continue to try to calm fears of near-term rate hikes outside of the BOJ/RBA. However, the key swing factor remains the length of the Iran war, as that will determine the trajectory of energy prices in the next 12 months. Our baseline remains for a 4-8 week war, as President Trump urgently searches for a U.S. exit from the Iran war. This would argue for a further modest decline in 2yr yields. However, we attach a 30% probability to a 2-6 month war, which could see USD150 oil prices; greater risk of 2nd round effects and real risk of ECB/BOE rate hikes -- the Fed would likely find it difficult to hike rates. This week is key, with Trump's threat of an attack on Wednesday. A major attack of all Iran power plants would see large scale retailation from Iran and likely pivot the war scanario to 2-6 months. Thus 2yr yields will likely remain choppy this month, depending on sentiment towards the war length.

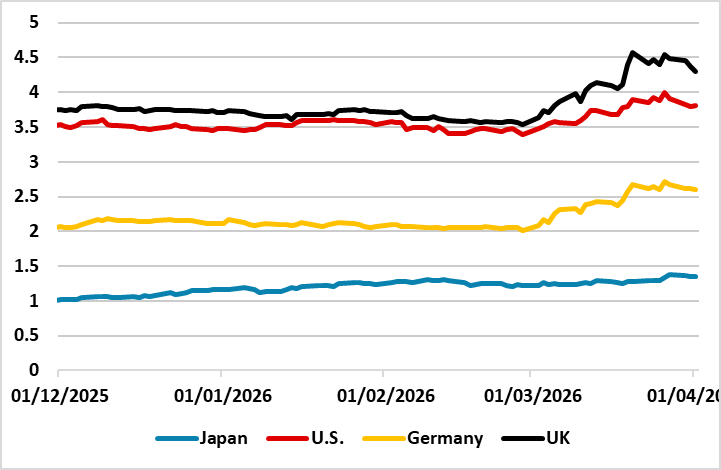

2yr DM government bond yields have surged higher on concerns over inflation induced monetary tightening with the Iran war. What happens next?

Figure 1: 2yr yields (%)

Source: Datastream/Continuum Economics

2yr yields in DM government bond markets have calmed after what appears to have been an overreaction, where a sharp jump in yields was seen with the Iran war (Figure 1). How will yields develop in the coming weeks/months?

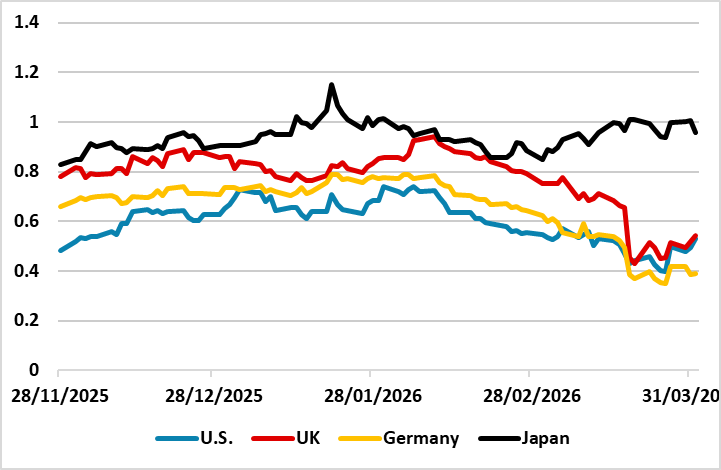

· Yield curve steepeners unwind. One of the reasons for the adjustment at the front-end, is that hedge funds and other money managers had been running long 2yr/short 10yr to play for a steeper yield curve. This is the classic play for DM government bonds when an easing cycle is underway and not yet complete. The Iran war fueled fears that rate cuts have ended and tightening could be seen instead. This amplified the initial jump in 2yr yields and prompted yield curve flattening (Figure 2) except in Japan – BOJ tightening expectations meant that the market was already biased to higher rates.

Figure 2: 10-2yr yields (%)

Source: Datastream/Continuum Economics

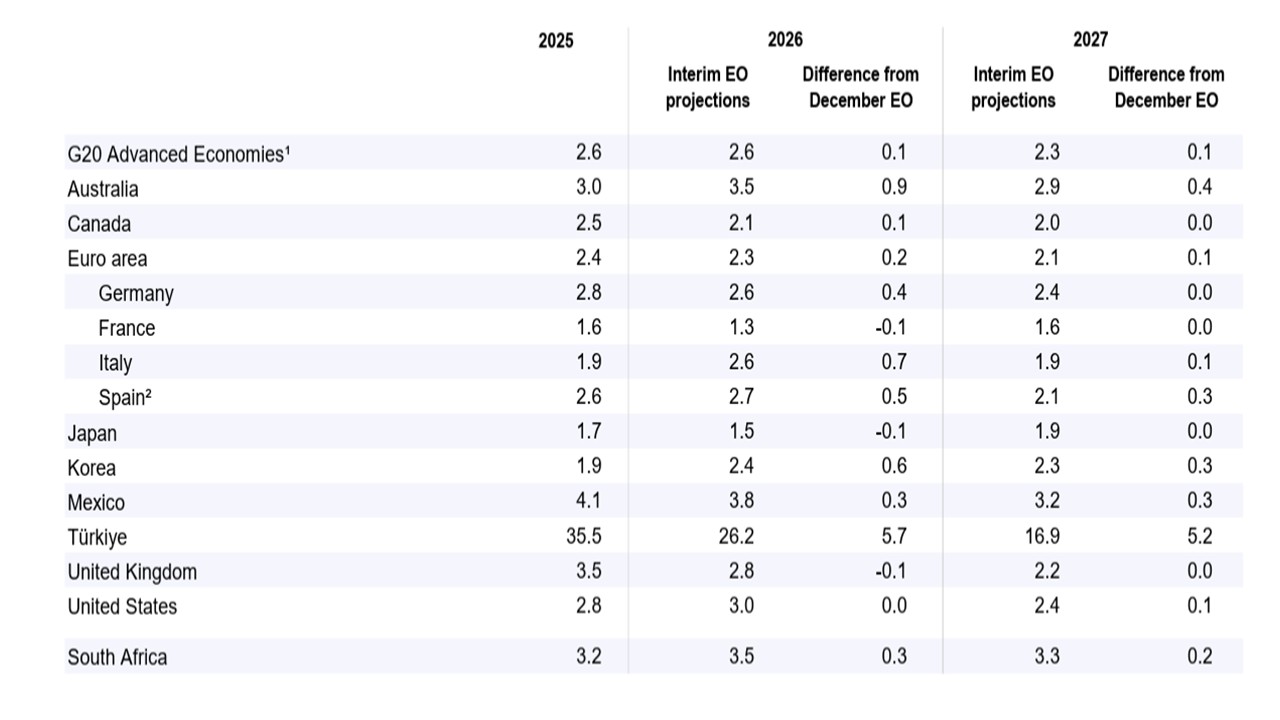

· Economists calmer than money markets. The 2nd reason that 2yr yields have started to edge down is that economists have made the argument that central bank policy needs to understand the duration of the shock and the contrasting economic conditions now versus 2022. In contrast, money markets had worried about a shock that could set off a wage-price spiral like 2022. As we detailed earlier this week (here), we see slacker labor markets/less global supply price pressures/less fiscal stimulus response and lower domestic demand than 2022. On a 4-8 week war scenario, this argues for a 1st round impact, but not 2nd round follow-through. Thus we still pencil in 50bps of cuts from the Fed before end 2026 (though this is a close call after the good March employment report (here) and 25bps cuts from the ECB and BOE, due to the softer underlying economic conditions. Other economists are putting forward similar caution, with the OECD baseline forecasts based on March 20 oil and natural gas prices showing little to modest 2nd round effects (here) and Figure 3. The caveat is if the war goes to a 2-6 month scenario, this would likely see oil prices rise to USD150. In this alternative scenario (here), the policy reaction function could see some DM countries hiking alongside BOJ/RBA and against further rate cuts.

Figure 3: Core Inflation Estimates (%)

Source: OECD (here)

· What next? The Fed on April 29/ECB on April 30/BOE on April 30 will be of great interest for further guidance on central bank thinking. By these dates it should also be clearer whether the Iran war is 4-8 weeks or moving to a more prolonged 2-6 month war. The latter can deliver further increase in oil prices, as current oil prices are being restrained by the 400mln barrels IEA release, which is unlikely to be repeated once strategic reserves are reduced. On our baseline of 4-8 weeks, we would expect caution but a further dampening down on interest rate hike fears as seen from BOE Bailey and ECB Schnabel in recent days. However, incoming data will also inform the debate, with the March U.S. CPI likely to be closely watched (here) but the March EZ CPI data (here) providing comfort that the 1st round effects in EZ this time are likely to be modest compared to 2022 – EZ natural gas prices are currently 1/6 of the Ukraine war peak. However, we attach a 30% probability to a 2-6 month war, which could see USD150 oil prices; greater risk of 2nd round effects and real risk of ECB/BOE rate hikes -- the Fed would likely find it difficult to hike rates. This week is key, with Trump's threat of an attack on Wednesday. A major attack of all Iran power plants would see large scale retailation from Iran and likely pivot the war scanario to 2-6 months. Thus 2yr yields will likely remain choppy this month, depending on sentiment towards the war length.