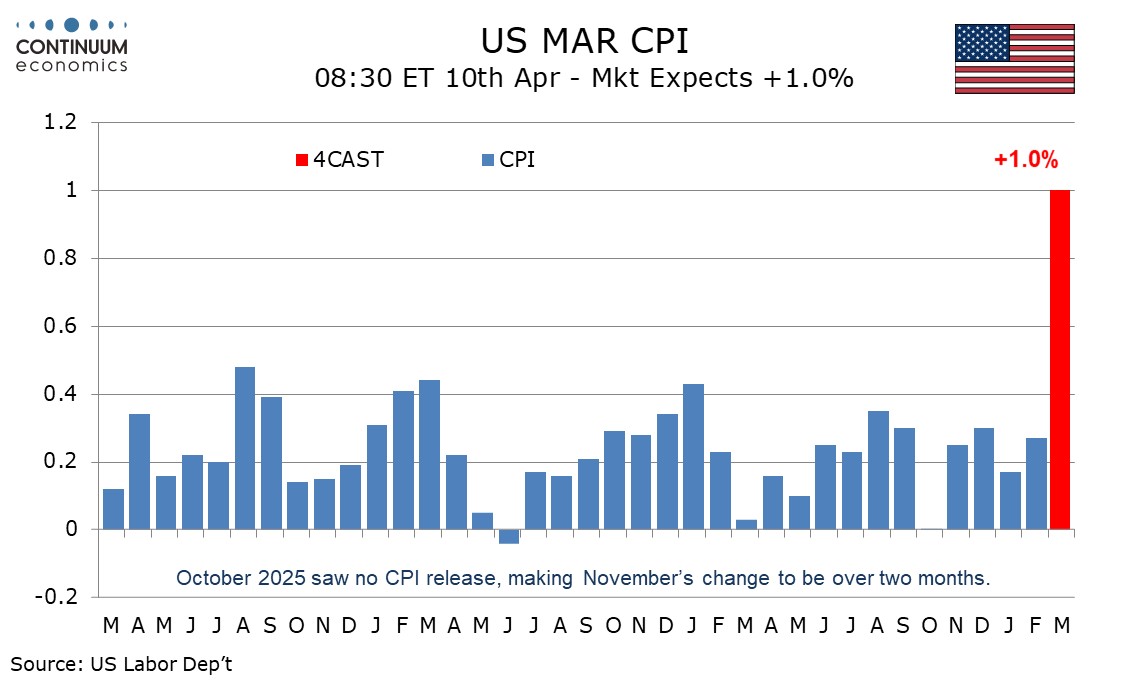

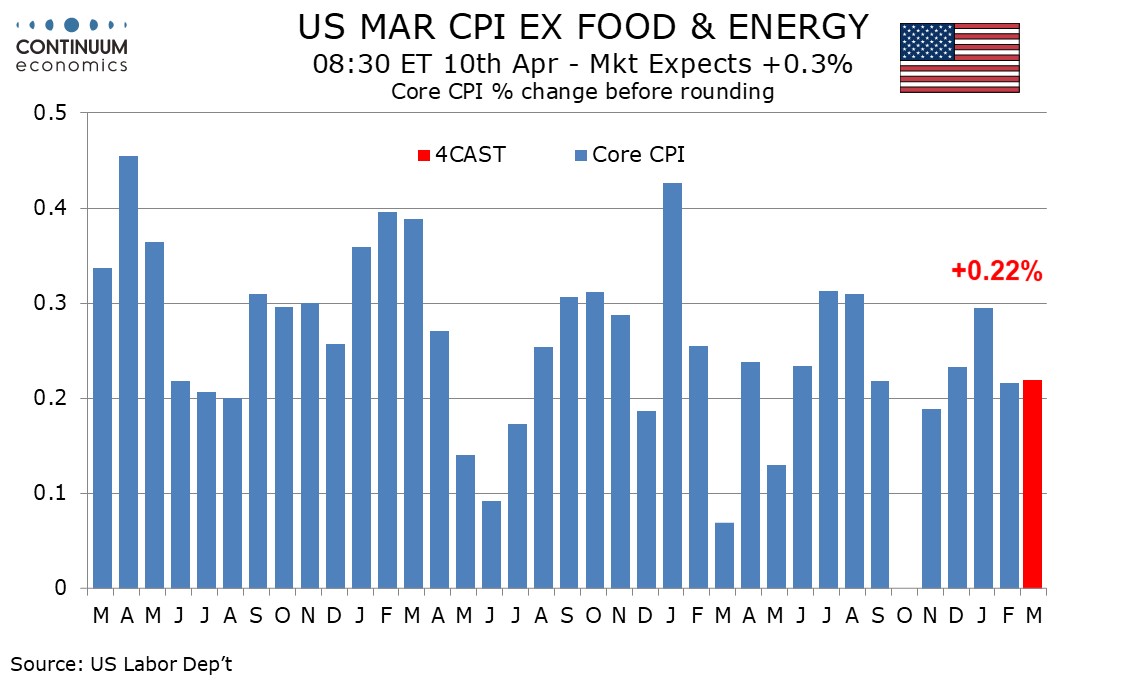

Preview: Due April 10 - U.S. March CPI - Energy to surge, but core rate seen similar to February

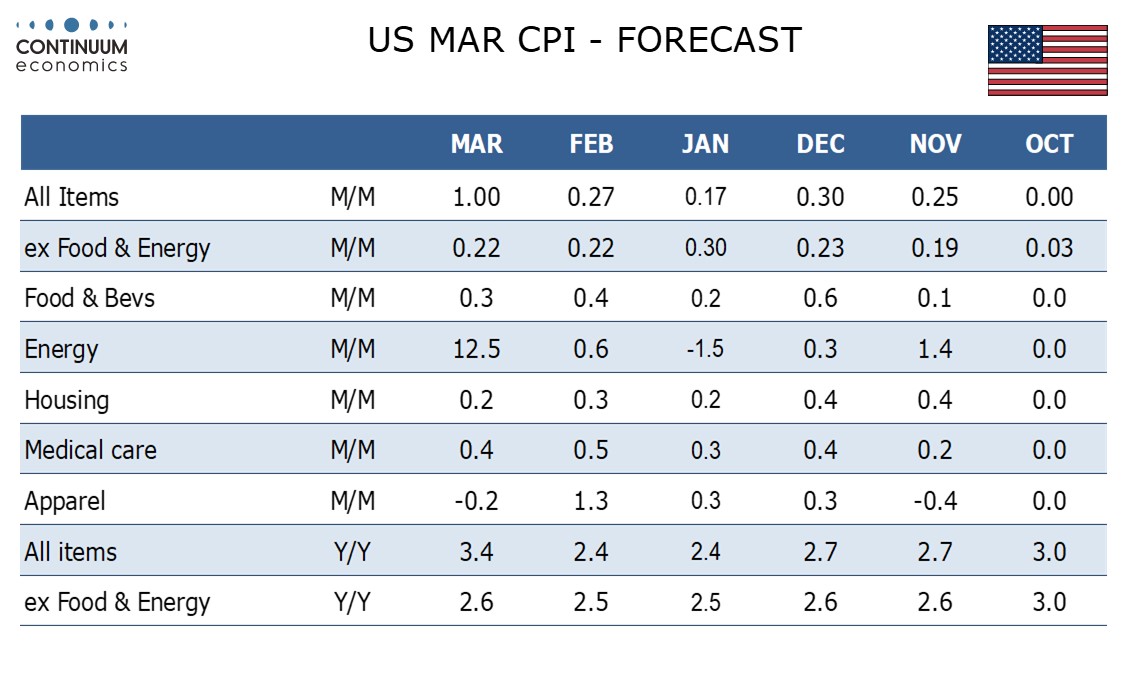

We expect March CPI to surge by 1.0% overall, which would be the strongest rise since June 2022, seen in the aftermath of the Russian invasion of Ukraine. However we expect only a moderate increase ex food and energy, of 0.22% before rounding, which would match that seen in February.

Even with some restraint from seasonal adjustments, gasoline prices look sure to see a sharp surge, which will explain nearly all of a 12.5% increase in energy, with most other components of the energy breakdown likely to seen only modest changes. We expect a moderate 0.3% increase in food, but there are upside risks going forward with the closure of the Strait of Hormuz disrupting fertilizer supplies.

Ex food and energy data has been showing a loss of momentum in recent months, with trend now looking close to 0.2% per month and even January at 0.3% not showing as strong a new year bounce as did most recent years. However PPI, some of which impacts core PCE prices, has been showing some acceleration even before the energy shock.

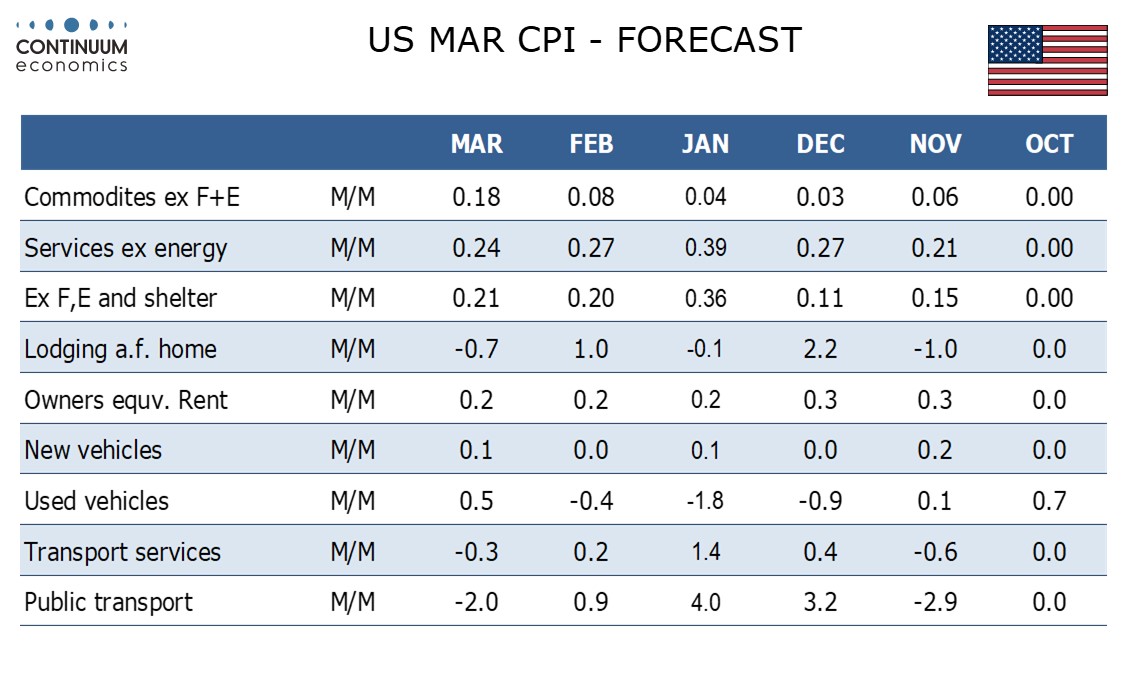

Housing inflation has been losing some momentum and March could see a further restraint from a softer month in the volatile lodging away from home subcomponent. We feel risk is on the downside on air fares with higher fuel prices likely to take time to feed through, and demand restrained by staff shortages at key airports. This should outweigh motor vehicle insurance being more stable after two straight declines.

While tariff-led inflation has probably peaked, we expect core goods to be a little firmer than in most recent months due to a correction in used autos from three straight declines, though this could be partially offset by slippage in apparel after a strong 1.3% rise in February. We expect goods less food and energy to rise by 0.18%, services less energy to rise by 0.24%, and CPI excluding food, energy and shelter to rise by 0.21%.

We expect yr/yr growth overall to jump to 3.4% from 2.4%, reaching its highest since April 2024. We expect the yr/yr pace ex food and energy to see a modest increase to 2.6% from 2.5%. March’s ex food and energy pace was the slowest since March 2021.