U.S. March Employment - Strong report suggests risks clearly higher on the inflation side

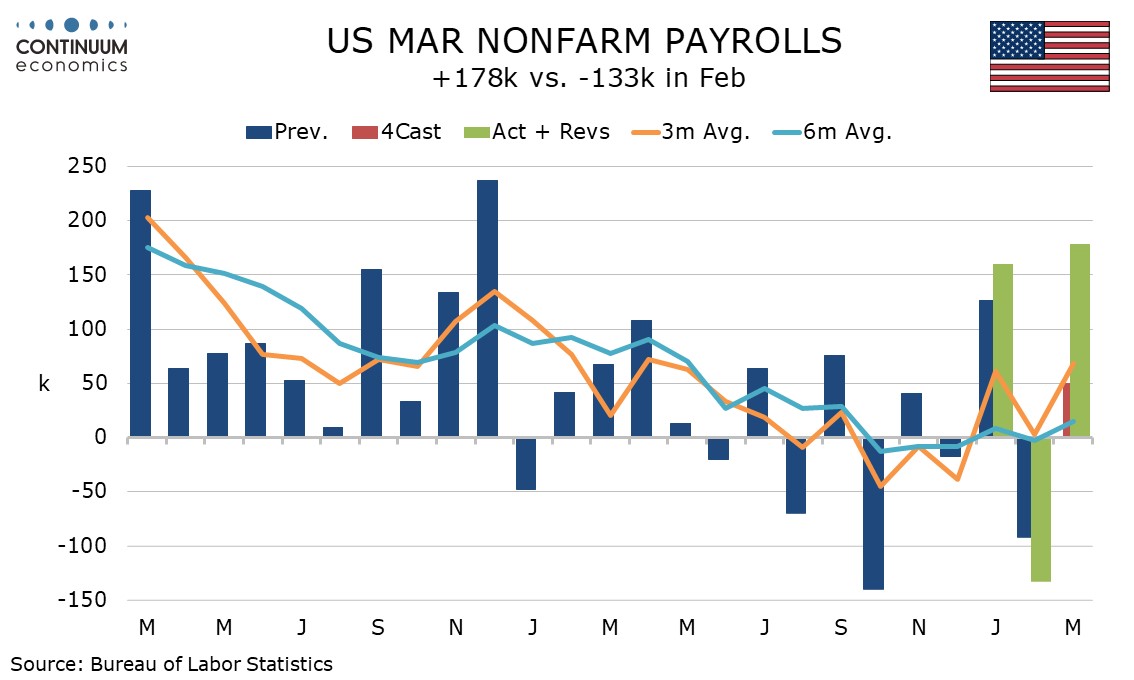

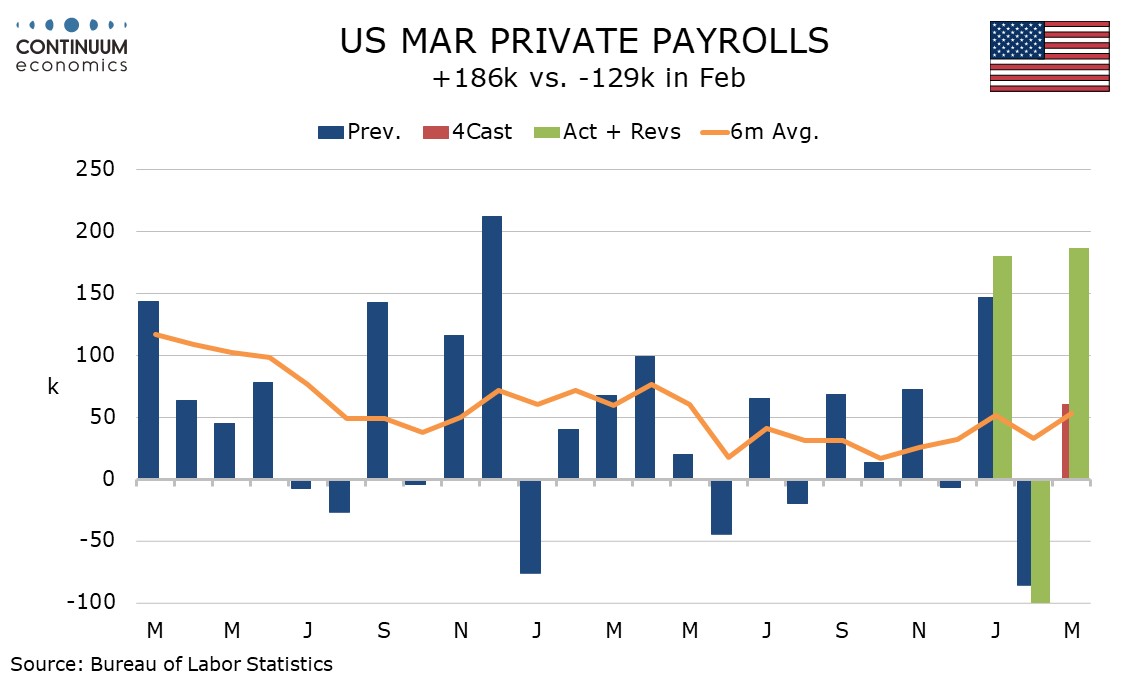

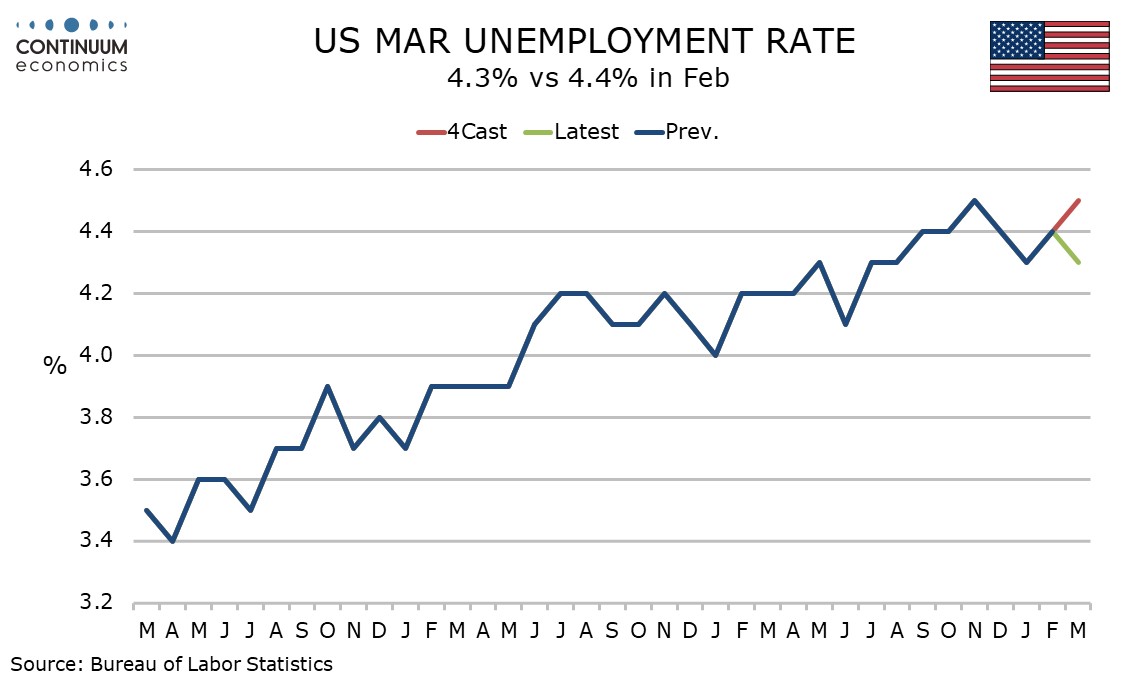

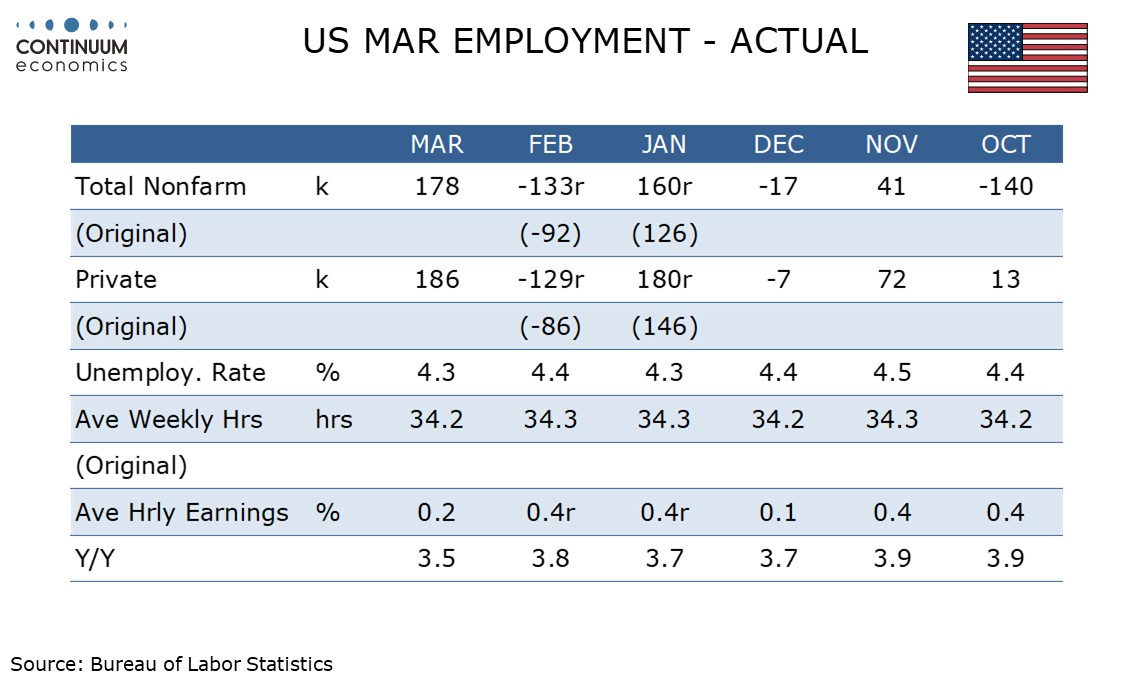

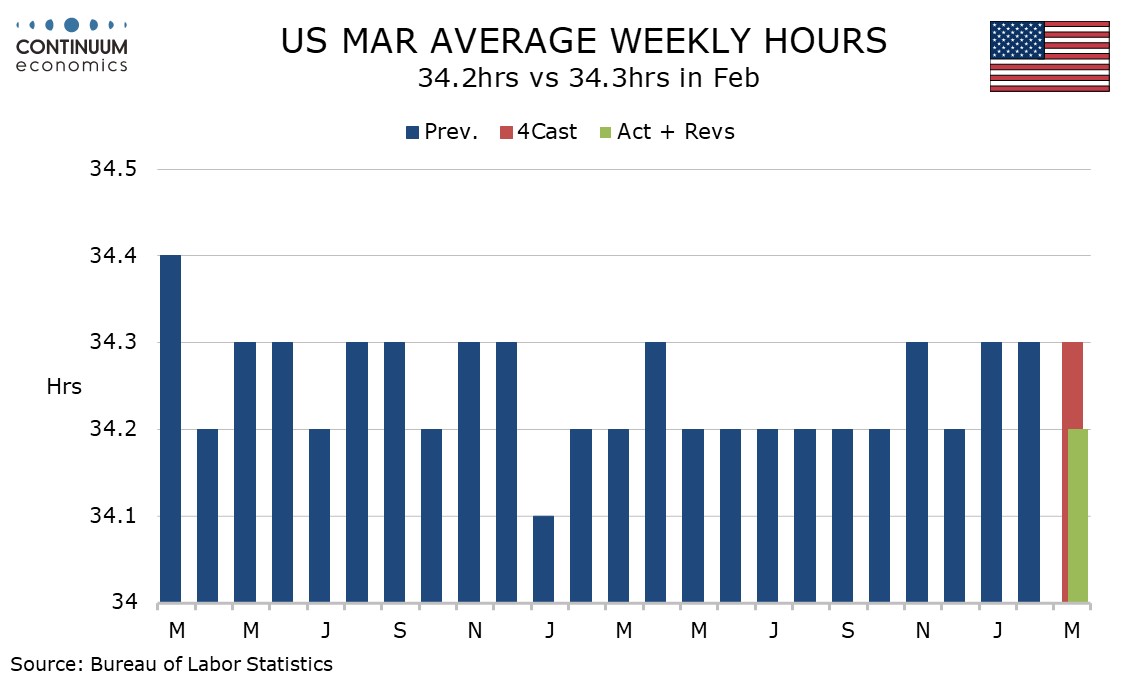

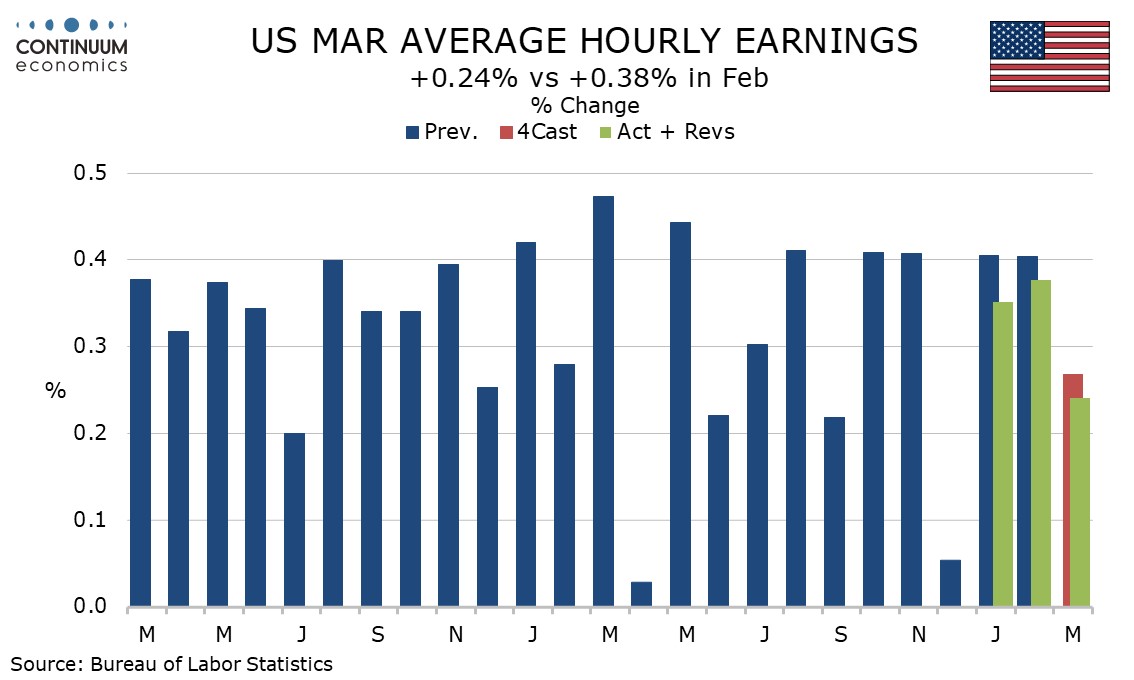

March’s non-farm payrolls is clearly on the strong side of expectations, up by 178k and an even stronger 186k in the private sector, with minimal net downward revisions of 7k. Unemployment unexpectedly fell to 4.3% from 4.4%. Less positive are a lower than expected 0.2% rise in average hourly earnings and a dip in the workweek to 34.2 from 34.3 hours, but this is clearly a positive report. The Fed will remain cautious but this data suggests that risks to the dual mandate are clearly higher on the inflation side.

Trend through 2025 showed very limited growth in payrolls, with no month showing private payrolls moving as much as 100k in either direction, with four months negative and eight positives. 2026 has shown more volatility, with private payrolls up by 180k in January, down by 129k in February and now up by 186k in March. The respective figures for overall payrolls are up 160k, down 133k and now up 178k. February’s weak month was revised lower and January’s strong month revised higher.

Some of the volatility appears weather-related, with January’s data surveyed before a cold spell which may have depressed February, and March’s survey week having seen unusually mild weather, which may have outweighed the impact of a cold spell in late February after February’s payroll was surveyed.

The three month average for overall payrolls at 68k is still quite modest but the highest since April 2025. The three month private sector average of 79k is however still below January’s. The six month average for overall payrolls at 15k is still restrained by heavy government layoffs in October but the private sector six month average of 52.5k is the highest since May 2025, if still quite subdued.

Job growth is still modest, but given weak immigration appears to be strong enough to stabilize the labor market. The unemployment rate slipped to 4.3% from 4.4% and has not changed much since the summer. The details of the household survey are however weak, the unemployment dip coming from a 396k fall in the labor force. The household survey’s estimate of employment is for a 64k decline, significantly weaker than the payroll.

Health care remains the strongest component in the payroll detail, up by 90k and that includes 31k returning strikers who caused a rare decline of 28k in February. Gains of 26k in construction and 44k in leisure and hospitality cam be seen as weather-sensitive after February declines which were more than fully reversed. Manufacturing was up by 15k after a 6k February decline and transport and warehousing rose by 21k, though this did not reverse a 48.5k decline seen in February.

The dip in the workweek meant that aggregate hours worked fell by 0.2% on the month, though aggregate hours worked increased by 1.0% annualized in Q1, up from 0.7% in Q4 and should allow a respectable GDP gain if productivity is positive. Construction and leisure and hospitality led the dip in aggregate hours worked, despite their positive data from employment.

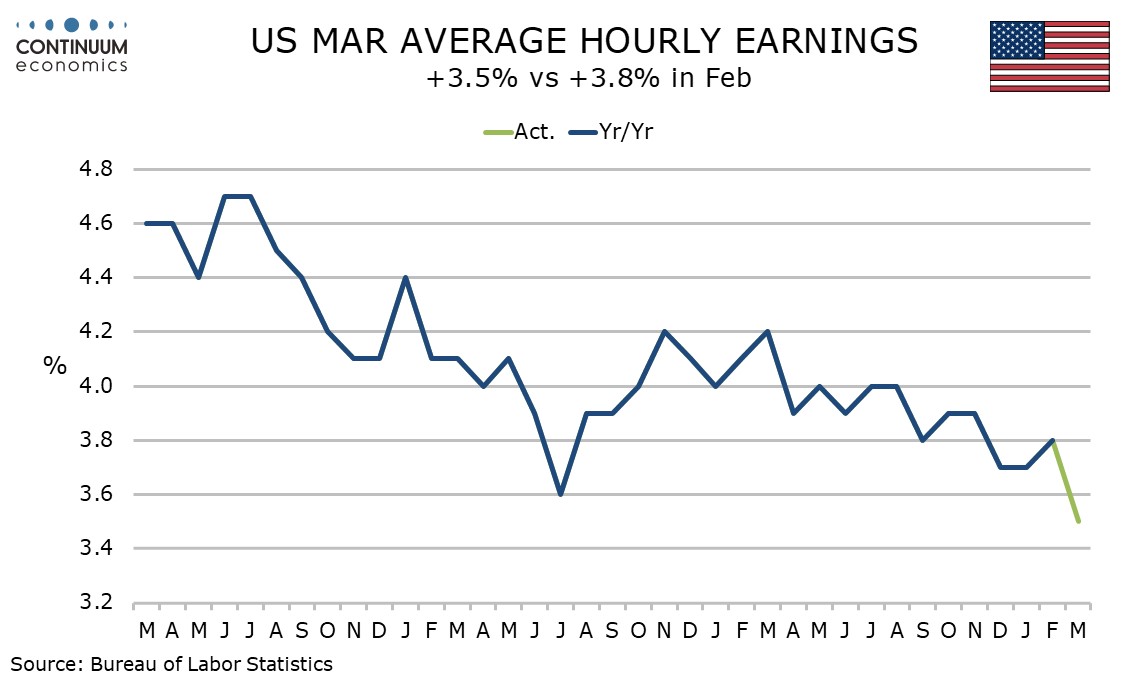

Average hourly earnings rose by 0.24% before rounding after two straight months which rose by 0.4% before rounding, which after revisions are now slightly below 0.4% before rounding rather than slightly above. Yr/yr growth of 3.5% from 3.8% is the slowest since May 2021. The Fed has reasons to be concerned about inflation, but these are not due to wage pressures.

This data suggests that going into the current oil shock, the Fed had only modest reasons for concern over labor market weakness, with risks greater on inflation, which have significantly escalated due to surging energy prices. Given high uncertainty the Fed is not going to rush into any moves, but the case for easing even if the Middle east crisis resolves has taken a hit. We are not revising our Fed call, for easings in September and December yet, with a lot still to be seen before then, but risk is increasingly on the hawkish side of our call.