Eurozone; ECB Tone More Neutral Than Suggested by March Meeting Market Reaction?

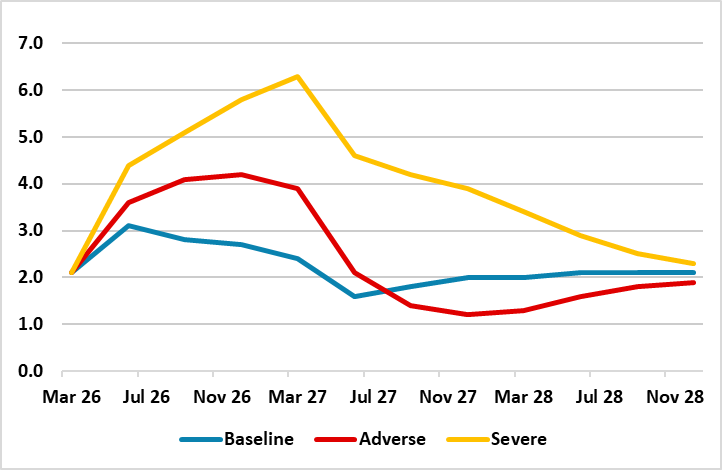

Little new can be taken from the minutes to the March ECB Council 19 meeting, save that at least to us the ECB was too optimistic about growth and too pessimistic about inflation. In regard to the latter, while acknowledging tighter financial conditions, the ECB still seemed to be downplaying what are worrying pre-war messages regarding credit (both supply and demands) evident in both survey and official monetary data which we think cannot be attributed to increasing non-bank financial intermediation. With much of the March meeting based around the baseline thinking, its discussions may seem even more dated given that the ECB hierarchy \re now suggesting that its more adverse scenario is more likely. If this is a pretext to press for early hiking, it is misplaced as both gas prices have fallen and are averaging below the baseline assumptions while the adverse inflation picture actually sees a persistent undershoot of target from mid-2027 onward even on stable policy (Figure 1). And taking the cue from the IMF which this week warned that central banks should resist the urge to tighten as this could damage economic output, we note just how much more modest the current demand backdrop is relative the energy shock of four years ago, especially for the consumer (Figure 2).

Figure 1: ECB Inflation Scenarios, Adverse Delivers More Persistent Inflation Undershoot than Baseline

Source; ECB, March Macro Projections - HICP % chg y/y

The minutes to the March 19 Council meeting do not provide any support the negative market reaction that followed the press conference and publication of the updated projections. Regardless, reading between the lines, it seems to be the case that the ECB is still reverberating from the 2022 energy shock and the criticism it faced of hiking too slowly. If so, the ECB is getting confused. What is notable is that this energy shock and the ECB’s positioning is very much different to that of 2022 - as the minutes largely agree! The labor market is less tight and where even the ECB minutes suggested that its wage tracker and surveys on wage expectations, both suggested that labour costs would ease further in the course of 2026; reference was also made to an empirical analysis which had found very limited pass-through from energy price shocks to wages. This shock is also occurring at a point when the EZ economy is operating with a margin of spare capacity as opposed to one reviving from a pandemic induced demand shock.

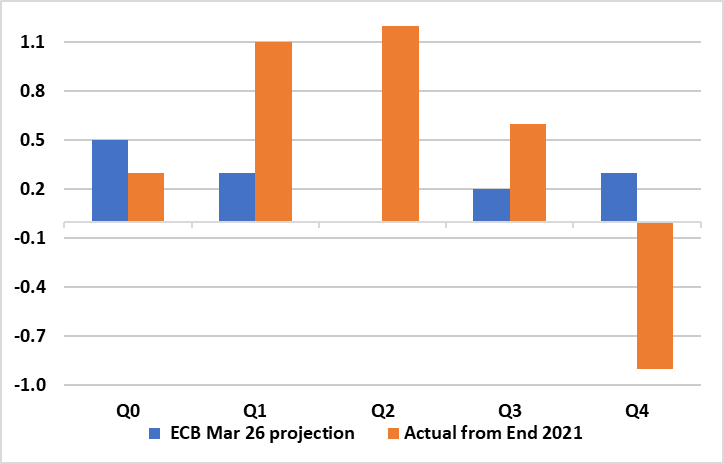

But this also reflects a clear contrast in terms of demand, particularly that of the consumer, this being vital in assessing the size and length of any impact in determining how persistent any inflation surge may be. As Figure 2 shows, even on the basis of consumer spending growing by around 1% as the ECB currently expects for the current year, this would still be far less that that seen the energy prices shock four years ago when such expenditure rose by over three times as fast. Furthermore, this time around, increases in household fuel and utility costs, and other prices, are more likely to squeeze real incomes and damage already fragile household and business confidence, further weighing on demand. These factors could widen an output gap somewhat, more than potentially constraining second-round effects as should be fact that the current main official rate is currently 2.5 ppt higher than four years ago while HICP inflation is much lower so that ‘real’ rates are very much higher!

All of which back up recent IMF comments, the latter emphasizing the downside risks to growth. And the ECB minutes did highlight such risks. As we would agree, the baseline projection for growth could still be seen as too benign, especially since the war could precipitate non-linear effects on growth. First, consumption growth was projected to be supported by a decline in the saving rate. However, in a situation of particularly high uncertainty in which households were concerned about their financial prospects, the saving rate might not fall by as much as expected. Second, business investment, and especially investment in artificial intelligence, which had been one of the most dynamic components of investment, could be highly sensitive to constraints on energy availability and to high energy prices. Third, the projection for the global growth outlook might also be too optimistic.

These are just the added considerations that the ECB will have to assess and recent comments suggest it is in no hurry to make sudden conclusions. Indeed, speaking from either side of the hawk-dove divide, Council member Schnabel suggested yesterday of no need to rush into a decision to raise rates while BoF Governors Villeroy de Galhau stressed that ‘a focus on April would be premature’.

Figure 2: Consumer Far Weaker than Four Years Ago?

Source: ECB, CE – q/q % chg in consumer spending

Admittedly, such comments have come others, including Lagarde, that its that the ECB’s more adverse scenario has become more likely than the baseline, the former having a much large spike in oil and gas prices. We would not interpret too much from this line of thinking, partly because it is not consistent with the facts given the manner in which gas prices (these vital for determining electricity pricing too) have fallen back of late. But also the adverse scenario delivers a slight more delayed but much more marled and persistent undershoot of the inflation target in the second half of the ECB forecast horizon (Figure 1) – despite not encompassing the circa 50 bp of monetary tightening in the baseline. Ironically, over the forecast horizon, the adverse scenario sees the price level some 2.5 ppt higher than otherwise but no net damage to GDP. Is this and indication of the damage that rate hikes may wreak or an indication too that its exogenous events that are determining EZ inflation, making the case for hiking even more dubious?