Eurozone: ECB Downplaying Supply of Credit as it Focuses on its Cost

Even amid increasing suggestions that the Middle East conflict will reap marked real economy damage that should limit the length and extent of any inflation surge, markets are still pricing in almost three 25 bp ECB hikes in the coming year. We think this is still very excessive and reflects an outlook that assesses policy purely in terms of the costs of credit and ignores supply. This is important as even before the conflict broke out six weeks ago, there were signs that banks were reining in the supply of credit even amid what the ECB had (probably excessively) been suggesting was an improving economic backdrop. The next ECB Bank Lending Survey (due two days before the Apr 30 Council meeting will be important in this regard and if the energy shock of four years ago is anything to go by, banks are likely to signal an increased reluctance to lend, especially without collateral backing. This is likely both to reflect and accentuate the weak real economy outlook we were fearing even before the current conflict. As a result, we still see the next ECB move being a token cut later this year.

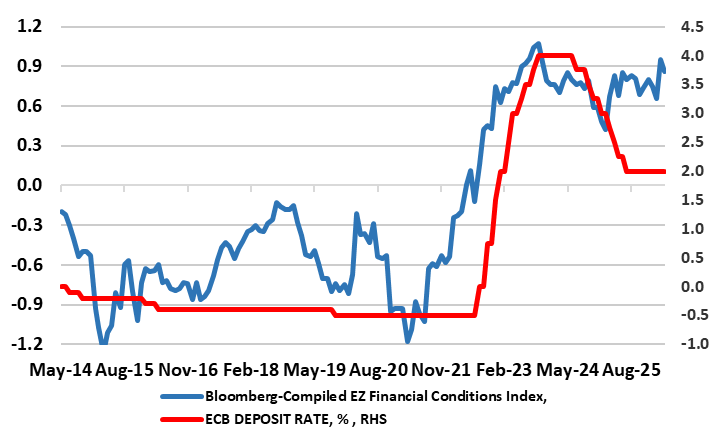

Figure 1: Tighter Financial Condition Despite Lower Policy Rate

Source: Bloomberg, ECB

As we have argued repeatedly, any official policy rate represents only part of the monetary stance. Instead, any monetary policy transmission mechanism depends on a broader set of financing conditions – including the cost and availability of bank credit, and prices in a range of asset markets. Indeed, ECB Chief Economist Lane has cited at least nine factors that would need to be assessed towards creating a summary policy stance index. One gauge widely favoured is a financial conditions index that incorporates a range of asset prices including exchange rates, short and long terms interest rates, equity prices and spreads, usually for corporates rather than sovereign. As Figure 1 shows, a Bloomberg compiled financial conditions index is telling a different story about the stance of ECB policy, instead suggesting that in spite of stable official rates the overall monetary stance has been getting tighter and not just since the outbreak of the Iran conflict.

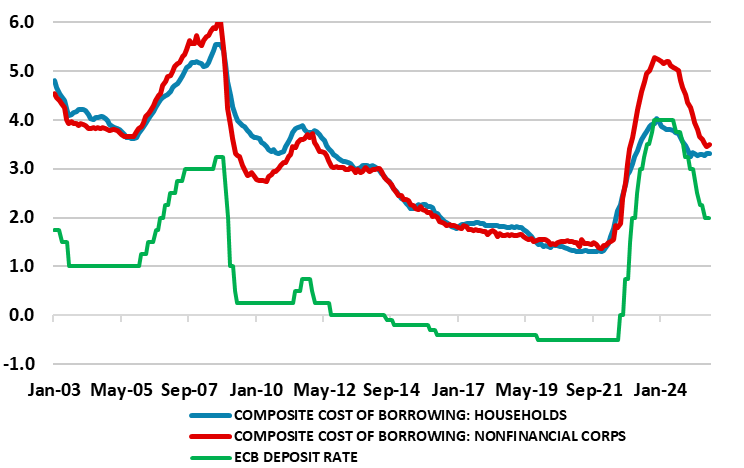

And this assumes that changes in policy rates are fully passed on by banks to borrowers, something that does not seem to have been the case during the most recent easing cycle (Figure 2). Indeed, while the ECB discount rate (now down to 2%) is some 2 ppt below the peak last seen in mid-2024, the effective cost of borrowing for firms has fallen by only 1.5 ppt while that for household by a puny 40 bp!

Figure 2: Actual Borrowing Cost Down Far Less Than Lower Policy Rate

Source: ECB, %

This is all the more notable because (and as suggested above) assessing the policy stance and the monetary transmission mechanism includes not just the cost of credit buts its availability or supply. Sure, aggregates such as financial conditions indices will partly reflect credit supply but not to the full extent that a credit market such as that of the EZ. Indeed, in the EZ, banks provide some 70% of credit demanded – unlike the likes of the U.S. where banks provide less than half that.

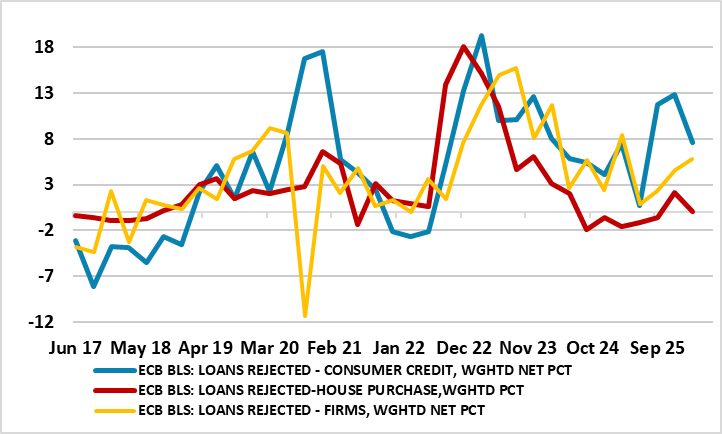

Moreover, there are clearer signs from various surveys and official monetary data that suggest a clearer wariness from banks have about the recent, current and projected economic outlook even before the latest conflict broke out. Indeed, the (last) Bank Lending Survey (BLS) published three months ago, saw EZ banks report a clear net tightening of credit standards (banks’ internal guidelines for loan approval criteria) for loans or credit lines to enterprises in last quarter. Moreover, banks reported only a small net easing of credit standards for loans to households for house purchase (net percentage of -2%), whereas credit standards for consumer credit and other lending to households tightened further. Notably, for firms, this additional credit tightening surpassed the expectations reported by banks in the previous survey round and, according to the BLS, reflected ‘ongoing and perhaps deeper concerns about the outlook for firms and the broader economy, as well as banks’ lower risk tolerance’ the former probably accentuated by tariff-induced trade concerns given that export orientated companies were the focus of bank’s worries. But more troubling still, banks reported a further net increase in the share of rejected loan applications across all loan categories, particularly for firms and consumer credit. Furthermore, the extent of rejected loans was well above recent and pre-pandemic averages (Figure 3).

Figure 3: Loan Rejection Rates Rising and Above Long-Term Averages

Source: ECB

From the ECB perspective, as seen at January’s Council meeting, these developments were seen as surprising given the ongoing gradual recovery in the economy and its greater than expected resilience. The Council back in January admitted that the tightening of credit standards had been driven by perceived risks to the economic outlook and banks’ lower risk tolerance, indicating that they were showing signs of greater risk aversion, which was leading them to become more cautious in their lending. It was suggested that higher uncertainty – possibly linked to geopolitical risks – may have increased the risk perceptions of banks. The tightening could also indicate that banks had doubts about the solvency of some non-financial corporations and saw risks of rising non-performing loans. At the same time, the Council argued that the tightening of credit standards in the bank lending survey and the Survey on the Access to Finance of Enterprises should not be over interpreted.

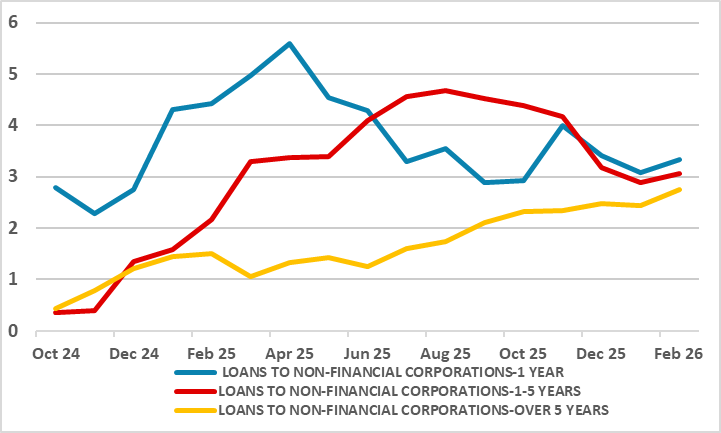

This is complacency, not least as a clear aspect of recent lending trends is that banks seem much more reluctant to lend without collateral – all the more understandable given wide-ranging and extensive uncertainty. As seen in Figure 3, the largest percentage of rejected loans is for consumer credit, ie lending without the kind of collateral that lending for house purchase involves. The less marked, but still clear rise, in rejection rates for company lending does not give a break down, but actual lending data reveals a clear picture. Unsurprisingly, and even in normal times, let alone the uncertain backdrop at present, banks almost always demand collateral for longer-term bank loans to firms (typically over three years). As the latter carry higher risk due to the extended repayment period, lenders require collateral—such as real estate, machinery, or inventory—to secure their investment and reduce risk. In this regard, amid what has been a clear slowing in overall non-financial company credit growth, this has occurred as longer term lending (ie over years but which requires collateral) has picked up, while that for shorter term lending (most notably less than one year has slowed sharply (Figure 4).

Figure 4: Contrasting Trends in Company Credit Growth Reflect Collateral?

Source: ECB, % chg y/y

The account of the March 19 ECB Council meeting is due on Apr 16 and it will be interesting to see the extent that the issues and trends discussed above were addressed by the members, let alone the extent to which the fall-out from the conflict may amplify and extend them. Very probably but maybe more implicitly the Council may decide to wait for the next BLS update due for publication two days before the Apr 30 ECB meeting, especially as it is likely to have been polled through March and thus will reveal the early reaction by borrowers and banks to the real activity damage and inflation rise that the conflict has already wrought.

Recently we have stressed how different the current energy price shock is to that of the Ukraine War breakout four years ago, very much in terms of the relative policy stance, labor market backdrops and even the extent to excess demand has varied. But as far as banks are concerned, we think the reaction that will be revealed later this month will be similar to that of four years ago and which led to the marked increase in credit standards and rejection s rates (Figure 3 again) albeit with a subtle and important difference being that the latter have already been on the rise for the last few quarters. While ECB hawks may focus on stemming second round price effects by flagging or even demanding higher policy rates they are ignoring that that the cost of credit is already rising (as financial conditions tighten) while credit supply is being reined in by bank wariness.