Markets and the Iran War

• The Trump administration’s objective appears to be pivoting from regime change to hurting Iran ballistic missile capabilities, which argues for a 2-4 week war rather than a prolonged war. However, the most intense missile battles will likely occur in the next one week and markets are hyper sensitive to oil or gas production or export facilities being hit and how long they will stop production/exports. Uncertainty also exists whether enough Gulf countries interceptor missiles exist for Iran drones. Risk off has not finished yet.

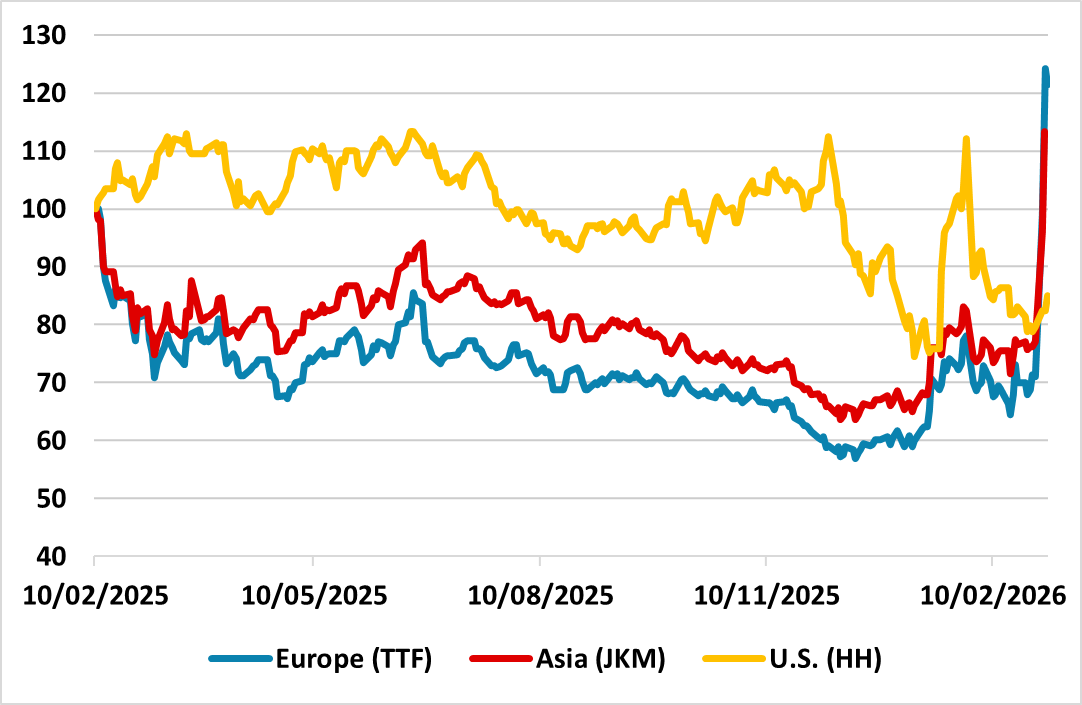

Financial markets have seen an initial reaction to the Iran war, but what happens next? Figure 1: Global Gas Prices (Feb 2025 = 100)  Source: Bloomberg/Continuum Economics

Source: Bloomberg/Continuum Economics

The bounce in oil/gas prices, selloff in equities and bounce in the USD were to be expected on a risk off event of the scale of the Iran war, but government bonds have also sold off on inflation concerns. What next for financial markets?

• Length of War and Oil/Gas Damage. The economic impact for the global economy depends both on the length of the war (plus associated effective closure of straits of Hormoz) and any lasting damage to oil/gas production and export facilities. The Trump administration’s objective appears to be pivoting from regime change to hurting Iran ballistic missile capabilities and doing a deal with a transformed regime, which argues for a 2-4 week war rather than a prolonged war. Trump offer of U.S. backed reasonable tanker insurance and navel escorts through the straits of Hormuz suggest some economic pain is starting to impact the Trump administration. However, the most intense missile battles will likely occur in the next one week between Iran and Israel/U.S. and Gulf countries and markets are hyper sensitive to production or export facilities being hit and how long they will stop production/exports. More focus exists currently on Qatar LNG production stoppage, that has caused a much more significant jump in gas than oil prices. More oil or gas production damage could accelerate the equity market selloff. Meanwhile, the inflation pain is more directed towards Europe and Asia currently (Figure 1), as the U.S. is self-sufficient in gas production and the rise in Henry Hub gas prices has been much less. The added uncertainty is that though Iran missiles may only last another week, the less lethal drone stockpile could be larger and outlive Gulf countries interceptor missile defences. Risk off has not finished yet.

• U.S. Voters and gasoline prices/stock market. Trump is sensitive to voters cost of living concerns, which is dependent on gasoline prices and so Tuesday’s new oil price surge will likely be causing nerves in the White House. Additionally, a selloff in U.S. equities and rise in government bond yields prompted Trump to soften the reciprocal tariffs last April. If the U.S. equity correction deepens, then it could prompt a change of tactics from Trump – though further rises in U.S. government bond yields may not last if Friday March 6 U.S. employment report is weak.

• Front end curves and safe havens. The initial reaction has been a parallel shift upwards in yield curve on fears that the inflation shock could have some 2nd round effects and mean that DM central banks (Fed and BOE) cannot cut interest rates in the coming months and that easing over the next 12 months could be smaller. However, central banks are likely to look through the increase in oil and gas prices on the view that they will be temporary and with only modest economic momentum argues against the idea of rate hikes (except those already planned in Japan and Australia). This could mean that the front-end of some DM curves attract interest in U.S./UK, especially if remaining Iran officials were to become open to the idea of restarting talks with the U.S. (the shift of view could come as early as next week, when Iran missile stocks become low and though of survival prompt regime transformation). Other traditional safe havens have been mixed with gold in favour, but the Japanese Yen out of fashion. However, the JPY has become so undervalued, that a snap higher could be seen on a worsening of the Iran war and hints that the worst could be over.