EZ HICP Preview (Apr 30): Headline Surges Again as Core Stabilises?

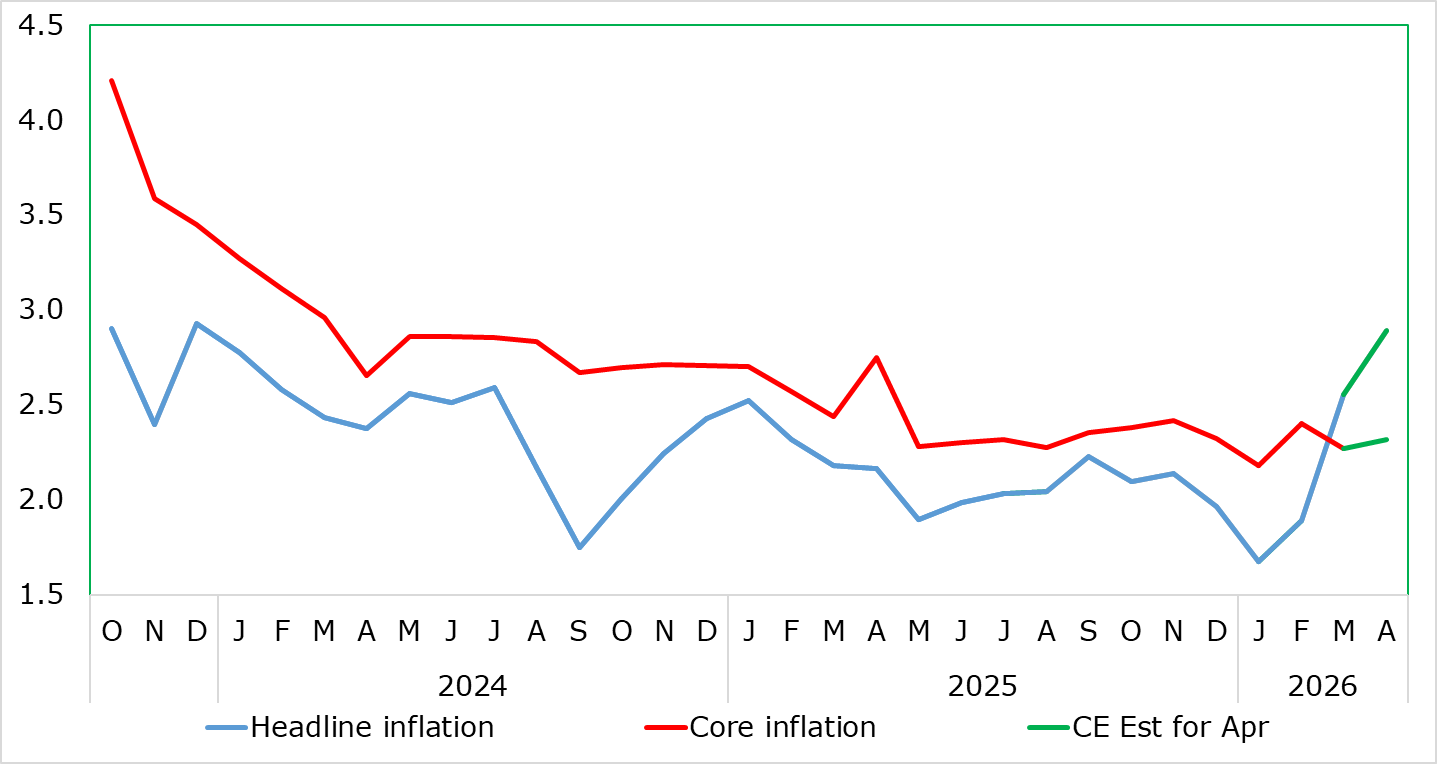

The first of the Iran War induced rise in prices arrived with the final March HICP data in line with expectations, as the headline rate spiked higher to 2.6% from February’s 1.9%, but with the core rate falling back (Figure 1) underscoring that this March surge was purely energy-led. Indeed, this March data suggested benign price pressures outside of energy, albeit with more energy price rises yet to come. Indeed, the latter should be evident in the April flash HICP which we see (at this juncture) up to 2.9%/3.0% but with upside risks should the recent fall in wholesale energy costs not feed through somewhat into retailing prices (Figure 2). But on the basis that this does occur, and with us seeing more real economy and labor market damage, which together with tight(er) financial conditions we do not see the HICP rising as much as the ECB envisages beyond this quarter but we do concur that the headline may be back below target by mid-2027.

Figure 1: Headline Sharply Higher Again But Core Stable?

Source: Eurostat, CE

Thus we still see the peak in HICP inflation at around the 3% we averaging through the current quarter. We accept risks not least stemming from our assumption of the Iran conflict not lasting more than eight weeks, with perhaps the extent and form of any end to hostilities being the key conundrum. While tilted to the upside, this produces risks on both sides but those possibly precipitating second-round effects, we note the marked contrast in the labor market and consumer perceptions compared to the inflation surge that followed the invasion of Ukraine four years ago.

Of course, the Middle East conflict is changing what has been a clear disinflationary outlook that seemingly persisted into March outside of energy. Given volatility in energy prices and uncertainty about conflict goals and timing, projecting the EZ outlook at this juncture is fraught with risks greater than usual.

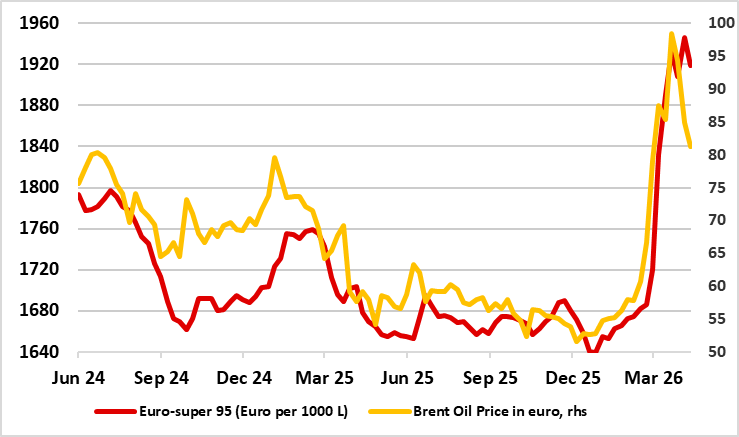

Figure 2: Fuel Prices Falling – More Wholesale Than Retail Though

Source: European Commission,

The more vocal hawks at the ECB remain focused on seemingly still apparent resilient services inflation but now are allowing the energy price surge to perturb them further. Of course, the ECB is still reverberating from the energy-induced surge in inflation that ensued from the pandemic and then the Ukraine War and the criticism levied at it about being slow to react. But perspective is needed as it is important to stress that the EZ economy is better positioned to absorb shocks, with the current situation very different from that of Feb 2022 and the Ukraine War in which in losing access to Russian gas was a ‘shock’ super-imposed on an EZ economy where demand was recovering from the pandemic the latter having caused clear shortages.

Admittedly, a further rise in cost pressures is already emerging given what is happening to retail fuel prices so even into this month - in some cases seemingly rising much more than perhaps the wholesale price would suggest – more fuel price data arrive every Thursday from the European Commission. But both retail and particularly wholesale prices have started to fall (Figure 2), more notably for gas than oil regarding the former, suggesting that upside risks to inflation may now stem more from any second-round effects that purely from energy. As for any spill-over effects this month, we think the April core rate will remain at the 2.3% rate set in March, tempered by the impact of the early Easter both on services prices and that for food.

NB; the EZ HICP data will be preceded by national CPI/HICP data with key German data due Apr 29 and where we see a relatively larger April jump from 3.8% to 3.3%!